|

市場調查報告書

商品編碼

1906245

負載測試器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Load Bank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

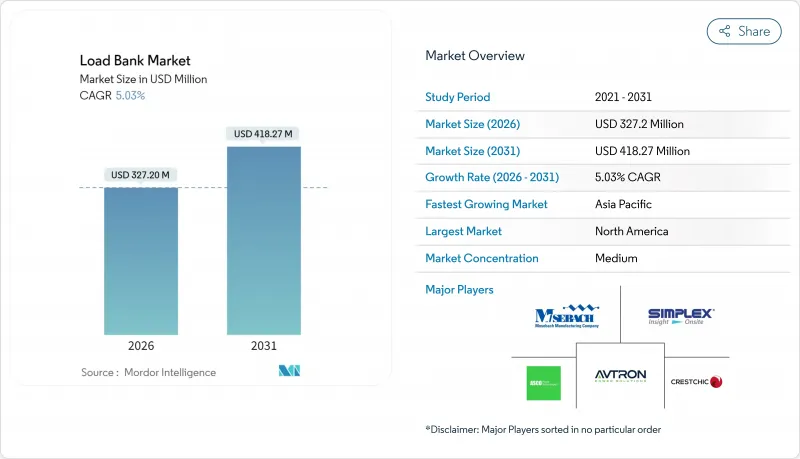

預計到 2026 年,負載測試器市場規模將達到 3.272 億美元,高於 2025 年的 3.1153 億美元。

預計到 2031 年將達到 4.1827 億美元,2026 年至 2031 年的複合年成長率為 5.03%。

這一成長動能主要由超大規模資料中心的擴張、需要進行穩定性檢驗的可再生能源密集型電網以及關鍵任務設施日益嚴格的效能要求所驅動。資料中心營運商正在提高功率密度標準,這需要進行多階段檢驗,並擴大了負載測試器服務供應商的租賃機會。可再生能源的併網增加了對電阻性和電抗性系統以及能夠模擬風能、太陽能和儲能計劃動態負載曲線的電子系統的需求。製造商正在透過可回收高達96%測試能量的再生設計來應對這一需求,這一特性正日益成為新建公用事業和微電網採購的必要條件。同時,原物料價格上漲和計劃交付週期縮短正促使許多買家轉向輕資產租賃模式,進而影響整個負載測試器市場的競爭策略。

全球負載測試器市場趨勢與洞察

資料中心容量快速擴張

2024年,資料中心建設支出將達到每年315億美元,全球新增資料中心面積將接近5,000萬平方英尺。超大規模營運商現在要求從工廠啟動到整合系統檢驗全程進行持續驗收測試,這顯著提高了租賃負載測試器的使用率。為了維持服務等級協議,臨時負載箱會在維護窗口期間定期重新部署,從而產生持續收入。人工智慧工作負載的功率密度不斷提高,迫使資料中心試運行需要進行兆瓦級負載測試的高容量備用發電機。託管空間的提前預租正在加快試運行進度,縮短測試時間,並推高市場上可快速部署的負載測試器產品的溢價。

由於可再生能源的快速成長,電網穩定變得尤為重要。

整合風能和太陽能的電力公司必須證明其符合 IEEE 1547-2018 併網通訊協定,該協議強調有功功率管理和頻率響應。在巴西的 Morro dos Ventos 風電場通訊協定中,使用了一個 3.3 MVA 的負載測試器來檢驗145 MW 風力渦輪機的輸出功率,然後再併網。對於太陽能發電計劃,在不斷變化的太陽輻射條件下進行棄風測試是強制性的,這推動了對能夠模擬突發負載變化的可編程電子單元的需求。能源儲存系統增加了場景的複雜性,電池放電和發電機備用電源之間的無縫切換透過混合負載測試來檢驗。亞洲和南美洲的電力公司正在尋求能夠支援多個變電站的攜帶式大容量設備,這促進了相容負載測試器市場的擴張。

計劃週期短更有利於租賃而非購買。

試運行團隊擴大在幾週內完成負載測試器的採購,這削弱了設備採購的合理性。儲存、維護和折舊免稅額成本使得租賃在生命週期經濟效益方面更具優勢,尤其是在多個計劃並行運作時。大型租賃公司利用與原始設備製造商 (OEM) 的批量折扣,擠壓了單一製造商的利潤空間。設施管理團隊傾向於將測試納入能源基礎設施合約的打包服務協議,從而減少了對設備的直接需求。這種向服務型模式的結構性轉變預計將增加負載測試器市場的整體收入,但會抑制獨立銷售量。

細分市場分析

混合式負載單元將電阻性和無功功率元件整合於同一機殼內,預計到2025年將佔據負載測試器市場44.60%的佔有率,使承包商能夠使用單一租賃單元完成各種試運行任務。儘管電子負載系統目前的裝置量較小,但預計到2031年將以7.78%的複合年成長率成長。其可再生能源架構可將高達96%的吸收能量回饋電網,從而降低測試週期內的運作成本並減少現場的餘熱需求。純電阻式產品定位為入門級產品,適用於無需功率因數校正的簡單發電機下拉測試。同時,無功式產品可為馬達控制和UPS檢驗提供精確的感性或容性負載。

在超大規模資料中心,電子類產品應用最為迅速,因為降低冷卻負荷和縮短停機時間至關重要。營運商正擴大採用機架級再生式冷凍單元,並將其與建築管理軟體對接。同時,混合式設計在租賃設備中仍然很受歡迎,它在單一撬裝單元上模擬主動和被動組件,從而提高可用性並降低物流成本。純被動產品仍是電力公司檢驗運轉率因數校正設備的小眾市場。泰克科技於2024年4月收購了EA Elektro-Automatik,將其3.8MW再生式冷凍平台擴展至96%以上的往返效率,凸顯了產業向高效、數位化控制解決方案的融合趨勢。

功率超過2000kW的設備將以6.62%的複合年成長率成長,這反映了需要超過100MW電力的超大規模資料中心的快速成長。這些資料中心需要兆瓦級的發電機組和對應的負載測試器,以便透過一次下拉測試即可對整個系統進行全面測試。同時,功率低於500kW的設備在2025年仍將佔總收入的39.30%,這主要得益於醫院和商業建築對UPS和緊急發電機進行例行檢查的需求。隨著中型資料中心的興起,501-2000kW負載測試器的市場規模也在穩定擴大,但增速低於功率兩端的設備。

規模經濟有利於大容量撬裝設備的生產,但運輸物流和現場搬運的限制仍是限制因素。小型平台由於成本低、易於移動而保持市場需求,尤其是在服務分散基本客群的租賃車隊中。最小和最大細分市場之間的兩極化凸顯了不同產業採購標準的差異,並強化了產品系列多元化作為競爭優勢的必要性。

負載測試器市場報告按類型(混合負載測試器、電子負載測試器等)、負載容量(500KW 以下、2000KW 以上等)、外形規格(可攜式、機架式/模組化等)、應用(資料中心/雲端、可再生能源整合/微電網等)、最終用戶(公共產業、租賃/服務供應商等)和地區(北美、歐洲、亞太地區)進行細分、歐洲、亞太地區等地區。

區域分析

到2025年,北美地區將佔施耐德電氣總收入的35.10%,這得益於Schneider Electric計畫在2027年前投資7億美元擴大其製造能力。此舉將加強資料中心和公共產業的國內供應鏈。諸如NFPA 110等法規結構要求對關鍵基礎設施的發電機進行滿載測試,從而保障了基準需求。銅價上漲加劇了成本壓力,並推動了在地採購,從而縮短了前置作業時間。成熟的租賃生態系統支援快速部署,並使該地區的服務能力脫穎而出。

亞太地區預計將以7.45%的複合年成長率成為成長最快的地區,這主要得益於資料中心裝置容量年均22%的成長,預計東京、雪梨、孟買和首爾等主要大都會地區的裝置容量將達到2996兆瓦。各國為促進人工智慧和雲端運算應用而製定的策略正在推動對備用電源的投資,而多樣化的氣候條件則要求設備能夠承受高濕度和極端溫度變化。中國新的資料中心能源效率法規,以及新加坡計劃的重啟,正在推動先進可再生能源設備的採購。

歐洲在嚴格的環境政策基礎上穩步取得進展。歐盟指令2000/14/EC限制了室外裝置的噪音排放,促使原始設備製造商(OEM)採用改良的擋板和低速風扇設計。歐盟再生能源計畫(REPowerEU)的可再生能源容量目標正在加速分散式能源併網測試,並擴大其應用範圍。市場參與企業正在利用模組化貨櫃解決方案,以滿足都市區噪音法規和面積,並與更廣泛的綠色基礎設施計劃保持一致。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 資料中心容量快速成長

- 由於可再生能源的快速成長,對電網穩定性的需求日益成長

- 關鍵設施的容錯需求

- 租賃/臨時電力設施擴建

- 偏遠地區混合交流-直流微電網的興起

- 燃料節約促使人們傾向選擇再生負載測試器

- 市場限制

- 由於計劃週期短,租房比買房更受歡迎。

- 原物料價格波動(銅、不鏽鋼)

- 原始設備製造商之間缺乏互通性標準

- 都市區噪音和熱排放法規遵守情況問題

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 電阻負載測試器

- 無功負載測試器

- 混合負載測試器

- 電子負載測試器

- 按負載容量(千瓦額定值)

- 小於500千瓦

- 501~1,000 kW

- 1,001~2,000 kW

- 2000度或以上

- 按外形規格

- 可攜式的

- 拖車式/移動式

- 固定式

- 機架式/模組化

- 透過使用

- 發電和試運行

- 資料中心和雲

- 製造業和工業

- 海洋/造船

- 石油天然氣和石化

- 可再生能源併網和微電網

- 國防和航太地面支援

- 醫療及其他必要設施

- 最終用戶

- 公共產業

- 商業和工業業主

- 租賃和服務供應商

- 國防和政府機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- ASCO Power Technologies(Schneider Electric)

- Crestchic Loadbanks

- Avtron Power Solutions(Vertiv)

- Simplex(Cummins)

- Mosebach Manufacturing

- Load Banks Direct

- Eagle Eye Power Solutions

- Kaixiang Power

- Sephco Industries

- Powerohm Resistors(AMETEK)

- Hillstone Products

- Tatsumi Ryoki

- Shenzhen KSTAR

- ComRent International

- Hitec Power Protection

- Nordhavn Power Solutions

- Pite Tech

- Johnson Controls(Load Bank Division)

- Trystar Load Banks

- Pacific Power Source

- Powerhaul International

第7章 市場機會與未來展望

Load Bank Market size in 2026 is estimated at USD 327.2 million, growing from 2025 value of USD 311.53 million with 2031 projections showing USD 418.27 million, growing at 5.03% CAGR over 2026-2031.

Momentum originates from hyperscale data-center build-outs, renewable-rich grids requiring stability validation, and stricter performance mandates for mission-critical facilities. Data-center operators are raising power-density benchmarks, prompting multi-stage validation that expands rental opportunities for load-bank service providers. Renewable integration adds demand for resistive-reactive and electronic systems that can simulate dynamic load profiles for wind, solar, and storage projects. Manufacturers respond with regenerative designs that recover up to 96% of test energy, a feature increasingly requested in new utility and microgrid procurements. At the same time, raw-material inflation and short project timelines pivot many buyers toward asset-light rental models, influencing competitive strategy across the load bank market.

Global Load Bank Market Trends and Insights

Rapid Data-Center Capacity Additions

Annual data-center construction spending stood at USD 31.5 billion in 2024, and the global pipeline is nearing 50 million ft2 of new space. Hyperscale operators now demand sequential acceptance tests that start at the factory and end with integrated system validation, significantly lifting the utilization of rental load banks. Temporary fleets are routinely redeployed during maintenance windows to sustain service-level agreements, generating recurring revenue. AI workloads lift power density, forcing facilities to commission higher-capacity standby generators that require multi-megawatt load tests. Early pre-leasing of colocation space accelerates the commissioning schedule, compressing test timelines and elevating the premium on fast-deploy load bank market offerings.

Grid-Stability Needs Amid Renewable Surge

Utilities integrating wind and solar must show compliance with IEEE 1547-2018 interconnection protocols, which emphasize active power management and frequency response.Wind-farm projects such as Brazil's Morro Dos Ventos used a 3.3 MVA load bank to validate 145 MW of turbine output before grid tie-in. Photovoltaic installations now include curtailment testing under varying irradiance profiles, driving demand for programmable electronic units that can replicate rapid load ramps. Energy-storage systems complicate scenarios; seamless transition between battery discharge and generator backup is verified through hybrid load tests. Utilities in Asia and South America seek portable high-capacity rigs to service multiple substations, bolstering the addressable load bank market.

Short Project Cycles Favor Rentals Over Purchases

Commissioning teams increasingly source load banks for only a few weeks, undermining the case for capital purchases. Storage, maintenance, and depreciation costs tilt life-cycle economics toward renting, especially when multiple projects run concurrently. Large rental houses leverage volume-purchase discounts with OEMs, tightening margin pressure on standalone manufacturers. Facilities management groups prefer bundled service contracts that fold testing into wider energy-infrastructure deals, reducing direct equipment demand. This structural swing toward services constrains unit volumes as overall load bank market revenues grow.

Other drivers and restraints analyzed in the detailed report include:

- Resiliency Mandates for Mission-Critical Facilities

- Expansion of Rental/Temporary Power Fleet

- Volatility in Raw-Material Prices (Copper, Stainless Steel)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid units held 44.60% of the load bank market share in 2025 by combining resistive and reactive elements inside one enclosure, allowing contractors to complete a wider range of commissioning tasks with a single rental. Though smaller in installed base, electronic systems are forecast for an 7.78% CAGR through 2031 as their regenerative architecture returns up to 96% of absorbed energy to the grid, trimming test-cycle operating costs and lowering on-site heat rejection needs. Pure resistive products remain the entry-level option for straightforward generator pull-down checks where power-factor correction is unnecessary, while reactive models provide precise inductive or capacitive loading for motor-control and UPS validation.

The electronic category is gaining ground fastest inside hyperscale data halls that must limit cooling loads and shorten outage windows; operators increasingly embed rack-level regenerative units that synchronize with building-management software. Meanwhile, hybrid designs stay popular with rental fleets because a single skid can simulate real and reactive components, improving utilization and cutting logistics. Pure reactive offerings persist as a niche for utilities that verify power-factor compensation banks. Tektronix's April 2024 acquisition of EA Elektro-Automatik expanded its regenerative platform to 3.8 MW with >=96% round-trip efficiency, underscoring industry convergence on high-efficiency, digitally controlled solutions.

Units above 2,000 kW will expand at a 6.62% CAGR, mirroring the surge of hyperscale campuses exceeding 100 MW utility feeds. These facilities require multi-megawatt generator strings and commensurate load banks capable of full-system testing in a single pull-down. Conversely, sub-500 kW devices maintained 39.30% of 2025 revenue, underpinned by routine UPS and standby-generator checks in hospitals and commercial buildings. The load bank market size for 501-2,000 kW equipment advances steadily as mid-tier data-centers proliferate, though growth moderates relative to extremes at both ends.

Economies of scale favor manufacturing higher-capacity skids, but transport logistics and site-handling constraints remain limiting factors. Smaller platforms preserve demand due to low cost and ease of mobility, particularly in rental fleets that service distributed customer bases. Polarization between the smallest and largest segments underscores divergent procurement criteria across industries, reinforcing product-portfolio diversification as a competitive necessity.

The Load Bank Market Report is Segmented by Type (Hybrid Load Banks, Electronic Load Banks, and More), Load Capacity (Up To 500 KW, Above 2, 000 KW, and More), Form Factor (Portable, Rack-Mounted/Modular, and More), Application (Data Centres and Cloud, Renewable-Energy Integration and Microgrids, and More), End-User (Utilities, Rental and Service Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America controlled 35.10% of 2025 revenue, underpinned by Schneider Electric's USD 700 million manufacturing expansion pledge through 2027, which enhances domestic supply chains serving data centers and utilities. Regulatory frameworks such as NFPA 110 prescribe full-load generator tests for critical infrastructure, sustaining baseline demand. Tariffs on copper raise cost pressure and prompt localization moves that shorten lead times. Mature rental ecosystems support rapid deployment, differentiating the region's service capability.

Asia-Pacific is projected to have the quickest 7.45% CAGR thanks to a 22% annual increase in data-center inventory reaching 2,996 MW across metro hubs like Tokyo, Sydney, Mumbai, and Seoul. National strategies encouraging AI and cloud adoption elevate backup-power investments, while diverse climates necessitate equipment able to endure high humidity and wide temperature swings. China's new data-center energy-efficiency rules and Singapore's restart of the project collectively stimulate the procurement of advanced regenerative units.

Europe exhibits steady progression anchored in stringent environmental policy. Directive 2000/14/EC caps noise emissions for outdoor equipment, pushing OEMs to integrate improved baffling and low-RPM fan designs. Renewable-capacity targets under REPowerEU accelerate grid-support trials for distributed energy resources, widening the application scope. Market participants leverage modular container solutions compatible with urban noise and footprint constraints, aligning with broader green-infrastructure ambitions.

- ASCO Power Technologies (Schneider Electric)

- Crestchic Loadbanks

- Avtron Power Solutions (Vertiv)

- Simplex (Cummins)

- Mosebach Manufacturing

- Load Banks Direct

- Eagle Eye Power Solutions

- Kaixiang Power

- Sephco Industries

- Powerohm Resistors (AMETEK)

- Hillstone Products

- Tatsumi Ryoki

- Shenzhen KSTAR

- ComRent International

- Hitec Power Protection

- Nordhavn Power Solutions

- Pite Tech

- Johnson Controls (Load Bank Division)

- Trystar Load Banks

- Pacific Power Source

- Powerhaul International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid data-centre capacity additions

- 4.2.2 Grid-stability needs amid renewable surge

- 4.2.3 Resiliency mandates for mission-critical facilities

- 4.2.4 Expansion of rental/temporary power fleet

- 4.2.5 Rise of hybrid AC-DC microgrids in remote sites

- 4.2.6 Growing preference for regenerative load banks to curb fuel burn

- 4.3 Market Restraints

- 4.3.1 Short project cycles favour rentals over purchases

- 4.3.2 Volatility in raw-material prices (copper, stainless steel)

- 4.3.3 Limited interoperability standards across OEMs

- 4.3.4 Noise & heat-dissipation compliance hurdles in urban sites

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Resistive Load Banks

- 5.1.2 Reactive Load Banks

- 5.1.3 Hybrid Load Banks

- 5.1.4 Electronic Load Banks

- 5.2 By Load Capacity (kW Rating)

- 5.2.1 Up to 500 kW

- 5.2.2 501 to 1,000 kW

- 5.2.3 1,001 to 2,000 kW

- 5.2.4 Above 2,000 kW

- 5.3 By Form Factor

- 5.3.1 Portable

- 5.3.2 Trailer-Mounted/Mobile

- 5.3.3 Stationary

- 5.3.4 Rack-Mounted/Modular

- 5.4 By Application

- 5.4.1 Power Generation and Commissioning

- 5.4.2 Data Centres and Cloud

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Marine and Shipbuilding

- 5.4.5 Oil and Gas and Petrochemical

- 5.4.6 Renewable-Energy Integration and Microgrids

- 5.4.7 Defence and Aerospace Ground Support

- 5.4.8 Healthcare and Other Mission-Critical Facilities

- 5.5 By End-user

- 5.5.1 Utilities

- 5.5.2 Commercial and Industrial Owners

- 5.5.3 Rental and Service Providers

- 5.5.4 Defence and Government

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ASCO Power Technologies (Schneider Electric)

- 6.4.2 Crestchic Loadbanks

- 6.4.3 Avtron Power Solutions (Vertiv)

- 6.4.4 Simplex (Cummins)

- 6.4.5 Mosebach Manufacturing

- 6.4.6 Load Banks Direct

- 6.4.7 Eagle Eye Power Solutions

- 6.4.8 Kaixiang Power

- 6.4.9 Sephco Industries

- 6.4.10 Powerohm Resistors (AMETEK)

- 6.4.11 Hillstone Products

- 6.4.12 Tatsumi Ryoki

- 6.4.13 Shenzhen KSTAR

- 6.4.14 ComRent International

- 6.4.15 Hitec Power Protection

- 6.4.16 Nordhavn Power Solutions

- 6.4.17 Pite Tech

- 6.4.18 Johnson Controls (Load Bank Division)

- 6.4.19 Trystar Load Banks

- 6.4.20 Pacific Power Source

- 6.4.21 Powerhaul International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球負載測試設備市場:市場規模、佔有率、成長率、依類型和應用劃分的產業分析、區域洞察及未來預測(2026-2034)

全球負載測試設備市場:市場規模、佔有率、成長率、依類型和應用劃分的產業分析、區域洞察及未來預測(2026-2034) 電池負載測試儀市場按產品類型、測試模式、應用、最終用戶和分銷管道分類,全球預測(2026-2032)

電池負載測試儀市場按產品類型、測試模式、應用、最終用戶和分銷管道分類,全球預測(2026-2032) 全球負載測試器市場:市場規模分析(按電流、安裝位置、類型、最終用戶和地區分類)及未來預測(2025-2035 年)

全球負載測試器市場:市場規模分析(按電流、安裝位置、類型、最終用戶和地區分類)及未來預測(2025-2035 年) 負載測試設備市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

負載測試設備市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測 負載箱市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、應用、地區和競爭細分,2020-2030 年

負載箱市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、應用、地區和競爭細分,2020-2030 年 負載測試器市場報告:2030 年趨勢、預測與競爭分析

負載測試器市場報告:2030 年趨勢、預測與競爭分析