|

市場調查報告書

商品編碼

1906231

類器官:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Organoids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

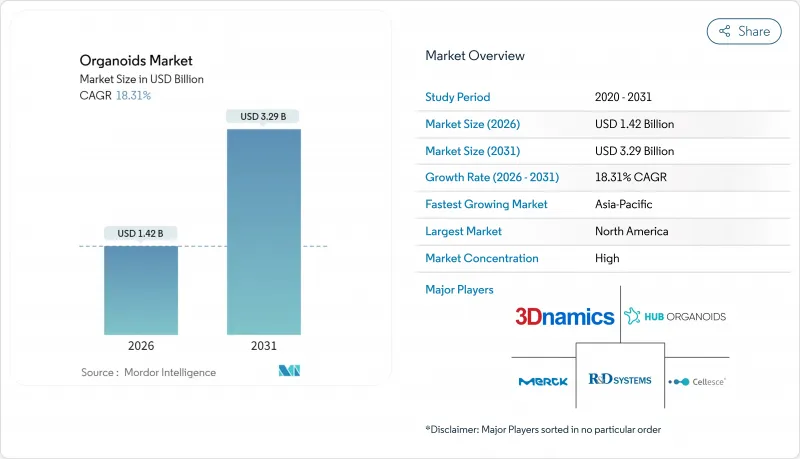

預計類器官市場將從 2025 年的 12 億美元成長到 2026 年的 14.2 億美元,到 2031 年將達到 32.9 億美元,2026 年至 2031 年的複合年成長率為 18.31%。

這一強勁成長是由三大因素共同推動的:監管機構逐步淘汰動物試驗、3D生物列印技術的快速成熟以及製藥業向與人類相關的疾病模型的轉變。史丹佛大學開發的血管化心臟和肝臟類器官克服了以往限制下游生產的尺寸障礙。此外,無基質通訊協定減輕了細胞外水凝膠的成本負擔,而細胞外水凝膠的成本一直是個長期存在的難題。癌症治療計畫依賴患者來源的腫瘤類器官來降低高失敗率,加上動物試驗核准數量的整體下降,這些因素都促進了商業需求,加速了3D人體模型的應用。受託研究機構(CRO)正在擴展其承包類器官服務,隨著小規模生物技術公司將複雜的培養流程外包,進一步推動了類器官市場的發展。

全球類器官市場趨勢與洞察

在癌症藥物開發平臺中快速應用

為了克服癌症藥物研發中高達90%的傳統失敗率,藥廠正將源自患者的腫瘤類器官應用於早期藥物發現。類器官保留了腫瘤的異質性,使得在進行成本高昂的臨床試驗之前,即可基於真實的患者生物學特徵進行多藥聯合篩檢。這種方法能夠即時洞察抗藥性機制,並有助於制定適應性給藥策略。辛辛那提兒童醫院的多區域肝臟類器官在囓齒動物模型中展現出更高的存活率,這表明類器官從靜態疾病模型發展成為功能性組織替代物的複雜性。大型製藥企業之間的競爭體現在它們紛紛設立專門的類器官研發部門、提交知識產權申請以及為3D腫瘤平台投入創業投資資金投資等方面。

利用病患來源的類器官增加精準醫療試驗

類器官指導的臨床試驗正在推動治療方案從群體平均值轉向真正個人化的轉變。一項胰臟癌研究在預測療效方面達到了 83.3% 的敏感性和 92.9% 的特異性,證實了其臨床效用。針對罕見疾病的臨床試驗正在利用類器官在體外模擬疾病,即使患者樣本有限,也能克服招募障礙。 iScience 公司報告了首個人類發炎性腸道疾病移植臨床試驗,標誌著再生類器官療法的臨床應用正式啟動(01343-9)。監管機構正在製定基於類器官的伴隨診斷指南,為未來將預測性檢測與標靶治療相結合的產品鋪平道路。

耗材和專用細胞外基質水凝膠高成本

動物性基質,例如Matrigel,價格昂貴,每毫升售價200-500美元,佔培養成本的60%之多,這限制了其在資金雄厚的實驗室之外的廣泛應用。批次間的差異導致昂貴的檢驗週期,進一步加重了預算負擔。目前市場上湧現的合成或工程水凝膠可望實現價格穩定和批次間一致性的提升。同時,利用低黏附性塑膠和可控攪拌的無基質培養通訊協定的研究有望完全消除細胞外基質(ECM)的輸入,但這些策略需要新的標準操作規程和大量的細胞株重新驗證。

細分市場分析

截至2025年,幹細胞衍生系統將佔據類器官市場62.94%的佔有率,這表明其符合標準化篩檢要求。此細分市場受益於誘導多功能細胞(iPSCs),iPSCs具有在整個生產過程中穩定分化的特性,從而降低了批次間差異,並有助於監管審核。由於成長率可預測且智慧財產權保護清晰,幹細胞驅動的類器官市場目前佔據最大的收入佔有率。腫瘤衍生類器官雖然基數較小,但由於腫瘤中心需要用於治療分層的患者特異性模型,其複合年成長率(CAGR)仍高達19.18%。

誘導多能幹細胞重編程、微流體灌注和多細胞共培養技術的交叉融合,正在擴展幹細胞和腫瘤系統的生理學研究深度。資料共用聯盟已開始存檔與每個細胞系相關的基因組和藥理學特徵,從而實現跨機構的Meta分析。然而,腫瘤來源的模型必須克服移植率和培養壽命方面的異質性,才能達到幹細胞層面的可靠性。

到2025年,藥物發現和篩檢領域將佔類器官市場規模的41.42%,反映出大型製藥企業迫切需要降低研發失敗率並儘早發現毒性風險。高內涵篩檢和微型多孔生物反應器的整合將使每次實驗能夠生產數萬個類器官,接近化合物庫的規模。然而,精準醫療和個人化醫療領域將呈現最高的成長軌跡,複合年成長率將達到19.84%。基於類器官的治療決策,尤其是在結直腸癌和胰腺癌領域獲得監管部門批准,將使該應用場景有望快速獲得醫療保險報銷。

人工智慧流程處理類器官影像分析和單細胞轉錄組學數據,能夠加速先導化合物的篩選,減少人為錯誤,並發現一些反直覺的生物標記。毒理學和疾病建模領域的應用也將隨之而來,尤其是在類器官能夠重現囓齒動物研究中無法實現的器官特異性代謝方面。再生醫學仍是一個新興領域,但成功的臨床前肝臟和甲狀腺移植實驗凸顯了其變革性潛力。

區域分析

北美地區在2025年初貢獻了43.88%的收入,這得益於美國食品藥物管理局(FDA)加速非動物模型研發的藍圖,以及美國衛生研究院(NIH)對史丹佛大學等研究中心的大力資助。美國科技巨頭如賽默飛世爾科技(Thermo Fisher Scientific)投資41億美元收購與類器官工作流程相契合的高純度過濾設備,進一步強化了該領域的生態系統。從多區域肝臟到血管化心臟組織等學術突破正透過技術轉移機構直接整合到商業化產品線。

歐洲擁有強大的學術基礎,荷蘭、德國和英國等國均設有叢集。默克集團收購HUB Organoids公司便是旨在拓展其先進生物學產品組合的策略整合的典範。政策制定者正順應公眾輿論,反對使用動物進行研究,並推動優先發展3D人體模型的津貼體系。儘管由於成員國之間的經濟差異,相關技術的採用率有所不同,但諸如創新藥物舉措(IMI)等泛歐盟計劃正在幫助協調標準和資金流向。

預計亞太地區將成為成長最快的地區,到2031年複合年成長率將達到21.38%。中國的五年規劃已將再生醫學列為重點發展領域,並為大學和Start-Ups提供津貼。這些企業正透過合資企業和智慧財產權共用協議與西方製藥公司合作。日本擁有成熟的細胞療法監管體系,能夠進行早期人體試驗。韓國、澳洲和印度的契約製造資源正在不斷擴展,使該地區成為極具吸引力的低成本試點生產基地。儘管外匯波動和人力資源發展的挑戰構成風險因素,但政府的支持措施和不斷增加的臨床試驗數量為長期發展提供了支持。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在腫瘤藥物研發流程中快速應用

- 利用病患來源的類器官增加精準醫療試驗

- 動物實驗核准的減少推動了3D人體模型的發展

- 政府津貼用於幹細胞和3D培養基礎設施

- 類器官生物樣本庫貨幣化模式的興起

- CRISPR基因編輯的「下一代」類器官引發智慧財產權競賽

- 市場限制

- 高昂的耗材成本和特殊的細胞外基質水凝膠

- 缺乏檢測間重複性標準

- 胚胎樣腸胚研究的倫理檢驗

- 缺乏用於運輸活體類器官的冷藏物流

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 類器官生物樣本庫的現狀

第5章 市場規模與成長預測

- 按類型

- 幹細胞衍生類器官

- 腫瘤來源的類器官

- 透過使用

- 藥物發現與篩檢

- 疾病與毒理學建模

- 精準醫療與個人化醫療

- 再生醫學

- 其他(例如,基因編輯檢驗)

- 最終用戶

- 製藥和生物技術公司

- 學術和研究機構

- 合約研究組織 (CRO) 和合約研發生產力組織 (CDMO)

- 醫院和診斷檢查室

- 透過技術

- 基於支架的3D培養

- 無需支架/漂浮培養

- 整合微流體/晶片器官

- 3D生物列印輔助類器官

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Corning Inc.

- STEMCELL Technologies Inc.

- Lonza Group AG

- Greiner Bio-One International GmbH

- Cellesce Ltd

- Hubrecht Organoid Technology

- Emulate Inc.

- CN Bio Innovations Ltd

- MIMETAS BV

- InSphero AG

- ATCC

- Sartorius AG

- Eppendorf SE

- Miltenyi Biotec BV & Co. KG

- BICO Group AB

- Hubrecht Organoid Biobank(Hub)

- QGel SA

- Advanced BioMatrix Inc.

第7章 市場機會與未來展望

The organoids market is expected to grow from USD 1.20 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 3.29 billion by 2031 at 18.31% CAGR over 2026-2031.

The strong upside rests on three converging forces: regulatory mandates that phase out animal testing, fast-maturing 3-D bioprinting, and the pharmaceutical shift to human-relevant disease models. Vascularized heart and liver organoids created at Stanford remove the size barriers that once limited downstream manufacturing, while matrix-free protocols are easing the long-standing cost burden of extracellular hydrogels. Commercial demand is reinforced by oncology programs that now rely on patient-derived tumor organoids to trim high attrition rates, and by the broader decline in animal-testing approvals that accelerates 3-D human model uptake. Contract research organizations (CROs) are scaling turnkey organoid services, putting additional momentum behind the organoids market as smaller biotechs outsource complex culture workflows.

Global Organoids Market Trends and Insights

Rapid Adoption in Oncology Drug-Discovery Pipelines

Pharmaceutical teams are embedding patient-derived tumor organoids into early discovery to curb the historical 90% failure rate of oncology assets. Organoids conserve tumor heterogeneity, enabling multiple drug combinations to be screened against authentic patient biology before costly clinical trials. The approach supplies real-time insight into resistance mechanisms and informs adaptive dosing strategies. Cincinnati Children's multi-zonal liver organoids, which improved rodent survival, illustrate how organoid complexity now extends beyond static disease modeling toward functional tissue replacement. Competitive urgency among big pharma is reflected in dedicated organoid units, IP filings, and venture funding channelled to 3-D tumor platforms.

Rising Precision-Medicine Trials Using Patient-Derived Organoids

Organoid-guided trials are shifting care from population averages to truly individualized regimens. A pancreatic cancer study achieved 83.3% sensitivity and 92.9% specificity in predicting responses, underscoring clinical relevance. Trials focused on rare diseases leverage organoids to overcome recruitment hurdles, modeling pathologies in vitro with only limited patient samples. iScience reported the first human inflammatory bowel disease transplant trial, marking clinical entry for regenerative organoid therapy (01343-9). Regulators are drafting guidance for organoid-based companion diagnostics, clearing a path for future products that link predictive assays with targeted therapeutics.

High Consumable Costs & Specialized ECM Hydrogels

Animal-derived matrices such as Matrigel cost USD 200-500 per mL and account for up to 60% of culture spend, discouraging widespread adoption outside well-funded labs. Batch variability triggers expensive validation cycles that further inflate budgets. Synthetic or engineered hydrogels now entering the market promise price stability and better lot-to-lot consistency. Parallel research on matrix-free protocols-leveraging low-adhesion plastics and controlled agitation-could eliminate ECM inputs altogether, but these strategies require fresh standard-operating procedures and extensive cell-line requalification.

Other drivers and restraints analyzed in the detailed report include:

- Decline in Animal-Testing Approvals Spurring 3-D Human Models

- CRISPR-Edited "Next-Gen" Organoids Creating IP Race

- Lack of Assay-to-Assay Reproducibility Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stem-cell-derived systems captured 62.94% of organoids market share in 2025, underscoring their suitability for standardized screening requirements. The segment benefits from well-characterized induced pluripotent stem cells that differentiate reliably across production runs, reducing batch variance and easing regulatory audits. The stem-cell-driven organoids market contributes the largest slice of current revenue owing to predictable expansion rates and clear intellectual-property paths. Tumor-derived organoids, while holding a smaller base, are rising at a 19.18% CAGR as oncology centers demand patient-specific avatars for treatment stratification.

The technological intersection of iPSC reprogramming, microfluidic perfusion, and multi-cell co-culture is expanding the physiological depth of both stems and tumor systems. Data sharing consortia have started to archive genomic and pharmacological fingerprints linked to each line, enabling meta-analysis across institutions. Nevertheless, tumor-derived models must still overcome heterogeneity in take rates and culture lifespans before matching stem-cell reliability.

Drug discovery and screening amassed 41.42% of the 2025 organoids market size, reflecting big pharma's urgent need to lower attrition and spot toxic liabilities earlier. Integration of high-content screening with miniaturized multi-well bioreactors now yields tens of thousands of organoids per experiment, approaching compound-library scale. Precision and personalized medicine, however, exhibits the highest trajectory with a 19.84% CAGR. Regulatory recognition of organoid-guided therapy decisions, especially in colorectal and pancreatic cancers, positions this use-case for fast-track reimbursement pathways.

Artificial-intelligence pipelines that parse organoid imaging and single-cell transcriptomics accelerate hit identification, reduce human error, and uncover non-intuitive biomarkers. Toxicology and disease-modeling applications follow closely, especially where organoids replicate organ-specific metabolism absent in rodent studies. Regenerative medicine remains an emerging frontier, yet the successful liver and thyroid preclinical implants underscore its transformative potential.

The Organoids Market Report is Segmented by Type (Stem-Cell-Derived Organoids, Tumor-Derived Organoids), Application (Drug Discovery & Screening, Disease & Toxicology Modelling, and More), End User (Pharmaceutical & Biotech Companies, Academic & Research Institutes, and More), Technology (Scaffold-Based 3-D Culture, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America opened 2025 with 43.88% revenue, buoyed by the FDA roadmap that accelerates non-animal models and by generous National Institutes of Health funding for CuSTOM, Stanford, and other hubs. U.S. conglomerates such as Thermo Fisher Scientific reinforced the ecosystem by allocating USD 4.1 billion to acquire high-purity filtration assets that dovetail with organoid workflows. Academic breakthroughs-from multi-zonal liver to vascularized cardiac tissue-feed directly into commercial pipelines through technology-transfer offices.

Europe sits on a solid academic backbone with clusters in the Netherlands, Germany, and the United Kingdom. Merck KGaA's purchase of HUB Organoids exemplifies strategic consolidation aimed at expanding advanced-biology portfolios. Policymakers align with public sentiment against animal use, driving grant schemes that prioritize 3-D human models. Economic diversity across member states causes uneven adoption rates, but pan-EU initiatives-such as the Innovative Medicines Initiative-help harmonize standards and funding streams.

Asia-Pacific is the fastest-growing territory at 21.38% CAGR to 2031. China's Five-Year Plan prioritizes regenerative medicine, funneling grants to universities and startups that co-develop with Western pharma through joint ventures and IP-sharing arrangements. Japan offers a mature regulatory path for cell-based therapies, enabling earlier human trials. South Korea, Australia, and India are scaling contract manufacturing resources, making the region an attractive site for cost-effective pilot production. While currency fluctuations and training gaps pose risks, government incentives and rising clinical-trial volume underpin long-term expansion.

- Thermo Fisher Scientific

- Merck

- Corning

- Stem Cell Technologies

- Lonza Group

- Greiner Bio One International

- Cellesce

- Hubrecht Organoid Technology

- Emulate

- CN Bio Innovations Ltd

- Mimetas

- InSphero

- ATCC

- Sartorius

- Eppendorf

- Miltenyi Biotec B.V. & Co. KG

- BICO Group AB

- Hubrecht Organoid Biobank (Hub)

- QGel SA

- Advanced BioMatrix Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption in oncology drug-discovery pipelines

- 4.2.2 Rising precision-medicine trials using patient-derived organoids

- 4.2.3 Decline in animal-testing approvals spurring 3-D human models

- 4.2.4 Government grants for stem-cell & 3-D culture infrastructure

- 4.2.5 Organoid biobank monetisation models emerging

- 4.2.6 CRISPR-edited "next-gen" organoids creating IP race

- 4.3 Market Restraints

- 4.3.1 High consumable costs & specialised ECM hydrogels

- 4.3.2 Lack of assay-to-assay reproducibility standards

- 4.3.3 Ethical scrutiny over embryo-like gastruloid work

- 4.3.4 Limited cold-chain logistics for live organoid shipping

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Organoid Biobank Landscape

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Stem-cell-derived Organoids

- 5.1.2 Tumor-derived Organoids

- 5.2 By Application

- 5.2.1 Drug Discovery & Screening

- 5.2.2 Disease & Toxicology Modelling

- 5.2.3 Precision & Personalised Medicine

- 5.2.4 Regenerative Medicine

- 5.2.5 Others (e.g., Gene-editing validation)

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotech Companies

- 5.3.2 Academic & Research Institutes

- 5.3.3 CROs & CDMOs

- 5.3.4 Hospitals & Diagnostics Labs

- 5.4 By Technology

- 5.4.1 Scaffold-based 3-D Culture

- 5.4.2 Scaffold-free / Suspension Culture

- 5.4.3 Micro-fluidic / Organ-on-chip-integrated

- 5.4.4 3-D Bioprinting-assisted Organoids

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Merck KGaA

- 6.3.3 Corning Inc.

- 6.3.4 STEMCELL Technologies Inc.

- 6.3.5 Lonza Group AG

- 6.3.6 Greiner Bio-One International GmbH

- 6.3.7 Cellesce Ltd

- 6.3.8 Hubrecht Organoid Technology

- 6.3.9 Emulate Inc.

- 6.3.10 CN Bio Innovations Ltd

- 6.3.11 MIMETAS BV

- 6.3.12 InSphero AG

- 6.3.13 ATCC

- 6.3.14 Sartorius AG

- 6.3.15 Eppendorf SE

- 6.3.16 Miltenyi Biotec B.V. & Co. KG

- 6.3.17 BICO Group AB

- 6.3.18 Hubrecht Organoid Biobank (Hub)

- 6.3.19 QGel SA

- 6.3.20 Advanced BioMatrix Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2034年全球類器官與球狀體市場機會與策略全球類器官市場:機會與策略展望(至2034年)

2034年全球類器官與球狀體市場機會與策略全球類器官市場:機會與策略展望(至2034年) 類器官及球狀體市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、組件、材料類型、製程、設備分類

類器官及球狀體市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、組件、材料類型、製程、設備分類 全球類器官和球狀體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球類器官和球狀體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 類器官市場按產品類型、技術、應用和最終用戶分類 - 全球預測 2026-2032

類器官市場按產品類型、技術、應用和最終用戶分類 - 全球預測 2026-2032 類器官及球狀體市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

類器官及球狀體市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 類器官和球狀體的全球市場:各類型,各來源,各用途,各終端用戶,各地區-市場規模,產業動態,機會分析,預測(2025年~2033年)2025年全球類器官市場報告

類器官和球狀體的全球市場:各類型,各來源,各用途,各終端用戶,各地區-市場規模,產業動態,機會分析,預測(2025年~2033年)2025年全球類器官市場報告 2021-2031年歐洲類器官市場報告:範圍、細分、動態與競爭分析

2021-2031年歐洲類器官市場報告:範圍、細分、動態與競爭分析 球狀體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按方法、按來源、按應用、按地區和競爭進行細分,2020-2030 年

球狀體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按方法、按來源、按應用、按地區和競爭進行細分,2020-2030 年