|

市場調查報告書

商品編碼

1906244

聚乙烯丁醛(PVB)中間層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Polyvinyl Butyral (PVB) Interlayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

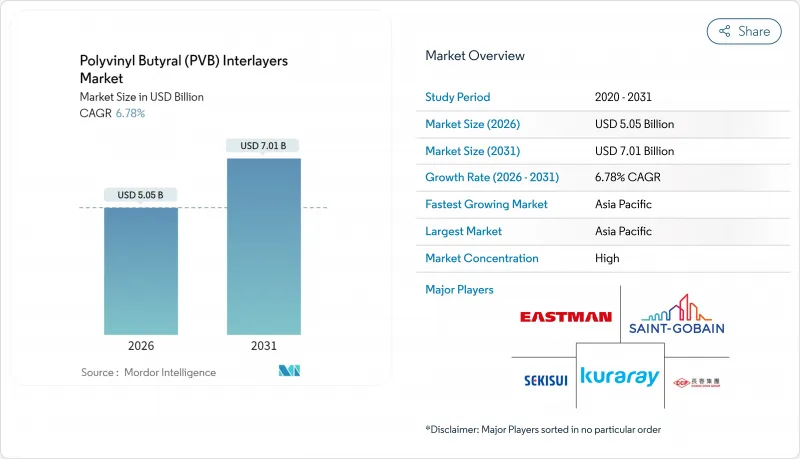

聚乙烯丁醛(PVB) 中間層市場預計將從 2025 年的 47.3 億美元成長到 2026 年的 50.5 億美元,預計到 2031 年將達到 70.1 億美元,2026 年至 2031 年的複合年成長率為 6.78%。

日益嚴格的安全法規、永續性以及對輕量化車輛和綠色建築的需求,是推動這一市場擴張的根本動力。電動車專案正在擴大玻璃的應用範圍,從擋風玻璃擴展到所有窗戶;而獲得LEED認證的建築則指定使用高性能夾層建築幕牆,以減少太陽熱量的穿透並阻擋紫外線。製造商正在推出集隔音、太陽能控制和防撞功能於一體的多功能薄膜,這進一步拓展了聚乙烯丁醛(PVB)夾層市場的潛在機會。然而,原料成本的波動和新興的回收管道正在擠壓利潤空間,並推動主要供應商進行垂直整合。

全球聚乙烯丁醛(PVB)中間層薄膜市場趨勢及洞察

汽車和建築領域對夾層安全玻璃的應用日益廣泛

電動車專案消除了引擎雜訊掩蔽效應,推動了汽車製造商對整合式隔音聚乙烯丁醛)層的側窗和後窗玻璃的需求。積水化學最新推出的S-LEC系列產品可阻擋近紅外光,降低車內溫度並延長車輛續航里程。同時,建築師們正在為高層建築的外牆指定使用大型夾層玻璃面板,其中的夾層可以吸收衝擊能量並防止碎片粘附,從而確保居住者的安全。跨領域的技術轉移縮短了研發週期,使得一個終端應用領域的創新能夠快速應用於其他領域,從而增強了聚乙烯丁醛(PVB)夾層市場。

車輛乘員安全和玻璃強度方面的監管要求

美國公路交通安全管理局 (NHTSA) 的聯邦機動車輛安全標準 217a 將於 2027 年生效,該標準要求客車使用先進的玻璃,這將顯著擴大聚乙烯丁醛(PVB) 夾層的需求。歐洲經濟委員會 (ECE) 的修正案也強調行人安全和翻滾強度,迫使汽車製造商轉向使用更厚、多層層壓玻璃,並採用高模量夾層。更嚴格的法規將增加每輛車的材料用量,這將使能夠配製在寬溫度範圍內保持透明度的抗衝擊薄膜的供應商獲得優勢。

聚乙烯丁醛醛樹脂及其添加劑的價格波動

積水化學株式會社於2024年10月將其S-LEC薄膜的標價上調6%至15%,隨後伊士曼公司也於2025年4月起將塑化劑價格上調0.04美元/磅。中國於2025年1月將PVC進口關稅提高至5.5%,這將為樹脂加工商帶來每噸22.95至23.85美元的額外成本負擔。由於OEM合約中價格通常按每個型號週期固定,下游加工商面臨利潤空間壓縮,聚乙烯丁醛(PVB)中間層市場整體正在經歷行業整合和深化垂直一體化,以確保原料供應並規避價格波動風險。

細分市場分析

到2025年,標準薄膜將佔總銷售額的61.62%,證實了其在安全玻璃領域的廣泛應用。同時,隨著電動車動力系統風噪和胎噪的增加,隔音薄膜的年複合成長率(CAGR)也達到了7.48%。 Sufflex Q隔音薄膜無需改變生產流程即可降低車內聲壓高達7分貝。將隔音、遮光和結構性能整合於單一層壓板中的多功能混合產品,正吸引希望減少零件數量的汽車製造商的注意。用於隔音解決方案的聚乙烯丁醛(PVB)中間層的市場規模預計將從2026年的5億美元成長到2031年的7.1億美元,這預示著價值結構的轉變。紫外線阻隔和抗颶風等級的產品雖然仍處於小眾市場,但利潤豐厚,尤其是在美國沿海和加勒比海地區的建築市場,這些地區極易受到極端天氣的影響,因此對這些產品的需求尤為強勁。

在競爭中,產品系列的廣度正成為比單價更重要的決定性因素。製造商透過調整塑化劑比例,即可將標準級芯材與聲學級芯材互換,從而最佳化工廠使用率,並與全球原始設備製造商 (OEM) 達成雙重採購協議。這種能力正在加速傳統薄膜的替代,同時增強供應商的鎖定效應,並提升其在聚乙烯丁醛(PVB) 中間層市場的定價權。

2025年,片材和捲材產品佔出貨量的84.10%,主要得益於成熟的物流和層壓設施。然而,隨著建築幕牆承包商尋求減少廢棄物和提高生產線速度,根據計劃特定尺寸量身定做的薄膜產品正以7.55%的複合年成長率快速成長。數位切割刀和雷射系統能夠實現與BIM模型相符的客製化佈局,從而減少現場修整工作。受都市區大型企劃興起的推動,預計到2025年,客製化規格聚乙烯丁醛(PVB)夾層的市場佔有率將達到15.90%,並在2031年超過20%。本地層壓設施對於運輸寬度超過3.2米的大型面板至關重要,這有助於實現地域多角化,並促進薄膜製造商和建築幕牆玻璃安裝商之間的合作。

價值創造正從樹脂噸位轉向服務。能夠提供結構模擬、準時交貨套件和現場技術支援的供應商,正在將大宗商品參與企業難以匹敵的無形差異化優勢貨幣化。即使樹脂價格走軟,這些能力也能推高聚乙烯丁醛(PVB) 中間層市場的平均售價,並確保利潤率。

聚乙烯丁醛(PVB) 中間層薄膜市場報告按類型(標準 PVB、隔音 PVB 等)、形式(片材/捲材、客製化切割/預層壓薄膜)、應用(汽車擋風玻璃、汽車側窗和後窗玻璃等)、最終用戶行業(汽車和運輸、建築等)和地區(亞太地區、北美等)細分。

區域分析

到2025年,亞太地區將佔全球營收的44.35%,年複合成長率達7.84%,主要得益於中國每年2,500萬輛的汽車產量和創紀錄的城市建設速度。 2025年1月,PVC進口關稅上調至5.5%,這將使樹脂成本增加23美元/噸,促使玻璃加工商轉向國內PVB薄膜供應商。在印度,不斷成長的汽車銷售和智慧城市規劃(儘管基數較低)也成為額外的成長要素。日本和韓國的領先製造商正在推出隔音和隔熱創新技術,這些技術正在影響整個區域供應鏈。同時,東南亞國協正利用其低廉的人事費用和位於亞洲物流中心的地理位置,吸引新的層壓板生產能力。

北美是一個穩定的替換市場,這得益於美國美國公路交通安全管理局 (NHTSA) 嚴格的法規,這些法規推動了規範標準的製定。計劃於 2027 年生效的公車玻璃法規預計將增加市場需求量和複雜性。節能建築維修,尤其是在美國陽光地帶,傾向於使用遮陽聚乙烯醇縮丁醛 (PVB) 玻璃來抵消尖峰時段冷卻負荷。加拿大的聯邦碳定價機制將進一步推動維修選擇高隔熱玻璃,從而擴大聚乙烯丁醛(PVB) 夾層玻璃的潛在市場。

歐洲仍以技術為中心,其生產者延伸責任制(EPR)體系的實施,使得人們對回收的期望日益提高。 Tarkett公司2024年推出的層壓板再生料回收技術創新,將碳排放強度降低至全新PVB材料的1/25。諸如此類的進步,正將再生材料的使用從監管負擔轉變為市場優勢。儘管需求成長緩慢,但隨著產品組合的擴展,納入多功能、低碳中間層,其價值成長速度持續超過銷售成長速度。

南美洲和中東及非洲地區合計佔全球銷售額不到10%,但卻在小規模的基數上實現了兩位數的成長。巴西汽車需求的復甦以及沿岸地區的大型建設計劃對具有優異耐熱性和耐磨性的玻璃提出了更高的要求。隨著區域法規的日益嚴格,那些針對熱帶氣候最佳化配方的供應商正在搶佔先機,為聚乙烯丁醛(PVB)中間層市場的未來規模化發展奠定了基礎。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 汽車和建築業對夾層安全玻璃的需求不斷成長

- 關於乘員安全和玻璃強度的法規要求

- 對節能玻璃和紫外線防護的需求不斷成長

- 擴大綠建築和LEED認證建築

- 擋風玻璃和建築玻璃面板的更換率不斷提高

- 市場限制

- 聚乙烯丁醛(PVB)樹脂及添加劑的價格波動

- 廢舊產品回收的限制

- 運輸大卷材料面臨的物流挑戰

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 標準聚乙烯丁醛(PVB)中間層

- 聲學聚乙烯丁醛(PVB)中間層

- 太陽能控制聚乙烯丁醛(PVB)中間層

- 彩色和色調聚乙烯丁醛(PVB)夾層

- 抗紫外線/高性能聚乙烯丁醛(PVB)中間層

- 按形式

- 片材/卷材

- 客製化切割/預覆膜薄膜

- 透過使用

- 汽車擋風玻璃

- 汽車側窗和後窗

- 建築玻璃(窗戶、建築幕牆、屋頂)

- 室內裝潢玻璃和隔間

- 特殊應用(防彈/防爆)

- 按最終用戶行業分類

- 汽車和運輸設備

- 建築/施工

- 國防與安全

- 家用電子電器和智慧顯示器

- 其他終端用戶產業(鐵路、航太、海運)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Chang Chun Group

- Eastman Chemical Company

- Everlam

- Genau Manufacturing Company LLP(GMC LLP)

- Guangzhou Aojisi New Material Co., Ltd.

- Huakai Plastic(Chongqing)Co., Ltd.

- Jiangsu Daruihengte Science & Technology Co., Ltd.

- Jinjing(Group)Co., Ltd.

- KB PVB

- Kuraray Co., Ltd.

- Saint-Gobain

- SEKISUI CHEMICAL CO., LTD.

- ZHEJIANG DECENT NEW MATERIAL CO., LTD

第7章 市場機會與未來展望

The Polyvinyl Butyral Interlayers market is expected to grow from USD 4.73 billion in 2025 to USD 5.05 billion in 2026 and is forecast to reach USD 7.01 billion by 2031 at 6.78% CAGR over 2026-2031.

Rising safety regulations, sustainability mandates and the push for lighter vehicles and greener buildings anchor this expansion. Electric-vehicle programs are widening the glazing envelope from the windshield to every window, while LEED-driven construction specifies high-performance laminated facades that curb solar heat gains and block ultraviolet radiation. Manufacturers are unveiling multi-functional films that combine acoustic damping, solar control and bird-collision deterrence, thereby enlarging the addressable opportunity for the polyvinyl butyral interlayers market. At the same time, raw-material cost swings and still-nascent recycling routes squeeze margins and spur vertical integration among leading suppliers.

Global Polyvinyl Butyral (PVB) Interlayers Market Trends and Insights

Growing Adoption of Laminated Safety Glass in Automotive and Construction

Electric-vehicle programs remove the masking effect of engine noise, intensifying OEM demand for side and rear glass that integrates acoustic polyvinyl butyral layers. SEKISUI's latest S-LEC series blocks near-infra-red radiation to trim cabin heat and extend driving range. Architects simultaneously specify oversized laminated panels in high-rise facades, where the interlayer absorbs impact energy and keeps shards bonded for occupant safety. Trans-sector technology transfer shortens development cycles and reinforces the polyvinyl butyral interlayers market as innovations in one end-use quickly migrate to the other.

Regulatory Mandates for Vehicle-Occupant Safety and Glass Strength

The U.S. NHTSA Federal Motor Vehicle Safety Standard 217a comes into effect in 2027 and compels advanced glazing on long-distance buses, materially enlarging the downstream pool for the polyvinyl butyral interlayers market. Similar ECE revisions in Europe focus on pedestrian safety and rollover integrity, driving OEMs toward thicker multi-layer laminates with higher-modulus interlayers. Regulations heighten per-vehicle material loading and reward suppliers capable of formulating impact-resistant films that remain clear under wider temperature ranges.

Price Fluctuations in Polyvinyl Butyral Resins and Additives

SEKISUI raised S-LEC film list prices by 6-15% in October 2024, followed by Eastman adding USD 0.04/lb on plasticizers from April 2025. China's January 2025 tariff lift on PVC imports to 5.5% imposes an incremental USD 22.95-23.85/t cost burden on resin processors. Because OEM contracts often lock prices for model cycles, downstream fabricators face margin compression, prompting consolidation and deeper vertical integration to secure feedstock and hedge volatility across the polyvinyl butyral interlayers market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Energy-Efficient Glazing and UV Protection

- Expansion of Green Buildings and LEED-Certified Construction

- Limitations in Recycling of End-of-Life PVB Interlayers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard films delivered 61.62% of 2025 revenue, underscoring their ubiquity in safety glass. Meanwhile acoustic formats are growing at 7.48% CAGR as electric-vehicle drivetrains expose wind and tire noise. Saflex Q reduces cabin sound pressure by up to 7 dB without process retooling. Multi-functional hybrids that embed acoustic, solar and structural properties in one stack entice automakers to curb part counts. The polyvinyl butyral interlayers market size for acoustic solutions is projected to climb from USD 0.5 billion in 2026 to USD 0.71 billion in 2031, illustrating a shift in value mix. UV-screening and hurricane-rated grades stay niche yet profit-rich, particularly in coastal U.S. and Caribbean construction markets vulnerable to extreme weather.

In competitive terms, portfolio breadth is overtaking unit cost as the decisive lever. Producers offering interchangeable cores that switch from standard to acoustic by adjusting plasticizer ratios optimize plant utilization and win dual-sourcing awards with global OEMs. This capability accelerates cannibalization of legacy films but anchors supplier lock-in, which supports pricing leverage within the polyvinyl butyral interlayers market.

Sheet and roll goods supplied 84.10% of 2025 shipments due to mature logistics and lamination tooling. Yet tailored-cut films, dispensed in project-specific dimensions, are gaining 7.55% CAGR as facade contractors demand waste minimization and faster line speeds. Digital knife and laser systems enable custom layouts that mirror BIM models, reducing on-site trim. The polyvinyl butyral interlayers market share for tailor-made formats reached 15.90% in 2025 and could top 20% by 2031 as urban megaprojects proliferate. Transporting jumbo panels wider than 3.2 m calls for local lamination hubs, encouraging regionalisation of production footprints and alliances between film makers and facade glaziers.

Value creation shifts from resin tonnage to service. Suppliers bundling structural simulation, on-time kit delivery and on-site technical support monetize intangible differentiators difficult for commodity entrants to match. Those capabilities elevate average selling prices even when resin indices soften, insulating margins across the polyvinyl butyral interlayers market.

The Polyvinyl Butyral (PVB) Interlayers Market Report is Segmented by Type (Standard PVB, Acoustic PVB, and More), Form (Sheet/Roll Form, Custom-Cut/Pre-laminated Film), Application (Automotive Windshields, Side and Rear Automotive Glazing, and More), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific produced 44.35% of global revenue in 2025 and is growing at 7.84% CAGR, powered by China's 25-million-unit vehicle output and record-breaking urban construction pace. The January 2025 hike in PVC import tariffs to 5.5% adds USD 23/t to resin costs, nudging glass processors toward domestic PVB film suppliers. India's vehicle-sales expansion and smart-city programs feed additional momentum, albeit from a lower base. Japanese and South Korean champions inject acoustic and solar-control innovation that diffuses through regional supply chains. Meanwhile ASEAN countries attract new lamination capacity, leveraging lower labor costs yet remaining inside Asia's logistical orbit.

North America represents a steady replacement market where stringent NHTSA rules elevate specification levels. The forthcoming 2027 bus-glazing mandate is set to lift demand volumes and complexity. Building retrofits for energy savings, especially in the U.S. Sun Belt, favor solar-control PVB that offsets peak cooling loads. Canada's federal carbon-pricing scheme further tilts renovation choices toward high-insulation glass, widening the addressable slice of the polyvinyl butyral interlayers market.

Europe remains technology-centric, with Extended Producer Responsibility schemes escalating recycling expectations. Tarkett's 2024 breakthrough in reclaiming lamination offcuts shrinks carbon intensity by 25 times relative to virgin PVB. Such advances reposition recycled content from compliance burden to marketing gain. Demand growth is modest, yet product-mix enrichment toward multi-functional and low-carbon interlayers keeps value rising ahead of volume.

South America, the Middle East and Africa together account for under 10% of global turnover but deliver double-digit growth off small bases. Brazil's auto-recovery and Gulf construction mega-projects require heat-resistant, sand-abrasion-tolerant glazing. Suppliers that tailor formulations to tropical climates lock in early influence as regional regulations tighten, setting the stage for future scale in the polyvinyl butyral interlayers market.

- Chang Chun Group

- Eastman Chemical Company

- Everlam

- Genau Manufacturing Company LLP (GMC LLP)

- Guangzhou Aojisi New Material Co., Ltd.

- Huakai Plastic (Chongqing) Co., Ltd.

- Jiangsu Daruihengte Science & Technology Co., Ltd.

- Jinjing (Group) Co., Ltd.

- KB PVB

- Kuraray Co., Ltd.

- Saint-Gobain

- SEKISUI CHEMICAL CO., LTD.

- ZHEJIANG DECENT NEW MATERIAL CO., LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of laminated safety glass in automotive and construction

- 4.2.2 Regulatory mandates for vehicle-occupant safety and glass strength

- 4.2.3 Rising demand for energy-efficient glazing and UV protection

- 4.2.4 Expansion of green buildings and LEED-certified construction

- 4.2.5 Increasing replacement rate of windshields and architectural glass panels

- 4.3 Market Restraints

- 4.3.1 Price fluctuations in Polyvinyl Butyral (PVB) resins and additives

- 4.3.2 Limitations in recycling of end-of-life Polyvinyl Butyral (PVB) interlayers

- 4.3.3 Logistical challenges in transporting large-format rolls

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Standard Polyvinyl Butyral (PVB) Interlayers

- 5.1.2 Acoustic Polyvinyl Butyral (PVB) Interlayers

- 5.1.3 Solar-Control Polyvinyl Butyral (PVB) Interlayers

- 5.1.4 Colored and Tinted Polyvinyl Butyral (PVB) Interlayers

- 5.1.5 UV-Resistant / High-Performance Polyvinyl Butyral (PVB) Interlayers

- 5.2 By Form

- 5.2.1 Sheet / Roll Form

- 5.2.2 Custom-Cut / Pre-laminated Film

- 5.3 By Application

- 5.3.1 Automotive Windshields

- 5.3.2 Side and Rear Automotive Glazing

- 5.3.3 Architectural Glazing (Windows, Facades, Roofs)

- 5.3.4 Interior Decorative Glass and Partitions

- 5.3.5 Specialty (Bullet-, Blast-Resistant)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Defense and Security

- 5.4.4 Consumer Electronics and Smart Displays

- 5.4.5 Other End-user Industries (Rail, Aerospace, Marine)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles {(includes ... Recent Developments)}

- 6.4.1 Chang Chun Group

- 6.4.2 Eastman Chemical Company

- 6.4.3 Everlam

- 6.4.4 Genau Manufacturing Company LLP (GMC LLP)

- 6.4.5 Guangzhou Aojisi New Material Co., Ltd.

- 6.4.6 Huakai Plastic (Chongqing) Co., Ltd.

- 6.4.7 Jiangsu Daruihengte Science & Technology Co., Ltd.

- 6.4.8 Jinjing (Group) Co., Ltd.

- 6.4.9 KB PVB

- 6.4.10 Kuraray Co., Ltd.

- 6.4.11 Saint-Gobain

- 6.4.12 SEKISUI CHEMICAL CO., LTD.

- 6.4.13 ZHEJIANG DECENT NEW MATERIAL CO., LTD

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth in smart-glass and switchable Polyvinyl Butyral (PVB) technologies

- 7.3 Advancement in bio-based and recyclable interlayers