|

市場調查報告書

商品編碼

1852158

奈米纖維:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Nanofiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

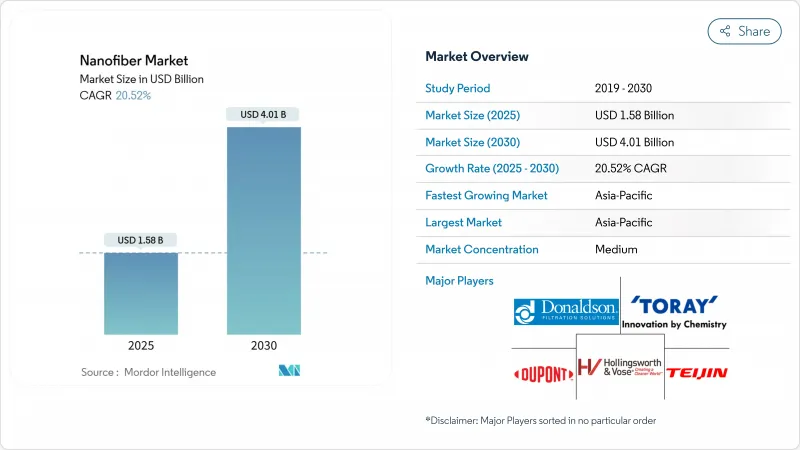

預計到 2025 年,奈米纖維市場規模將達到 15.8 億美元,到 2030 年將達到 40.1 億美元,預測期(2025-2030 年)的複合年成長率為 20.52%。

醫療、過濾、儲能和先進纖維應用領域對高比表面積材料的需求不斷成長,支撐了這一前景。亞太地區以38%的收入佔比領先,並受益於強大的製造業生態系統,預計到2030年將以22%的複合年成長率成長,鞏固其作為規模最大且成長最快的區域市場的雙重地位。在成熟的靜電紡絲生產能力的支持下,聚合物產品類型將佔2024年收入的42%,而碳水化合物基產品將以27%的複合年成長率引領成長,反映了更廣泛的永續性轉型。東麗和杜邦等全球領導者保持其銷售量領先地位,而奈米層等創新企業則利用其專有的製造技術,搶佔高利潤的醫療和能源細分市場。碳奈米纖維規模化生產面臨的挑戰依然嚴峻,加上聚丙烯腈(PAN)原料價格波動,削弱了近期的供應前景。

全球奈米纖維市場趨勢與洞察

來自醫療和製藥行業的需求不斷成長

以奈米纖維為基礎的藥物傳遞平台目前可實現超過85%的載藥量,並持續釋放長達96小時,顯著增強治療藥物的黏附性並降低全身毒性。其類似細胞外基質的結構支持卓越的細胞黏附,從而建構新一代組織支架,加速傷口癒合並最大限度地減少疤痕形成。採用先進傷口敷料的醫院患者周轉率不斷提高,從而降低醫療成本並增加採購誘因。奈米纖維支架在整形外科的監管路徑也日益清晰,降低了開發商的上市時間風險。總而言之,這些醫學突破提升了報銷前景,並增強了高價值醫療保健管道的持續需求。

電動車超級工廠對高表面積電池隔膜的需求

靜電紡絲奈米纖維隔膜如今可在150°C高溫下保持尺寸不變,從而滿足電動車的關鍵安全標準。其離子電導率的提升可使快充性能提高高達40%,同時保持循環壽命,吸引了亞洲和美國超級工廠的採購。自動化卷對卷生產線的年產量超過300萬平方米,縮小了與傳統聚烯薄膜的成本差距。主要電池製造商的安裝正在鎖定多年供應契約,並為奈米纖維供應商提供可預測的產量資訊。中國和美國的國家清潔旅遊激勵政策進一步推動了新型電池化學體系中隔膜的應用。

PAN原料價格不穩定

聚丙烯腈(PAN)約佔碳奈米纖維前驅物的90%,其現貨價格每年波動高達20%,侵蝕了下游供應商的利潤穩定性。丙烯腈原料短缺導致的供應中斷加劇了庫存風險,促使生產商尋求石油瀝青質或木質素的替代品,這些替代品可以將原料成本降低至每公斤9美元以下,同時提升永續性。雜質控制和機械性能方面的差異延長了過渡期,也延長了PAN價格波動帶來的風險。買家正透過指數掛鉤合約進行避險,但由於長期價格前景依然有限,積極的產能擴張受到限制。

細分市場分析

2024年,聚合物基纖維將佔總銷售額的42%,這主要得益於成熟的靜電紡絲生產線以及其在包裝、過濾和生物醫學設備等應用領域廣泛的化學多功能性。碳水化合物基纖維雖然目前銷量仍然較低,但正以27%的複合年成長率快速成長,因為終端用戶正在尋求符合全球循環經濟指令的可生物分解的生物來源替代品。纖維素奈米纖維的拉伸強度可與芳香聚醯胺媲美,在常溫常壓下即可生物分解,這促使包裝供應商將其應用於一次性包裝產品中。幾丁質奈米纖維因其固有的抗菌性能而備受創傷護理產品製造商的青睞,並推動了貝殼廢棄物回收利用方面的投資。碳奈米纖維在特種能源和電子領域正發揮著重要作用,但生產規模和成本的挑戰限制了其近期成長。

碳水化合物基產品的發展勢頭得益於品牌所有者減少化石塑膠使用的承諾。歐盟多個成員國已立法禁止使用一次性合成纖維,進一步推動了這一趨勢。複合奈米纖維(聚合物和陶瓷相的混合物)在高溫過濾領域發揮關鍵作用。金屬和金屬氧化物級奈米纖維可用於催化和感測應用,這些應用對高導電性和光催化活性要求較高。陶瓷奈米纖維作為航太隔熱材料和爐襯材料的需求仍然強勁。隨著原料研發轉向林業和農業廢棄物,成本曲線預計將趨於一致,從而促進整個奈米纖維市場的發展。

區域分析

到2024年,亞太地區將佔全球銷售額的38%,其中中國、日本和韓國受益於發達的電子產品供應鏈和政府支持的奈米技術計畫。中國蓬勃發展的電動車生產基地正在推動對奈米纖維舉措的需求。針對永續材料的區域振興基金進一步降低了對木質素衍生奈米纖維工廠的投資風險。這項生態系統將推動亞太地區的複合年成長率達到22%,亞太地區將持續引領全球銷售成長。

北美在全球產生收入中扮演關鍵角色,其中美國佔據主導地位,其2025會計年度國家奈米技術計畫預算高達22億美元,用於津貼醫療保健、國防和能源領域。基於奈米纖維的再生植入的臨床試驗已獲得美國食品藥物管理局(FDA)的快速通道資格,加速了其商業化進程。國防機構正在資助過濾裝置和防護衣的研發,從而加強國內供應鏈。加拿大的乾淨科技激勵政策以及其接近性汽車產業中心的地理優勢,正在推動電池材料領域的跨境合作。

在德國和法國嚴格的永續性框架的推動下,歐洲在可生物分解奈米纖維包裝和暖通空調解決方案領域處於市場領先地位。 「地平線歐洲」津貼促進了產學研合作叢集的形成,從而加速規模化生產和標準化,而REACH法規則提供了監管確定性。儘管成長率落後於亞太地區,但歐盟禁止使用某些一次性塑膠的政策正在為餐飲服務和個人保健產品創造替代機會。在南美洲以及中東和非洲,為解決飲用水短缺和提高農業效率而採取的舉措正在推動收入成長,其中奈米纖維膜在海水淡化和控制釋放肥料領域的應用尤為突出。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 來自醫療和製藥行業的需求不斷成長

- 電動車超級工廠對高表面積電池隔膜的需求

- 高效率過濾介質的需求

- 汽車產業的成長

- 紡織業的擴張

- 市場限制

- PAN原料價格不穩定

- 向碳奈米纖維過渡的困難

- 健康與安全問題

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 技術概覽

- 專利分析

第5章 市場規模與成長預測

- 依產品類型

- 聚合物奈米纖維

- 碳奈米纖維

- 複合奈米纖維

- 金屬和金屬氧化物奈米纖維

- 陶瓷奈米纖維

- 碳水化合物基奈米纖維

- 透過使用

- 水和空氣過濾

- 醫療保健

- 儲能

- 汽車與運輸

- 電子學

- 紡織品

- 其他用途

- 透過製造技術

- 靜電紡絲(針式)

- 無針靜電紡絲

- 解決方案

- 強制紡絲/旋轉噴射紡絲

- 熔噴

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Applied Sciences Inc.

- Argonide Corporation

- Asahi Kasei Corporation

- Chuetsu Pulp & Paper Co. Ltd.

- Donaldson Company Inc.

- DuPont

- Esfil Tehno AS

- eSpin Technologies Inc.

- FibeRio Technology Corp.

- Hollingsworth & Vose

- IREMA-Filter GmbH

- Japan Vilene Company Ltd.

- NanoLayr Ltd

- Nanoval GmbH & Co. KG

- NIPPON PAPER INDUSTRIES CO., LTD.

- Pardam SRO

- Rengo Co., Ltd.

- Sappi Ltd.

- SNC Fiber

- Spur AS

- Teijin Limited

- Toray Industries Inc.

- US Global Nanospace Inc.

第7章 市場機會與未來展望

The Nanofiber Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 4.01 billion by 2030, at a CAGR of 20.52% during the forecast period (2025-2030).

Heightened demand for high-surface-area materials in medical, filtration, energy storage, and advanced textile applications anchors this outlook. Asia-Pacific, with an existing 38% revenue lead, benefits from strong manufacturing ecosystems and is expected to expand at 22% CAGR through 2030, reinforcing its dual role as both the largest and fastest-growing regional base. The polymeric product category holds 42% of 2024 revenue, supported by mature electrospinning capacity, while carbohydrate-based grades set the growth tempo at 27% CAGR, reflecting a wider sustainability shift. Global incumbents such as Toray Industries and DuPont maintain volume leadership while innovators like NanoLayr deploy proprietary manufacturing to capture high-margin medical and energy niches. Persistent scale-up hurdles for carbon nanofibers, coupled with price volatility in polyacrylonitrile (PAN) feedstock, temper the near-term supply outlook.

Global Nanofiber Market Trends and Insights

Increasing Demand from Medical and Pharmaceutical Industries

Nanofiber-based drug delivery platforms now achieve 85%-plus drug loading and sustained release for up to 96 hours, sharply improving therapeutic adherence and lowering systemic toxicity. Their extracellular-matrix-like architecture supports superior cell attachment, enabling next-generation tissue scaffolds that cut healing time and minimize scarring. Hospitals adopting advanced wound dressings cite patient-turnover gains that translate to reduced care costs, strengthening procurement appetite. Regulatory pathways for nanofiber scaffolds in orthopedics continue to clarify, lowering time-to-market risk for developers. Collectively, these medical breakthroughs elevate reimbursement prospects and reinforce recurring demand across high-value healthcare channels.

Demand for High-Surface-Area Battery Separators in EV Gigafactories

Electrospun nanofiber separators now withstand 150 °C thermal excursions without dimensional loss, addressing critical EV safety standards. Enhancements in ion conductivity are extending fast-charge capability by up to 40% while preserving cycle life, a gain attracting procurement from Asian and US gigafactories. Automated roll-to-roll lines scale output beyond 3 million m2 annually, narrowing cost gaps with conventional polyolefin films. Capital deployment by major cell producers is locking in multiyear supply contracts, providing predictable volume visibility for nanofiber vendors. National clean-mobility incentives in China and the United States further amplify separator adoption in new cell chemistries.

Volatile PAN Feedstock Prices

PAN constitutes about 90% of carbon nanofiber precursors, and its spot price fluctuates by up to 20% annually, eroding margin stability for downstream suppliers. Supply disruptions linked to acrylonitrile feed shortages intensify inventory risk, prompting producers to pursue petroleum-asphaltene or lignin alternatives that can cut raw-material cost below USD 9 per kg while raising sustainability credentials. Transition timeframes remain lengthy due to impurity management and variable mechanical performance, prolonging exposure to PAN volatility. Buyers hedge through index-linked contracts, but long-term pricing visibility is still limited, dampening aggressive capacity expansion.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Efficiency Filtration Materials

- Growth in the Automotive Industry

- Difficulty in Shifting Carbon Nanofibers from Lab to Plant Scale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polymeric category anchors 42% of 2024 revenue, driven by well-established electrospinning lines and broad chemical versatility across packaging, filtration and biomedical devices. Carbohydrate-based grades, while smaller in volume, accelerate at a 27% CAGR as end-users pursue biodegradable, bio-sourced alternatives aligned with global circular-economy mandates. Cellulose nanofibers rival aramid tensile strength yet biodegrade under ambient conditions, compelling packaging suppliers to adopt them in single-use applications. Chitin nanofibers attract wound-care producers due to inherent antimicrobial traits, spurring investment in shellfish-waste valorization. Carbon nanofibers find significant use in specialty energy and electronics applications; however, production scale and cost challenges are restraining immediate growth.

Momentum for carbohydrate-based products is amplified by brand-owner commitments to cut fossil plastic use. Legislative bans on single-use synthetic fibers in several EU states compound this pull. Composite nanofibers, which blend polymer and ceramic phases, play a significant role in high-temperature filtration niches. Metal and metal-oxide grades serve catalytic and sensing applications where elevated conductivity or photocatalytic activity is critical. Ceramic nanofibers retain demand for thermal insulation in aerospace and furnace linings. As raw-material R&D migrates toward forestry and agricultural waste streams, cost curves are expected to converge, bolstering the broader nanofiber market.

The Nanofiber Market Report is Segmented by Product Type (Polymeric Nanofiber, Carbon Nanofiber, and More), Application (Water and Air Filtration, Medical, and More), Manufacturing Technology (Electrospinning (Needle-Based), Needle-Less Electrospinning, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 38% of 2024 revenue, with China, Japan and South Korea benefitting from deep electronic supply chains and government-backed nanotech initiatives. Robust EV production bases in China elevate local demand for nanofiber separators, while strict environmental guidelines accelerate uptake in air-filtration retrofits. Regional stimulus funds earmarked for sustainable materials further de-risk investment in lignin-derived nanofiber plants. This ecosystem underpins a 22% regional CAGR, ensuring Asia-Pacific continues to anchor global volume growth.

North America, driven by the U.S. with its USD 2.2 billion FY-25 National Nanotechnology Initiative budget, which allocates grants to medical, defense, and energy sectors, plays a significant role in global revenue generation. High-value healthcare projects dominate demand; clinical trials for nanofiber-based regenerative implants secure FDA fast-track status, accelerating commercialization. Defense agencies sponsor filtration and protective-wear R&D, fortifying domestic supply chains. Canada's clean-technology incentives and proximity to automotive hubs kindle cross-border collaboration in battery materials.

Europe, driven by Germany and France's stringent sustainability frameworks, leads in the market for biodegradable nanofiber packaging and HVAC solutions. Horizon Europe grants foster university-industry clusters that fast-track scale-up and standardization, while REACH compliance guidelines supply regulatory certainty. Although growth rates trail Asia-Pacific, EU directives banning select single-use plastics are opening replacement opportunities in food-service and personal-care products. In South America, the Middle East, and Africa, where programs addressing potable-water scarcity and enhancing agricultural efficiency are gaining traction, revenue is driven by the early adoption of nanofiber membranes in desalination and controlled-release fertilizers.

- Applied Sciences Inc.

- Argonide Corporation

- Asahi Kasei Corporation

- Chuetsu Pulp & Paper Co. Ltd.

- Donaldson Company Inc.

- DuPont

- Esfil Tehno AS

- eSpin Technologies Inc.

- FibeRio Technology Corp.

- Hollingsworth & Vose

- IREMA-Filter GmbH

- Japan Vilene Company Ltd.

- NanoLayr Ltd

- Nanoval GmbH & Co. KG

- NIPPON PAPER INDUSTRIES CO., LTD.

- Pardam SRO

- Rengo Co., Ltd.

- Sappi Ltd.

- SNC Fiber

- Spur AS

- Teijin Limited

- Toray Industries Inc.

- US Global Nanospace Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from the Medical and Pharmaceutical Industries

- 4.2.2 Demand for High-Surface-Area Battery Separators in EV Gigafactories

- 4.2.3 Demand for High-Efficiency Filtration Materials

- 4.2.4 Growth in the Automotive Industry

- 4.2.5 Expansion in the Textile Industry

- 4.3 Market Restraints

- 4.3.1 Volatile PAN Feedstock Prices

- 4.3.2 Difficulty in Shift of Carbon Nanofibers from Lab Scale to Plant Scale due to Small Size and Complexity

- 4.3.3 Health and Safety Concerns

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Technology Snapshot

- 4.7 Patent Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polymeric Nanofiber

- 5.1.2 Carbon Nanofiber

- 5.1.3 Composite Nanofiber

- 5.1.4 Metal and Metal Oxide Nanofiber

- 5.1.5 Ceramic Nanofiber

- 5.1.6 Carbohydrate-based Nanofiber

- 5.2 By Application

- 5.2.1 Water and Air Filtration

- 5.2.2 Medical

- 5.2.3 Energy Storage

- 5.2.4 Automotive and Transportation

- 5.2.5 Electronics

- 5.2.6 Textiles

- 5.2.7 Other Applications

- 5.3 By Manufacturing Technology

- 5.3.1 Electrospinning (Needle-Based)

- 5.3.2 Needle-less Electrospinning

- 5.3.3 Solution Blow Spinning

- 5.3.4 ForceSpinning/Rotary Jet Spinning

- 5.3.5 Melt Blowing

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Applied Sciences Inc.

- 6.4.2 Argonide Corporation

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Chuetsu Pulp & Paper Co. Ltd.

- 6.4.5 Donaldson Company Inc.

- 6.4.6 DuPont

- 6.4.7 Esfil Tehno AS

- 6.4.8 eSpin Technologies Inc.

- 6.4.9 FibeRio Technology Corp.

- 6.4.10 Hollingsworth & Vose

- 6.4.11 IREMA-Filter GmbH

- 6.4.12 Japan Vilene Company Ltd.

- 6.4.13 NanoLayr Ltd

- 6.4.14 Nanoval GmbH & Co. KG

- 6.4.15 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.16 Pardam SRO

- 6.4.17 Rengo Co., Ltd.

- 6.4.18 Sappi Ltd.

- 6.4.19 SNC Fiber

- 6.4.20 Spur AS

- 6.4.21 Teijin Limited

- 6.4.22 Toray Industries Inc.

- 6.4.23 US Global Nanospace Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing R&D and High-potential Market for Cellulosic Nanofibers

奈米纖維市場:按產品類型、技術和終端應用產業分類-2026-2032年全球市場預測

奈米纖維市場:按產品類型、技術和終端應用產業分類-2026-2032年全球市場預測 2026年全球奈米纖維市場報告

2026年全球奈米纖維市場報告 奈米纖維市場規模、佔有率、趨勢和預測:按產品、技術、應用和地區分類,2026-2034年2026年全球醫用奈米纖維材料市場報告2026年全球奈米科技服飾市場報告

奈米纖維市場規模、佔有率、趨勢和預測:按產品、技術、應用和地區分類,2026-2034年2026年全球醫用奈米纖維材料市場報告2026年全球奈米科技服飾市場報告 奈米纖維傷口敷料市場預測至2032年:按材料類型、傷口類型、功能特性、最終用戶和地區分類的全球分析

奈米纖維傷口敷料市場預測至2032年:按材料類型、傷口類型、功能特性、最終用戶和地區分類的全球分析 聚合物奈米纖維:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

聚合物奈米纖維:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 奈米纖維市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、技術、應用、地區和競爭細分,2020-2030 年)纖維素奈米纖維標籤市場預測(至 2032 年):按產品類型、來源、應用、最終用戶和地區進行的全球分析自清潔奈米纖維市場預測(至2032年):按材料類型、塗層、製造技術、最終用戶和地區進行的全球分析

奈米纖維市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、技術、應用、地區和競爭細分,2020-2030 年)纖維素奈米纖維標籤市場預測(至 2032 年):按產品類型、來源、應用、最終用戶和地區進行的全球分析自清潔奈米纖維市場預測(至2032年):按材料類型、塗層、製造技術、最終用戶和地區進行的全球分析