|

市場調查報告書

商品編碼

1851926

礦業化學品:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Mining Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

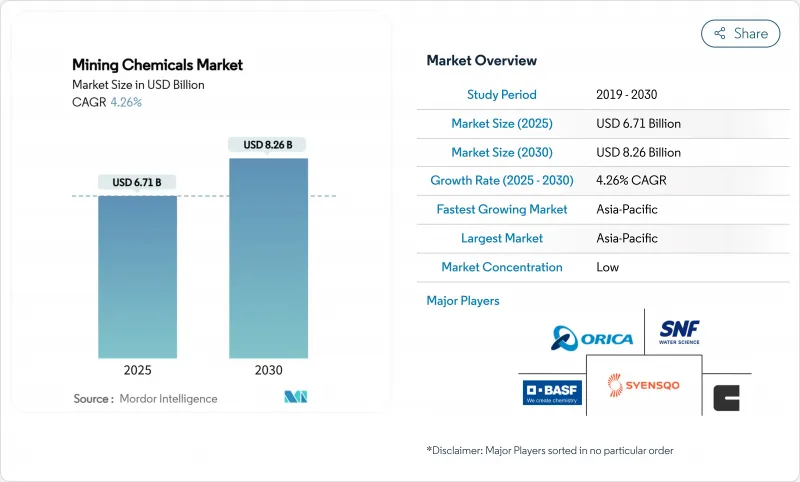

預計到 2025 年,礦業化學品市場規模將達到 67.1 億美元,到 2030 年將達到 82.6 億美元,預測期(2025-2030 年)複合年成長率為 4.26%。

電池金屬需求的成長、日益嚴格的環境法規以及加速的能源轉型,正引導採購決策轉向更具選擇性、更環保高效的試劑配方,這些配方能夠在提高金屬回收率的同時,降低水和電力消耗。亞太地區仍然是主要的生產基地,但北美新增產能以及對濕式冶金的戰略投資,正支撐著亞太其他地區需求的穩定成長。浮選劑仍然是收入的主要驅動力,但成長勢頭最強勁的是溶劑萃取劑,它能夠實現鋰、鎳、鈷和稀土的低碳製程。市場競爭適中,老牌供應商透過併購和數位化最佳化來維持市場佔有率,而規模較小的參與企業則正在拓展生物基化學品和乾法加工助劑業務,以在礦業化學品市場中開闢尚未被充分滿足的細分領域。

全球礦業化學品市場趨勢與洞察

亞太和北美地區的採礦資本支出增加

美國正在推動礦業化學品市場試劑需求的強勁成長。光是在澳大利亞,資源出口收入預計在2024-2025年就將達到3,800億美元,而一系列新的銅、鋰和鎳計劃正在推動浮選、浸出和水處理試劑包的競標競標擴大。銅冶煉廠的加工成本在2024年轉為負值,顯示精礦供應緊張,並刺激了依賴高純度溶劑抽取劑的新型濕式冶金投資。金融分析師估計,廣泛的工業資本支出週期每年將向基礎設施注入2.5兆至5兆美元,透過增加對關鍵礦物的需求,間接增強礦業化學品市場。能夠將數位化計量控制與專用配方相結合的供應商正在贏得長期供應契約,因為營運商正在新資產中實現工廠化學製程的標準化。

電動車和可再生能源供應鏈推動礦產需求成長

對鋰、鎳和鈷礦的探勘正在加速,預計到2030年,全球礦產需求將增加三倍。每加工一噸鋰輝石或紅土礦,所需的化學試劑比傳統基底金屬製程多消耗40%至200%,這推動了整個礦業化學品市場溶劑萃取和結晶試劑用量的成長。同時,電池製造商轉向磷酸鋰鐵和鈉離子電池工藝,也帶來了新的製程控制挑戰,需要客製化螯合劑。隨著地緣政治摩擦加劇關鍵礦產供應中斷的可能性,礦商正在簽訂多年期試劑契約,以對沖供應風險並增強礦業化學品市場的結構性成長。

加強對有毒試劑的全球監管

各國政府目前要求氰化物、汞和黃藥的使用者按照更嚴格的法規進行註冊,這些法規要求持續監測、緊急時應對計畫,並為礦山關閉後的水處理提供財務擔保。 《國際氰化物管理規範》和美國土地管理局近期關於長期處理資金的規定,都推高了合規成本。歐洲監管機構正在考慮進一步禁止使用含全氟烷基和多氟烷基物質(PFAS)的發泡,這將加速礦業化學品市場向替代界面活性劑的轉型。供應商要麼進行改革,要麼面臨市場准入限制,這將減緩短期成長,但會刺激長期創新。

細分市場分析

到2024年,浮選藥劑將佔礦業化學品市場佔有率的55.88%,凸顯了其在從日益複雜的礦石中分離銅、鋅和貴金屬硫化物方面的重要作用。捕收劑佔據了該市場收入的最大佔有率,其次是減壓劑、凝聚劑、攪拌劑和分散劑,這些產品用於調節礦漿化學成分以實現最佳動力學效果。像Syensqo的AEROPHINE系列這樣的優質捕收劑,在用量比傳統黃原酸鹽低30%的情況下,仍能提升選擇性。減壓劑可以消除硫化鐵的稀釋,而合成絮凝劑則可以穩定粗粒浮選迴路中的氣泡尺寸。受礦石品位下降的推動,浮選藥劑的礦業化學品市場規模預計將穩步成長,因為礦石品位下降需要更細的研磨工藝和增加化學品用量以維持回收率。

萃取試劑、稀釋劑、萃取劑和反萃取液的複合年成長率 (CAGR) 為 4.39%,在所有功能領域中最高。這一成長趨勢源自於計畫建造的用於鋰鹵水、鎳紅土礦和多金屬精礦的大型濕式冶金生產線。BASF的濕式冶金平台能夠以比冶煉低 40% 的能耗生產高純度金屬鹽,使溶劑萃取成為極具吸引力的脫碳途徑。

礦業化學品報告按功能(浮選化學品、萃取化學品、磨礦助劑)、應用(礦物加工、污水處理)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

區域分析

亞太地區預計2024年將維持54.56%的礦業化學品市場收入佔有率,主要得益於中國在銅、鎳和稀土加工領域的領先地位,以及印度大力推進國內礦產蘊藏量的商業化。中國的鋰和鎳精煉產業叢集,加上國家對非洲和拉丁美洲礦山的投資,在整體經濟放緩的情況下,支撐了強勁的需求。

隨著華盛頓致力於保障先進電池和關鍵礦產的供應鏈安全,北美市場正蓬勃發展。聯邦政府的激勵措施已推動超過1500億美元的電池和材料計劃投資,從而提振了鋰、鎳和鈷提取生產線的試劑需求。預計到2024年,加拿大探勘支出將增加至41億美元,其中小型礦業公司將積極進行稀土和關鍵金屬礦床的濕式冶金試驗。

歐洲正經歷密集的創新,儘管規模不大。歐盟的《關鍵原料法》支持國內精煉和回收利用,促進了電池材料循環中特殊試劑的使用。BASF和科萊恩從歐洲工廠供應不含PFAS的起泡劑和生物收集器,提高了區域自給自足能力和競爭優勢。南美洲鋰三角和智利銅礦的擴張鞏固了其關鍵地位,而非洲豐富的礦產資源為能夠克服基礎設施和管治複雜性的供應商提供了發展機會。中東的需求雖然不大,但磷酸鹽肥料和鋁的垂直整合大型企劃表明,該地區存在一些選擇性成長點。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太和北美地區的礦業資本投資正在成長

- 電動車和可再生能源供應鏈推動礦產需求

- 大型礦場應制定更嚴格的水循環標準

- 商品價格回升為探勘預算提供支持

- 為符合ESG要求,轉向生物基吸附劑

- 市場限制

- 全球範圍內加強對有毒試劑的監管

- 波動性原油衍生原料的成本

- 無需濕試劑的新型乾加工技術

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按功能

- 漂浮化學品

- 浮選劑

- 抑制劑

- 凝聚劑

- 牙線器

- 分散劑

- 萃取化學品

- 沖淡

- 抽取劑

- 研磨輔助設備

- 漂浮化學品

- 透過使用

- 礦物加工

- 污水處理

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 澳洲、紐西蘭

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF

- 3M

- AECI

- Arkema

- Betachem(Pty)Ltd

- Celanese Corporation

- Chevron Phillips Chemical Company LLC

- Clariant

- CTC(Tennant Consolidated Group)

- Ecolab

- FMC Corporation

- Indorama Ventures Public Limited

- Kemira

- NASACO

- Orica Limited

- Qingdao Ruchang Mining Industry Co. Ltd

- Sasol

- SNF Group

- Syensqo

第7章 市場機會與未來展望

The Mining Chemicals Market size is estimated at USD 6.71 billion in 2025, and is expected to reach USD 8.26 billion by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

Rising demand for battery metals, stricter environmental regulations, and the accelerated energy transition are steering purchasing decisions toward more selective and eco-efficient reagent formulations that raise metal recovery while cutting water and power use. Asia-Pacific remains the dominant production hub, while new capacity in North America and strategic investments in hydrometallurgy underpin steady offtake growth across the rest of the mining chemicals market. Flotation agents continue to anchor revenue, yet the strongest momentum lies in solvent-extraction reagents that enable low-carbon flowsheets for lithium, nickel, cobalt, and rare earths. Competition is moderate: established suppliers defend share through mergers and acquisitions and digital optimization, whereas smaller entrants deploy bio-based chemistries and dry-processing aids to tap under-served niches in the mining chemicals market.

Global Mining Chemicals Market Trends and Insights

Increasing Mining CAPEX in APAC and North America

United States is translating into brisk reagent demand in the mining chemicals market. Australia alone expects resource export earnings to reach USD 380 billion in 2024-25, and the pipeline of new copper, lithium, and nickel projects is widening reagent tenders for flotation, leaching, and water treatment packages. Copper smelter treatment charges turned negative in 2024, signaling tight concentrate supply and encouraging fresh hydrometallurgical investments that rely on high-purity solvent-extraction agents. Financial analysts estimate that the broader industrial capex cycle could inject USD 2.5-5 trillion annually into infrastructure, indirectly fortifying the mining chemicals market through higher demand for critical minerals. Suppliers capable of bundling digital dosing control with specialty formulations are winning long-term supply contracts as operators standardize plant chemistry across new assets.

Surging Mineral Demand from EV and Renewable-Energy Supply Chains

Battery gigafactories commissioned in 2024 catapulted United States cell output by 40%, accelerating the hunt for lithium, nickel, and cobalt units and inflating global mineral demand forecasts three-fold by 2030. Each incremental tonne of spodumene or laterite processed consumes 40-200% more chemical reagents than legacy base-metal flowsheets, lifting solvent-extraction and crystallization reagent volumes across the mining chemicals market. In parallel, cell makers pivoting to lithium iron phosphate and sodium-ion chemistries are creating fresh process-control challenges that require tailor-made chelating agents. Miners are locking in multi-year reagent contracts to de-risk supply as geopolitical friction raises the specter of critical mineral disruptions, reinforcing structural growth for the mining chemicals market.

Tightening Global Regulations on Toxic Reagents

Governments now compel cyanide, mercury, and xanthate users to register under stricter codes that demand continuous monitoring, emergency response plans, and financial assurance for post-closure water treatment. The International Cyanide Management Code and recent U.S. Bureau of Land Management rules on long-term treatment funds have escalated compliance costs. European regulators consider additional bans on PFAS-based frothers, accelerating the shift toward alternative surfactants across the mining chemicals market. Suppliers must either reformulate or face restricted market access, dampening near-term growth but catalyzing long-run innovation.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Water-Recycling Norms in Large Mines

- Shift to Bio-Based Collectors for ESG Compliance

- Emerging Dry-Processing Technologies That Bypass Wet Reagents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flotation reagents captured 55.88% of the mining chemicals market share in 2024, underscoring their essential role in separating copper, zinc, and precious-metal sulfides from increasingly complex ores. Collectors account for the largest slice of this revenue, followed by depressants, flocculants, frothers, and dispersants that adjust pulp chemistry for optimum kinetics. Premium collectors such as Syensqo's AEROPHINE series deliver improved selectivity at doses up to 30% lower than legacy xanthates, a feature prized by miners seeking both cost savings and ESG compliance. Depressants eliminate iron sulfide dilution, while synthetic frothers stabilize bubble size in coarse-particle flotation circuits. The mining chemicals market size for flotation reagents is forecast to grow steadily on the back of declining ore grades, which force operators to grind finer and add more chemistries to maintain recovery.

Extraction reagents, diluents, extractants, and stripping solutions, are expanding at a 4.39% CAGR, the highest among functional segments. This trajectory stems from large-scale hydrometallurgical lines planned for lithium brines, nickel laterites, and polymetallic concentrates. BASF's hydrometallurgy platform consumes 40% less energy than smelting and yields high-purity metal salts, making solvent extraction an attractive decarbonization pathway.

The Mining Chemicals Report is Segmented by Function (Flotation Chemicals, Extraction Chemicals, and Grinding Aids), Application (Mineral Processing and Wastewater Treatment), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific maintained a 54.56% revenue hold on the mining chemicals market in 2024 thanks to China's dominant position in copper, nickel, and rare-earth processing as well as India's push to commercialize domestic mineral reserves. China's lithium and nickel refining clusters, coupled with state-backed investments in African and Latin American mines, underpin resilient demand even amid broader economic softening.

North America's market is growing as Washington pursues supply-chain security for advanced batteries and critical minerals. Federal incentives spurred more than USD 150 billion in announced cell and raw-material projects, reinforcing reagent demand in lithium, nickel, and cobalt extraction lines. Canada's exploration spend climbed to USD 4.1 billion in 2024, with junior players driving hydrometallurgy trials for rare-earth and critical-metal deposits.

Europe exhibits modest volume but intensive innovation. The EU Critical Raw Materials Act supports domestic refining and recycling, lifting specialty reagent uptake in battery material loops. BASF and Clariant supply PFAS-free frothers and bio-collectors from European plants, raising regional self-sufficiency and competitive differentiation. South America's lithium triangle and Chilean copper expansions secure a pivotal role, while Africa's mineral wealth offers upside for suppliers able to navigate infrastructure and governance complexities. Middle East demand is minor, yet vertically integrated mega-projects in phosphate fertilizers and aluminum point to selective growth pockets.

- BASF

- 3M

- AECI

- Arkema

- Betachem (Pty) Ltd

- Celanese Corporation

- Chevron Phillips Chemical Company LLC

- Clariant

- CTC (Tennant Consolidated Group)

- Ecolab

- FMC Corporation

- Indorama Ventures Public Limited

- Kemira

- NASACO

- Orica Limited

- Qingdao Ruchang Mining Industry Co. Ltd

- Sasol

- SNF Group

- Syensqo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Mining CAPEX in APAC and North America

- 4.2.2 Surging Mineral Demand from EV And Renewable-Energy Supply Chains

- 4.2.3 Stricter Water-Recycling Norms in Large Mines

- 4.2.4 Commodity-Price Rebound Sustaining Exploration Budgets

- 4.2.5 Shift to Bio-Based Collectors for ESG Compliance

- 4.3 Market Restraints

- 4.3.1 Tightening Global Regulations on Toxic Reagents

- 4.3.2 Volatile Crude-Derived Raw-Material Costs

- 4.3.3 Emerging Dry-Processing Technologies that Bypass Wet Reagents

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Flotation Chemicals

- 5.1.1.1 Collectors

- 5.1.1.2 Depressants

- 5.1.1.3 Flocculants

- 5.1.1.4 Frothers

- 5.1.1.5 Dispersants

- 5.1.2 Extraction Chemicals

- 5.1.2.1 Diluents

- 5.1.2.2 Extractants

- 5.1.3 Grinding Aids

- 5.1.1 Flotation Chemicals

- 5.2 By Application

- 5.2.1 Mineral Processing

- 5.2.2 Wastewater Treatment

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Australia and New Zealand

- 5.3.1.8 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 3M

- 6.4.3 AECI

- 6.4.4 Arkema

- 6.4.5 Betachem (Pty) Ltd

- 6.4.6 Celanese Corporation

- 6.4.7 Chevron Phillips Chemical Company LLC

- 6.4.8 Clariant

- 6.4.9 CTC (Tennant Consolidated Group)

- 6.4.10 Ecolab

- 6.4.11 FMC Corporation

- 6.4.12 Indorama Ventures Public Limited

- 6.4.13 Kemira

- 6.4.14 NASACO

- 6.4.15 Orica Limited

- 6.4.16 Qingdao Ruchang Mining Industry Co. Ltd

- 6.4.17 Sasol

- 6.4.18 SNF Group

- 6.4.19 Syensqo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球礦業電化學加工市場:市場規模、佔有率、趨勢分析(按製程類型、回收金屬和地區分類)、細分市場預測,2025-2033年

全球礦業電化學加工市場:市場規模、佔有率、趨勢分析(按製程類型、回收金屬和地區分類)、細分市場預測,2025-2033年 2025 年至 2033 年礦用化學品市場規模、佔有率、趨勢及預測(按產品類型、礦物類型、應用和地區)

2025 年至 2033 年礦用化學品市場規模、佔有率、趨勢及預測(按產品類型、礦物類型、應用和地區) 全球礦業化學品市場(按類型、形式和應用)預測 2025-2032

全球礦業化學品市場(按類型、形式和應用)預測 2025-2032 礦業浮選化學品市場規模、佔有率、成長分析(按化學品類型、礦石類型、應用、最終用途、地區)- 產業預測 2025-2032

礦業浮選化學品市場規模、佔有率、成長分析(按化學品類型、礦石類型、應用、最終用途、地區)- 產業預測 2025-2032 2032 年礦山浮選化學品市場預測:按礦石類型、化學類型、應用、最終用戶和地區進行的全球分析

2032 年礦山浮選化學品市場預測:按礦石類型、化學類型、應用、最終用戶和地區進行的全球分析 2025年礦業化學品全球市場報告

2025年礦業化學品全球市場報告 礦業化學品市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035)

礦業化學品市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035) 礦山浮選化學品市場報告:趨勢、預測和競爭分析(至 2031 年)

礦山浮選化學品市場報告:趨勢、預測和競爭分析(至 2031 年) 鑽井化學品市場:按化學品、流體類型、應用和地區分類

鑽井化學品市場:按化學品、流體類型、應用和地區分類 礦業用浮游化學品的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

礦業用浮游化學品的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)