|

市場調查報告書

商品編碼

1906192

母粒:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Masterbatch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

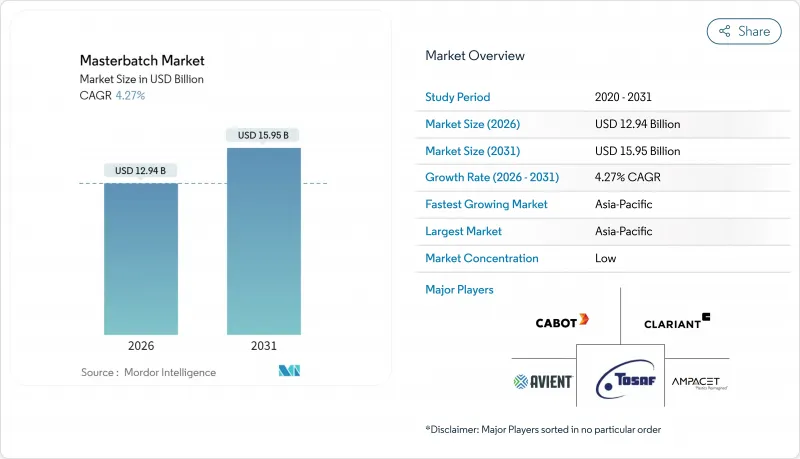

預計到 2026 年,母粒市場規模將達到 159.5 億美元,2026 年至 2031 年的複合年成長率為 4.27%。

儘管原料價格波動,但包裝、汽車輕量化和通訊電纜護套領域的持續需求繼續支撐著市場成長。亞太地區在母粒市場保持主導地位,佔45%的市場佔有率,這主要得益於中國和印度不斷成長的塑膠加工能力。白色配方佔銷售額的32%,因為二氧化鈦基遮光性和紫外線防護仍然是關鍵。各公司正積極應對日益嚴格的全球廢棄物法規,並將研發預算集中在生物基載體、抗菌添加劑以及能夠提升再生聚丙烯性能的配方技術。由於跨國公司專注於永續創新,並試圖抵禦具有成本競爭力的區域供應商,市場競爭強度仍然適中。

全球母粒市場趨勢與洞察

塑膠包裝產業需求不斷成長

在電子商務蓬勃發展和品牌商追求貨架差異化的推動下,包裝行業仍然是色母粒和添加劑濃縮物的最大消費領域。美國和歐盟的食品接觸法規正促使加工商轉向符合FDA和歐盟標準的等級產品,以確保色彩穩定性和加工效率。具有抗菌和阻隔性的產品有助於延長生鮮食品的保存期限,而可回收的載體系統則有助於實現循環經濟目標。科萊恩和安佩斯在母粒市場提供食品級解決方案,這些解決方案不僅滿足遷移限制,還能在大批量生產線上提供一致的色彩。

汽車產業對塑膠的需求不斷成長

為了減輕汽車平臺重量,聚丙烯化合物的應用日益普及,推動了對抗紫外線、耐刮擦和阻燃母粒的需求。 GRAFE 的基礎黑系列產品提供深邃的黑色,無需多道調配工序即可實現經濟高效的內裝著色。此外,OEM 對產品耐久性和降低揮發性有機化合物 (VOC)排放的要求,也進一步推動了對專用添加劑的需求。

原料成本波動為母粒生產商帶來挑戰

二氧化鈦和炭黑的價格受週期性波動的影響,導致濃縮物生產成本上升。這種波動是由於顏料產能中斷、能源價格上漲以及週期性的出口限制造成的。製造商透過尋找多種關鍵顏料來源、簽訂與指數掛鉤的合約以及配製高濃度濃縮物來降低單位使用成本,從而應對這一風險。

細分市場分析

白色濃縮液將在母粒市場佔據最大佔有率,到2025年將佔市場規模的31.40%,這主要得益於其在遮光性和紫外線防護方面的重要作用。高純度二氧化鈦為乳製品瓶、瓶蓋和建築幕牆提供了所需的亮度和耐熱性。受高階包裝、家用電器和汽車內部裝潢建材對具有一致光澤的客製化簾子的需求推動,預計到2031年,彩色母粒的複合年成長率將達到4.67%。黑色產品將繼續保持強勁的需求,以滿足導電性和耐候性產品的需求,同時,特效配方在高階化妝品領域也越來越受歡迎,珠光和金屬顏料被用於提升產品的貨架吸引力。

重新聚焦的永續性目標正推動基於生物基或回收材料的白色和彩色解決方案的發展。為應對顏料價格壓力,供應商正在改進分散技術,以在保持遮蓋力的同時減少二氧化鈦的使用量。同時,色彩開發團隊正在利用數位配色平台,以更低的稀釋度重現品牌顏色,從而縮短新產品的認證週期。

區域分析

預計到2025年,亞太地區將佔全球營收的44.60%,並在2031年之前以4.78%的複合年成長率成長。中國加工商正在推動薄膜、紡織品和汽車零件行業的消費量,而印度加工商則在擴大其在軟包裝和白色家電行業的產能。中國憑藉其龐大的製造基地和不斷成長的國內需求,引領著區域母粒市場的發展,而印度則因其塑膠加工能力的擴張而崛起為重要的成長中心。 [2] 政府對電子製造業的激勵措施正在促進著色劑的在地採購,從而提高區域自主性。可支配收入的成長持續推動對美觀消費品的需求,而這些消費品依賴高性能著色劑。

北美是一個高價值但成熟的市場,其食品接觸應用和汽車行業的標準極為嚴格。美國是該地區銷售的主要驅動力,我們與複合材料生產商緊密合作,開發與化學回收樹脂相容的濃縮液。加拿大包裝製造商使用我們的抗菌配方生產肉類托盤,而墨西哥家電製造商則指定使用我們耐刮的黑色聚丙烯化合物作為外牆面板。

歐洲在先進功能性和環境友善性方面享有盛譽。德國和東歐汽車產業中心對紫外線穩定、低VOC組合藥物的訂單持續穩定。即將推出的歐盟再生材料含量強制令將有利於閉合迴路聚丙烯/聚乙烯體係用母粒。東地中海地區的加工商在利用中東原料優勢的同時,也面臨越來越大的碳邊境調節機制合規壓力。

中東和非洲雖然貢獻較小,但受益於一體化石化聯合企業以具有競爭力的成本供應樹脂和顏料中間體。科萊恩位於沙烏地阿拉伯的工廠正在提高該地區管道、薄膜和纖維製造商所需的著色劑和添加劑濃縮物的供應量。波灣合作理事會(GCC)國家的基礎設施計劃正在刺激對用於電線導管和電纜護套的阻燃和耐候化合物的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 塑膠包裝產業需求不斷成長

- 汽車產業對塑膠的需求不斷成長

- 朝向更輕、更多再生材料含量更高的聚丙烯化合物的轉變,正在推動白色和填充母粒的使用。

- 光纖電纜基礎設施的發展推動了對阻燃母粒的需求。

- 在醫療和衛生產品中的使用量增加

- 市場限制

- 原料成本波動

- 嚴格的環境法規

- 與液體著色劑的競爭

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 白母粒

- 黑母粒

- 母粒

- 添加劑母粒

- 特效母粒

- 透過聚合物

- 聚乙烯

- 聚丙烯

- 高衝擊聚苯乙烯

- 聚氯乙烯

- 聚對苯二甲酸乙二酯

- 其他

- 最終用戶

- 包裝

- 建築/施工

- 汽車/運輸設備

- 電氣和電子設備

- 消費品

- 農業

- 其他(醫療、紡織等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Americhem

- Ampacet Corporation

- Astra Polymers

- Avient Corporation

- Scientific and Production Company "BARS-2"

- BASF

- Cabot Corporation

- Clariant

- Dainichiseika Color and Chemicals Mfg. Co. Ltd.

- Gabriel-Chemie GmbH

- Heubach Group

- Hubron International

- JJPlastalloys

- Penn Color Inc. Masterbatch & Color Concentrates

- Plastiblends

- Plastika Kritis SA

- RTP Company

- Samplast Plast

- Shanghai Janton Industrial Co., Ltd

- Sukano

- Tosaf Compounds Ltd.

第7章 市場機會與未來展望

Masterbatch market size in 2026 is estimated at USD 12.94 billion, growing from 2025 value of USD 12.41 billion with 2031 projections showing USD 15.95 billion, growing at 4.27% CAGR over 2026-2031.

Growth is supported by sustained demand in packaging, automotive lightweighting, and telecom cable jacketing despite raw-material price swings. Asia Pacific retains leadership in the masterbatch market with a 45% revenue share, helped by rising plastic conversion capacity in China and India. White formulations account for 32% of sales because titanium-dioxide-based opacity and UV protection remain indispensable. Companies are directing R&D budgets toward bio-based carriers, antimicrobial additives, and formulations that improve the performance of recyclate-rich polypropylene, aligning with tightening global waste directives. Competitive intensity is moderate as multinationals focus on sustainable innovation to defend share against cost-driven regional suppliers.

Global Masterbatch Market Trends and Insights

Rising Demand in Plastic Packaging Industry

E-commerce growth and brand owners' quest for shelf differentiation keep packaging the single largest consumer of color and additive concentrates. Food contact regulations in the United States and the European Union are steering converters toward FDA- and EU-compliant grades that ensure color stability and processing efficiency. Antimicrobial and oxygen-barrier variants help extend product life in fresh-food formats, while recyclable carrier systems support circular-economy targets. Clariant and Ampacet offer food-grade solutions that allow processors to achieve consistent color across high-throughput lines while meeting migration limits in the masterbatch market.

Increasing Demand of Plastic in Automotive Industry

Vehicle platforms rely on polypropylene compounds to reduce weight, driving uptake of UV-, scratch- and flame-retardant masterbatches. GRAFE's Base Black series provides deep-black shades, enabling cost-effective interior trim coloration without multiple compounding steps. OEM directives for durability and lower volatile organic compound emissions further strengthen demand for purpose-built additive packages.

Feedstock Cost Volatility Challenges Masterbatch Manufacturers

Titanium dioxide and carbon black prices are prone to cyclical swings that inflate concentrate production costs. Volatility stems from pigment capacity outages, rising energy tariffs, and periodic export restrictions. Producers counter this exposure by dual-sourcing critical pigments, negotiating index-linked contracts, and formulating high-loading concentrates that lower cost per application dose.

Other drivers and restraints analyzed in the detailed report include:

- Fiber-Optic Cable Infrastructure Build-out

- Increased Use in Healthcare and Hygiene Products

- Strict Environmental Regulations Impact Product Development

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White concentrates captured the largest 31.40% share of masterbatch market size in 2025, underpinned by their critical role in opacity and UV protection. High-purity titanium dioxide delivers brightness and heat stability needed in dairy bottles, caps, and facades. Color masterbatch is expected to post a 4.67% CAGR to 2031 due to premium packaging, consumer electronics, and automotive interiors seeking custom shades with consistent gloss. The black category retains strong demand in conductive and weatherable products, while special-effect formulations gain traction in luxury cosmetics, using pearlescent and metallic pigments for shelf appeal.

Renewed sustainability goals foster white and color solutions based on bio-sourced or recycled carriers. Suppliers are refining dispersion methods that lower titanium dioxide usage yet maintain opacity to manage pigment price pressure. Meanwhile, color developers exploit digital color-matching platforms to replicate brand hues at lower let-down ratios, shortening qualification cycles for new SKUs.

The Masterbatch Market Report Segments the Industry by Type (White Masterbatch, Black Masterbatch, Colour Masterbatch, Additive Masterbatch, and More), Polymer (Polypropylene, Polyethylene, High Impact Polystyrene, and More), End-User Industry (Building & Construction, Packaging, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific accounted for 44.60% of worldwide revenue in 2025 and is forecast to advance at 4.78% CAGR through 2031. Chinese processors lead volume consumption across film, fiber, and automotive parts, while Indian converters scale capacity in flexible packaging and white goods. China leads the regional masterbatch market due to its massive manufacturing base and growing domestic demand, while India is emerging as a significant growth center with expanding plastics processing capacity[2]. Government incentives for electronics manufacturing encourage local sourcing of color additives, increasing regional self-reliance. Rising disposable incomes continue to uplift demand for aesthetically appealing consumer products that rely on high-performance colorants.

North America represents a high-value but mature market characterized by stringent food-contact and automotive standards. The United States dominates regional sales, collaborating closely with compounders to develop concentrates compatible with chemically recycled resins. Canadian packaging firms adopt antimicrobial formulations for meat trays, and Mexican appliance producers specify scratch-resistant black PP compounds for exterior panels.

Europe maintains its reputation for advanced functionality and eco-compliance. Automotive hubs in Germany and Eastern Europe drive steady orders for UV-stable and low-VOC formulations. Upcoming recycled-content mandates in the European Union favor masterbatches designed for closed-loop polypropylene and polyethylene systems. Eastern Mediterranean processors tap into Middle-East feedstock advantages yet face rising pressure to comply with carbon-border adjustment mechanisms.

The Middle East and Africa, while still a smaller contributor, benefit from integrated petrochemical complexes supplying resin and pigment intermediates at competitive costs. Clariant's Saudi facility improves regional availability of color and additive concentrates for pipe, film, and fiber producers . Infrastructure projects in Gulf Cooperation Council countries stimulate demand for flame-retardant and weatherable compounds in electrical conduits and cable jacketing.

- Americhem

- Ampacet Corporation

- Astra Polymers

- Avient Corporation

- Scientific and Production Company "BARS-2"

- BASF

- Cabot Corporation

- Clariant

- Dainichiseika Color and Chemicals Mfg. Co. Ltd.

- Gabriel-Chemie GmbH

- Heubach Group

- Hubron International

- JJPlastalloys

- Penn Color Inc. Masterbatch & Color Concentrates

- Plastiblends

- Plastika Kritis S.A.

- RTP Company

- Samplast Plast

- Shanghai Janton Industrial Co., Ltd

- Sukano

- Tosaf Compounds Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand in Plastic Packaging Industry

- 4.2.2 Increasing Demand of Plastic in Automotive Industry

- 4.2.3 Shift Toward Lightweight Recyclate Rich PP Compounds Boosting White and Filler Masterbatch Usage

- 4.2.4 Fiber Optic Cable Infrastructure Build out Propelling Flame Retardant Masterbatch Demand

- 4.2.5 Increased Use in Healthcare and Hygiene Products

- 4.3 Market Restraints

- 4.3.1 Feedstock Cost Volatility

- 4.3.2 Strict Environmental Regulations

- 4.3.3 Competition from Liquid Colorants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 White Masterbatch

- 5.1.2 Black Masterbatch

- 5.1.3 Colour Masterbatch

- 5.1.4 Additive Masterbatch

- 5.1.5 Special Effect Masterbatch

- 5.2 By Polymer

- 5.2.1 Polyethylene

- 5.2.2 Polypropylene

- 5.2.3 High Impact Polystyrene

- 5.2.4 Polyvinyl Chloride

- 5.2.5 Polyethylene Terephthalate

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Packaging

- 5.3.2 Building and Construction

- 5.3.3 Automotive and Transportation

- 5.3.4 Electrical and Electronics

- 5.3.5 Consumer Goods

- 5.3.6 Agriculture

- 5.3.7 Others (Healthcare, Textile, etc.)

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Americhem

- 6.4.2 Ampacet Corporation

- 6.4.3 Astra Polymers

- 6.4.4 Avient Corporation

- 6.4.5 Scientific and Production Company "BARS-2"

- 6.4.6 BASF

- 6.4.7 Cabot Corporation

- 6.4.8 Clariant

- 6.4.9 Dainichiseika Color and Chemicals Mfg. Co. Ltd.

- 6.4.10 Gabriel-Chemie GmbH

- 6.4.11 Heubach Group

- 6.4.12 Hubron International

- 6.4.13 JJPlastalloys

- 6.4.14 Penn Color Inc. Masterbatch & Color Concentrates

- 6.4.15 Plastiblends

- 6.4.16 Plastika Kritis S.A.

- 6.4.17 RTP Company

- 6.4.18 Samplast Plast

- 6.4.19 Shanghai Janton Industrial Co., Ltd

- 6.4.20 Sukano

- 6.4.21 Tosaf Compounds Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Rising Demand for Biobased Masterbatch

母粒市場:按類型、聚合物、製程、形態和應用分類-2026-2032年全球市場預測填充母粒市場:2026-2032年全球市場預測(依載體聚合物、產品形式、填充類型、包裝形式、應用、銷售管道和最終用途產業分類)黑母粒市場:按類型、載體樹脂、形態和最終用途產業分類-2026-2032年全球市場預測碳酸鈣填料市場:按形態、等級、類型和最終用途產業分類-2026-2032年全球預測阻燃母粒市場:依聚合物類型、添加劑類型、作用機理、形態、應用及通路分類-全球預測,2026-2032年

母粒市場:按類型、聚合物、製程、形態和應用分類-2026-2032年全球市場預測填充母粒市場:2026-2032年全球市場預測(依載體聚合物、產品形式、填充類型、包裝形式、應用、銷售管道和最終用途產業分類)黑母粒市場:按類型、載體樹脂、形態和最終用途產業分類-2026-2032年全球市場預測碳酸鈣填料市場:按形態、等級、類型和最終用途產業分類-2026-2032年全球預測阻燃母粒市場:依聚合物類型、添加劑類型、作用機理、形態、應用及通路分類-全球預測,2026-2032年 黑母粒市場:市場規模-按地區、應用和預測至2034年

黑母粒市場:市場規模-按地區、應用和預測至2034年 全球阻燃母粒市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球阻燃母粒市場規模、佔有率、趨勢及成長分析報告(2026-2034) 母粒市場報告:按類型、聚合物類型、應用和地區分類(2026-2034 年)

母粒市場報告:按類型、聚合物類型、應用和地區分類(2026-2034 年) 2026年全球母粒市場報告

2026年全球母粒市場報告 永續母粒市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、應用、地區及競爭格局分類,2021-2031年)

永續母粒市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、應用、地區及競爭格局分類,2021-2031年)