|

市場調查報告書

商品編碼

1906063

聚矽氧烷塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Polysiloxane Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

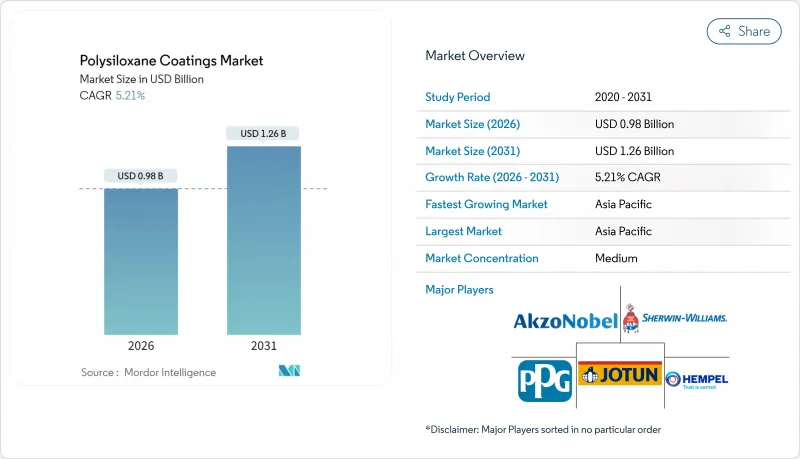

預計聚矽氧烷塗料市場將從 2025 年的 9.3 億美元成長到 2026 年的 9.8 億美元,到 2031 年將達到 12.6 億美元,2026 年至 2031 年的複合年成長率為 5.21%。

在嚴苛的海洋和能源環境中,矽有機混合材料的使用日益增多;新興國家基礎設施投資不斷成長;以及全球揮發性有機化合物(VOC)法規日趨嚴格,這些因素共同推動了市場需求的成長。規範制定者將聚矽氧烷基系統視為延長維護週期、降低生命週期成本以及滿足不斷變化的健康和安全標準的有效途徑,從而為其高價策略奠定了基礎。領先的供應商正大力推廣雙層環氧-聚矽氧烷基塗料,以取代三層富鋅環氧-聚氨酯塗料體系,從而在熟練油漆工短缺的時代降低勞動力需求。同時,超高固態塗料可在不影響邊緣覆蓋率的前提下減少溶劑排放。競爭的重點正轉向樹脂創新、以收購為主導的產品組合建造以及確保訂單重複購買的區域性技術服務項目。

全球聚矽氧烷塗料市場趨勢及洞察

在腐蝕性環境中,海上和頁岩油氣資產的資本投資不斷成長

全球上游業者正增加對深水和頁岩油田的投資,這些油田的鋼材會暴露在高濃度氯化物、二氧化碳和硫化氫的環境中。聚矽氧烷技術只需兩層塗層即可提供必要的C5防護,從而縮短浮體式生產平台在日益狹窄的作業窗口期內的修整時間。與傳統的環氧塗層相比,資產所有者也十分欣賞其減少底漆滲漏的優勢,這一優勢可以延緩飛濺區域高成本的維修工作。近期獲得認證的系統已完成超過15,000小時的鹽霧試驗,並在3,000小時的QUV測試後仍保持85%以上的光澤度,證實了該技術的耐久性。因此,海上承包商正在將聚矽氧烷面漆納入其導管架、甲板和火炬塔的標準維護規範中,作為其延壽計畫的一部分。服務供應商強調,高塗層厚度只需一次交叉噴塗即可提供足夠的邊緣保護,從而緩解偏遠水域勞動力短缺造成的生產力挑戰。

亞洲和非洲的公私合營大型企劃儲備

中國、印度和非洲各國政府正在共同投資建造跨境管道和終端網路,這些網路必須能夠承受濕度波動、沙漠沙礫的磨損以及紫外線照射。聚矽氧烷基塗料即使在-40°C至+120°C的溫度循環中也能保持附著力和柔軟性,從而減少了因地面重塗而導致的停工。工程、採購和施工 (EPC) 聯合體普遍要求符合 ISO 12944 C4 或 C5 標準,而聚矽氧烷基混合塗料只需更少的塗層即可達到此標準。當地安裝人員受益於更快的乾燥速度,從而提高了工作效率——這對於每天施工路段移動數公里的線性計劃至關重要。正如BASF與東方宇虹的合作所表明的那樣,供應商正在深化區域夥伴關係,將全球樹脂技術與現場培訓相結合,以滿足當地的品質標準。東非和東協地區領先的天然氣管道走廊建設進度預示著未來幾年防護領域聚矽氧烷基塗料的銷售將持續成長。

熟練油漆工短缺推高了現場施工成本。

到2025年,美國經NACE認證的噴塗工的平均時薪將超過50美元,在季節性維護高峰期,加班費還會進一步上漲。德國和荷蘭也面臨類似的勞動力短缺問題,老員工的退休速度超過了新員工的入職速度。聚矽氧烷基塗料需要精確的混合比例和露點控制,這將進一步加劇勞動力短缺。僅人事費用一項,就導致船舶修理廠的競標價格比去年同期上漲了15%,迫使一些船東推遲了重新噴漆的周期。製造商正在推出單組分和預混合料套裝來應對這一問題,以減少現場操作,但這些產品的樹脂成本往往更高。雖然塗料供應商和產業協會主導的培訓計畫旨在認證新的噴塗工,但由於招募新員工需要數年時間,預計短期內需求成長將會放緩。

細分市場分析

環氧樹脂-聚矽氧烷混合塗料將在聚矽氧烷塗料市場佔據最大佔有率,預計到2025年將佔總收入的38.86%。其優點在於結合了環氧樹脂的底漆級附著力和矽酮的紫外線穩定性,使得雙層層級構造能夠滿足ISO 12944 C5-M性能標準。在海上平台導管架的現場測試證實,其維護週期可超過15年,進一步降低了勞動力短缺環境下的總擁有成本。這使得終端用戶願意接受更高的價格,並以此為基礎簽訂了平台升級和艦艇維修等長期合約。

儘管市場規模較小,但由於丙烯酸聚矽氧烷雜化材料具有優異的保色性和低泛黃性,其複合年成長率高達5.62%,成為市場上成長最快的產品。郵輪、建築建築幕牆和橋樑梁體計劃等領域對這類材料的需求日益成長。加州和歐洲經濟區 (EEA) 嚴格的揮發性有機化合物 (VOC) 法規進一步推動了水性丙烯酸矽氧烷分散體的普及,這類分散體能夠在不犧牲光澤度的前提下減少溶劑排放。聚酯改質產品利用酯鍵增強耐化學性,在易受酸鹼侵蝕的化工廠中佔有了一席之地。氟化聚矽氧烷混合物和陶瓷填充型產品分別針對極端溫度環境和易受塗鴉的交通設施,凸顯了樹脂化學家致力於開發多功能性能替代方案以取代多層塗料的更廣泛趨勢。最近對室溫固化、無乳化劑的矽酮黏合劑的研究證實了水解應力的降低,表明下一代產品將兼具零 VOC 特性和高機械強度。

區域分析

預計到2025年,亞太地區將佔據聚矽氧烷塗料市場54.88%的佔有率,2026年至2031年的複合年成長率將達到6.55%。這主要得益於中國無可比擬的造船規模和韓國在液化天然氣運輸船建造領域的領先地位。北京大力推動國產海軍艦艇建設,以及「十四五」規劃中260吉瓦離岸風力發電裝置容量的目標,進一步推動了國內需求。在日本,高規格化學品船和浮式儲存再氣化裝置(FSRU)計劃要求使用高矽面漆以防止貨物洩漏,也促進了市場成長。印度的薩加爾馬拉港口開發案以及東協地區模組化造船廠的興起,正在擴大亞太地區的基本客群。

北美地區佔據第二大市場佔有率,這主要得益於墨西哥灣浮體式生產設施的維修、加拿大油砂模組化以及橋樑和機場等聯邦基礎設施更新計劃。美國環保署 (EPA) 將工業維護塗料中揮發性有機化合物 (VOC) 的含量限制在 275 克/公升或以下,這促使資產所有者轉向使用超高固態聚矽氧烷塗料。區域電力公司正在排煙脫硫管中採用這些混合產品,因為其矽酮骨架能夠承受酸性冷凝循環。美國墨加協定 (USMCA) 下的自由貿易物流正在簡化樹脂和顏料的跨境供應,並縮短墨西哥海上工程總承包 (EPC) 設施所需高固態聚矽氧烷產品的前置作業時間。

歐洲仍是一個具有重要戰略意義的市場,並呈現出更穩定的成長態勢。北海的拆船作業和離岸風力發電的升級改造帶動了對維護塗料的需求,而北歐的造船廠正在建造需要低溫固化聚矽氧烷底漆的冰級供應船。歐盟即將實施的環矽氧烷法規正推動市場朝向相容的水性分散體材料快速轉型,該地區也因此成為下一代配方的試驗場。德國高速公路橋樑升級改造工程需要25年的防腐蝕保護,而兩層環氧-聚矽氧烷雙層塗層系統即可實現這一目標,並減少車道封閉時間。中東、非洲和南美洲正在崛起為長期需求中心。巴西的鹽鹽層下FPSO訂單和阿拉伯聯合大公國的港口擴建計劃預計將採用聚矽氧烷技術,以適應高鹽度環境下的延長檢測週期。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 增加對腐蝕性海上和頁岩資產的油氣資本投資

- 亞洲和非洲的公私合營大型企劃儲備

- 從溶劑型材料轉向超高固態混合材料

- 模組化風力塔製造廠數量激增

- 液化天然氣裝運船隻船隊迅速擴張

- 市場限制

- 由於熟練油漆工短缺,現場施工成本不斷上漲

- 對環狀矽氧烷產品的監管審查

- 高溫循環下的邊緣缺陷失效

- 來自氟聚合物面漆的競爭威脅

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧-聚矽氧烷雜化物

- 丙烯酸-聚矽氧烷雜化物

- 聚酯改質聚矽氧烷

- 其他樹脂類型

- 按最終用戶行業分類

- 保護

- 石油和天然氣

- 電力

- 基礎設施

- 海洋

- 其他終端用戶產業

- 保護

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- Akzo Nobel NV

- Asian Paints Ltd.

- Hempel A/S

- Jotun

- KISHO Corporation Co.,Ltd

- Metcon Coatings & Chemicals India Private Limited.

- NCP Coatings LLC

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Thomas Industrial Coatings

- Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- Tikkurila

- Tnemec

- Yung Chi Paint & Varnish MFG. CO.,LTD

第7章 市場機會與未來展望

The Polysiloxane Coatings Market is expected to grow from USD 0.93 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 5.21% CAGR over 2026-2031.

The rising specification of these silicone-organic hybrids in harsh marine and energy settings, along with elevated infrastructure spending in emerging economies and tightening global VOC regulations, collectively underpin demand momentum. Specification engineers view polysiloxane systems as an effective path to extend maintenance cycles, cut life-cycle cost, and comply with evolving health and safety norms, an alignment that reinforces premium pricing power. Major suppliers highlight two-coat epoxy-polysiloxane alternatives that replace three-coat zinc-rich epoxy-polyurethane schemes, thereby reducing labor needs at a time of skilled painter scarcity. Meanwhile, ultra-high-solid variations reduce solvent release without sacrificing edge coverage. Competitive emphasis has therefore shifted to resin innovation, acquisition-led portfolio shaping, and region-specific technical service programs that secure repeat orders.

Global Polysiloxane Coatings Market Trends and Insights

Growing Oil and Gas CAPEX in Corrosive Offshore and Shale Assets

Global upstream operators are channeling new capital toward deep-water and shale prospects that expose steel to high concentrations of chloride, CO2, and H2S. Polysiloxane technology provides the required C5 protection in two coats, reducing trimming time on floating production platforms where weather windows narrow each year. Asset owners also cite lower under-film blistering versus conventional epoxies, a benefit that delays costly touch-ups in splash zones. Recent qualified systems have exceeded 15,000 hours of salt-spray testing while maintaining gloss retention above 85% after 3,000 hours of QUV, reinforcing the technology's durability credentials. Offshore contractors, therefore, embed polysiloxane topcoats in standard maintenance specifications for jackets, decks, and flare towers as part of life-extension programs. Service providers emphasize that high film-build capability enables adequate edge protection with one cross-spray pass, easing productivity hurdles created by labor shortages in remote basins.

Public-Private Megaproject Pipelines in Asia and Africa

Governments in China, India, and several African nations are co-funding cross-country pipelines and terminal networks that must withstand humidity swings, desert sand abrasion, and ultraviolet exposure. Polysiloxane systems retain adhesion and flexibility across -40°C to +120°C cycles, reducing the need for shutdowns to recoat above-ground sections. Engineering, procurement, and construction (EPC) consortia largely mandate ISO 12944 C4 or C5 compliance, a threshold that polysiloxane hybrids reach with fewer coats. Local applicators gain speed benefits from faster touch-dry times, a critical factor on linear projects where kilometer-long spreads move daily. Suppliers deepen regional partnerships-exemplified by BASF and Oriental Yuhong-to blend global resin expertise with on-site training that meets local quality standards. Forward schedules for gas pipeline corridors in East Africa and ASEAN suggest a multi-year tailwind for polysiloxane sales into protective segments.

Skilled-Painter Scarcity Inflating Field-Applied Costs

Average hourly wages for NACE-certified sprayers in the United States exceeded USD 50 in 2025, and overtime premiums escalate further during seasonal maintenance peaks. Similar shortages are also evident in Germany and the Netherlands, as an aging workforce retires faster than newcomers enter. Polysiloxane systems require accurate mix ratios and dew-point control, amplifying the impact of labor gaps. Ship-repair yards report bid prices up 15% year-on-year on labor alone, pushing some owners to postpone repaint cycles. Manufacturers counter with single-component or pre-blended kits that reduce on-site handling, but these variants often carry a higher resin cost. Training initiatives led by coating suppliers and trade associations aim to certify new applicators; however, the pipeline will take years to refill, which will mute near-term volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Transition from Solvent-Borne to Ultra-High-Solid Hybrids

- Rapid Expansion of LNG Carrier Fleet

- Regulatory Scrutiny on Cyclic Siloxane By-Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy-polysiloxane hybrids accounted for the largest share of the polysiloxane coatings market, with a revenue share of 38.86% in 2025. Their dominance stems from the union of epoxy's primer-level adhesion with silicone's UV stability, which together allow a two-layer build to meet ISO 12944 C5-M performance. Field studies on offshore jackets confirm maintenance intervals above 15 years, a result that amplifies total cost-of-ownership savings when labor is scarce. End-users thus perceive price premiums as acceptable, anchoring long-term contracts for platform upgrades and naval refits.

Acrylic-polysiloxane hybrids, although having a smaller base, boast the quickest 5.62% CAGR due to their superior color retention and low yellowing, which appeal to cruise vessels, architectural facades, and bridge girder projects. Strict VOC limits in California and the European Economic Area further steer specifiers toward water-based acrylic-siloxane dispersions that release fewer solvents without sacrificing gloss. Polyester-modified grades carve a niche in chemical plants exposed to acids and alkalis, leveraging ester linkages to boost chemical resistance. Fluorinated polysiloxane blends and ceramic-filled variants target extreme-temperature units and graffiti-prone transit structures, respectively, underscoring a broader trend: resin chemists seek multi-attribute performance to replace multi-coat stacks. Recent lab work on room-temperature-curing emulsifier-free silicone binders reduces hydrolytic stress, suggesting next-generation offerings will merge zero-VOC status with higher mechanical strength.

The Polysiloxane Coatings Market Report is Segmented by Resin Type (Epoxy-Polysiloxane Hybrids, Acrylic-Polysiloxane Hybrids, Polyester-Modified Polysiloxane, and Other Resin Types), End-User Industry (Protective, Marine, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured a 54.88% share of the polysiloxane coatings market in 2025 and is set to log a 6.55% CAGR from 2026-2031, anchored by China's unrivaled shipbuilding scale and South Korea's dominance in LNG vessel construction. Beijing's push for locally built naval ships and the country's 14th Five-Year Plan, which targets 260 GW of offshore wind capacity, intensifies domestic demand for these products. Japan contributes through high-spec chemical carriers and FSRU projects that specify silicone-rich topcoats to resist cargo spillage. India's Sagarmala port upgrade and the growth of modular fabrication yards across ASEAN widen the regional customer pool.

North America holds the second-largest share, driven by the Gulf of Mexico's floating production unit refurbishment, the modularization of Canadian oil sands, and federal infrastructure renewal projects across bridges and airports. The US EPA's aim to clamp VOCs below 275 g/L in industrial maintenance coatings steers asset owners toward ultra-high-solid polysiloxane systems. Regional power-utilities adopt these hybrids for flue-gas desulfurization ducting because silicone backbones withstand acidic condensation cycles. Free-trade logistics under USMCA streamline cross-border resin and pigment supply, lowering lead times for high-build polysiloxane shipments into Mexican offshore EPC hubs.

Europe shows steadier growth yet stays strategically important. North Sea decommissioning and wind-farm repowering generate maintenance coatings work, while Nordic yards fabricate ice-class supply vessels requiring low-temperature cure polysiloxane primers. The upcoming EU cyclic-siloxane restriction drives early conversion to compliant water-based dispersions, making the region a test bed for next-generation formulations. Germany's autobahn bridge renewal program specifies 25-year anti-corrosion performance, a target that epoxy-polysiloxane duplex systems can meet in two layers, thereby curbing lane-closure days. Middle East & Africa and South America emerge as long-term demand centers. Brazil's pre-salt FPSO backlog and UAE's port expansions are likely to adopt polysiloxane technology to meet extended inspection cycles in hot saline environments.

- Akzo Nobel N.V.

- Asian Paints Ltd.

- Hempel A/S

- Jotun

- KISHO Corporation Co.,Ltd

- Metcon Coatings & Chemicals India Private Limited.

- NCP Coatings LLC

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Thomas Industrial Coatings

- Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- Tikkurila

- Tnemec

- Yung Chi Paint & Varnish MFG. CO.,LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing oil and gas CAPEX in corrosive offshore and shale asset

- 4.2.2 Public-private megaproject pipelines in Asia and Africa

- 4.2.3 Transition from solvent-borne to ultra-high-solid hybrids

- 4.2.4 Surge of modular wind-tower fabrication yards

- 4.2.5 Rapid expansion of LNG carrier fleet

- 4.3 Market Restraints

- 4.3.1 Skilled-painter scarcity inflating field-applied costs

- 4.3.2 Regulatory scrutiny on cyclic siloxane by-products

- 4.3.3 Edge-defect failures under high-temperature cycling

- 4.3.4 Competitive threat from fluoropolymer top-coats

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy-Polysiloxane Hybrids

- 5.1.2 Acrylic-Polysiloxane Hybrids

- 5.1.3 Polyester-Modified Polysiloxane

- 5.1.4 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Protective

- 5.2.1.1 Oil and Gas

- 5.2.1.2 Power

- 5.2.1.3 Infrastructure

- 5.2.2 Marine

- 5.2.3 Other End-user Industries

- 5.2.1 Protective

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints Ltd.

- 6.4.3 Hempel A/S

- 6.4.4 Jotun

- 6.4.5 KISHO Corporation Co.,Ltd

- 6.4.6 Metcon Coatings & Chemicals India Private Limited.

- 6.4.7 NCP Coatings LLC

- 6.4.8 PPG Industries, Inc.

- 6.4.9 The Sherwin-Williams Company

- 6.4.10 Thomas Industrial Coatings

- 6.4.11 Tianjin Jinhai Special Coatings & Decoration Co., Ltd.

- 6.4.12 Tikkurila

- 6.4.13 Tnemec

- 6.4.14 Yung Chi Paint & Varnish MFG. CO.,LTD

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment

遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)電子束固化塗料市場:依樹脂類型、配方、設備類型及應用分類-2026-2032年全球市場預測前表面塗料市場:2026-2032年全球市場預測(依產品種類、裝飾性塗料類型、價格範圍、包裝規格、應用、最終用戶產業及通路分類)

遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)電子束固化塗料市場:依樹脂類型、配方、設備類型及應用分類-2026-2032年全球市場預測前表面塗料市場:2026-2032年全球市場預測(依產品種類、裝飾性塗料類型、價格範圍、包裝規格、應用、最終用戶產業及通路分類) 塗料和清漆市場規模、佔有率和成長分析:按產品類型、配方技術、樹脂材料、應用和地區分類-2026-2033年產業預測地毯背襯塗層市場:塗層材料、背襯類型、安裝方法和最終用途—2026-2032年全球市場預測彩色抗蝕劑材料市場:按應用、終端用戶產業、技術、類型、形態和工作分類-2026年至2032年全球市場預測

塗料和清漆市場規模、佔有率和成長分析:按產品類型、配方技術、樹脂材料、應用和地區分類-2026-2033年產業預測地毯背襯塗層市場:塗層材料、背襯類型、安裝方法和最終用途—2026-2032年全球市場預測彩色抗蝕劑材料市場:按應用、終端用戶產業、技術、類型、形態和工作分類-2026年至2032年全球市場預測 全球高性能塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034)溫度反應塗料市場:依技術、配方、溫度範圍及最終用途產業分類-2026-2032年全球市場預測套模塗層市場:依材料類型、塗層類型、基材類型、形狀、最終用途產業、應用方法和功能分類-2026-2032年全球預測高性能航太塗料市場:按平台、技術、產品類型、最終用途和應用分類-2026-2032年全球預測

全球高性能塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034)溫度反應塗料市場:依技術、配方、溫度範圍及最終用途產業分類-2026-2032年全球市場預測套模塗層市場:依材料類型、塗層類型、基材類型、形狀、最終用途產業、應用方法和功能分類-2026-2032年全球預測高性能航太塗料市場:按平台、技術、產品類型、最終用途和應用分類-2026-2032年全球預測