|

市場調查報告書

商品編碼

1906238

油壓缸:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Hydraulic Cylinder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

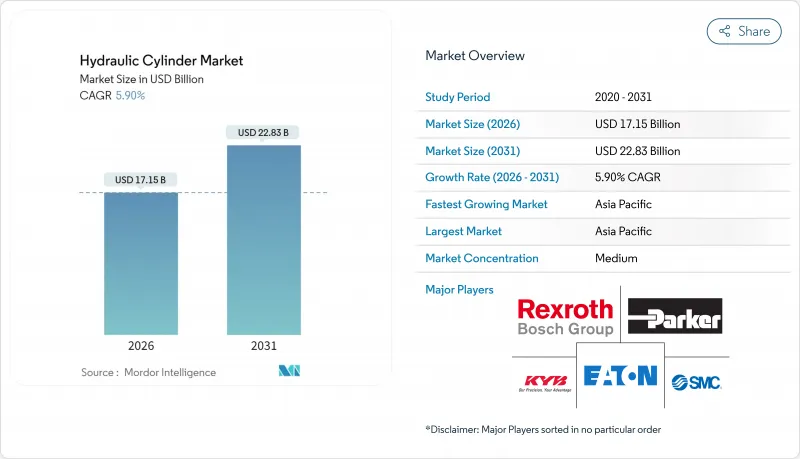

預計油壓缸市場將從 2025 年的 161.9 億美元成長到 2026 年的 171.5 億美元,到 2031 年將達到 228.3 億美元,2026 年至 2031 年的複合年成長率為 5.9%。

基礎設施計劃的強勁資本投資、倉儲自動化的快速發展以及智慧電液解決方案的普及,正在推動油壓缸市場的發展。然而,投入成本的波動和選擇性電氣化正在抑制其成長。施工機械(一台挖土機最多可整合六個液壓缸)和電子商務物流網路對高循環次數的升降傾斜系統的需求,是推動市場成長的主要動力。亞太地區憑藉中國龐大的製造業規模和印度的公共工程支出,維持著市場領先地位;而北美則受益於1.2兆美元的《基礎設施投資和就業創造法案》。在終端市場,供應商正透過整合感測器、物聯網閘道和可再生驅動架構來擴大其競爭優勢,從而降低生命週期能源成本,並透過預測性維護創造新的收入來源。

全球油壓缸市場趨勢與洞察

基礎設施和施工機械繁榮

基礎設施建設支出正帶動對配備多個大噸位液壓缸的挖土機、裝載機和高空作業平台的需求激增。美國聯邦政府的支出正在推動重型設備車隊的成長,提高運轉率。同樣的情況也出現在亞洲,亞洲的離岸能源資本投資較去年同期成長了15%。原始設備製造商(OEM)正在積極應對,指定使用具有能源回收迴路的液壓缸,以減少高達64%的液壓損失,從而降低油耗,並符合企業脫碳政策。利率趨於穩定,縮短了融資週期,這進一步刺激了對高度依賴液壓驅動的小型施工機械的需求。

發展中地區農業機械化的進展

印度、巴西和撒哈拉以南非洲的機械化計畫正在推動曳引機的普及,並增加液壓系統的複雜性。三點式懸吊、裝載臂和轉向輔助系統都依賴能夠在多塵高溫環境下精確控制流量的液壓缸。對水力發電混合動力傳動系統的田間試驗證實,犁地中峰值扭矩降低了18.8%,這表明該技術具有在保持液壓密度的同時節省燃油的潛力。本地組裝設施使製造商能夠規避關稅並縮短前置作業時間,從而增強了農業油壓缸市場的韌性。

輕型應用中電動致動器的快速普及

電動致動器效率提升高達75-80%,且零洩漏,因此在精密包裝、實驗室自動化和小型裝載機等領域越來越受歡迎。其超過1億次的超長循環壽命,也使其在這些細分市場中比液壓系統更俱生命週期成本優勢。儘管油壓缸行業選擇性替代的趨勢仍在繼續,但製造商正透過擴展其混合動力和全電動產品線來降低風險並維持市場佔有率。

細分市場分析

雙作用液壓缸預計將佔2025年總收入的57.74%,以鞏固其在鏟鬥、壓力機和轉向柱設備的雙向負載控制領域在整個油壓缸市場中的地位。整合式壓力感測器提高了精度,使原始設備製造商(OEM)能夠在自動化焊接生產線上實現重複性目標。單作用液壓缸採用重力回油機構,可縮小泵浦的尺寸和液壓油的用量,其複合年成長率將達到5.93%,為剪式升降機和自卸車提供了極具吸引力的折衷方案。再生迴路選項進一步降低了能耗,為注重成本的買家拓展了應用場景。

市場結構分化促使企業採用客製化的籌資策略。大型非公路用車輛製造商簽訂多年期雙作用液壓缸供應協議,採購具有同步流路的液壓缸;而售後市場經銷商則更傾向於模組化的單作用液壓缸產品,以滿足其多樣化的設備需求。能夠在通用加工單元中切換生產兩種不同設計的供應商,可以透過最大限度地減少製程切換期間的停機時間並提高毛利率,從而增強其在油壓缸市場的競爭優勢。

2025年,焊接式汽缸將佔總收入的44.15%,這主要得益於其一體式汽缸體的強度和優異的性價比。農業和礦業原始設備製造商(OEM)正在指定使用壓力高達3000 PSI的焊接式氣壓缸,利用一體式密封圈縮短安裝時間。伸縮式汽缸雖然規模較小,但由於都市區週期。

拉桿式和銑削式液壓缸分別在工廠自動化和金屬加工領域仍然十分重要,因為在這些領域,產品的可維護性和嚴苛的運作條件決定了其選擇。供應商透過專有的密封組件來延長維護週期,並透過滿足工業4.0資料收集要求的在線連續位置感測技術來區分產品。如此廣泛的規格範圍使得油壓缸市場能夠提供功率、行程和運作等各種適用性的選擇。

區域分析

到2025年,亞太地區將佔全球營收的40.62%,年複合成長率達6.73%,主要得益於印度高鐵走廊和中國離岸風力發電擴建等大型企劃的推動。恆力等主要企業正在擴建其垂直整合工廠,以取代進口高階氣瓶,從而縮短前置作業時間並降低到岸成本。供應商的接近性也符合區域整車廠商所採用的準時制生產模式。

北美位居第二,這得益於聯邦政府對基礎設施的投資,用於升級建築車隊和改造內陸港口的物料輸送系統。隨著預測性維護的日益普及,本地製造商正透過先進的冶金技術和數位化整合來滿足終端用戶對資料豐富型設備的需求,從而實現差異化競爭優勢。

在歐洲,對永續性和降噪的重視正推動智慧電液設計的應用,以減少能源浪費。綠色交易指令的立法推動,促使原始設備製造商訂單可生物分解的液壓油和採用防漏技術的液壓缸。

中東地區受原油價格波動影響,液壓缸需求出現波動,但沙烏地阿拉伯天然氣處理設施的擴建帶動了管道建設用大口徑液壓缸訂單的復甦。在非洲和拉丁美洲,農業機械化補貼和採礦特許權為市場提供了利好,但匯率波動給進口商帶來了挑戰。在所有地區,擁有本地服務網路和快速備件供應的供應商在油壓缸市場中都佔據了優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對基礎設施和施工機械的需求不斷成長

- 發展中地區農業機械化的進展

- 電子商務主導了倉儲物料輸送自動化的激增

- 移動機械向電液「智慧」油缸的轉變

- 油壓缸在風力發電機變槳控制的應用日益廣泛

- 航太和國防生產週期恢復

- 市場限制

- 輕型應用中電動致動器的快速普及

- 鋼材價格波動推高了氣瓶的成本結構。

- 舊有系統中的長期維護和洩漏問題

- 採礦和石油天然氣產業的週期性資本支出

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按功能

- 單作用

- 雙動式

- 根據規格

- 焊接

- 拉桿

- 伸縮

- 銑床類型

- 按孔徑

- 小於 50 毫米

- 50至150毫米

- 150毫米或以上

- 按最終用戶行業分類

- 施工機械

- 農業

- 物料輸送和堆高機

- 礦業

- 工業製造

- 航太/國防

- 海洋

- 石油和天然氣

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bosch Rexroth AG

- Parker-Hannifin Corporation

- Eaton Corporation plc

- SMC Corporation

- KYB Corporation

- Caterpillar Inc.

- Enerpac Tool Group Corp.

- Wipro Infrastructure Engineering(division of Wipro Enterprises Pvt. Ltd.)

- Liebherr-International AG

- Jiangsu Hengli Hydraulic Co., Ltd.

- Texas Hydraulics Inc.

- Bucher Hydraulics GmbH

- Aggressive Hydraulics, Inc.

- Festo SE and Co. KG

- Bailey International, LLC

- PMC Hydraulics AB

- HYDAC International GmbH

- Kawasaki Heavy Industries, Ltd.

- Ingersoll-Rand plc(Doosan Portable Power cylinders)

- Caterpillar OEM Solutions(Aftermarket cylinders)

第7章 市場機會與未來展望

The hydraulic cylinder market is expected to grow from USD 16.19 billion in 2025 to USD 17.15 billion in 2026 and is forecast to reach USD 22.83 billion by 2031 at 5.9% CAGR over 2026-2031.

Robust capital spending on infrastructure projects, rapid warehouse automation, and the deployment of smart electro-hydraulic solutions together propel the hydraulic cylinder market, even as input-cost volatility and selective electrification temper expansion. Demand is anchored by construction machinery, where each excavator alone integrates up to six cylinders, and by e-commerce logistics networks that specify high-cycle lift and tilt systems. Asia-Pacific retains primacy on the back of Chinese manufacturing scale and Indian public-works outlays, while North America benefits from the USD 1.2 trillion Infrastructure Investment and Jobs Act. Across end-markets, suppliers widen their moats by embedding sensors, IoT gateways, and regenerative drive architectures that shrink lifetime energy costs and unlock predictive-maintenance revenue streams.

Global Hydraulic Cylinder Market Trends and Insights

Infrastructure and construction-equipment boom

Infrastructure outlays stimulate a cascading need for excavators, loaders, and aerial platforms, each fitted with multiple high-tonnage cylinders. In the United States, federal spending revives heavy-equipment fleets and raises utilization rates, an effect echoed in Asia where offshore-energy capex is growing 15% year-on-year. OEMs respond by specifying cylinders with energy-recovery circuits that save up to 64% of hydraulic losses, cutting fuel burn and aligning with corporate decarbonization mandates. Shorter financing cycles, enabled by stabilizing interest rates, further unlock compact-equipment demand that disproportionately relies on hydraulic actuation.

Rising farm mechanization in developing regions

Mechanization programs in India, Brazil, and sub-Saharan Africa accelerate tractor penetration and elevate hydraulic complexity. Three-point hitches, loader arms, and steering assist all depend on cylinders capable of precise flow-modulation under dusty, high-temperature conditions. Field research on hybrid hydraulic-electric drivelines shows peak-torque cuts of 18.8% during plowing, validating the technology's fuel-savings potential while preserving hydraulic force density. Localized assembly hubs help manufacturers sidestep tariff regimes and shorten lead times, reinforcing the hydraulic cylinder market's resilience in agriculture.

Rapid adoption of electric actuators in light-duty applications

Efficiency gains of 75-80% and zero-leakage operation make electric actuators attractive for precision packaging, lab automation, and compact loaders. High-cycle life beyond 100 million strokes also tilts lifecycle economics away from hydraulics in these niches. Manufacturers mitigate risk by expanding portfolios to include hybrid and all-electric offerings, ensuring wallet-share retention even as the hydraulic cylinder industry experiences selective substitution.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce-led surge in warehouse material-handling automation

- Shift toward electro-hydraulic smart cylinders in mobile machinery

- Volatile steel prices inflating cylinder cost structure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Double-acting designs generated 57.74% of 2025 revenue, cementing their role in two-way load control for buckets, presses, and steering columns across the hydraulic cylinder market. Embedded pressure transducers elevate precision, enabling OEMs to achieve repeatability targets in automated welding lines. Single-acting models post a 5.93% CAGR as gravity-return architectures reduce pump sizing and fluid volume, a compelling trade-off for scissor-lifts and tipper bodies. Regenerative circuit options further cut energy draw, expanding addressable use-cases for cost-sensitive buyers.

The dual-market dynamic fosters tailored sourcing strategies. High-volume off-highway builders lock in multi-year supply agreements for double-acting cylinders with synchronized flow paths, while aftermarket distributors favor modular single-acting SKUs to match heterogeneous equipment fleets. Suppliers that can flex production between the two designs on common machining cells minimize changeover downtime and widen gross-margin spreads, reinforcing their competitiveness within the hydraulic cylinder market.

Welded cylinders contributed 44.15% of 2025 turnover thanks to their one-piece body strength and favorable cost-to-pressure ratio. OEMs in agriculture and mining specify welded models up to 3,000 PSI, leveraging integrated glands that shorten installation time. Telescopic cylinders, despite a smaller base, accelerate at a 6.14% CAGR as urban job-sites demand compact stowed lengths and extended reach. Telematik multi-section systems stretch seven stages without external chains, offering maintenance-free operation and cycle-time advantages.

Tie-rod and mill-type designs retain relevance in factory automation and metals processing respectively, where serviceability or extreme-duty requirements dictate product choice. Vendors differentiate through proprietary seal stacks that extend service intervals and through inline position sensing that satisfies Industry 4.0 data-collection mandates. This broad specification spectrum ensures the hydraulic cylinder market provides fit-for-purpose options across force, stroke, and duty-cycle axes.

The Hydraulic Cylinder Market Report is Segmented by Function (Single-Acting, and Double-Acting), Specification (Welded, Tie-Rod, Telescopic, and Mill-Type), Bore Size (Below 50 Mm, 50-150 Mm, and Above 150 Mm), End-User Industry (Construction Equipment, Agriculture, Material Handling and Forklifts, Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured 40.62% of 2025 revenue and records an 6.73% CAGR, driven by megaprojects such as India's high-speed rail corridors and China's offshore wind build-out. Domestic champions like Hengli scale vertically integrated plants to replace imported high-end cylinders, trimming lead times and landed costs. Supplier proximity also aligns with just-in-time practices adopted by regional OEMs.

North America ranks second, buoyed by federal infrastructure spending that refreshes construction fleets and upgrades inland-port material-handling systems. Local producers differentiate via advanced metallurgy and digital integration, meeting end-user demand for data-rich equipment as predictive-maintenance adoption rises.

Europe emphasizes sustainability and noise reduction, prompting the uptake of smart electro-hydraulic designs that curtail energy waste. OEMs receive legislative stimulus from EU Green Deal directives, spurring orders for cylinders with biodegradable fluids and leak-prevention technologies.

The Middle East sees demand swings tied to oil-price cycles, but gas-processing expansion in Saudi Arabia revives large-bore cylinder orders for pipeline construction. Africa and Latin America benefit from agricultural mechanization subsidies and mining concessions, though currency volatility challenges importers. Across all regions, suppliers that offer localized service networks and rapid spare-parts fulfillment gain advantage in the hydraulic cylinder market.

- Bosch Rexroth AG

- Parker-Hannifin Corporation

- Eaton Corporation plc

- SMC Corporation

- KYB Corporation

- Caterpillar Inc.

- Enerpac Tool Group Corp.

- Wipro Infrastructure Engineering (division of Wipro Enterprises Pvt. Ltd.)

- Liebherr-International AG

- Jiangsu Hengli Hydraulic Co., Ltd.

- Texas Hydraulics Inc.

- Bucher Hydraulics GmbH

- Aggressive Hydraulics, Inc.

- Festo SE and Co. KG

- Bailey International, LLC

- PMC Hydraulics AB

- HYDAC International GmbH

- Kawasaki Heavy Industries, Ltd.

- Ingersoll-Rand plc (Doosan Portable Power cylinders)

- Caterpillar OEM Solutions (Aftermarket cylinders)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure and construction-equipment boom

- 4.2.2 Rising farm mechanization in developing regions

- 4.2.3 E-commerce-led surge in warehouse material-handling automation

- 4.2.4 Shift toward electro-hydraulic "smart" cylinders in mobile machinery

- 4.2.5 Growing use of hydraulic cylinders in wind-turbine pitch control

- 4.2.6 Recovery of aerospace and defense production cycles

- 4.3 Market Restraints

- 4.3.1 Rapid adoption of electric actuators in light-duty applications

- 4.3.2 Volatile steel prices inflating cylinder cost structure

- 4.3.3 Chronic maintenance and leakage issues in legacy systems

- 4.3.4 Cyclical CAPEX in mining and oil and gas sectors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Function

- 5.1.1 Single-Acting

- 5.1.2 Double-Acting

- 5.2 By Specification

- 5.2.1 Welded

- 5.2.2 Tie-Rod

- 5.2.3 Telescopic

- 5.2.4 Mill-Type

- 5.3 By Bore Size

- 5.3.1 Below 50 mm

- 5.3.2 50 - 150 mm

- 5.3.3 Above 150 mm

- 5.4 By End-User Industry

- 5.4.1 Construction Equipment

- 5.4.2 Agriculture

- 5.4.3 Material Handling and Forklifts

- 5.4.4 Mining

- 5.4.5 Industrial Manufacturing

- 5.4.6 Aerospace and Defense

- 5.4.7 Marine

- 5.4.8 Oil and Gas

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Colombia

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Egypt

- 5.5.5.2.5 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bosch Rexroth AG

- 6.4.2 Parker-Hannifin Corporation

- 6.4.3 Eaton Corporation plc

- 6.4.4 SMC Corporation

- 6.4.5 KYB Corporation

- 6.4.6 Caterpillar Inc.

- 6.4.7 Enerpac Tool Group Corp.

- 6.4.8 Wipro Infrastructure Engineering (division of Wipro Enterprises Pvt. Ltd.)

- 6.4.9 Liebherr-International AG

- 6.4.10 Jiangsu Hengli Hydraulic Co., Ltd.

- 6.4.11 Texas Hydraulics Inc.

- 6.4.12 Bucher Hydraulics GmbH

- 6.4.13 Aggressive Hydraulics, Inc.

- 6.4.14 Festo SE and Co. KG

- 6.4.15 Bailey International, LLC

- 6.4.16 PMC Hydraulics AB

- 6.4.17 HYDAC International GmbH

- 6.4.18 Kawasaki Heavy Industries, Ltd.

- 6.4.19 Ingersoll-Rand plc (Doosan Portable Power cylinders)

- 6.4.20 Caterpillar OEM Solutions (Aftermarket cylinders)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

油壓缸活塞密封件市場:材料類型、密封結構、運作類型和最終用途產業分類-全球預測,2026-2032年雙作用油壓缸市場:按缸體類型、缸徑、活塞桿配置、安裝方式、應用和最終用戶產業分類,全球預測,2026-2032年車輛油壓缸市場(按車輛類型、缸體類型、安裝方式、銷售管道、缸徑、行程長度和材料分類)-全球預測,2026-2032年

油壓缸活塞密封件市場:材料類型、密封結構、運作類型和最終用途產業分類-全球預測,2026-2032年雙作用油壓缸市場:按缸體類型、缸徑、活塞桿配置、安裝方式、應用和最終用戶產業分類,全球預測,2026-2032年車輛油壓缸市場(按車輛類型、缸體類型、安裝方式、銷售管道、缸徑、行程長度和材料分類)-全球預測,2026-2032年 油壓缸市場分析及預測(至2035年):依類型、產品類型、應用、材料類型、技術、最終用戶、組件、功能及安裝類型分類

油壓缸市場分析及預測(至2035年):依類型、產品類型、應用、材料類型、技術、最終用戶、組件、功能及安裝類型分類 日本工業油壓缸市場:規模、佔有率、趨勢和預測:按功能、規格、缸徑、最終用途行業和地區分類(2026-2034 年)

日本工業油壓缸市場:規模、佔有率、趨勢和預測:按功能、規格、缸徑、最終用途行業和地區分類(2026-2034 年) 2026年全球油壓缸市場報告

2026年全球油壓缸市場報告 油壓缸市場-全球產業規模、佔有率、趨勢、機會與預測:按功能、產品類型、應用、最終用戶產業、地區和競爭格局分類,2021-2031年日本液壓缸市場報告(按功能、類型、缸徑、應用、最終用途行業和地區分類,2026-2034年)

油壓缸市場-全球產業規模、佔有率、趨勢、機會與預測:按功能、產品類型、應用、最終用戶產業、地區和競爭格局分類,2021-2031年日本液壓缸市場報告(按功能、類型、缸徑、應用、最終用途行業和地區分類,2026-2034年) 油壓缸市場規模、佔有率和成長分析(按缸徑、產品類型、工作原理、應用、產業垂直領域和地區分類)-產業預測,2026-2033年

油壓缸市場規模、佔有率和成長分析(按缸徑、產品類型、工作原理、應用、產業垂直領域和地區分類)-產業預測,2026-2033年 油壓缸市場規模、佔有率和趨勢分析報告:按產品、缸徑、功能、應用、地區和細分市場預測,2026-2033年

油壓缸市場規模、佔有率和趨勢分析報告:按產品、缸徑、功能、應用、地區和細分市場預測,2026-2033年