|

市場調查報告書

商品編碼

1906917

機器視覺系統(MVS):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Machine Vision Systems (MVS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

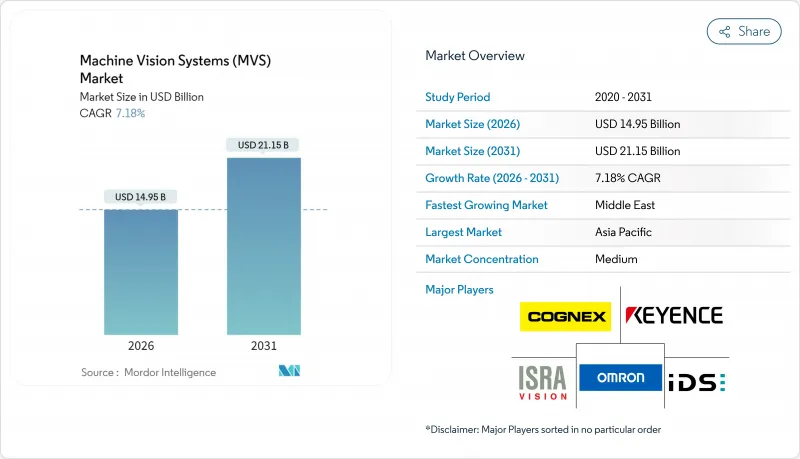

預計機器視覺系統(MVS)市場將從 2025 年的 139.5 億美元成長到 2026 年的 149.5 億美元,到 2031 年將達到 211.5 億美元,2026 年至 2031 年的複合年成長率為 7.18%。

這種加速成長反映了對零缺陷製造日益成長的需求、人工智慧與工業成像技術的融合,以及在汽車、半導體、物流和醫療等行業不斷擴展的應用場景。曾經在硬體規格上競爭的供應商,如今正透過深度學習軟體、雲端連線和訂閱定價模式來脫穎而出,企業也在尋求端到端的品質保證,以降低保固風險。儘管基於雲端的部署仍佔少數,但可擴展處理和遠端管理的優勢正迫使供應商加強其網路安全和資料管治框架。區域成長模式顯示,亞太地區保持著製造業的主導地位,中東地區正在擴大新的自動化計劃,而北美和歐洲則實施了有利於認證視覺架構的嚴格責任規則。

全球機器視覺系統(MVS)市場趨勢與洞察

對零缺陷製造的需求日益成長

在汽車電池製造和先進電子產品組裝,即使是單一缺陷也是不可接受的。因此,生產商正在放棄統計抽樣,轉而採用100%在線連續檢測。配備高光譜遙測相機的機器視覺系統(MVS)能夠以亞毫米級解析度識別材料和結構異常,從而避免代價高昂的召回和保固責任。歐盟的監管變化強化了財務責任,推動了對高解析度感測器和人工智慧分類器的投資。雲端連接的儀錶板為工廠管理人員提供即時缺陷圖,加快了根本原因調查。隨著零缺陷專案的日益成熟,提供承包分析、邊緣推理和堅固耐用的工業硬體的供應商正在機器視覺系統(MVS)市場中佔據越來越大的佔有率。

視覺引導機器人的應用日益普及

機器人搭載的攝影機引導機械手臂隨機放置零件,以實現以往由管線工人完成的揀貨、組裝和組裝任務。康耐視透過客戶案例進一步展示了生產力的提升:人工智慧視覺技術將汽車零件的換型時間從數小時縮短至數分鐘。搭載相機的邊緣處理器支援即時抓取規劃,而碰撞規避演算法則可減少廢棄物。在倉庫中,視覺引導的移動機器人正被整合到系統中,用於定位庫存和了解包裝狀況,為無人值守的履約中心奠定基礎。在勞動力持續短缺的背景下,視覺引導的機器人技術正在增加靈活的生產能力,並加速機器視覺系統 (MVS) 市場在離散製造和物流領域的成長。

熟練的機器視覺整合技術人員短缺

複雜的視覺系統實現需要光學、照明、影像處理、神經網路調優和工業網路等技術,但將這些技術作為單一學科進行教授的工程課程卻寥寥無幾。中小企業將計劃外包,而系統整合商的訂單仍排得訂單,導致前置作業時間延長,總成本上升。供應商認證計畫分散,阻礙了人才流動,並限制了新興市場的勞動力資源。實施延遲延長了投資回收期,並限制了機器視覺系統(MVS)在新興經濟體的市場滲透率,尤其是在價格敏感型應用領域。儘管產學合作旨在規範課程設置,但預計中期內供應仍將持續超過需求。

細分市場分析

到2025年,硬體仍將佔據機器視覺系統(MVS)市場60.15%的佔有率,鞏固其在工業環境影像擷取中的基礎性作用。相機、鏡頭、照明設備和影像擷取卡構成了資本密集的基礎組件,但商品化壓力和標準介面正在擠壓利潤空間。軟體將以7.42%的複合年成長率成長,透過深度學習推理、資料集管理和低程式碼應用程式建構器創造價值。斑馬技術公司的「Aurora」軟體在2024年新增了預訓練神經網路,降低了准入門檻並推動了經常性收入。原始設備製造商(OEM)正擴大將邊緣硬體與終身軟體訂閱捆綁銷售,轉向基於年金的經營模式,這正在重塑機器視覺系統市場的獲利模式。

這種轉變正雲端協作、模型版本控制和網路安全成為日益重要的企業採購標準。提供整合軟體堆疊的整合商有可能取代以硬體為中心的競爭對手,而感測器供應商則透過與人工智慧框架合作來保持競爭力。隨著終端用戶尋求全機隊分析,軟體正成為異質攝影機環境的控制基礎,加速了從銷售零件到提供功能的轉變。

到2025年,基於PC的安裝方案將佔機器視覺系統(MVS)市場規模的57.35%,因其適用於計算密集型演算法和多攝影機編配而備受青睞。然而,將光學、照明和處理能力整合到堅固耐用模組中的智慧攝影機將以7.24%的複合年成長率(CAGR)實現最快的成長。像Hailo-10H這樣的汽車邊緣加速器將變壓器網路和生成式人工智慧引入攝影機模組,從而縮小了機櫃的面積。倉庫業者正在繞過外部PC,採用即插即用的智慧攝影機進行條碼解碼、體積測量和損壞偵測。智慧攝影機供應商正在提供基於瀏覽器的配置功能,將部署時間從幾天縮短到幾小時,從而鞏固了其在整個機器視覺系統(MVS)市場小型化應用領域的領先地位。

儘管邊緣運算技術取得了長足進步,但在需要Terabyte級吞吐量的研究機構、半導體代工廠和多頻譜環境中,PC後端仍然至關重要。混合架構正在興起,智慧相機執行初步推斷,而PC則聚合更深入的分析,這表明兩者可以共存,而非完全替代。

機器視覺系統 (MVS) 報告按組件(硬體、軟體)、產品類型(基於 PC、基於智慧型相機)、成像類型(2D、3D、高光譜遙測和頻譜)、部署模式(本地部署、邊緣/嵌入式、雲端部署)、終端用戶產業(電子與半導體、食品飲料、物流與零售等)以及地區進行細分。市場預測以美元 (USD) 為以金額為準。

區域分析

到2025年,亞太地區將佔全球收入的40.25%,這主要得益於中國強大的電子組裝能力、日本的機器人技術以及韓國的儲存晶片製造工廠。區域各國政府正在資助智慧工廠升級改造,而契約製造製造商也積極採用視覺技術以滿足嚴格的出口品質標準。印度正受益於與生產連結獎勵計畫,以吸引全球行動電話和電池製造商,從而提振當地對在線連續檢測的需求。東南亞國家正在汽車線束和晶片封裝領域開拓利基市場,推動視覺技術的普及和供應商生態系統的不斷深化。

北美正利用電動車和半導體工廠的退貨政策和激勵措施。美國食品藥物管理局(FDA) 和國家公路交通安全管理局 (NHTSA) 的監管推動了對可產生審核追蹤的檢驗視覺生產線的投資。加拿大安大略省和魁北克省的先進製造群正在整合人工智慧視覺和機器人技術以填補勞動力短缺,而墨西哥的汽車產業走廊則正在部署價格適中的智慧攝影機生產線以維持原始設備製造商 (OEM) 的核准。

歐洲注重品質的中型製造商和嚴格的責任法律持續推動工業4.0技術的穩定普及。德國和義大利正在完善其工業4.0項目,融合視覺技術、機器人技術和製造執行系統(MES)。中東地區正經歷最快的複合年成長率(CAGR),達到8.22%,這主要得益於沙烏地阿拉伯和阿拉伯聯合大公國將主權財富基金投入非石油製造業,包括食品加工、消費品和可再生能源。土耳其的汽車出口和埃及的包裝工廠正在推動該地區工業4.0技術的普及。

南美洲的機器視覺系統應用與出口型農業企業和汽車生產密切相關,但宏觀經濟波動限制了其普及。非洲仍處於發展中,但南非的汽車產業中心和摩洛哥的電子組裝基地為供應商在不斷擴張的機器視覺系統(MVS)市場中站穩了腳跟。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對零缺陷製造的需求日益成長

- 擴大視覺引導機器人技術的應用

- 電子設備小型化導致對3D視覺的需求不斷成長

- 食品和藥品的嚴格品質標準

- 設備端人工智慧推理晶片的普及

- VaaS(視覺即服務)訂閱模式的興起

- 市場限制

- 熟練的機器視覺整合商短缺

- 高解析度和高光譜遙測相機的高成本

- 雲端連結視覺系統中的網路安全風險

- 影像感測器半導體供應鏈波動性

- 產業生態系分析

- 宏觀經濟因素的影響

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 視覺系統

- 相機

- 光學和照明系統

- 影像擷取卡

- 其他硬體

- 軟體

- 硬體

- 依產品類型

- 基於PC

- 智慧型攝影機底座

- 按影像類型

- 2D成像

- 3D成像

- 高光譜遙測和頻譜成像

- 透過部署模式

- 本地部署

- 邊緣/嵌入式

- 基於雲端的

- 按最終用戶行業分類

- 車

- 電子裝置和半導體

- 食品/飲料

- 醫療和藥品

- 物流與零售

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 中東

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 非洲

- 南非

- 埃及

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cognex Corporation

- Keyence Corporation

- Omron Corporation

- Teledyne Technologies Incorporated

- Sony Group Corporation

- Atlas Copco AB(ISRA Vision)

- IDS Imaging Development Systems GmbH

- National Instruments Corporation

- MVTec Software GmbH

- Basler AG

- Allied Vision Technologies GmbH

- TKH Group NV(LMI Technologies)

- FLIR Systems Inc(Teledyne)

- Intel Corporation

- Qualcomm Technologies Inc

- Sick AG

- Panasonic Holdings Corporation

- Stemmer Imaging AG

- Zebra Technologies Corporation

- Hitachi Ltd

第7章 市場機會與未來展望

The machine vision systems market is expected to grow from USD 13.95 billion in 2025 to USD 14.95 billion in 2026 and is forecast to reach USD 21.15 billion by 2031 at 7.18% CAGR over 2026-2031.

The acceleration reflects rising demand for zero-defect production, the fusion of artificial intelligence with industrial imaging, and expanding use cases across automotive, semiconductor, logistics, and healthcare operations. Vendors that once competed on hardware specifications now differentiate through deep-learning software, cloud connectivity, and subscription pricing, while enterprises pursue end-to-end quality assurance to limit warranty exposure. Cloud-based deployment, still a minority, benefits from scalable processing and remote management, pushing vendors to harden cybersecurity and data-governance frameworks. Regional growth patterns show Asia-Pacific retaining manufacturing primacy, the Middle East scaling greenfield automation projects, and North America and Europe enforcing tighter liability rules that favor certified vision architectures.

Global Machine Vision Systems (MVS) Market Trends and Insights

Rising Need for Zero-Defect Manufacturing

Automotive battery manufacturing and advanced electronics assemblies cannot tolerate single-point defects, leading producers to abandon statistical sampling in favor of 100% inline inspection. Machine vision systems equipped with hyperspectral cameras identify material or structural anomalies at sub-millimeter resolution, preventing costly recalls and warranty liabilities. Regulatory amendments in the European Union reinforce financial accountability, motivating investment in higher-resolution sensors and AI classifiers. Cloud-linked dashboards give plant managers real-time defect maps that shorten root-cause investigations. As zero-defect programs mature, vendors that deliver turnkey analytics, edge inference, and hardened industrial hardware capture incremental share within the machine vision systems market.

Increasing Adoption of Vision-Guided Robotics

Robot-mounted cameras now guide grippers through random part orientations, enabling bin-picking, kitting, and assembly tasks once reserved for line workers. Cognex reported customers trimming automotive changeover time from hours to minutes using AI-enabled vision, strengthening the productivity case. Edge processors inside the camera support real-time grasp planning, while collision-avoidance algorithms reduce scrap. Warehouses integrate vision-guided mobile robots that localize inventory and capture package condition, forming the backbone of lights-out fulfillment hubs. As labor scarcity persists, vision-guided robotics adds flexible capacity and accelerates the machine vision systems market across discrete and logistics sectors.

Lack of Skilled Machine Vision Integrators

Complex vision deployments span optics, lighting, image processing, neural-network tuning, and industrial networking, skills that engineering programs seldom teach as a single discipline. Small and medium enterprises outsource projects, yet system integrators remain over-booked, raising lead times and total cost. Vendor certification tracks are fragmented, making talent portability difficult and limiting labor pools in emerging markets. Delayed rollouts widen the return-on-investment horizon, especially for price-sensitive applications, constraining uptake of the machine vision systems market in growth economies. Academic-industry partnerships are forming to standardize curricula, but supply will lag demand through the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for 3D Vision in Electronics Miniaturization

- Stringent Quality Rules for Food and Pharmaceuticals

- High Cost of High-Resolution and Hyperspectral Cameras

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained a 60.15% machine vision systems market share in 2025, underscoring its foundational role in capturing images across industrial environments. Cameras, lenses, lighting, and frame grabbers form a capital-intensive base, but commoditization pressures and standard interfaces squeeze margins. Software, advancing at a 7.42% CAGR, captures value through deep-learning inference, dataset management, and low-code application builders. Aurora software from Zebra Technologies added ready-trained neural networks in 2024, lowering entry barriers and pushing recurring revenue. OEMs increasingly package lifetime software subscriptions with edge hardware, pivoting to an annuity model that reshapes profit pools within the machine vision systems market.

The shift elevates cloud orchestration, model versioning, and cybersecurity as corporate procurement criteria. Integrators that offer unified software stacks stand to displace hardware-centric competitors, while sensor vendors partner with AI frameworks to remain relevant. As end users pursue fleet-wide analytics, software becomes the control plane over heterogeneous camera footprints, accelerating the transition from component sales to capability delivery.

PC-based installations represented 57.35% of the machine vision systems market size in 2025, favored for compute-intensive algorithms and multi-camera orchestration. However, smart cameras, compressing optics, lighting, and processing into a rugged module, record the fastest 7.24% CAGR. Automotive-qualified edge accelerators such as Hailo-10H bring transformer networks and generative AI to the camera pod, shrinking cabinet footprints. Warehouse operators adopt plug-and-play smart cameras for barcode decoding, volumetric measurement, and damage detection, bypassing external PCs. Smart-camera vendors package browser-based configuration that cuts deployment days to hours, tightening their grip on small-form-factor applications across the machine vision systems market.

Despite edge advances, PC back-ends remain indispensable in research labs, semiconductor fabs, and multi-spectral setups requiring terabytes of throughput. Hybrid architectures emerge in which smart cameras perform preliminary inference while PCs aggregate deeper analytics, illustrating coexistence rather than outright displacement.

The Machine Vision Systems Report is Segmented by Component (Hardware, and Software), Product Type (PC-Based, and Smart Camera-Based), Imaging Type (2D, 3D, and Hyperspectral and Multispectral), Deployment Mode (On-Premise, Edge/Embedded, and Cloud-Based), End-User Industry (Electronics and Semiconductors, Food and Beverage, Logistics and Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 40.25% of 2025 revenue, anchored by China's electronics assembly capacity, Japan's robotics expertise, and South Korea's memory-chip fabs. Regional governments fund smart-factory upgrades, while contract manufacturers embed vision to meet stringent export quality criteria. India benefits from production-linked incentives that draw global handset and battery makers, boosting local demand for inline inspection. Southeast Asian nations carve out niches in automotive wiring and chip packaging, raising vision penetration and deepening supplier ecosystems.

North America leverages reshoring policies and incentives for electric-vehicle and semiconductor plants. Regulatory oversight by the U.S. FDA and NHTSA spurs investments in validated vision lines that generate audit trails. Canada's advanced-manufacturing clusters in Ontario and Quebec integrate AI vision with robotics to offset labor constraints, while Mexico's automotive corridor deploys affordable smart-camera lines to maintain OEM approvals.

Europe combines quality-obsessed midsize manufacturers with rigorous liability statutes, sustaining steady uptake. Germany and Italy refine Industrie 4.0 programs that merge vision, robotics, and MES integration. The Middle East delivers the fastest 8.22% CAGR as Saudi Arabia and United Arab Emirates channel sovereign wealth into non-oil manufacturing, including food processing, consumer goods, and renewables. Turkey's automotive exports and Egypt's packaging plants widen regional installations.

South America shows sporadic adoption tied to export agribusiness and vehicle production, though macroeconomic volatility tempers volume. Africa remains nascent, but South Africa's automotive hubs and Morocco's electronics assemblies offer footholds for suppliers in the expanding machine vision systems market.

- Cognex Corporation

- Keyence Corporation

- Omron Corporation

- Teledyne Technologies Incorporated

- Sony Group Corporation

- Atlas Copco AB (ISRA Vision)

- IDS Imaging Development Systems GmbH

- National Instruments Corporation

- MVTec Software GmbH

- Basler AG

- Allied Vision Technologies GmbH

- TKH Group NV (LMI Technologies)

- FLIR Systems Inc (Teledyne)

- Intel Corporation

- Qualcomm Technologies Inc

- Sick AG

- Panasonic Holdings Corporation

- Stemmer Imaging AG

- Zebra Technologies Corporation

- Hitachi Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Zero-Defect Manufacturing

- 4.2.2 Increasing Adoption of Vision-Guided Robotics

- 4.2.3 Growing Demand for 3D Vision in Electronics Miniaturisation

- 4.2.4 Stringent Quality Rules for Food and Pharmaceuticals

- 4.2.5 Surge in On-Device AI Inference Chips

- 4.2.6 Emergence of Vision-as-a-Service Subscription Models

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Machine Vision Integrators

- 4.3.2 High Cost of High-Resolution and Hyperspectral Cameras

- 4.3.3 Cybersecurity Risks in Cloud-Connected Vision Systems

- 4.3.4 Supply Chain Volatility of Image Sensor Semiconductors

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Vision Systems

- 5.1.1.2 Cameras

- 5.1.1.3 Optics and Illumination Systems

- 5.1.1.4 Frame Grabbers

- 5.1.1.5 Other Hardwares

- 5.1.2 Software

- 5.1.1 Hardware

- 5.2 By Product Type

- 5.2.1 PC-Based

- 5.2.2 Smart Camera-Based

- 5.3 By Imaging Type

- 5.3.1 2D Imaging

- 5.3.2 3D Imaging

- 5.3.3 Hyperspectral and Multispectral Imaging

- 5.4 By Deployment Mode

- 5.4.1 On-Premise

- 5.4.2 Edge/Embedded

- 5.4.3 Cloud-Based

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Electronics and Semiconductors

- 5.5.3 Food and Beverage

- 5.5.4 Healthcare and Pharmaceutical

- 5.5.5 Logistics and Retail

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.5 Middle East

- 5.6.5.1 Turkey

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cognex Corporation

- 6.4.2 Keyence Corporation

- 6.4.3 Omron Corporation

- 6.4.4 Teledyne Technologies Incorporated

- 6.4.5 Sony Group Corporation

- 6.4.6 Atlas Copco AB (ISRA Vision)

- 6.4.7 IDS Imaging Development Systems GmbH

- 6.4.8 National Instruments Corporation

- 6.4.9 MVTec Software GmbH

- 6.4.10 Basler AG

- 6.4.11 Allied Vision Technologies GmbH

- 6.4.12 TKH Group NV (LMI Technologies)

- 6.4.13 FLIR Systems Inc (Teledyne)

- 6.4.14 Intel Corporation

- 6.4.15 Qualcomm Technologies Inc

- 6.4.16 Sick AG

- 6.4.17 Panasonic Holdings Corporation

- 6.4.18 Stemmer Imaging AG

- 6.4.19 Zebra Technologies Corporation

- 6.4.20 Hitachi Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

機器視覺市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、功能和解決方案分類

機器視覺市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、部署方式、最終用戶、功能和解決方案分類 機器視覺市場:2026-2032年全球市場預測(按類型、交付方式、系統類型、波長範圍、影像擷取模式、應用、產業和銷售管道)

機器視覺市場:2026-2032年全球市場預測(按類型、交付方式、系統類型、波長範圍、影像擷取模式、應用、產業和銷售管道) 機器視覺市場在採後品質分析的應用-全球及區域分析:按應用、產品和地區分類-分析與預測(2025-2035 年)

機器視覺市場在採後品質分析的應用-全球及區域分析:按應用、產品和地區分類-分析與預測(2025-2035 年) 2026年全球機器視覺市場報告2026年全球機器視覺軟體市場報告基於人工智慧的機器視覺市場:按產品、技術、應用和最終用戶產業分類——2026年至2032年全球預測

2026年全球機器視覺市場報告2026年全球機器視覺軟體市場報告基於人工智慧的機器視覺市場:按產品、技術、應用和最終用戶產業分類——2026年至2032年全球預測 機器視覺市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

機器視覺市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 日本機器視覺系統市場規模、佔有率、趨勢及預測(按組件、產品、最終用途產業及地區分類),2026-2034年2026年全球機器視覺系統及組件市場報告

日本機器視覺系統市場規模、佔有率、趨勢及預測(按組件、產品、最終用途產業及地區分類),2026-2034年2026年全球機器視覺系統及組件市場報告 視覺引導機器人(VGR)系統市場規模、佔有率及預測:依二維/三維視覺、機器人類型(關節型、SCARA)、軟體整合及應用(組裝、品質控制)劃分-全球預測至2036年

視覺引導機器人(VGR)系統市場規模、佔有率及預測:依二維/三維視覺、機器人類型(關節型、SCARA)、軟體整合及應用(組裝、品質控制)劃分-全球預測至2036年