|

市場調查報告書

商品編碼

1906066

奈米多孔膜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Nanoporous Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

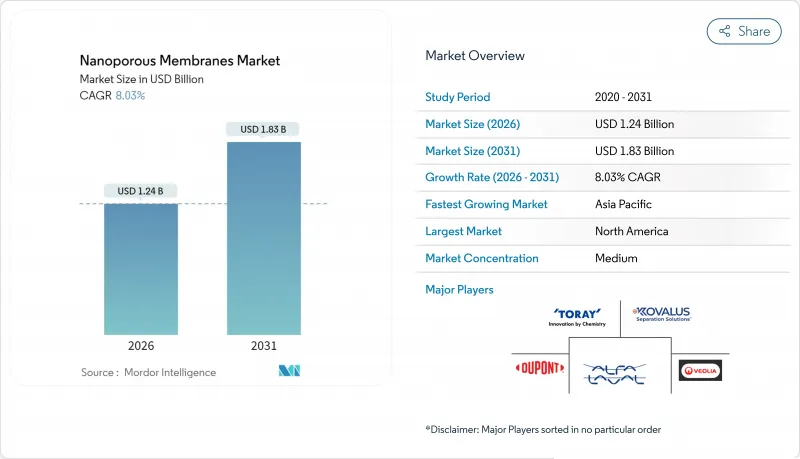

奈米多孔膜市場在 2025 年的價值為 11.5 億美元,預計到 2031 年將達到 18.3 億美元,而 2026 年為 12.4 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 8.03%。

水處理、燃料電池和生物醫學製程對高性能分離技術的需求不斷成長,是推動這一成長的關鍵因素。日益嚴格的工業污水法規、全球範圍內海水淡化廠的大規模建設以及不斷提升的生物處理能力,共同推動了先進膜平台的快速普及。技術供應商正致力於有機-無機混合設計和人工智慧驅動的效能建模,以降低能耗、減少膜污染並縮短企業發展週期。隨著現有企業收購利基創新者以擴大生產規模和應用範圍,競爭日益激烈。

全球奈米多孔膜市場趨勢及洞察

廢棄物和污水再利用的需求日益成長

市政當局和工業業者正在擴大薄膜生物反應器生產線和奈米過濾過濾最終處理流程的規模,以完善水循環,達到飲用水水資源再利用目標,並遵守嚴格的排放法規。香港大學以絲素蛋白為基礎的過濾平台將水質淨化率提高了10倍,同時降低了80%的能耗,展現了目前可實現的顯著效率提升。公共產業優先選擇兼具高污染物去除率和抗污染性能的薄膜材料,推動了對結合生物預處理和奈米級過濾的混合系統的資本投資。隨著資產所有者採用基於績效的契約,對提供預測性維護和低壓設計的供應商的需求日益成長。這正在加速對模組化工廠的投資,這些工廠可以快速部署到缺水的都市區走廊。

提高缺水地區的海水淡化能力

埃及、阿爾及利亞和海灣地區的大規模鹹水和海水淡化中心正推動超高壓逆滲透膜元件的需求達到歷史新高。埃及新建的日處理量達750萬立方公尺的工廠,充分展現了埃及政府目前水安全計畫的規模。歐盟的設施(2,178座工廠,每日處理量686萬立方公尺)正在將可再生能源和能源回收技術融入薄膜處理生產線,以顯著降低營業成本。為此,供應商正在研發能夠處理濃度高達25萬ppm的進水、使用壽命更長且能耐受強效預處理化學品的薄膜材料。地下水開採和鹵水開採的先導計畫對薄膜的耐久性提出了更高的要求,凸顯了複合材料和陶瓷基材在高鹽環境細分市場中的價值。

價格敏感型開發中國家的普及速度緩慢

儘管安全飲用水的需求迫切,但資金限制和熟練勞動力短缺阻礙了膜技術的普及應用。阿爾及利亞的海水淡化藍圖凸顯了資金籌措方面的障礙,即便計劃存量不斷增加。對進口組件的依賴推高了生命週期成本,而本地有限的製造能力又減緩了備件的供應。發展融資舉措正試圖彌補融資缺口,但與需求相比,部署速度仍然緩慢。如果組件製造成本和服務模式無法降低,薄膜技術在農村和郊區的普及應用將仍然有限。

細分市場分析

有機膜佔奈米多孔膜市場規模的63.44%,預計到2031年將以8.47%的複合年成長率成長。其主導地位主要得益於成本效益高的捲對卷生產方式和優異的脫鹽性能。聚醯胺薄膜複合片材兼具高選擇性和可擴展的生產技術,正逐漸成為海水淡化和工業污水處理的主流材料。磺酸鹽聚醚醚酮(PEC)的最新進展為燃料電池提供了一種低成本的質子交換方案,對目前由昂貴的含氟聚合物製成的產品構成了挑戰。

將氧化石墨烯或氧化鋯等無機填料融入聚合物基體的混合型奈米多孔膜設計,是奈米多孔膜市場成長最快的細分領域,它兼具有機械材料的易加工性和陶瓷的耐久性。幾丁聚醣衍生的薄膜採用可再生原料,在維持機械強度的同時,也具有生物分解性,因此深受追求循環經濟概念的顧客青睞。雖然在大批量專案中,純有機系統的製造成本仍然更具優勢,但在高溫、高溶劑環境下,陶瓷膜和混合膜正逐漸佔據一席之地,因為其較高的初始成本可以透過更長的組件使用壽命來彌補。

奈米多孔膜市場報告按材料類型(有機、無機、混合)、應用領域(水處理、燃料電池、生物醫學、食品加工及其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

區域分析

北美地區在嚴格的環境法規和大規模的水利基礎設施預算的推動下,預計到2025年將保持37.20%的收入佔有率。光是德克薩斯州運作60座市政海水淡化廠,日產量達1.72億加侖。沿海海水淡化計劃的可行性研究也正在進行中。該地區也是鋰鹵水純化中心,杜邦公司的FilmTec LiNE-XD奈米過濾線具有高鋰滲透性和二價金屬去除率,專為直接鋰提取製程而設計。

亞太地區預計將以9.22%的複合年成長率成為成長最快的地區,這主要得益於中國龐大的膜製造基地、印度城市水處理設施的擴張以及日本燃料電池供應鏈的不斷完善。中國企業,例如國初科技,正在將膜技術應用於工業、製藥和市政設施,這反映了該地區作為生產國和消費國的雙重角色。新加坡的新生水策略正在推動對抗污染奈米過濾技術的持續研發投入,而東南亞國家則正在採用低壓系統來滿足農村地區的衛生需求。

歐洲是一個成熟而又充滿創新活力的中心,運作2178座海水淡化廠,並且與可再生能源的聯繫日益緊密。一個德國研究聯盟正在測試可降低壓力需求的原子膜,地中海沿岸國家正在試驗使用濃縮鹽水以提高計劃經濟效益。中東和非洲地區,以埃及的世界級海水淡化廠為首,提供了大規模供水的機會,但資金籌措複雜性也隨之增加。在南美洲,巴西和阿根廷的海水淡化建設正在加速推進,儘管仍處於早期階段,但此時正值水資源短缺威脅水力發電可靠性之際。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對廢棄物和污水回收的需求不斷成長

- 提高缺水地區的海水淡化能力

- 更嚴格的工業污水排放標準

- 生物加工中對高純度過濾的需求

- 利用奈米級膜的實驗室晶片實驗室診斷技術

- 市場限制

- 價格敏感型開發中國家的採用率較低

- 堵塞和清潔循環帶來的成本增加

- 特種奈米材料的供應和價格波動;

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依材料類型

- 有機的

- 無機物

- 混合

- 透過使用

- 水處理

- 燃料電池

- 生物醫學

- 食品加工

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alfa Laval

- Applied Membranes Inc.

- AXEON Water Technologies Inc.

- BASF

- DuPont

- Hunan Keensen Technology Co. Ltd

- Hydranautics-A Nitto Group Company

- inopor GmbH

- InRedox LLC

- Kovalus Separation Solutions

- MICRODYN-NADIR GmbH

- Osmotech Membranes Pvt Ltd

- Pure-Pro Water Corporation

- SiMPore Inc.

- SmartMembranes GmbH

- Synder Filtration Inc.

- TORAY INDUSTRIES, INC.

- Veolia

第7章 市場機會與未來展望

The Nanoporous Membranes Market was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.24 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

Growing demand for high-performance separation in water treatment, fuel cells, and biomedical processes is the primary engine behind this expansion. Regulatory tightening on industrial effluents, aggressive global desalination build-outs, and rising bioprocessing throughput needs all favor the rapid adoption of advanced membrane platforms. Technology suppliers are positioning around hybrid organic-inorganic designs and AI-enabled performance modeling to reduce energy use, tackle fouling, and shorten development cycles. Competitive intensity is rising as incumbents acquire niche innovators to secure scale advantages in manufacturing and broaden application coverage.

Global Nanoporous Membranes Market Trends and Insights

Growing Need for Waste- and Waste-Water Re-Use

Municipal and industrial operators are scaling membrane bioreactor lines and nanofiltration polishing steps to close water loops, achieve potable-reuse goals, and meet stringent discharge caps. A silk-based nanofiltration platform from the University of Hong Kong purifies water 10 times faster while cutting energy use by 80%, illustrating the step-change efficiency gains now possible. Utilities prioritize membranes that balance high contaminant rejection with fouling resistance, driving capital spending toward hybrid systems that pair biological pretreatment with nano-scale filtration. As asset owners adopt performance-based contracts, suppliers offering predictive maintenance and low-pressure designs gain traction. The result is accelerating investment in modular plants that can be deployed rapidly in water-scarce urban corridors.

Desalination Capacity Additions in Water-Scarce Regions

Mega-scale brackish and seawater desalination hubs in Egypt, Algeria, and Gulf states are catalyzing record demand for ultra-high-pressure reverse-osmosis elements. Egypt's newly completed 7.5 million m3/day station underscores the volumetric scale now targeted by government water-security programs. EU facilities, 2,178 plants producing 6.86 million m3/day, are layering renewable power and energy-recovery devices onto membrane trains to slash operating costs. Suppliers are, in turn, engineering membranes rated for 250,000 ppm feed, longer lifespans, and harsh pretreatment chemistries. Subsurface intakes and brine-mining pilots add further durability requirements, elevating the value of composite and ceramic substrates in niche high-salinity settings.

Low Adoption in Price-Sensitive Developing Countries

Capital constraints and limited skilled labor curb membrane roll-outs, despite urgent needs for safe water. Algeria's desalination roadmap highlights financing hurdles even as project pipelines swell. Dependence on imported modules inflates life-cycle costs, while sparse local manufacturing capacity delays spare-part deliveries. Development-finance initiatives attempt to bridge funding gaps, yet scaling remains slow relative to demand. Without cost-down advances in module fabrication and service models, adoption in rural and peri-urban centers will remain muted.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Industrial Effluent Discharge Norms

- Bioprocessing Demand for High-Purity Filtration

- Fouling and Cleaning-Cycle Cost Penalties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Organic membranes command 63.44% of the nanoporous membranes market size and are projected for an 8.47% CAGR through 2031, sustaining their lead via cost-effective roll-to-roll production and strong salt-rejection performance. Polyamide thin-film-composite sheets dominate desalination and industrial wastewater service because they marry high selectivity with scalable fabrication. Recent advances in sulfonated poly(ether ether ketone) provide low-cost proton-exchange options for fuel cells, challenging premium fluoropolymer incumbents.

Hybrid designs blending polymer matrices with inorganic fillers such as graphene oxide or zirconia are expanding fastest within the nanoporous membranes market, pairing the processability of organics with ceramic durability. Chitosan-derived membranes highlight renewable feedstocks that add biodegradability while maintaining mechanical integrity, appealing to customers pursuing circular-economy metrics. Manufacturing cost curves still favor pure organics for high-volume bids, yet ceramics and hybrids are gaining footholds in high-temperature, solvent-rich environments where extended module life offsets up-front premiums.

The Nanoporous Membranes Report is Segmented by Material Type (Organic, Inorganic, and Hybrid), Application (Water Treatment, Fuel Cell, Biomedical, Food Processing, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 37.20% revenue lead in 2025 on the back of rigorous environmental oversight and expansive water-infrastructure budgets. Texas alone operates 60 municipal desalination units producing 172 million gallons daily, with coastal seawater projects in feasibility review. The region is also a hotbed for lithium-brine purification, where DuPont's FilmTec LiNE-XD nanofiltration line targets direct-lithium-extraction flows with high lithium passage and divalent-metal rejection.

Asia-Pacific is forecast to register the fastest 9.22% CAGR, buoyed by China's massive membrane manufacturing base, India's urban water-treatment build-out, and Japan's fuel-cell supply-chain expansion. Chinese firms such as Guochu Technology integrate membranes across industrial, pharma, and municipal installations, underscoring the region's dual role as producer and consumer. Singapore's NEWater strategy drives sustained research and development spend on fouling-resistant nanofiltration, while South-East Asian nations adopt low-pressure systems to address rural sanitation needs.

Europe remains a mature yet innovative hub, running 2,178 desalination plants and increasingly pairing them with renewable-energy inputs. German research consortia trial atomically thin membranes to trim pressure requirements, and Mediterranean states are implementing brine-valorization pilots to enhance project economics. The Middle East and Africa, led by Egypt's world-scale desal plant, offer high-volume opportunities balanced against financing complexities. South America's build-outs in Brazil and Argentina are nascent but accelerating as water scarcity dents hydro-power reliability.

- Alfa Laval

- Applied Membranes Inc.

- AXEON Water Technologies Inc.

- BASF

- DuPont

- Hunan Keensen Technology Co. Ltd

- Hydranautics - A Nitto Group Company

- inopor GmbH

- InRedox LLC

- Kovalus Separation Solutions

- MICRODYN-NADIR GmbH

- Osmotech Membranes Pvt Ltd

- Pure-Pro Water Corporation

- SiMPore Inc.

- SmartMembranes GmbH

- Synder Filtration Inc.

- TORAY INDUSTRIES, INC.

- Veolia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Need for Waste- and Waste-Water Re-Use

- 4.2.2 Desalination Capacity Additions in Water-Scarce Regions

- 4.2.3 Stricter Industrial Effluent Discharge Norms

- 4.2.4 Bioprocessing Demand for High-Purity Filtration

- 4.2.5 Lab-on-Chip Diagnostics Adopting Nano-Scale Membranes

- 4.3 Market Restraints

- 4.3.1 Low Adoption in Price-Sensitive Developing Countries

- 4.3.2 Fouling and Cleaning-Cycle Cost Penalties

- 4.3.3 Volatile Supply and Pricing of Specialty Nanomaterials

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Organic

- 5.1.2 Inorganic

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 Water Treatment

- 5.2.2 Fuel Cell

- 5.2.3 Biomedical

- 5.2.4 Food Processing

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market-level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alfa Laval

- 6.4.2 Applied Membranes Inc.

- 6.4.3 AXEON Water Technologies Inc.

- 6.4.4 BASF

- 6.4.5 DuPont

- 6.4.6 Hunan Keensen Technology Co. Ltd

- 6.4.7 Hydranautics - A Nitto Group Company

- 6.4.8 inopor GmbH

- 6.4.9 InRedox LLC

- 6.4.10 Kovalus Separation Solutions

- 6.4.11 MICRODYN-NADIR GmbH

- 6.4.12 Osmotech Membranes Pvt Ltd

- 6.4.13 Pure-Pro Water Corporation

- 6.4.14 SiMPore Inc.

- 6.4.15 SmartMembranes GmbH

- 6.4.16 Synder Filtration Inc.

- 6.4.17 TORAY INDUSTRIES, INC.

- 6.4.18 Veolia

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

奈米多孔膜市場報告:按材料、製造方法、應用和地區分類(2026-2034 年)

奈米多孔膜市場報告:按材料、製造方法、應用和地區分類(2026-2034 年) 奈米多孔膜市場-全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區和競爭細分,2020-2030 年

奈米多孔膜市場-全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區和競爭細分,2020-2030 年 奈米多孔膜市場-2024年至2029年預測

奈米多孔膜市場-2024年至2029年預測