|

市場調查報告書

商品編碼

1852150

1,4-丁二醇:市佔率分析、產業趨勢、統計、成長預測(2025-2030)1,4 Butanediol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

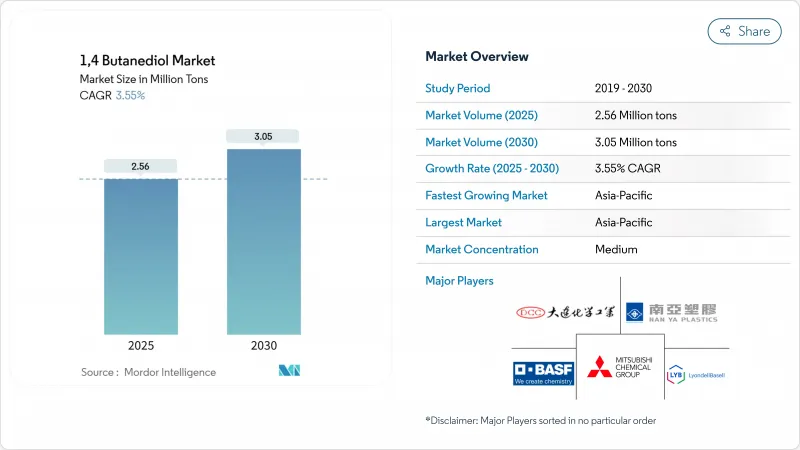

預計 1,4-丁二醇市場規模在 2025 年將達到 256 萬噸,到 2030 年將達到 305 萬噸,預測期(2025-2030 年)複合年成長率為 3.55%。

推動生產擴張的因素包括:氨綸紗線對四氫呋喃 (THF) 的需求不斷成長、電動車 (EV) 連接器對聚對聚丁烯對苯二甲酸酯(PBT) 的需求日益成長,以及生物發酵製程的興起,這些都有助於降低碳排放強度。隨著生物技術授權者與尋求更環保生產能力的製造商合作,競爭日益激烈;同時,老牌石化製造商則透過最佳化其再生製程設備來應對這項挑戰。在北美和歐洲,政府獎勵以及汽車、電子和服裝品牌日益增強的永續性目標,正在刺激對生物基產能的投資。同時,碳化鈣衍生的乙炔價格波動以及日益嚴格的健康和安全法規,也促使生產商實現原料多元化。

全球1,4-丁二醇市場趨勢及洞察

對四氫呋喃(THF)和氨綸纖維的需求不斷成長

四氫呋喃 (THF) 仍然是一種重要的衍生物,為氨綸紗線提供聚對甲氧基乙二醇 (PTMEG),而氨綸紗線是高性能服裝、醫用紡織品和汽車內飾的基礎材料。氨綸的消費正從基礎運動休閒服轉向對彈性和回彈性能要求更高的高性能服飾。因此,生產商正在擴大催化劑升級,例如生物炭負載的釕-錸休閒,這些體係可以減少氫氣的使用並提高選擇性,從而有助於在近期亞洲價格波動的情況下穩定利潤率。服裝品牌對回收的推動促使 THF 供應商與下游工廠合作,致力於減少範圍 3排放並探索循環原料。這種動態的融合使得 1,4-丁二醇市場與合成纖維產業鏈的健康息息相關。

更輕的電動車正在推動PBT在汽車連接器中的應用。

為了提高能量密度,汽車製造商正在重新設計其高壓架構,採用PBT外殼,在保持介電強度的同時,將系統重量減輕15-30%。零件製造商表示,與傳統材料相比,射出成型成型製程的週期時間更短,從而能夠提高生產線速度,以應對電動車需求的加速成長。北美供應鏈正在透過新的混煉生產線得到服務,這些生產線將生物回收的1,4-丁二醇與回收聚酯相結合,從而將產品碳足跡減少30%以上,並滿足國內含量獎勵。這種向工程熱塑性塑膠的結構性轉變將在未來十年內鞏固1,4-丁二醇市場的持續成長動能。

健康與安全問題

由於1,4-丁二醇具有影響中樞神經系統的急性毒性,全球監管機構正在收緊其暴露限值。歐洲的REACH和CLP框架要求提供大量文件,這增加了合規成本,並可能導致缺乏先進EHS(環境、健康與安全)基礎設施的小型配方商被市場淘汰。雖然大型製造商可以透過閉合迴路處理和操作人員培訓計劃來緩解這些限制,但下游的個人護理和消費品行業面臨更大的挑戰。這些動態限制了某些高價值應用領域的成長,並需要在整個市場持續投資於安全管理系統。

細分市場分析

預計到2024年,採用Reppe製程生產的1,4-丁二醇市場規模將佔據70%的主導地位,這主要得益於成熟的乙炔基資產以及中國有利的煤炭經濟效益。然而,生物發酵製程的產量正以7.40%的複合年成長率快速成長,這主要得益於代謝工程技術的突破,該技術能夠將PET廢棄物衍生的乙二醇轉化為高純度的1,4-丁二醇。例如,越南即將投產的年產5萬噸的裝置等商業性應用案例,凸顯了技術許可方如何將實驗室滴度轉化為工業提純技術,目前已實現超過99%的回收率,且單價具有競爭力。

對煤基乙炔的持續環境限制以及主要出口市場可能實施的碳排放邊境調整,提高了雷佩法合成1,4-丁二醇的成本門檻。在丙烯氧化物經濟效益較高或丁二烯區域供應過剩的情況下,戴維法和丁二烯法合成1,4-丁二醇則提供了製程上的彈性。因此,1,4-丁二醇市場體現了一種投資組合策略,生產商透過在多種合成路線上配置資金來對沖監管和原料風險,同時最佳化生命週期排放。

區域分析

亞太地區在1,4-丁二醇市場佔據主導地位,2024年市佔率高達76%,預計到2030年將以3.87%的複合年成長率成長。中國憑藉其龐大的再生能源產能(主要由煤製乙炔驅動)引領這一主導,而BASF湛江一體化工廠等新計劃正在擴大區域工程塑膠的生產。印度和韓國正在擴建下游彈性體、紡織品和電子產品工廠,深化區域整合,並促進亞洲內部貿易流量。

北美將佔據全球需求的相當大一部分,這主要得益於汽車行業PBT(塑膠、生物基和塑膠)使用量的成長以及生物基BDO(生物基紡織品、 ...

儘管整體成長放緩,歐洲在永續性主導的創新領域仍處於領先地位。 Novamon位於義大利的生物基丁二醇(bio-BDO)生產單元以及多家用於生物循環PBT的複合設施,體現了該地區與循環經濟目標的契合。更嚴格的CLP合規性提高了市場准入門檻,並鼓勵生產特種等級產品,因為這些產品的高溢價可以抵消其高昂的營運成本。南美洲以及中東和非洲地區的需求成長較為溫和,其中巴西的紡織業和沙烏地阿拉伯的石化叢集正成為1,4-丁二醇市場的新驅動力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

第2章 研究假設與市場定義

- 調查範圍

- 調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對四氫呋喃(THF)和氨綸纖維的需求不斷成長

- 更輕的電動車正在推動PBT在汽車連接器中的應用。

- 聚氨酯應用拓展

- 原料藥合成中對藥用級GBL的需求

- 美國和歐盟政府對生物基BDO工廠的補貼

- 市場限制

- 健康與安全問題

- 原物料價格波動

- 來自替代材料的競爭

- 價值鏈分析

- 產能分析(主要生產商)

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(價值及數量)

- 透過生產過程

- 雷佩工藝

- 戴維流程

- 丁二烯工藝

- 環氧丙烷法

- 生物發酵途徑

- 導數

- 四氫呋喃(THF)

- 聚丁烯對苯二甲酸酯(PBT)

- γ-丁內酯(GBL)

- 聚氨酯(PU)

- 其他衍生性商品

- 按最終用戶行業分類

- 車

- 纖維

- 電氣和電子

- 醫療保健和製藥

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ashland

- BASF SE

- Chang Chun Group

- CJ CHEILJEDANG CORP.

- DCC

- Genomatica, Inc.

- Grupa Azoty

- Henan Kaixiang Fine Chemical Co. Ltd

- Jiangsu Hailun Petrochemical Co. Ltd

- LyondellBasell Industries Holdings BV

- Markor Chemicals Group Co. Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Novamont SpA

- Shandong Yuanli Science And Technology Co. Ltd

- Shanxi Sanwei Group Co. Ltd

- Sinochem Internation Corporation

- Sipchem Company

- Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- Xinjiang Tianye(Group)Co. Ltd

第7章 市場機會與未來展望

The 1,4 Butanediol Market size is estimated at 2.56 Million tons in 2025, and is expected to reach 3.05 Million tons by 2030, at a CAGR of 3.55% during the forecast period (2025-2030).

Output expansion rests on the interplay of incremental demand for tetrahydrofuran (THF) in spandex yarns, rising interest in polybutylene terephthalate (PBT) for electric-vehicle (EV) connectors, and the emergence of bio-fermentation routes that lower carbon intensity. Competitive intensity is rising as biotechnology licensors strike alliances with producers seeking greener capacity, while incumbent petrochemical players counter by debottlenecking Reppe-process assets. Government incentives in North America and Europe, combined with rising sustainability targets among automotive, electronics, and apparel brands, are accelerating investment in bio-based capacity even as conventional acetylene routes remain cost-competitive in coal-rich regions. At the same time, price volatility for calcium-carbide-derived acetylene and stricter health-and-safety regulations are pushing producers to diversify feedstocks.

Global 1,4 Butanediol Market Trends and Insights

Rising Demand for Tetrahydrofuran (THF) and Spandex Fibers

THF remains the pivotal derivative, feeding PTMEG for spandex yarns that underpin performance apparel, medical textiles, and automotive interiors. Spandex consumption is shifting from basic athleisure to high-function garments requiring enhanced stretch and recovery. Producers are therefore scaling catalytic upgrades such as biochar-supported Ru-Re systems that cut hydrogen usage and improve selectivity, helping stabilize margins amid recent Asian price swings. Apparel brands' push for recyclability is prompting THF suppliers to explore circular feedstocks, aligning with downstream mills that target lower scope-3 emissions. These converging dynamics keep the 1,4 butanediol market closely tied to the health of the synthetic-fiber chain.

Lightweighting Drive in EVs Fueling PBT Adoption in Auto Connectors

Automakers prioritizing energy-density gains are redesigning high-voltage architectures around PBT housings that trim system weight by 15-30% while preserving dielectric strength. Component makers report faster cycle times via injection molding versus legacy materials, enabling higher line speeds as EV demand accelerates. The North American supply base is responding with new compounding lines that pair bio-circular 1,4-butanediol with recycled polyesters, cutting product carbon footprints by over 30% and satisfying domestic content incentives. This structural tilt toward engineering thermoplastics cements a durable pull for the 1,4 butanediol market through the decade.

Health and Safety Concerns

Global regulators tighten exposure limits as 1,4 butanediol shows acute toxicity affecting the central nervous system. Europe's REACH and CLP frameworks require extensive documentation, triggering higher compliance costs and risking market exit for smaller formulators lacking advanced EHS infrastructure. Large producers mitigate this restraint via closed-loop handling and operator-training programs, yet downstream personal-care and consumer-product sectors face heightened hurdles. These dynamics temper growth in certain high-value applications and necessitate continuous investment in safety management systems across the 1,4 butanediol market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Polyurethane Applications

- Pharma-grade GBL Demand for Solvent-Based API Synthesis

- Raw Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1,4 butanediol market size tied to the Reppe process stood at a commanding 70% share in 2024, underpinned by mature acetylene-based assets and favorable coal economics in China. Yet bio-fermentation volumes are scaling quickly at a 7.40% CAGR, propelled by metabolic-engineering breakthroughs that convert PET-waste-derived ethylene glycol into high-purity BDO. Commercial deployments such as the forthcoming 50,000 ton/yr Vietnamese unit highlight how licensors bridge laboratory titers with industrial purification technologies that now achieve more than 99% recovery at competitive unit costs.

Continued environmental levies on coal-based acetylene and prospective carbon-border adjustments in key export markets raise the cost bar for the Reppe route. Davy and butadiene-based syntheses offer process diversity where propylene-oxide co-product economics or regional butadiene surpluses prevail. The 1,4 butanediol market therefore reflects a portfolio approach in which producers hedge regulatory and feedstock risk by allocating capital across multiple routes while optimizing life-cycle emissions.

The 1, 4 Butanediol Market Report Segments the Industry by Production Process (Reppe Process, Davy Process, Butadiene-Based Process, and More), Derivative (Tetrahydrofuran (THF), Polybutylene Terephthalate (PBT), Gamma-Butyrolactone (GBL), and More), End-User Industry (Automotive, Textile, Electrical and Electronics, and More) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominates the 1,4 butanediol market with a 76% share in 2024 and a projected 3.87% CAGR to 2030. China anchors this leadership through vast Reppe-route capacity supported by coal-derived acetylene, while new projects such as BASF's Zhanjiang Verbund site broaden regional production of engineering plastics. India and South Korea are scaling downstream elastomer, textile, and electronics plants, deepening regional integration and raising intra-Asian trade flows.

North America accounts for a meaningful share of global demand, supported by PBT usage in autos and rising bio-BDO investments. Qore's Iowa plant, scheduled to produce 66,000 tons annually from 2025, leverages corn-based dextrose and captures federal tax incentives, establishing a domestic low-carbon supply that resonates with brand-owner procurement policies. Canada and Mexico add incremental growth through automotive parts and technical-textile exports.

Europe exhibits slower headline expansion but leads in sustainability-led innovation. Novamont's Italian bio-BDO unit and multiple compounding facilities for bio-circular PBT illustrate regional alignment with circular-economy objectives. Stricter CLP compliance elevates entry barriers, encouraging specialty-grade production where premium pricing offsets higher operating costs. South America, the Middle East, and Africa contribute modest but rising demand, with Brazil's textile sector and Saudi Arabia's petrochemical clusters offering new pull for the 1,4 butanediol market.

- Ashland

- BASF SE

- Chang Chun Group

- CJ CHEILJEDANG CORP.

- DCC

- Genomatica, Inc.

- Grupa Azoty

- Henan Kaixiang Fine Chemical Co. Ltd

- Jiangsu Hailun Petrochemical Co. Ltd

- LyondellBasell Industries Holdings B.V.

- Markor Chemicals Group Co. Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Novamont SpA

- Shandong Yuanli Science And Technology Co. Ltd

- Shanxi Sanwei Group Co. Ltd

- Sinochem Internation Corporation

- Sipchem Company

- Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- Xinjiang Tianye (Group) Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Study Assumptions and Market Definition

- 2.1 Scope of the Study

- 2.2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Tetrahydrofuran (THF) and Spandex Fibers

- 4.2.2 Lightweighting Drive in EVs Fueling PBT Adoption in Auto Connectors

- 4.2.3 Expansion of Polyurethane Applications

- 4.2.4 Pharma-grade GBL Demand for Solvent-Based API Synthesis

- 4.2.5 Government Subsidies for Bio-based BDO Plants in US and EU

- 4.3 Market Restraints

- 4.3.1 Health and Safety Concerns

- 4.3.2 Raw Material Price Volatility

- 4.3.3 Competition from Alternative Materials

- 4.4 Value Chain Analysis

- 4.5 Production Capacity Analysis (Major Players)

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Production Process

- 5.1.1 Reppe Process

- 5.1.2 Davy Process

- 5.1.3 Butadiene-Based Process

- 5.1.4 Propylene Oxide-Based Process

- 5.1.5 Bio-fermentation Route

- 5.2 By Derivative

- 5.2.1 Tetrahydrofuran (THF)

- 5.2.2 Polybutylene Terephthalate (PBT)

- 5.2.3 Gamma-Butyrolactone (GBL)

- 5.2.4 Polyurethane (PU)

- 5.2.5 Other Derivatives

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Textile

- 5.3.3 Electrical and Electronics

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ashland

- 6.4.2 BASF SE

- 6.4.3 Chang Chun Group

- 6.4.4 CJ CHEILJEDANG CORP.

- 6.4.5 DCC

- 6.4.6 Genomatica, Inc.

- 6.4.7 Grupa Azoty

- 6.4.8 Henan Kaixiang Fine Chemical Co. Ltd

- 6.4.9 Jiangsu Hailun Petrochemical Co. Ltd

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Markor Chemicals Group Co. Ltd

- 6.4.12 Mitsubishi Chemical Group Corporation

- 6.4.13 NAN YA PLASTICS CORPORATION

- 6.4.14 Novamont SpA

- 6.4.15 Shandong Yuanli Science And Technology Co. Ltd

- 6.4.16 Shanxi Sanwei Group Co. Ltd

- 6.4.17 Sinochem Internation Corporation

- 6.4.18 Sipchem Company

- 6.4.19 Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- 6.4.20 Xinjiang Tianye (Group) Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Advancements in Bio-Based Production Technologies

1,4-丁二醇市場:2026-2032年全球市場預測(依產品類型、製造流程、通路、應用及最終用途產業分類)

1,4-丁二醇市場:2026-2032年全球市場預測(依產品類型、製造流程、通路、應用及最終用途產業分類) 1,4-丁二醇市場報告:按類型、衍生物、最終用途產業和地區分類(2026-2034 年)

1,4-丁二醇市場報告:按類型、衍生物、最終用途產業和地區分類(2026-2034 年) 2026-2030年全球γ-丁內酯市場

2026-2030年全球γ-丁內酯市場 1,4-丁二醇全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)2,3-丁二醇全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

1,4-丁二醇全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)2,3-丁二醇全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 丁二醇產能、產量、市場規模、平均價格及預測(2018-2034 年)

丁二醇產能、產量、市場規模、平均價格及預測(2018-2034 年) 1,4-丁二醇全球市場報告,2026年

1,4-丁二醇全球市場報告,2026年 γ-戊內酯:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

γ-戊內酯:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 2,3-丁二醇的全球市場全球γ-丁內酯市場

2,3-丁二醇的全球市場全球γ-丁內酯市場