|

市場調查報告書

商品編碼

1906130

導電塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Electrically Conductive Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

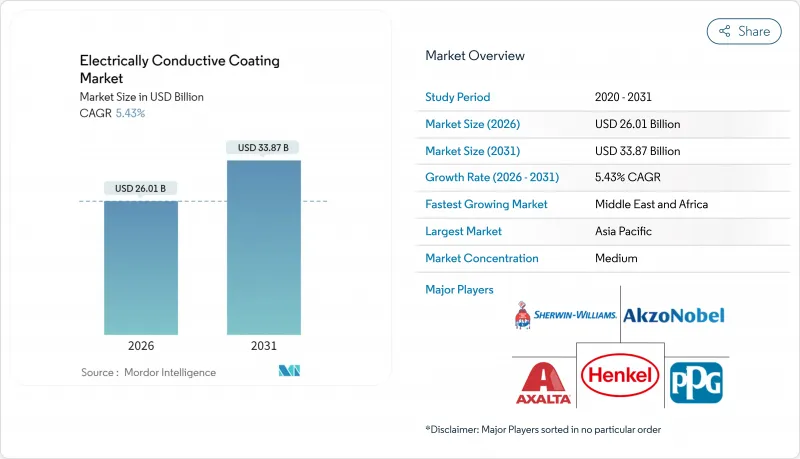

預計導電塗料市場將從 2025 年的 246.7 億美元成長到 2026 年的 260.1 億美元,到 2031 年將達到 338.7 億美元,2026 年至 2031 年的複合年成長率為 5.43%。

導電塗層市場正從傳統的防靜電應用轉向高附加價值的電磁干擾 (EMI) 屏蔽應用,以支援 5G 基礎設施的部署和設備小型化。雖然銀填充丙烯酸酯仍然是主流選擇,但導電塗層市場目前更青睞銅基和聚氨酯基體系,因為它們在導電性、柔軟性和成本方面實現了更好的平衡。亞太地區密集的電子產品供應鏈正在縮短採購週期,而北美和歐洲的原始設備製造商 (OEM) 則願意為具有毫米波屏蔽、熱穩定性和符合 REACH 法規的塗層支付更高的價格。隨著特種材料製造商將奈米填料分散技術應用於從電池機殼到醫療植入等各種領域,競爭對手之間的競爭日益激烈,進一步擴大了導電塗層市場的機會。

全球導電塗佈市場趨勢與洞察

擴展抗靜電應用

在半導體製造廠、無塵室和先進汽車組裝線上,靜電放電控制已成為一項關鍵任務要求,這推動了對既能保持表面電阻率又不增加體積的薄型防靜電層的持續需求。與傳統的炭黑填充系統相比,奈米碳管增強丙烯酸樹脂具有更優異的耐磨性,從而延長了高流量生產區域的維護週期。汽車供應商正在透過對燃油模組和HVAC外殼(這些區域先前缺乏屏蔽要求)進行塗層處理,以響應2024年修訂版IEC 61340測試通訊協定更為嚴格的合格標準。航太和醫療設備製造商正在指定使用低揮發性防靜電薄膜來保護高價值電子產品在洲際運輸過程中的安全,這使得靜電控制成為設計要求,而非事後考慮。

來自電氣和電子行業的需求不斷成長

原始設備製造商 (OEM) 在 CAD 設計階段將塗層融入產品設計,這使得導電塗層市場從主導轉向工程主導型。軟性聚醯亞胺基板和陶瓷複合材料依靠噴塗塗層來貼合不規則形狀的機殼。整合天線的物聯網節點傾向於使用薄聚合物薄膜而非金屬外殼,這要求供應商確保可預測的表面電阻,以防止阻抗不匹配。共同開發契約規定在原型製作階段製程工程師必須協同辦公,從而將材料專業知識融入消費性電子產品藍圖。

重金屬填料的毒性和環境問題。

2024 年 REACH 法規附件 XVIII 的諮詢將把三氧化二銻和氧化鎘列為高度關注物質,這將迫使配方師轉向石墨烯和奈米碳管體系,儘管它們的每公斤價格更高。一級汽車供應商正在利用生命週期評估來評估材料,尤其優先考慮那些報廢後可回收的塗料。醫療和航太的買家現在要求供應商聲明保證鉛和汞不會進入混配過程,這增加了依賴金屬薄片填充的傳統生產線的審核負擔。

細分市場分析

截至2025年,丙烯酸塗料在導電塗料市場中佔比33.58%,這得益於強大的亞洲供應鏈以及符合區域空氣品質法規的水性產品。聚氨酯塗料是成長引擎,其複合年成長率高達5.95%,這主要得益於電動車和穿戴式裝置對彈性的依賴,以承受振動和彎曲。航太領域持續選用耐熱溫度高達200°C的高溫環氧樹脂,這一細分市場雖然穩定,但規模化發展較為罕見。

聚酯樹脂可用於製造低成本的消費品外殼。矽膠樹脂用於保護暴露於原子氧環境中的衛星,而氟聚合物則用於覆蓋需要血液相容性的植入式導線。 ISO 9001通訊協定強調製程的可重複性,從而推動了在線連續電阻率掃描器的研發,該掃描器可對塗層的每一公尺檢驗。終端市場的多元化降低了丙烯酸樹脂的易損性,而向軟性元件的轉變則使聚氨酯成為導電塗層市場未來大規模生產的領導者。

區域分析

到2025年,亞太地區將佔據導電塗層市場47.85%的佔有率,主要得益於中國消費性電子產品的出口和台灣晶圓代工廠產業的蓬勃發展。各地區政府正在補貼本地供應鏈,將前置作業時間時間縮短至數天。韓國的記憶體工廠正在採用與在線連續濺鍍製程相容的塗層,而日本則在為高階混合動力汽車改進零VOC配方技術。北美也將佔據相當大的市場佔有率,因為主要企業需要能夠屏蔽雷達航電的塗層。歐洲正在推廣無添加劑化學技術,以符合未來REACH法規的修訂要求,並正努力將自身打造成為綠色配方中心。

中東和非洲地區預計將以5.75%的複合年成長率成長。這主要得益於阿拉伯聯合大公國自由貿易區的優惠政策,這些政策吸引了專業電子代工。沙烏地阿拉伯正將導電塗層工廠集中到其「2030願景」工業園區,旨在降低對進口的依賴。在南美洲,主要汽車製造商正將其生產基地從亞洲轉移至其他地區,以分散風險,從而形成區域性汽車電子產品生產線,並創造在局部需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大防靜電保護應用

- 來自電氣和電子行業的需求不斷成長

- 5G基礎設施中EMI/RFI屏蔽技術的快速應用

- 穿戴式電子設備的快速小型化

- 用於植入的導電生物相容性塗層的出現

- 市場限制

- 重金屬填料的毒性與環境問題

- 白銀和銅價格波動

- 奈米填料分散問題引起的缺陷

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 丙烯酸樹脂

- 環氧樹脂

- 聚酯纖維

- 聚氨酯

- 其他類型

- 透過導電填料

- 銅

- 鋁

- 銀

- 其他材料類型

- 透過使用

- 電子電器設備

- 車

- 航太/國防

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- A & A Coatings

- Akzo Nobel NV

- Ameetuff Technical Paints Industries

- Axalta Coating Systems

- BeDimensional

- CAIG

- Creative Materials Inc.

- Cromas Paints

- Gelest Inc.

- Henkel AG & Co. KGaA

- Holland Shielding Systems BV

- MG Chemicals

- Parker-Hannifin Corporation

- PPG Industries Inc.

- RS Coatings

- Specialty Coating Systems Inc.

- The Sherwin-Williams Company

第7章 市場機會與未來展望

The Electrically Conductive Coating market is expected to grow from USD 24.67 billion in 2025 to USD 26.01 billion in 2026 and is forecast to reach USD 33.87 billion by 2031 at 5.43% CAGR over 2026-2031.

The electrically conductive coating market is shifting from legacy anti-static roles to value-added electromagnetic interference (EMI) shielding, supporting 5G infrastructure rollouts and device miniaturization. Silver-filled acrylics remain the mainstream choice; however, the electrically conductive coating market now favors copper-based and polyurethane systems that strike a balance between conductivity, flexibility, and cost. Asia-Pacific's dense electronics supply chains keep procurement cycles short, while North American and European original equipment manufacturers (OEMs) pay premiums for coatings that deliver millimeter-wave shielding, thermal stability, and REACH compliance. Competitive rivalry intensifies as specialty materials firms bring nano-filler dispersion know-how to applications ranging from battery enclosures to medical implants, further widening the electrically conductive coating market opportunity.

Global Electrically Conductive Coating Market Trends and Insights

Rising Applications for Anti-Static Protection

Electrostatic discharge control has become mission-critical in semiconductor fabs, cleanrooms, and advanced vehicle assembly lines, driving sustained demand for thin anti-static layers that maintain surface resistivity without adding bulk. Carbon-nanotube-reinforced acrylics exhibit greater abrasion resistance than traditional carbon-black-filled systems, thereby extending maintenance intervals in high-traffic production zones. Automotive suppliers are now coating fuel modules and HVAC housings that previously had no shielding requirements, in response to a 2024 update of IEC 61340 test protocols that tightened pass-fail margins. Aerospace and medical device OEMs specify low-outgassing anti-static films to protect high-value electronics during transcontinental shipment, effectively making static control a default design parameter rather than a last-minute fix.

Growing Demand from Electrical and Electronics Industry

OEMs embed coatings into product architecture at the CAD stage, turning the electrically conductive coating market into an engineering-driven rather than procurement-driven purchase. Flexible polyimide boards and ceramic composites rely on spray-applied coatings that stretch with odd-shaped enclosures. IoT nodes with integrated antennas opt for thin polymeric films over metal cans to prevent detuning, prompting suppliers to ensure predictable surface impedance. Joint-development agreements now stipulate co-location of process engineers during pre-production, embedding material expertise inside consumer-electronics roadmaps.

Toxicity and Environmental Concerns of Heavy-Metal Fillers

REACH Annex XVIII consultations in 2024 flagged antimony trioxide and cadmium oxide as substances of very high concern, compelling formulators to pivot to graphene and carbon nanotube systems, despite higher per-kilogram prices. Automotive tier-1 suppliers utilize life-cycle assessments to evaluate materials, prioritizing coatings based on their recyclability at the end of life. Medical and aerospace buyers now request supplier declarations that no lead or mercury enters the formulation pipeline, adding audit overhead for legacy lines that still rely on metal-flake loading.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Adoption of EMI/RFI Shielding in 5G Infrastructure

- Rapid Miniaturization in Wearable Electronics

- Volatility in Silver and Copper Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics held a 33.58% share of the electrically conductive coating market in 2025, underpinned by robust Asian supply chains and waterborne grades that meet regional air-quality mandates. Polyurethanes are the growth engine, expanding at a 5.95% CAGR as electric vehicles and wearables rely on their elasticity to survive vibration and flexing. Aerospace continues to specify high-temperature epoxies rated to 200 °C, a niche that holds steady but rarely scales.

Polyester chemistries provide low-cost consumer cases. Silicones protect satellites exposed to atomic oxygen, while fluoropolymers cover implantable leads that require hemocompatibility. ISO 9001 protocols have emphasized process repeatability, resulting in inline resistivity scanners that validate every meter of coated film. End-market diversification insulates acrylics, yet the shift to flexible devices positions polyurethanes as the future volume leader within the electrically conductive coating market.

The Electrically Conductive Coating Market Report is Segmented by Type (Acrylics, Epoxy, Polyesters, Polyurethanes, and Other Types), Conductive Filler Material (Copper, Aluminum, Silver, and Other Material Types), Application (Electronics and Electrical, Automotive, Aerospace and Defense, and Other Applications), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 47.85% of the electrically conductive coating market in 2025, anchored by China's consumer-electronics exports and Taiwan's foundry complexes. Regional governments subsidize local supply chains, cutting logistics lead times to days. South Korea's memory fabs embrace in-line sputterable coatings, while Japan refines zero-VOC recipes for high-end hybrid vehicles. North America holds a significant share, where defense primes insist on coatings that shield radar avionics. Europe advances additive-free chemistries to comply with future REACH amendments, positioning itself as the hub for green formulations.

The Middle-East and Africa are projected to grow at a 5.75% CAGR, driven by the United Arab Emirates' free-zone incentives that attract contract electronics manufacturers. Saudi Arabia bundles conductive-coating plants into Vision 2030 industrial parks, thereby reducing its dependence on imports. South America sees localized automotive electronics lines as auto majors diversify beyond Asia for risk mitigation, creating pockets of regional demand.

- A & A Coatings

- Akzo Nobel NV

- Ameetuff Technical Paints Industries

- Axalta Coating Systems

- BeDimensional

- CAIG

- Creative Materials Inc.

- Cromas Paints

- Gelest Inc.

- Henkel AG & Co. KGaA

- Holland Shielding Systems BV

- MG Chemicals

- Parker-Hannifin Corporation

- PPG Industries Inc.

- RS Coatings

- Specialty Coating Systems Inc.

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising applications for anti-static protection

- 4.2.2 Growing demand from electrical and electronics industry

- 4.2.3 Surge in adoption of EMI/RFI shielding in 5G infrastructure

- 4.2.4 Rapid miniaturization in wearable electronics

- 4.2.5 Emergence of conductive bio-compatible coatings for implants

- 4.3 Market Restraints

- 4.3.1 Toxicity and environmental concerns of heavy-metal fillers

- 4.3.2 Volatility in silver and copper prices

- 4.3.3 Dispersion challenges of nano-fillers causing defects

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Acrylics

- 5.1.2 Epoxy

- 5.1.3 Polyesters

- 5.1.4 Polyurethanes

- 5.1.5 Other Types

- 5.2 By Conductive Filler Material

- 5.2.1 Copper

- 5.2.2 Aluminum

- 5.2.3 Silver

- 5.2.4 Other Material Types

- 5.3 By Application

- 5.3.1 Electronics and Electrical

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Egypt

- 5.4.5.4 South Africa

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 A & A Coatings

- 6.4.2 Akzo Nobel NV

- 6.4.3 Ameetuff Technical Paints Industries

- 6.4.4 Axalta Coating Systems

- 6.4.5 BeDimensional

- 6.4.6 CAIG

- 6.4.7 Creative Materials Inc.

- 6.4.8 Cromas Paints

- 6.4.9 Gelest Inc.

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Holland Shielding Systems BV

- 6.4.12 MG Chemicals

- 6.4.13 Parker-Hannifin Corporation

- 6.4.14 PPG Industries Inc.

- 6.4.15 RS Coatings

- 6.4.16 Specialty Coating Systems Inc.

- 6.4.17 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

導電塗層市場報告:趨勢、預測與競爭分析(至2035年)

導電塗層市場報告:趨勢、預測與競爭分析(至2035年) 電泳塗裝市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

電泳塗裝市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年 導電聚合物塗層市場:按類型、應用、終端用戶產業和地區分類

導電聚合物塗層市場:按類型、應用、終端用戶產業和地區分類 導電塗料全球市場報告,2026年

導電塗料全球市場報告,2026年 工業導電塗料市場:依樹脂類型、基材類型、技術、固化類型、形態和應用分類-全球預測,2026-2032年按沉積技術、配方、產品等級、應用和最終用途分類的PEDOT塗層市場,全球預測,2026-2032年

工業導電塗料市場:依樹脂類型、基材類型、技術、固化類型、形態和應用分類-全球預測,2026-2032年按沉積技術、配方、產品等級、應用和最終用途分類的PEDOT塗層市場,全球預測,2026-2032年 全球導電塗料市場導電聚合物塗料市場報告:2031 年趨勢、預測與競爭分析

全球導電塗料市場導電聚合物塗料市場報告:2031 年趨勢、預測與競爭分析 全球導電塗料市場(2024-2028)

全球導電塗料市場(2024-2028)