|

市場調查報告書

商品編碼

1906137

射頻元件:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)RF Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

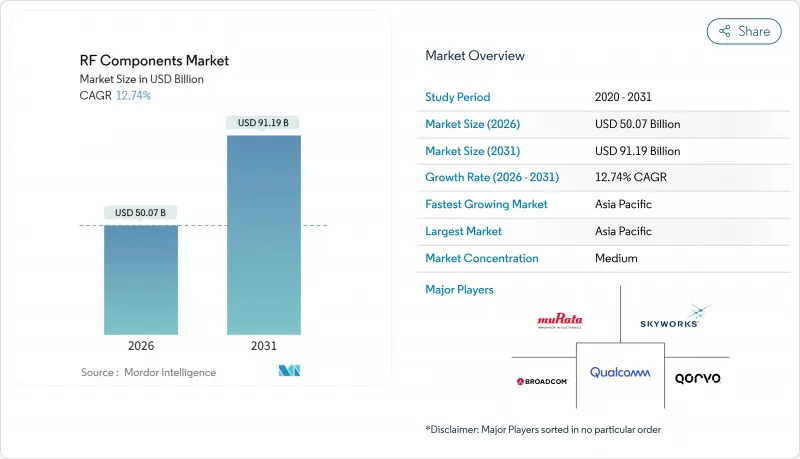

2025年射頻元件市值為444.1億美元,預計2031年將達到911.9億美元,高於2026年的500.7億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 12.74%。

這一成長軌跡反映了5G基地台、以雷達為中心的自動駕駛汽車和太空通訊平台的快速普及。政府推動半導體供應鏈本地化的計劃、40GHz以上頻段的技術突破以及智慧型手機功能的不斷增強,共同推動了市場需求的成長。競爭策略著重於垂直整合、人工智慧輔助設計自動化和先進的溫度控管封裝,這為能夠在性能和成本之間取得平衡並抵禦地緣政治逆風的供應商創造了機會。射頻組件市場也受惠於政策主導的開放式無線存取網(Open RAN)、低地球衛星星系和邊緣人工智慧工業自動化的投資,這些都需要頻率捷變且節能的架構。

全球射頻元件市場趨勢與洞察

5G基礎設施的進步將推動對大型基地台射頻元件的需求。

行動通訊業者持續提升5G大型基地台網路的密度,這就需要能夠承受高熱負荷的高效能功率放大器、低損耗濾波器和波束賦形開關。開放式無線存取網(Open RAN)計劃,特別是4.5億美元的公共無線供應鏈創新基金,強化了這項策略,該基金旨在促進具有多廠商互通性的軟體定義架構。 MaxLinear和RFHIC合作開發的55.2%高效GaN功率放大器,體現了大規模部署中節能的重點。大型基地台的高功率輸出高於小型基地台,這使得擁有成熟GaN製程的供應商具有競爭優勢。政策支援將持續到2027年,從而維持市場需求,為射頻組件市場的中期收入預測奠定堅實基礎。

汽車雷達整合加速了V2X生態系統的發展

具備L3級自動駕駛能力的車輛除了配備專用V2X收發器外,還包含多個77-81GHz雷達感知器,與2023款車型相比,每輛車的射頻組件數量加倍。北美和歐洲的監管機構強制要求高級駕駛輔助系統(ADAS)符合功能安全標準,迫使汽車製造商選擇完全合格的車用級射頻供應商。 ISO 26262認證和FCC Part 15合規性要求進一步限制了供應商的選擇,使其只能選擇可靠性久經考驗的供應商。雷達和V2X雙用途應用增加了設計的複雜性,推動了對既隔離又相容的整合前端模組的需求。高Q值介電材料的前置作業時間仍然很長,造成短期供應風險,並推高了合格庫存的價格。

高昂的資本支出需求限制了GaN/GaAs晶圓廠的擴張。

新建一條化合物半導體生產線可能需要耗資20億至50億美元,台積電位於亞利桑那州的晶圓廠建成後投資將超過1,650億美元。即使有《晶片技術創新與應用法案》(CHIPS Act)的激勵措施,中小規模參與企業在為分子束外延(MOCVD)設備資金籌措方面仍然舉步維艱。 MACOM公司獲得聯邦政府支持的1.8億美元擴建計畫表明,政府援助可以抵消部分資金壁壘,但無法完全消除這些壁壘。長達數年的建設和認證週期將延緩市場准入,促使產業整合,並有利於擁有折舊免稅額資產的現有企業。

細分市場分析

功率放大器將佔據射頻組件市場最大佔有率,到2025年市場規模將達到162.3億美元。它們在大型基地台無線電、雷達模組和家庭閘道器設備中的強大作用支撐了其市場需求,使其在效率提升方面保持領先地位。同時,射頻可調諧裝置市場到2031年將以每年13.74%的速度成長。各公司正在採用這些元件,尤其是在開放式無線存取網(Open RAN)低地球軌道(LEO)終端機中,以利用軟體定義架構簡化網路升級,實現無縫過渡。高通的X85調變解調器-射頻平台整合了人工智慧引擎,可動態調整濾波器和開關,代表著前端技術向更智慧化方向發展。將功率放大器、低雜訊放大器和調諧器整合到單一模組中的供應商,能夠為客戶提供更小的基板面積和更靈活的散熱設計;Qorvo最新的Wi-Fi 7前端模組就體現了這一趨勢。

次要因素也在推動這一趨勢。 5G NR Release 18 中更高階的 MIMO 拓樸結構增加了每個基地台的訊號路徑數量,即使每條路徑的電力消耗降低,也需要更多的功率放大器插槽。在智慧型手機領域,利用非連續載波聚合的 5G 待機模式的普及,推動了天線開關復用和射頻開關出貨量的成長。整合濾波器開關組支援 6GHz 以下頻寬的共存,在保持線性度的同時降低了物料成本。

在LTE和早期5G無線設備的廣泛應用推動下,6GHz以下頻寬仍佔據射頻組件市場62.10%的佔有率。然而,40-100GHz頻寬的成長速度最快,複合年成長率達13.63%,主要得益於企業固定無線接入(FWA)、回程傳輸鏈路以及新興的6G研究走廊。美國電訊資訊管理局(NTIA)就6G應用案例所進行的公眾諮詢凸顯了政府利用這些高頻段進行下一代Gigabit服務的意圖。精通熱敏封裝技術的供應商已做好準備,迎接這波新浪潮。由於毫米波5G在人口密集都市區的熱設計、安裝物流和回程傳輸成本等問題,預計24-40GHz頻段的普及速度將較為緩慢,難以實現大規模部署。

技術成熟度正在推動競爭:整合移相器的變速器整合電路可減小資料中心屋頂鏈路所需的天線孔徑,而氮化鎵/碳化矽功率放大器可在可控漏極電壓下實現更高的EIRP。監管協調,例如FCC的毫米波服務規則,有助於提高確定性,但仍需與現有衛星營運商進行複雜的共存管理。

區域分析

預計到2025年,亞太地區將主導射頻元件市場,佔55.85%的市佔率。這一快速成長主要得益於僅中國就有18家新工廠運作。政府補貼有效降低了單位成本,而與主要原始設備製造商(OEM)的地理位置接近性也提高了市場知名度。韓國和日本在基板材料和濾波陶瓷領域繼續保持主導,而台灣的晶圓代工廠則在多晶片模組的先進封裝技術領域處於領先地位。印度大力推動5G建設,並輔以生產關聯激勵政策(PLI),吸引了後端組裝業務,但該地區目前缺乏大規模晶圓代工廠。即使面臨日益增多的貿易限制,亞太地區的成本優勢仍將確保其在未來十年繼續佔據全球一半以上的出貨量。

北美正受惠於《晶片法案》(CHIPS Act)。台積電位於亞利桑那州的工廠不僅引進了4奈米製程工藝,也讓美國客戶更便捷地獲得先進的射頻封裝技術。此舉顯著降低了物流風險,並加強了國防供應鏈的安全。此外,來自無線創新基金的1.17億美元聯邦津貼正在推動美國國內開放式無線接取網路(RAN)無線電技術的發展,並將業務引向美國的射頻專家。加拿大正在加緊建設中頻段5G通訊基礎設施,但主要依賴美國進口的零件。同時,墨西哥的專業電子代工(EMS)產業正利用低成本的組裝契約,為客戶終端設備(CPE)生產產品。歐洲的目標是到2030年佔據全球半導體市場20%的佔有率,並透過《歐洲晶片法案》(European Chip Act)確立策略自主權。在德國和法國,汽車原始設備製造商(OEM)叢集正在建立符合歐洲新車安全評估協會(Euro NCAP)安全標準的雷達模組生產基地,從而提高了當地晶圓廠的運轉率。英國耗資1,600萬英鎊的低地球軌道(LEO)計畫支持Ka波段組件的研發,並促進新興的太空供應鏈發展。北歐國家正在試行毫米波固定無線接取技術,為農村地區提供寬頻服務,並向美國和日本供應商採購氮化鎵(GaN)前端設備。然而,諸如REACH化學品限制等監管挑戰正在延長組件認證週期,這無意中使那些擁有良好歐洲合規記錄的現有企業受益。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G基礎設施的推進

- 智慧型手機射頻前端組件數量快速成長

- 汽車雷達和V2X技術的廣泛部署

- 政府對太空和近地軌道(LEO)衛星星系的資助

- 射頻能源採集電源管理積體電路的快速普及

- 智慧工廠協作機器人的邊緣人工智慧毫米波感

- 市場限制

- GaN/GaAs晶圓廠的高額資本投入

- 28 GHz 以上的溫度控管挑戰

- 對超寬頻晶片實施更嚴格的出口管制

- 高Q值介電材料的短缺

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 定價分析

第5章 市場規模與成長預測

- 依組件類型

- 功率放大器

- 射頻濾波器

- 天線開關

- 低雜訊放大器

- 射頻可調諧裝置

- 按頻段

- 6GHz 以下頻段

- 6-24 GHz(C/X/Ku 波段)

- 24-40 GHz(毫米波 1)

- 40-100 GHz(毫米波 2)

- 透過半導體材料

- 砷化鎵(GaAs)

- 矽(CMOS/SOI)

- 氮化鎵(GaN)

- 矽鍺(SiGe)

- 按最終用戶行業分類

- 家用電子電器

- 電訊

- 車

- 航太/國防

- 工業自動化

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Broadcom Inc.

- Skyworks Solutions Inc.

- Qorvo Inc.

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors NV

- Qualcomm Incorporated

- Analog Devices, Inc.

- Texas Instruments Incorporated

- STMicroelectronics NV

- Renesas Electronics Corporation

- Infineon Technologies AG

- Cree Wolfspeed Inc.

- Knowles Corporation

- Panasonic Holdings Corporation

- Huawei Technologies Co., Ltd.

- MediaTek Inc.

- ON Semiconductor Corporation

- Teledyne Technologies Incorporated

- Cobham Advanced Electronic Solutions

- Amphenol RF Division

- Airgain Inc.

第7章 市場機會與未來展望

The RF components market was valued at USD 44.41 billion in 2025 and estimated to grow from USD 50.07 billion in 2026 to reach USD 91.19 billion by 2031, at a CAGR of 12.74% during the forecast period (2026-2031).

The growth path reflects surging deployments of 5G base stations, radar-centric autonomous vehicles, and space-based communications platforms. Government programs that localize semiconductor supply chains, breakthroughs in frequencies above 40 GHz, and rising content per smartphone collectively reinforce demand momentum. Competitive strategies emphasize vertical integration, AI-assisted design automation, and advanced thermal packaging, opening opportunities for suppliers able to balance performance and cost while navigating geopolitical headwinds. The RF components market also benefits from policy-driven investments in Open RAN, low-Earth-orbit (LEO) constellations, and edge-AI industrial automation, all of which require frequency-agile, power-efficient architectures.

Global RF Components Market Trends and Insights

5G Infrastructure Densification Drives Macro-Cell RF Dem

Mobile operators continue to densify 5G macro-cell networks, requiring high-efficiency power amplifiers, low-loss filters, and beam-steering switches that can withstand elevated thermal loads. The strategy is reinforced by Open RAN programs, notably the USD 450 million Public Wireless Supply Chain Innovation Fund, which incentivizes multi-vendor interoperability software-defined architectures. Partnerships, such as MaxLinear RFHIC's 55.2% efficiency GaN power amplifier, underline the focus on energy savings for large-scale deployments. As macro cells deliver higher power than small cells, suppliers with a mature GaN process gain a competitive edge. Policy support through 2027 ensures sustained demand, giving the RF components market a strong anchor for mid-term revenue visibility.

Automotive Radar Integration Accelerates V2X Ecosystem Development

Each Level-3-ready vehicle now features multiple 77-81 GHz radar sensors, alongside dedicated V2X transceivers, which doubles the RF content per unit compared to 2023 models. North American and European regulators require advanced driver-assistance systems (ADAS) to meet functional safety norms, nudging OEMs toward fully qualified automotive-grade RF suppliers. ISO 26262 certification and FCC Part 15 compliance further restrict sourcing to vendors with proven reliability records. The dual use of radar and V2X intensifies design complexity, increasing demand for integrated front-end modules that balance isolation and coexistence. Lead times for high-Q dielectric materials remain elevated, posing short-term supply risks yet reinforcing premium pricing for qualified inventories.

High CAPEX Requirements Limit GaN/GaAs Fab Expansion

A new compound-semiconductor line can cost USD 2-5 billion, underscored by TSMC's Arizona outlay that eclipses USD 165 billion when fully built. Even with CHIPS Act incentives, smaller entrants struggle to secure financing for molecular-beam epitaxy MOCVD tools. MACOM's USD 180 million expansion, subsidized by federal backing, illustrates how government aid can offset but not erase capital hurdles. The multiyear build--qualify cycle delays market entry, encouraging consolidation, and favoring incumbents with depreciated assets.

Other drivers and restraints analyzed in the detailed report include:

- Government Space Funding Catalyzes LEO Constellation RF Innovation

- mmWave Thermal Management Creates Technical Differentiation

- Shortage of High-Q Dielectric Materials Constrains Production

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power amplifiers generated the largest slice of the RF components market in 2025, accounting for USD 16.23 billion. Their entrenched role in macro-cell radios, radar modules, home-gateway equipment anchors volume demand, even as efficiency mates intensify. Meanwhile, RF tunable devices compound at 13.74% annually through 2031. Enterprises adopt these components to enable seamless cross-b transition, especially in Open RAN LEO terminals, where software-defined architectures streamline network upgrades. Qualcomm's X85 modem-RF platform integrates an AI engine that dynamically tunes filters and switches, highlighting the march toward smarter front ends. Suppliers that merge power amps, low-noise amps, and tuners into single modules help customers shrink board area while easing thermal budgets, a trend visible in Qorvo's latest Wi-Fi 7 front-end modules.

Second-order effects reinforce this trajectory. Higher-order MIMO topologies in 5G NR Release 18 boost the number of signal paths per base station, multiplying power-amplifier sockets even when per-path wattage tapers. In smartphones, antenna-switch multiplexing rises with 5G STBY modes that leverage non-contiguous carrier aggregation, driving RF switch shipments. Integrated filter-switch banks support coexistence across Sub-6 GHz spectra, preserving linearity while containing BOM costs.

The Sub-6 GHz domain still owns 62.10% of the RF components market share thanks to the sheer footprint of LTE early 5G radios. However, the 40-100 GHz band grows the fastest at a 13.63% CAGR, favored by enterprise fixed-wireless access (FWA), backhaul links, and emerging 6G research corridors. NTIA's public consultation on 6G use cases underscores governmental intent to leverage these higher bands for next-generation gigabit services. Suppliers adept at thermal-conscious packaging position themselves to capitalize on this incremental wave. The 24-40 GHz class observes steady, yet slower, adoption in dense urban mmWave 5G-thermal design, siting logistics, and backhaul costs temper mass rollout velocity.

Technical maturation drives competitive behavior. Beam-steering ICs with embedded phase shifters shrink the antenna aperture needed for data-center roof links, while GaN-on-SiC power amplifiers unlock higher EIRP at manageable drain voltages. Regulatory alignment, such as the FCC's millimeter-wave service rules, fosters certainty but still demands sophisticated coexistence management with satellite incumbents.

The RF Components Market Report is Segmented by Component Type (Power Amplifiers, RF Filters, Antenna Switches, and More), Frequency Band (Sub-6 GHz, 6-24 GHz, and More), Semiconductor Material (GaAs, Silicon, Gan, Sige), End-User Industry (Consumer Electronics, Telecommunication, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, Asia-Pacific dominated the RF components market, claiming a 55.85% share. This surge was largely fueled by the inauguration of 18 new fabs in China alone. Government subsidies have effectively reduced unit costs, and the region's proximity to key OEMs has bolstered visibility. While South Korea and Japan continue to lead in substrate materials and filter ceramics, Taiwan's foundries are at the forefront, providing advanced packaging for multichip modules. India's push for 5G, backed by the Production-Linked Incentive (PLI) scheme, is drawing backend assembly operations, though the country currently lacks a significant wafer-fab scale. Even with rising trade restrictions, Asia-Pacific's cost advantages ensure it anchors over half of the global shipments for the foreseeable decade.

North America is riding the wave of the CHIPS Act. TSMC's facility in Arizona is not only introducing 4-nanometer class processes but also bringing advanced RF packaging closer to U.S. clients. This move significantly reduces logistics risks, bolstering the security of defense supply chains. Additionally, federal grants amounting to USD 117 million, sourced from the wireless innovation fund, are championing domestic Open RAN radio development, steering business towards American RF specialists. While Canada is upgrading its telco infrastructure for mid-band 5G, it predominantly relies on U.S. component imports. Meanwhile, Mexico's EMS sector is capitalizing on low-cost assembly contracts for customer premises equipment (CPE) devices. Europe, eyeing a 20% share of the global semiconductor market by 2030, is positioning itself for strategic autonomy through the European Chips Act. In Germany and France, automotive OEM clusters are anchoring radar modules to meet Euro NCAP safety standards, boosting local fab utilization. The UK's GBP 16 million LEO program is backing Ka-band component R&D, nurturing a nascent space supply chain. Nordic nations are experimenting with millimeter-wave fixed wireless access for rural broadband, procuring GaN front-end equipment from U.S. and Japanese suppliers. However, regulatory challenges, such as the REACH chemistry rules, are extending part qualification cycles, inadvertently benefiting established players with a history of European compliance.

- Broadcom Inc.

- Skyworks Solutions Inc.

- Qorvo Inc.

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors N.V.

- Qualcomm Incorporated

- Analog Devices, Inc.

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Cree Wolfspeed Inc.

- Knowles Corporation

- Panasonic Holdings Corporation

- Huawei Technologies Co., Ltd.

- MediaTek Inc.

- ON Semiconductor Corporation

- Teledyne Technologies Incorporated

- Cobham Advanced Electronic Solutions

- Amphenol RF Division

- Airgain Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G infrastructure densification

- 4.2.2 Surge in RF front-end content per smartphone

- 4.2.3 Rising automotive radar and V2X deployments

- 4.2.4 Government funding for Space and LEO constellations

- 4.2.5 Rapid adoption of RF energy-harvesting PMICs

- 4.2.6 Edge-AI mmWave sensing in smart-factory cobots

- 4.3 Market Restraints

- 4.3.1 High CAPEX for GaN/GaAs wafer fabs

- 4.3.2 Thermal-management challenges above 28 GHz

- 4.3.3 Export-control tightening on ultra-wideband chips

- 4.3.4 Shortage of high-Q dielectric materials

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component Type

- 5.1.1 Power Amplifiers

- 5.1.2 RF Filters

- 5.1.3 Antenna Switches

- 5.1.4 Low-Noise Amplifiers

- 5.1.5 RF Tunable Devices

- 5.2 By Frequency Band

- 5.2.1 Sub-6 GHz

- 5.2.2 6-24 GHz (C/X/Ku)

- 5.2.3 24-40 GHz (mmWave 1)

- 5.2.4 40-100 GHz (mmWave 2)

- 5.3 By Semiconductor Material

- 5.3.1 Gallium Arsenide (GaAs)

- 5.3.2 Silicon (CMOS/SOI)

- 5.3.3 Gallium Nitride (GaN)

- 5.3.4 Silicon-Germanium (SiGe)

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Telecommunication

- 5.4.3 Automotive

- 5.4.4 Aerospace and Defense

- 5.4.5 Industrial Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Broadcom Inc.

- 6.4.2 Skyworks Solutions Inc.

- 6.4.3 Qorvo Inc.

- 6.4.4 Murata Manufacturing Co., Ltd.

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 Qualcomm Incorporated

- 6.4.7 Analog Devices, Inc.

- 6.4.8 Texas Instruments Incorporated

- 6.4.9 STMicroelectronics N.V.

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 Infineon Technologies AG

- 6.4.12 Cree Wolfspeed Inc.

- 6.4.13 Knowles Corporation

- 6.4.14 Panasonic Holdings Corporation

- 6.4.15 Huawei Technologies Co., Ltd.

- 6.4.16 MediaTek Inc.

- 6.4.17 ON Semiconductor Corporation

- 6.4.18 Teledyne Technologies Incorporated

- 6.4.19 Cobham Advanced Electronic Solutions

- 6.4.20 Amphenol RF Division

- 6.4.21 Airgain Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

90度混合耦合器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材質、最終用戶、功能、安裝方法

90度混合耦合器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材質、最終用戶、功能、安裝方法 2026年全球衛星到手機直接蜂窩市場報告2026年全球射頻元件市場報告

2026年全球衛星到手機直接蜂窩市場報告2026年全球射頻元件市場報告 全球高頻元件市場:依頻段、半導體材料、元件類型、終端用戶產業、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測

全球高頻元件市場:依頻段、半導體材料、元件類型、終端用戶產業、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測 全球射頻元件市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球射頻元件市場規模、佔有率、趨勢和成長分析報告(2026-2034) 射頻元件市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、區域及競爭格局分類,2021-2031年)

射頻元件市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、區域及競爭格局分類,2021-2031年) 射頻微波定向耦合器市場:按應用、材料、耦合值、方向性和連接埠配置分類,全球預測(2026-2032年)

射頻微波定向耦合器市場:按應用、材料、耦合值、方向性和連接埠配置分類,全球預測(2026-2032年) 射頻元件市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測

射頻元件市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測 2032 年衛星到行動電話直接通訊市場預測:按組件、衛星軌道、技術、應用、最終用戶和地區進行的全球分析

2032 年衛星到行動電話直接通訊市場預測:按組件、衛星軌道、技術、應用、最終用戶和地區進行的全球分析 全球高頻元件市場

全球高頻元件市場