|

市場調查報告書

商品編碼

1906283

鍺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germanium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

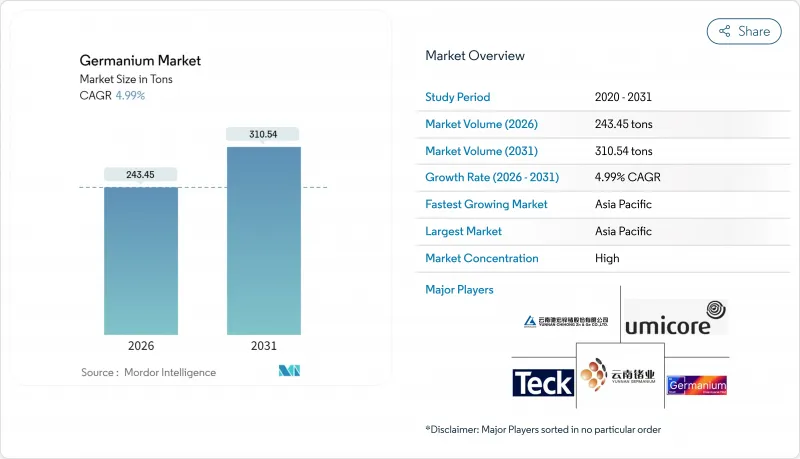

預計到 2026 年,鍺市場規模將達到 243.45 噸,高於 2025 年的 231.88 噸。預測到 2031 年,鍺市場規模將達到 310.54 噸,2026 年至 2031 年的複合年成長率為 4.99%。

價格趨勢印證了這一成長軌跡:中國收緊出口限制導致現貨價格在2025年3月飆升至每公斤4,150美元,較2023年1月上漲75%。需求主要集中在高效能應用領域,鍺的優異光學和電學性能彌補了其高成本。光纖基礎設施部署、航太太陽能電池陣列和量子研究都在推動鍺的消費量,國防機構也正在資助國內新建晶圓產能以降低供應風險。鍺作為鋅提煉產品,其獨特的性質限制了生產對價格飆升的反應速度,加劇了持續的供應緊張。這些因素共同推動了全球鍺市場在需求主導,但又高度依賴地緣政治因素的擴張。

全球鍺市場趨勢與洞察

對光纖通訊的需求不斷成長

通訊業者在擴展5G回程傳輸網路和試運行6G原型時,依賴摻鍺二氧化矽來維持洲際距離上的訊號強度。這種材料的高屈光對比度在超低損耗光纖中無與倫比,因此在長途線路中很難找到替代品。所以,即使每公里摻鍺量下降,網路密集化仍將推動總使用量的成長。中國在2023年後的戰略性鍺儲備和更嚴格的許可監管加劇了西方通訊業者的安全擔憂,並促使他們同時努力獲得非中國煉製路線的認證。日本和美國對大型預製棒工廠的投資表明,隨著數據流量的成長,鍺市場仍有持續上漲的空間。

自動駕駛汽車和工業成像領域對紅外線光學元件的需求激增

鍺在 8-12 微米波長範圍內的透明特性,為熱成像技術開闢了新的應用領域,從駕駛輔助攝影機到工廠檢測鏡頭,均可應用。歐盟法規強制要求從 2024 年起新車必須配備駕駛員監控功能,加速了該技術的普及。硫系玻璃雖然價格更低,但在透射效率和環境穩定性方面不如鍺,因此,原始設備製造商 (OEM) 仍然選擇鍺光學元件來建造高階安全系統。同時,工業維護領域對能夠耐受腐蝕性環境的紅外線窗口的需求也在不斷成長。

供應集中度以及中國的出口許可和禁令

截至2024年,中國將開採或提煉全球超過65%的原生鍺,其於2024年12月禁止直接向美國出口鍺的舉措,凸顯了這種供應集中帶來的影響。根據美國地質調查局(USGS)估計,全面禁止對美出口鍺將使美國GDP減少34億美元,其中40%的損失集中在半導體製造業。這凸顯了關鍵供應鏈的脆弱性。儘管總部位於比利時的優美科(Umicore)和總部位於剛果民主共和國的STL公司正在將其工廠擴建至年產能30噸,但產量仍然小規模,不足以彌補長期供應中斷帶來的影響。

細分市場分析

二氧化鍺佔鍺市場總量的30.08%,穩固確立了其作為光纖預型體和催化劑生產關鍵中間體的地位。其需求與通訊電纜鋪設的趨勢密切相關,因此該細分市場正處於穩定而漸進的成長軌道上。中國和比利時工廠溶劑萃取製程的改進提高了回收率,從而略微增加了從煙氣中獲取原料的需求。

預計到2031年,四氯化鍺的年複合成長率將達到5.54%,主要得益於量子級晶體生長商對超乾燥、超純前驅體的需求,這些前驅體可用於化學氣相沉積反應器。此外,雷射光學鍍膜應用也存在一定的市場需求,此應用需要透過氯化物基化學製程實現高精度的化學計量比控制。通常採用區域純化法製備的11N純度鍺錠可滿足紅外線透鏡毛坯和高頻電晶體基板的需求。然而,由於需求量不足(每年少於10噸),該細分市場的發展受到限制,而價格溢價則保護了綜合生產商免受大宗商品價格波動的影響。其他鍺化學品,例如四氟化鍺和碘化鍺,目前仍處於實驗室階段,等待更廣泛的商業性化應用。

鍺市場報告按類型(二氧化鍺、四氯化鍺、鍺錠及其他)、應用(光纖系統、紅外線光學元件、聚合催化劑、電子產品、太陽能電池及其他)和地區(亞太地區、北美地區、歐洲地區及世界其他地區)進行細分。市場預測以噸為單位。

區域分析

到2025年,亞太地區將佔據全球鍺市場58.80%的佔有率,主要得益於中國垂直整合的製造商將鋅冶煉廠浸出殘渣轉化為6N或更高純度的鍺。隨著通訊業者完成5G部署和半導體晶圓廠擴大高頻寬記憶體生產,預計到2031年,亞太地區的消費量將以5.53%的複合年成長率成長。中國政府的「戰略材料2035」計畫為13N晶體拉絲生產線的升級改造提供補貼,進一步鞏固了該地區的產能優勢。

北美市場地位顯著提升,這主要得益於國防和航太相關合約對超純晶片穩定供應的重視。 5N Plus 和 Teck Resources 等公司正在供應國內材料,但供應量不足以完全消除供應鏈風險。華盛頓州 2024 年國防生產法案的撥款正在推動新建提煉的可行性研究,這預示著該地區鍺市場將在政策主導擴張。

歐洲主要依賴比利時、德國和波蘭工廠的小規模生產,其餘部分則依賴進口,主要來自中國。歐盟於2024年6月通過的《關鍵材料法案》設定了2030年將進口依賴度降低至65%或以下的目標,並為回收示範計畫提供資金。優美科在剛果民主共和國的合資企業已取得初步進展,於2024年10月交付了首批5噸產品。世界其他地區,例如奈米比亞和哈薩克斯坦,也存在其他有發展前景的地區,但要達到環境和純度標準,需要大量資金投入。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對光纖通訊的需求不斷成長

- 自動駕駛汽車和工業成像領域對紅外線(IR)光學元件的需求激增

- 在高效能多結太陽能電池中採用鍺基板

- 超高純鍺在量子計算量子位元和低溫檢測器的應用

- 國防部資助擴大國內半導體級鍺晶片產能

- 市場限制

- 供應集中度以及中國的出口許可和禁令措施

- 鋅礦開採的產品特性導致價格波動。

- 與矽基替代品相比,純化和晶體生長成本較高

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 二氧化鍺

- 四氯化鍺

- 鍺錠

- 其他類型(四氟化鍺、溴化鍺、碘化鍺)

- 透過使用

- 光纖系統

- 紅外線光學

- 聚合催化劑

- 電子設備

- 太陽能電池

- 其他應用(磷光體、冶金、伽馬射線檢測器)

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 比利時

- 俄羅斯

- 其他歐洲地區

- 世界其他地區

- 南美洲

- 中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率**(%)/排名分析

- 公司簡介

- 5N Plus Inc.

- China Germanium Co., Ltd.

- Indium Corporation

- JSC Germanium

- Nyrstar

- Societe Pour Le Traitment du Terril de Lubumbashi(STL)

- Teck Resources Limited

- Umicore

- Yunnan Chihong Zinc & Germanium Co.

- YUNNAN GERMANIUM

第7章 市場機會與未來展望

Germanium market size in 2026 is estimated at 243.45 tons, growing from 2025 value of 231.88 tons with 2031 projections showing 310.54 tons, growing at 4.99% CAGR over 2026-2031.

Price momentum underscores this growth path: spot quotations climbed to USD 4,150 per kg in March 2025, a 75% jump from January 2023, after China widened its export curbs. Demand concentrates in high-performance uses where germanium's optical and electrical properties outweigh elevated costs. Fiber-optic infrastructure roll-outs, aerospace solar arrays, and quantum research all consume rising volumes, while defense agencies fund new domestic wafer capacity to contain supply risk. Ongoing tightness is accentuated by germanium's status as a by-product of zinc smelting, which limits the speed with which production can respond to price spikes. Together these forces anchor a demand-driven but geopolitically sensitive expansion for the global germanium market.

Global Germanium Market Trends and Insights

Rising demand for fiber-optic telecommunications

Telecom operators expanding 5G backhaul and trialing 6G prototypes rely on germanium-doped silica to preserve signal strength over transcontinental distances. The material's high refractive-index contrast is unmatched for ultra-low-loss fibers, keeping substitution infeasible for long-haul lines. Network densification, therefore, lifts tonnage even as dopant loadings per kilometer fall. China's strategic stock build and tighter licensing since 2023 amplified security concerns among Western carriers, prompting parallel efforts to qualify non-Chinese refining routes. Investments in larger preform facilities in Japan and the United States indicate sustained upside for the germanium market amid data-traffic growth.

Surging need for infrared optics in autonomous vehicles & industrial imaging

Germanium's 8-12 μm transparency opens thermal-imaging use cases from driver-assist cameras to factory inspection lenses. EU regulations that require driver-monitoring features in new models from 2024 accelerate adoption. While chalcogenide glasses offer a cheaper alternative, they lag germanium in transmission efficiency and environmental stability, keeping OEMs anchored to germanium optics for premium safety systems. Parallel demand comes from industrial maintenance, where infrared windows withstand corrosive conditions.

Concentrated supply & Chinese export licensing/bans

China mined or refined more than 65% of primary germanium in 2024, and its December 2024 ban on direct shipments to the United States showcased the leverage that concentration confers. The USGS projects that a full embargo would cut U.S. GDP by USD 3.4 billion, 40% of which would fall on semiconductor fabrication, underlining exposure along critical supply chains. Belgium's Umicore and DRC-based STL are scaling a 30 tpy plant but volumes remain too small to offset a prolonged suspension.

Other drivers and restraints analyzed in the detailed report include:

- Deployment of ultra-high-purity germanium in quantum computing qubits & cryogenic detectors

- Defense funding to on-shore semiconductor-grade germanium wafer capacity

- Price volatility linked to zinc-mine by-product nature

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The germanium market size attributed to germanium dioxide accounted for 30.08% of total volume, cementing its role as the workhorse intermediate for optical-fiber preforms and catalyst production. Demand tracks telecom cable deployment patterns, giving this segment a stable yet moderate growth path. Improving solvent-extraction circuits in Chinese and Belgian plants are lifting recovery yields, marginally expanding accessible feedstock from flue dusts.

Germanium tetrachloride is projected to grow at 5.54% CAGR through 2031 as quantum-grade crystal growers source ultra-dry, ultrapure precursor for chemical-vapor-deposition reactors. Niche volumes also serve laser-optic coatings where chloride-route chemistry delivers high stoichiometric control. Ingots, typically zone-refined to 11N purity, fulfill infrared lens blanks and high-frequency transistor substrates. Their sub-10 ton annual requirements keep this tier tight, with pricing premiums shielding integrated producers from commodity swings. Other germanium chemicals such as tetrafluoride and iodide remain laboratory-scale, awaiting broader commercial validation.

The Germanium Market Report is Segmented by Type (Germanium Dioxide, Germanium Tetrachloride, Germanium Ingots, Other Types), Application (Fiber Optics System, Infrared Optics, Polymerisation Catalysts, Electronics, Solar Cells, Other Applications), and Geography (Asia-Pacific, North America, Europe, Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominated the germanium market with a 58.80% share in 2025, supported by vertically integrated Chinese producers that convert zinc-smelter leach residues into 6N metal and higher. Regional consumption will climb at a 5.53% CAGR through 2031 as telecom carriers complete 5G roll-outs and semiconductor fabs ramp high-bandwidth memory production. Government incentives under China's "Strategic Materials 2035" program subsidize upgrades to 13N crystal pulling lines, reinforcing local capacity advantages.

North America has significantly strengthened its position in the market due to defense and space contracts, which prioritize guaranteed access to ultra-pure wafers. 5N Plus and Teck Resources furnish domestic feed, but volumes remain insufficient to fully de-risk the supply chain. Washington's Defense Production Act allocations in 2024 spurred feasibility studies for additional refining furnaces, signaling a policy-driven uptick in the region's germanium market.

Europe relies on Belgian, German, and Polish plants for modest production, importing the remainder mainly from China. The EU Critical Raw Materials Act, adopted in June 2024, sets a 65% import-dependency ceiling by 2030 and earmarks funding for recycling pilots. Early progress is visible in Umicore's DRC joint venture, which shipped its first 5-ton batch in October 2024. Rest-of-World locations such as Namibia and Kazakhstan host resource prospects but require significant capital to meet environmental and purity benchmarks.

- 5N Plus Inc.

- China Germanium Co., Ltd.

- Indium Corporation

- JSC Germanium

- Nyrstar

- Societe Pour Le Traitment du Terril de Lubumbashi (STL)

- Teck Resources Limited

- Umicore

- Yunnan Chihong Zinc & Germanium Co.

- YUNNAN GERMANIUM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for fiber-optic telecommunications

- 4.2.2 Surging need for infrared (IR) optics in autonomous vehicles and industrial imaging

- 4.2.3 Adoption of germanium substrates in high-efficiency multi-junction solar cells

- 4.2.4 Deployment of ultra-high-purity Ge in quantum computing qubits and cryogenic detectors

- 4.2.5 Defense funding to on-shore semiconductor-grade germanium wafer capacity

- 4.3 Market Restraints

- 4.3.1 Concentrated supply and Chinese export licensing/bans

- 4.3.2 Price volatility linked to zinc-mine by-product nature

- 4.3.3 High purification and crystal-growth costs vs. silicon alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Germanium Dioxide

- 5.1.2 Germanium Tetrachloride

- 5.1.3 Germanium Ingots

- 5.1.4 Other Types (Germanium Tetrafluoride, Germanium Bromide, Germanium Iodide)

- 5.2 By Application

- 5.2.1 Fiber Optics System

- 5.2.2 Infrared Optics

- 5.2.3 Polymerisation Catalysts

- 5.2.4 Electronics

- 5.2.5 Solar Cells

- 5.2.6 Other Applications (Phosphors, Metallurgy, and Gamma Ray Detectors)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 India

- 5.3.1.5 Rest of Asia-pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Belgium

- 5.3.3.4 Russia

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 5N Plus Inc.

- 6.4.2 China Germanium Co., Ltd.

- 6.4.3 Indium Corporation

- 6.4.4 JSC Germanium

- 6.4.5 Nyrstar

- 6.4.6 Societe Pour Le Traitment du Terril de Lubumbashi (STL)

- 6.4.7 Teck Resources Limited

- 6.4.8 Umicore

- 6.4.9 Yunnan Chihong Zinc & Germanium Co.

- 6.4.10 YUNNAN GERMANIUM

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

鍺市場:全球市場按產品類型、應用和最終用途行業分類的預測 - 2026-2032年

鍺市場:全球市場按產品類型、應用和最終用途行業分類的預測 - 2026-2032年 鍺(GeCl4、GeO2、ZRG、SCG)-全球市場、終端用戶、應用及競爭對手:2024-2031 年分析與預測矽鍺材料及元件市場:2026-2032年全球市場預測(依元件類型、材料組成、晶圓直徑、製造技術、應用及最終用途產業分類)鍺-68/鎵-68發生器市場:按技術、發生器容量、應用和最終用戶分類-2026年至2032年全球預測

鍺(GeCl4、GeO2、ZRG、SCG)-全球市場、終端用戶、應用及競爭對手:2024-2031 年分析與預測矽鍺材料及元件市場:2026-2032年全球市場預測(依元件類型、材料組成、晶圓直徑、製造技術、應用及最終用途產業分類)鍺-68/鎵-68發生器市場:按技術、發生器容量、應用和最終用戶分類-2026年至2032年全球預測 鍺全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)金鍺共晶市場按應用、形態、最終用戶、純度和工藝分類-全球預測(2026-2032 年)鍺-68市場按應用程式、產品類型、最終用戶和通路分類-2026-2032年全球預測鍺板市場依純度、等級、厚度、應用、通路和最終用戶分類-2026-2032年全球預測全球鍺市場-2025-2030年預測鍺箔市場按產品類型、純度等級、厚度、應用、最終用途產業和銷售管道分類-2025-2030 年全球預測

鍺全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)金鍺共晶市場按應用、形態、最終用戶、純度和工藝分類-全球預測(2026-2032 年)鍺-68市場按應用程式、產品類型、最終用戶和通路分類-2026-2032年全球預測鍺板市場依純度、等級、厚度、應用、通路和最終用戶分類-2026-2032年全球預測全球鍺市場-2025-2030年預測鍺箔市場按產品類型、純度等級、厚度、應用、最終用途產業和銷售管道分類-2025-2030 年全球預測