|

市場調查報告書

商品編碼

1906021

滑線測井服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Slickline Logging Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

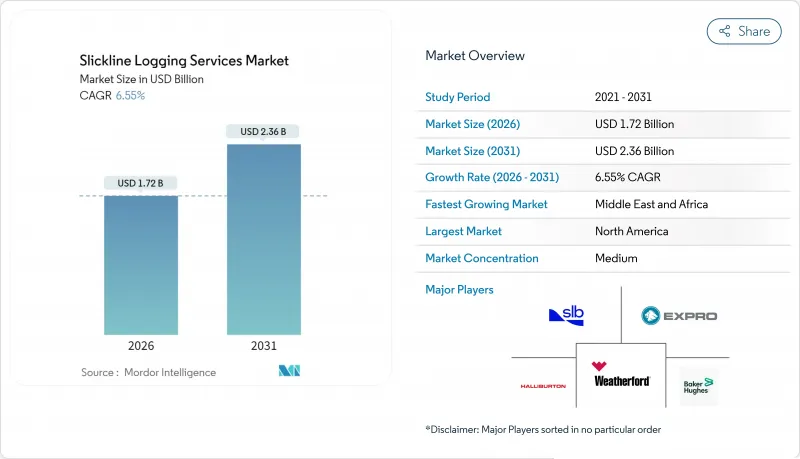

2025年,滑線測井服務市場價值為16.1億美元,預計2031年將達到23.6億美元,高於2026年的17.2億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.55%。

需求成長主要受以下因素驅動:營運商傾向於生產最佳化;深水和超深水計劃持續增加;以及數位化滑線平台快速普及,這些平台無需停產即可進行即時井下診斷。其他支援因素包括:老舊油井積壓日益增多;國家石油公司競標綜合服務;以及新興的碳捕獲試驗計畫,這些項目需要微創測井。人工智慧和自主作業技術的不斷進步,正在將傳統的機械維修作業轉變為數據驅動型干涉措施,從而延長資產壽命並降低開採成本。

全球滑線測井服務市場趨勢與洞察

深海和超深海鑽探的永續升級再造

預計到2025年,深水鑽井鑽機運轉率將維持在82%,這支撐了強勁的日租金,並滿足了在極端壓力和溫度條件下對可靠的滑線作業的需求。伍德賽德公司的Trion開發計劃(水深2500米,共18口井)等項目表明,地層評估和井完整性監測的持續需求源自於其複雜性。各國石油公司正將滑線服務納入多年期綜合鑽井契約,以實現營運協同效應並減少鑽機移動。即時滑線診斷技術與人工智慧鑽探平臺整合,以維持井控並最佳化儲存接觸。在偏遠水域進行的長期宣傳活動提升了多功能滑線管柱的價值,這些管柱無需額外調動即可完成機械作業、測井作業和清理作業。

老舊油井的干涉成本不斷增加

2030年,全球26萬口在運作中油井中約有三分之二的井齡將超過10年,預計全球井下作業支出將達到580億美元,業者的目標是使每口井的平均產量提高10%。滑線已從簡單的機械維修發展到配備高清攝影機和電子儀表的平台,為鑽井平台作業提供了一種成本更低的替代方案。北海業者正在試驗利用滑線進行跨接氣舉作業,預計將深水維修成本降低一半。其他應用包括機器人篩管回收和化學藥劑注入,這兩項技術都增強了針對性干預而非新鑽井的經濟合理性。

原油價格波動正在抑制上游產業的資本投資。

儘管服務成本有所下降,但美國獨立石油公司已將2024年的資本支出計畫縮減至617億美元至654億美元,凸顯了油價波動可能導致非必要干預措施推遲的風險。大型石油公司繼續將支出控制在230億美元至250億美元的狹窄範圍內,進一步強化了其謹慎的資本配置策略。由於滑線作業通常具有選擇性,當西德州中質原油(WTI)價格跌至損益平衡點以下時,業者會延後優先順序較低的作業。工程和安裝服務的通膨進一步加劇了干涉預算的壓力。服務提供者正透過基於績效的定價和多井套餐來應對這項挑戰,這些方案將付款與新增採油量掛鉤,而不是與現場作業時間掛鉤。

細分市場分析

2025年,井下套管作業佔滑線測井服務市場佔有率的59.12%,預計2026年至2031年將以6.88%的複合年成長率快速成長。這表明營運商優先考慮從現有油井中獲取價值,而非鑽探新井。這種主導地位的促進因素是老井數量的不斷增加。到2030年,超過三分之二的油井井齡將超過10運作,這將持續推動對機械維修、產量剖面分析和水泥黏結評估的需求,而這些服務無需出井即可完成。數位化滑線平台可將壓力、溫度和流量資料即時傳輸到地面,將測井和機械作業整合到一次作業中,從而實現即時診斷並減少非生產時間。因此,與井下套管作業相關的滑線測井服務市場規模受益於作業頻率和工具複雜性的雙重成長。人工智慧可即時提案最佳工具串配置,以最大限度地提高增量採收率。

裸井作業雖然規模較小,但在初始井筒建造階段以及需要精確評估儲存接觸面時,對於地層評估至關重要。這些作業需要直接接觸岩體,但由於鑽井預算限制和套管後返工頻率降低,盈利有限。自主式滑線牽引機的進步使作業者能夠執行多管完井作業,並透過狹窄井眼部署橋塞和跨接封隔器,從而擴大了套管後服務的範圍。頁岩氣藏的再壓裂計畫進一步推動了需求,因為滑線牽引的隔離工具能夠對成熟井進行目標增產,預計將最終採收率提高50%以上。這些因素共同作用,使套管作業成為收入成長的關鍵驅動力,而裸井服務則繼續提供高價值的細分應用,與更廣泛的滑線作業產品組合形成互補。

區域分析

北美地區在2025年之前將保持38.55%的收入佔有率,這得益於其龐大的老井存量和積極的壓裂再作業項目。在鷹灘頁岩油氣區和巴肯頁岩油氣區,採用滑線壓裂技術使最終可採儲量(EUR)提高了50%以上,證實了該技術的經濟可行性。在二疊紀盆地,人工智慧增強型數位化滑線裝置正被擴大部署,以減少停機時間和甲烷排放。預計加拿大近海大西洋油田和墨西哥的Trion深水計劃將拓展該地區頁岩油氣以外的收入來源。

預計到2031年,中東和非洲地區的複合年成長率將達到7.05%,這主要得益於上游7300億美元的投資以及旨在以天然氣替代發電領域液態燃料的「天然氣優先」策略。阿布達比國家石油公司(ADNOC)和沙烏地阿美公司正在競標一份綜合性的多年期契約,該契約將涵蓋滑線服務、鑽井、完井和碳捕獲監測等環節。奈及利亞超深水區和奈米比亞邊遠地區的油氣發現需要高壓高溫的滑線設備,這為專業服務船隊創造了機會。

亞太和歐洲正經歷均衡成長。中國和印度正在南海和孟加拉灣進行更深的鑽探,這些地區的高壓高溫儲存需要使用光纖滑線進行即時遙測。歐洲北海的作業量持續穩定,營運商的目標是利用無鑽機滑線作業系統將營運成本降低50%。南美洲受益於巴西的鹽鹽層下開發和阿根廷的瓦卡穆爾塔頁岩油田開發,這兩個項目均採用綜合服務模式,確保在三到五年內提供多次服務。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 即將進行的主要上游計劃

- 市場促進因素

- 深海和超深海鑽探的持續繁榮週期

- 老舊油井的井下作業成本不斷增加

- 快速採用數位化滑線平台

- 頁岩/緻密油壓裂計畫增加了干涉頻率

- 國家石油公司(NOC)將滑線納入綜合服務競標

- CCS試點井需要微創測井解決方案

- 市場限制

- 原油價格波動抑制了上游產業的資本投資。

- 加強對中間流體的健康、安全、環境和排放法規

- 全球合格的滑線人員短缺

- 2030年起,自主地下機器人將出現

- 供應鏈分析

- 監管環境

- 科技展望(數位滑線、生活數據、人工智慧)

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按孔類型

- 裸井

- 下套管井

- 按位置

- 陸上

- 離岸

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 挪威

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 韓國

- 東南亞國協

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- SLB

- Halliburton

- Baker Hughes

- Weatherford

- Expro Group

- Vallourec

- National Oilwell Varco

- Scientific Drilling

- Archer Ltd

- Superior Energy Services

- Nine Energy Service

- Altus Intervention

- TETRA Technologies

- Welltec

- TechnipFMC

- Nabors Industries

- NESR

- Axis Energy Services

- Patterson-UTI

第7章 市場機會與未來展望

The Slickline Logging Services Market was valued at USD 1.61 billion in 2025 and estimated to grow from USD 1.72 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031).

Demand is being propelled by operators' preference for production optimisation on existing wells, the steady rise in deep- and ultra-deepwater projects, and the rapid deployment of digital slickline platforms that enable real-time downhole diagnostics without halting production. Other supportive factors include the growing backlog of ageing wells, national oil companies' integrated service tenders, and emerging carbon-capture pilot programmes that require low-invasion logging. Continued advancements in artificial intelligence and autonomous operations are transforming conventional mechanical workovers into data-rich interventions that extend asset life and reduce lifting costs.

Global Slickline Logging Services Market Trends and Insights

Sustained Offshore Deep- & Ultra-Deepwater Drilling Upcycle

Deepwater rig utilisation stood at 82% in 2025, keeping day-rates firm and sustaining demand for robust slickline intervention under extreme pressure and temperature conditions. Projects such as Woodside's Trion development-18 wells in 2,500 m water-illustrate the complexity that fuels a continual need for formation evaluation and well-integrity surveillance. National oil companies are locking slickline services into multi-year integrated drilling contracts to capture operational synergies and reduce rig moves. Real-time slickline diagnostics now integrate with AI-enabled drilling platforms to maintain well control and optimize reservoir contact. Longer campaign durations in remote waters heighten the value of multi-function slickline strings that complete mechanical, logging, and clean-out tasks without additional mobilisation.

Rising Well-Intervention Spend on Ageing Wells

Roughly two-thirds of the world's 260,000 active wells will be more than 10 years old by 2030, pushing global intervention spend toward USD 58 billion as operators chase a 10% average output uplift per well. Slickline has evolved from simple mechanical retrieval into a platform for high-definition cameras and electronic gauges, offering a low-cost alternative to rig-based workovers. North Sea operators are piloting slickline-mediated straddle gas-lift activation that cuts deepwater workover costs by half. Additional applications include robotic screen retrieval and chemical deployment, all of which strengthen the economic case for targeted intervention over fresh drilling.

Crude-Price Volatility Curbing Upstream CAPEX

US independents trimmed their 2024 capital plans to USD 61.7-65.4 billion, despite lower service costs, highlighting how price swings can postpone discretionary interventions. Major companies continue to spend within a tight USD 23-25 billion band, reinforcing cautious cash allocation. Because slickline work is often elective, operators defer lower-priority jobs when WTI falls below breakeven thresholds. Inflation in engineering and installation services adds further pressure to intervention budgets. Providers respond with outcome-based pricing and multi-well packages that tie payment to incremental barrels recovered rather than time on-site.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Digital Slickline Platforms

- Shale/Tight-Oil Re-Frac Programmes Driving Frequent Interventions

- Tightening HSE & Emissions Regulations on Intervention Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cased hole interventions commanded 59.12% of slickline logging services market share in 2025 and are forecast to register the fastest 6.88% CAGR from 2026-2031, underscoring operators' preference to extract additional value from existing wellbores rather than drill new ones. This dominance is rooted in the growing inventory of ageing wells-more than two-thirds will surpass 10 years of service by 2030-which keeps demand high for mechanical repairs, production profiling, and cement-bond evaluation that can be executed without pulling tubing. Digital slickline platforms stream live pressure, temperature, and flow data to the surface, enabling real-time diagnostics and reducing non-productive time by combining logging and mechanical tasks in a single run. The slickline logging services market size associated with these cased operations, therefore, benefits from both higher job frequency and expanding tool complexity, as artificial intelligence recommends optimal tool-string configurations on the fly to maximize incremental barrels recovered.

Open hole work represents the smaller share of activity, yet remains essential for formation evaluation during initial well construction or when precise reservoir contact is critical. While these jobs require direct rock exposure, their revenue potential is limited by drilling budgets and fewer repeat visits once a well is cased. Advancements in autonomous slickline tractors now enable operators to navigate multi-string completions and deploy bridge plugs or straddle packers through restrictive profiles, thereby widening the scope of cased services. Re-fracturing programs in shale plays further amplify demand, as slickline-conveyed isolation tools enable targeted stimulation that can increase estimated ultimate recovery by 50% or more in a mature well. Together, these factors position cased hole operations as the primary engine of revenue expansion, while open hole services continue to deliver high-value niche applications that complement the broader slickline portfolio.

The Slickline Logging Services Market Report is Segmented by Hole Type (Open Hole and Cased Hole), Location of Deployment (Onshore and Offshore), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 38.55% revenue share in 2025, driven by a vast ageing well stock and prolific re-fracturing programs. The Eagle Ford and Bakken plays recorded EUR gains exceeding 50% when slickline-enabled re-fracs were executed, confirming the technique's economic relevance. AI-augmented digital slickline units are increasingly deployed in the Permian Basin to cut downtime and lower methane intensity. Canada's Atlantic offshore and Mexico's Trion deepwater project are set to widen regional revenue streams beyond shale.

The Middle East & Africa is forecast to grow at a 7.05% CAGR to 2031, supported by USD 730 billion of upstream spending and gas-directed strategies aimed at substituting liquid fuels in power generation. ADNOC and Saudi Aramco are issuing multi-year, integrated tenders that bundle slickline services with drilling, completion, and carbon capture monitoring. Nigeria's ultra-deepwater discoveries and Namibia's frontier finds require high-pressure, high-temperature slickline tool strings, creating opportunities for specialized service fleets.

Asia-Pacific and Europe provide balanced growth. China and India are drilling deeper in the South China Sea and Bay of Bengal, where HPHT reservoirs need fibre-optic slickline for live telemetry. Europe's North Sea continues to generate steady intervention volumes as operators target 50% work-over cost cuts through rigless slickline packages. South America remains buoyed by Brazil's pre-salt developments and Argentina's Vaca Muerta shale, both adopting integrated service models that secure multi-service lineups for three-to-five-year windows.

- SLB

- Halliburton

- Baker Hughes

- Weatherford

- Expro Group

- Vallourec

- National Oilwell Varco

- Scientific Drilling

- Archer Ltd

- Superior Energy Services

- Nine Energy Service

- Altus Intervention

- TETRA Technologies

- Welltec

- TechnipFMC

- Nabors Industries

- NESR

- Axis Energy Services

- Patterson-UTI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Major Upcoming Upstream Projects

- 4.3 Market Drivers

- 4.3.1 Sustained offshore deep- & ultra-deepwater drilling upcycle

- 4.3.2 Rising well-intervention spend on aging wells

- 4.3.3 Rapid adoption of digital slickline platforms

- 4.3.4 Shale/tight-oil re-frac programs driving frequent interventions

- 4.3.5 NOCs bundling slickline into integrated service tenders

- 4.3.6 CCS pilot wells needing low-invasion logging solutions

- 4.4 Market Restraints

- 4.4.1 Crude-price volatility curbing upstream CAPEX

- 4.4.2 Tightening HSE & emissions regulations on intervention fluids

- 4.4.3 Global shortage of certified slickline crews

- 4.4.4 Emergence of autonomous down-hole robots post-2030

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook (Digital Slickline, Live-well data, AI)

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Hole Type

- 5.1.1 Open Hole

- 5.1.2 Cased Hole

- 5.2 By Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Norway

- 5.3.2.4 NORDIC Countries

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 South Korea

- 5.3.3.4 ASEAN Countries

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SLB

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 Weatherford

- 6.4.5 Expro Group

- 6.4.6 Vallourec

- 6.4.7 National Oilwell Varco

- 6.4.8 Scientific Drilling

- 6.4.9 Archer Ltd

- 6.4.10 Superior Energy Services

- 6.4.11 Nine Energy Service

- 6.4.12 Altus Intervention

- 6.4.13 TETRA Technologies

- 6.4.14 Welltec

- 6.4.15 TechnipFMC

- 6.4.16 Nabors Industries

- 6.4.17 NESR

- 6.4.18 Axis Energy Services

- 6.4.19 Patterson-UTI

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球有線服務市場報告

2026年全球有線服務市場報告 全球電纜測井服務市場:市場規模、佔有率、成長率、產業分析、類型、應用和區域分析,未來預測(2026-2034)

全球電纜測井服務市場:市場規模、佔有率、成長率、產業分析、類型、應用和區域分析,未來預測(2026-2034) 電纜作業服務市場規模、佔有率和成長分析(按電纜類型、服務、井類型和地區分類)-2026-2033年產業預測

電纜作業服務市場規模、佔有率和成長分析(按電纜類型、服務、井類型和地區分類)-2026-2033年產業預測 滑線服務市場規模、佔有率和成長分析(按滑線工具、部署方法、作業方式和地區分類)-2026-2033年產業預測

滑線服務市場規模、佔有率和成長分析(按滑線工具、部署方法、作業方式和地區分類)-2026-2033年產業預測 按技術、服務類型、最終用戶、速度、應用和分銷管道分類的纜線服務市場 - 全球預測 2025-2032

按技術、服務類型、最終用戶、速度、應用和分銷管道分類的纜線服務市場 - 全球預測 2025-2032 有線服務市場規模及預測 2025-2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、孔類型、服務類型、應用和地理

有線服務市場規模及預測 2025-2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、孔類型、服務類型、應用和地理 有線服務市場-全球產業規模、佔有率、趨勢、機會和預測,按服務類型、應用、技術、地區和競爭細分,2020-2030 年預測鋼絲繩服務市場-全球產業規模、佔有率、趨勢、機會及預測(按鋼絲繩工具、應用、地區及競爭細分,2020-2030 年預測)

有線服務市場-全球產業規模、佔有率、趨勢、機會和預測,按服務類型、應用、技術、地區和競爭細分,2020-2030 年預測鋼絲繩服務市場-全球產業規模、佔有率、趨勢、機會及預測(按鋼絲繩工具、應用、地區及競爭細分,2020-2030 年預測) 2032 年有線服務市場預測:按有線類型、井類型、服務、位置、技術、應用、最終用戶和地區進行的全球分析

2032 年有線服務市場預測:按有線類型、井類型、服務、位置、技術、應用、最終用戶和地區進行的全球分析 2025 年至 2033 年有線服務市場報告,按有線類型(電力線、鋼絲)、服務類型(完井、干預、測井)、孔類型(裸眼、套管井)、應用(陸上、海上)和地區分類

2025 年至 2033 年有線服務市場報告,按有線類型(電力線、鋼絲)、服務類型(完井、干預、測井)、孔類型(裸眼、套管井)、應用(陸上、海上)和地區分類