|

市場調查報告書

商品編碼

1851909

醇醚:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Alcohol Ethoxylates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

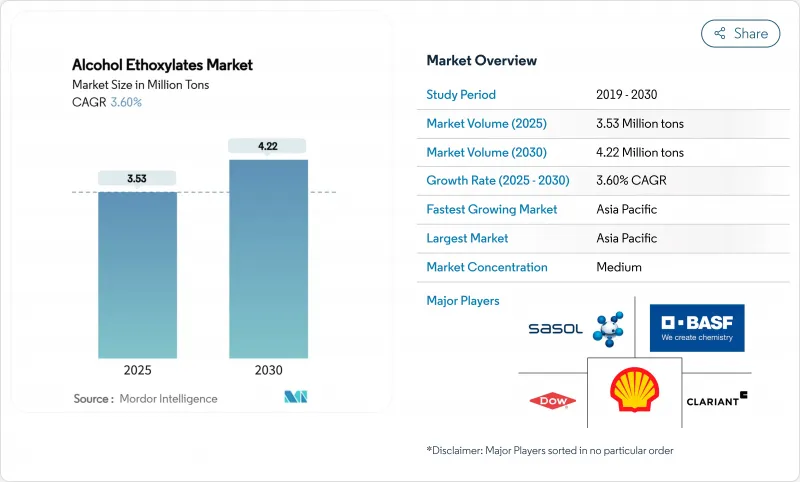

預計到 2025 年,醇醚市場規模將達到 353 萬噸,到 2030 年將達到 422 萬噸,預測期(2025-2030 年)複合年成長率為 3.60%。

這種溫和的成長反映了在新的、日益嚴格的環氧乙烷排放永續性法規的背景下,市場需求曲線日益成熟。生產商正透過生物基原料專案和更窄範圍的乙氧基化技術來應對,這些技術可以降低能源強度並提高生物分解性。高成長的亞洲經濟體對個人護理和商用清潔應用的強勁需求,正在推動印尼和巴西下游油脂化學品產能的擴張。同時,北美和歐洲的監管壓力迫使製造商提高排放標準,這推高了成本,並加速了向低碳界面活性劑等級的創新。這些趨勢表明,技術差異化和檢驗的永續性比單純的規模經濟更為重要。

全球醇醚市場趨勢與洞察

亞太地區對個人和家庭護理的需求不斷成長

中國、印度和東南亞地區持續的都市化和收入成長繼續推動高階個人護理產品的消費。負責人青睞醇醚類化合物,其溫和的特性和冷水清潔能力與這些市場流行的濃縮型液體清潔劑相得益彰。跨國公司正在擴大其通過生質能平衡認證的永續產品組合,這標誌著其正向低碳界面活性劑供應鏈轉型。零售商向電商平台的轉型進一步推動了產品差異化,供應商也面臨著在提供感官性能聲明的同時,提供透明的永續性數據的壓力。

在工業和機構清潔產品中的使用日益增多

即使在疫情高峰過後,醫療保健、食品服務和交通樞紐的強化衛生通訊協定仍將持續實施。醇醚類界面活性劑可在各種 pH 值和溫度範圍內有效去除污漬,即使在硬水條件下也能保持穩定的性能,使配方師無需使用磷酸鹽或溶劑即可滿足嚴格的消毒標準。北美和西歐市場成長最為強勁,這些地區的工業衛生法規正在推動對溫和、易生物分解界面活性劑的需求。

原物料價格波動

環氧乙烷和脂醇類價格的波動正在擠壓沒有避險或垂直整合的小型生產商的利潤空間。一家北美主要供應商近期宣布的乙二醇醚價格上漲,進一步證實了乙氧基化成本的上漲壓力。依賴南亞進口的製劑生產商由於外匯風險和運費額外費用,面臨最大的風險。

細分市場分析

至2024年,油脂化學品級產品將佔醇醚市場佔有率的58.19%,其複合年成長率(CAGR)為3.91%,增速將超過石化產品。東南亞的垂直整合確保了原料供應的穩定性,並減少了物流排放。企業採購政策強制要求可再生碳含量,這進一步推動了向生物基供應的轉型。歐洲和北美生產商已通過ISCC PLUS認證工廠並增加綠色環氧乙烷產量來應對這一挑戰,緩解了石化產品的不利影響,但這一趨勢並未逆轉。

油脂化學產業受益於雅加達和吉隆坡附近棕櫚油和椰子油蒸餾叢集,這些集群以低成本向當地的乙氧基化裝置供應原料。採用窄範圍技術的製造商能夠提供個人護理乳化所需的等級一致性,從而獲得溢價。儘管如此,石化產品正在對成本敏感的通用清潔劑市場站穩腳跟,而碳排放資訊揭露在這些市場仍然是可選的。

到2024年,C12-C14餾分將佔醇醚市場規模的41.55%,年增率達4.08%。其兼具清潔力和生物分解性,符合不斷變化的區域法規。較短的C9-C11同系物在對快速潤濕性要求較高的工業清潔劑中越來越受歡迎,而較長的C15-C18鏈則用於高階個人保健產品和油田化學品。

配方師們正擴大採用窄範圍的C12-C14乙氧基化物,以最大限度地減少遊離醇含量,並改善氣味和產品穩定性。他們也正在研究在低溫下不易結晶的支鏈類似物,以擴大其在冬季洗車液的應用。

區域分析

到2024年,亞太地區將佔據全球醇醚市場52.18%的佔有率,並在2030年之前以4.76%的複合年成長率引領成長。可支配收入的成長、零售清潔劑滲透率的提高以及充足的油脂化學品原料供應,正吸引著本土獨立企業和跨國巨頭的目光。印尼新建的脂醇類聯合裝置將為新加坡和泰國的區域個人護理中心提供醇醚化產品,從而加強亞洲內部貿易循環,並降低對歐洲的進口依賴。

北美是一個成熟且創新主導的市場環境,環境、健康和安全法規在採購決策中佔據主導地位。美國環保署對乙氧基化丙氧基化C12-C15醇類化合物用於農藥的耐受性豁免,凸顯了此技術在作物保護領域公認的安全性。種植者正優先考慮綠色化學升級數位化供應鏈追蹤,以符合品牌所有者的透明度計劃。

在歐洲,相關法規和政策正在修訂,推出了更嚴格的政策,例如數位產品護照和更高的生物分解性閾值。儘管需求成長緩慢,但供應商仍能從獲得永續性認證的產品中獲得溢價。在拉丁美洲,一家大型石化集團收購了巴西最大的乙氧基化物生產商,從而增強了供應,並使區域客戶能夠獲得價格更低的產品。在中東和非洲,儘管銷售量較低,但市場對高效能液體清潔劑的需求仍然強勁。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區對個人和家庭護理的需求不斷成長

- 在工業和機構清潔產品中的使用日益增多

- 擴大下游油脂化學品生產能力

- 人們衛生和清潔意識的提高

- 增加農藥使用以保護農作物

- 市場限制

- 原物料價格波動

- 日益成長的環境問題

- 是否有合適的替代方案

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按原產地

- 油脂化學品

- 石油化工衍生性商品

- 按碳鍊長度

- C9-C11

- C12-C14

- C15-C18 和支鏈

- 按形式

- 液體

- 糊狀/固態

- 透過使用

- 個人護理

- 肥皂和清潔劑

- 工業和設施清潔

- 農業化學品

- 油漆和塗料

- 紡織加工

- 其他應用(石油和天然氣(提高採收率、鑽井液))

- 地理

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BASF

- Clariant

- Croda International plc

- Dow

- Evonik Industries AG

- Huntsman International LLC

- India Glycols Limited

- Indorama Ventures Public Company Limited

- Kao Chemicals Europe, SLU

- Kemipex

- Mitsui Chemicals Inc.

- Nouryon

- Procter & Gamble

- SABIC

- Sasol Ltd

- Shell plc

- Stepan Company

- Syensqo

- Thai Ethoxylate Co., Ltd.(TEX)

第7章 市場機會與未來展望

The Alcohol Ethoxylates Market size is estimated at 3.53 Million tons in 2025, and is expected to reach 4.22 Million tons by 2030, at a CAGR of 3.60% during the forecast period (2025-2030).

The moderate expansion reflects a maturing demand curve even as new sustainability rules tighten around ethylene oxide emissions. Producers are responding with bio-based feedstock programs and narrower-range ethoxylation technologies that cut energy intensity and improve biodegradability. Strong personal-care and institutional cleaning demand in high-growth Asian economies, plus the build-out of downstream oleochemical capacity in Indonesia and Brazil, underpin steady volume gains. At the same time, regulatory pressure in North America and Europe forces manufacturers to upgrade emission controls, adding cost yet accelerating innovation toward low-carbon surfactant grades. These cross-currents define a competitive arena where technical differentiation and verified sustainability credentials outweigh pure scale economies.

Global Alcohol Ethoxylates Market Trends and Insights

Growing Personal-Care & Home-Care Demand in Asia-Pacific

Sustained urbanization and income growth in China, India, and Southeast Asia continue to lift premium personal-care consumption. Formulators favor alcohol ethoxylates for their mildness and cold-water detergency, traits well matched to concentrated liquid detergents popular in these markets. Multinationals expand sustainable portfolios certified under biomass balance schemes, signaling a pivot toward lower-carbon surfactant supply chains. Retail migration to e-commerce platforms further amplifies product differentiation, pushing suppliers to deliver transparent sustainability data alongside sensory performance claims.

Rising Use in Industrial & Institutional Cleaning Formulations

Elevated hygiene protocols across healthcare, food service, and transport hubs remain in force even after the pandemic peak. Alcohol ethoxylates provide effective soil removal over broad pH and temperature bands and deliver stable performance in hard-water conditions, enabling formulators to meet tightened disinfection standards without phosphates or solvents. Growth is strongest in North America and Western Europe, where regulatory mandates for occupational health drive demand for low-irritancy, readily biodegradable surfactants.

Feedstock Price Volatility

Swing pricing for ethylene oxide and fatty alcohols compresses margins for smaller producers lacking hedging programs or vertical integration. Recent glycol ether increases announced by a major North American supplier underscore the upward pressure on ethoxylation costs. Import-reliant formulators in South Asia face the greatest exposure due to currency risk and freight surcharges.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Downstream Oleochemical Capacity

- Rising Awareness Regarding Hygiene and Cleanliness

- Growing Environmental Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oleochemical grades captured 58.19% of alcohol ethoxylates market share in 2024 and will grow faster than petrochemical peers at a 3.91% CAGR. Vertical integration in Southeast Asia assures feedstock certainty and lowers logistics emissions. Corporate procurement policies that mandate renewable carbon content continue to migrate volumes toward bio-based supply. Producers in Europe and North America respond by certifying plants under ISCC PLUS and ramping green ethylene oxide output, which moderates the petrochemical retreat but does not reverse the trend.

The oleochemical segment benefits from palm and coconut oil distillation clusters near Jakarta and Kuala Lumpur that feed local ethoxylation units at lower cost. Producers marketing narrow-range technology achieve premium pricing by offering grade consistency required in personal-care emulsions. Nevertheless, petrochemical variants retain a foothold in cost-sensitive commodity detergents where carbon disclosure remains voluntary.

The C12-C14 cut constituted 41.55% of the alcohol ethoxylates market size in 2024, enjoying a 4.08% growth trajectory. Its balance of detergency and ready biodegradation meets evolving regional regulations. Shorter C9-C11 homologues gain traction in industrial cleaning where rapid wetting is prized, while longer C15-C18 chains serve premium personal-care and oilfield chemistries.

Formulators increasingly request narrow-range C12-C14 ethoxylates that minimize free alcohol content, improving odor and product stability. Research has also explored branched analogues that resist crystallization at low temperature, broadening usage in winter-grade vehicle washes.

The Alcohol Ethoxylates Market Report Segments the Industry by Origin Type (Oleochemical and Petrochemical), Carbon Chain Length (C9-C11 (Linear Alcohol Ethoxylates), C12-C14 (Lauryl Alcohol Ethoxylates), and More), Form (Liquid and Paste/Solid), Application (Personal Care, Soap and Detergents, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 52.18% of alcohol ethoxylates market size in 2024 and leads growth at 4.76% CAGR through 2030. Rising disposable income, expanding retail detergent penetration, and robust oleochemical feedstock supplies attract both local independents and multinational majors. Indonesia's new fatty alcohol complexes supply ethoxylation units that serve regional personal-care hubs in Singapore and Thailand, tightening intra-Asian trade loops and curbing import reliance on Europe.

North America presents a mature, innovation-led environment where environmental health and safety regulations dominate procurement decisions. The US Environmental Protection Agency's tolerance exemption for ethoxylated propoxylated C12-C15 alcohols in agrochemical use underscores the technology's accepted safety profile in crop protection. Producers emphasize green chemistry upgrades and digitalized supply tracking to comply with brand-owner transparency programs.

Europe faces a stricter policy backdrop as the revision of Regulation 648/2004 rolls in digital product passports and enhanced biodegradability thresholds. While demand growth is modest, suppliers enjoy premium pricing for verified sustainable grades. Latin America benefits from an enhanced supply position following a major petrochemical group's acquisition of Brazil's largest ethoxylate producer, ensuring regional customers receive local, lower-freight product. The Middle East and Africa record smaller volumes but exhibit keen interest in concentrated liquid detergents, a format that favors high-actives alcohol ethoxylates.

List of Companies Covered in this Report:

- BASF

- Clariant

- Croda International plc

- Dow

- Evonik Industries AG

- Huntsman International LLC

- India Glycols Limited

- Indorama Ventures Public Company Limited

- Kao Chemicals Europe, S.L.U.

- Kemipex

- Mitsui Chemicals Inc.

- Nouryon

- Procter & Gamble

- SABIC

- Sasol Ltd

- Shell plc

- Stepan Company

- Syensqo

- Thai Ethoxylate Co., Ltd. (TEX)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing personal-care & home-care demand in Asia-Pacific

- 4.2.2 Rising use in industrial & institutional cleaning formulations

- 4.2.3 Expanding downstream oleochemical capacity

- 4.2.4 Rising awareness regarding hygiene and cleanliness

- 4.2.5 Growing usage in agrochemicals for crop protection

- 4.3 Market Restraints

- 4.3.1 Feedstock price volatility

- 4.3.2 Growing environmental concerns

- 4.3.3 Availability of suitable alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Origin Type

- 5.1.1 Oleochemical-derived

- 5.1.2 Petrochemical-derived

- 5.2 By Carbon Chain Length

- 5.2.1 C9-C11

- 5.2.2 C12-C14

- 5.2.3 C15-C18 & Branched

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Paste / Solid

- 5.4 By Application

- 5.4.1 Personal Care

- 5.4.2 Soaps and Detergents

- 5.4.3 Industrial and Institutional Cleaning

- 5.4.4 Agricultural Chemicals

- 5.4.5 Paints and Coatings

- 5.4.6 Textile Processing

- 5.4.7 Other Applications (Oil & Gas (EOR, drilling fluids))

- 5.5 Geography

- 5.5.1 Asia-Pacifc

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacifc

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 BASF

- 6.4.2 Clariant

- 6.4.3 Croda International plc

- 6.4.4 Dow

- 6.4.5 Evonik Industries AG

- 6.4.6 Huntsman International LLC

- 6.4.7 India Glycols Limited

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 Kao Chemicals Europe, S.L.U.

- 6.4.10 Kemipex

- 6.4.11 Mitsui Chemicals Inc.

- 6.4.12 Nouryon

- 6.4.13 Procter & Gamble

- 6.4.14 SABIC

- 6.4.15 Sasol Ltd

- 6.4.16 Shell plc

- 6.4.17 Stepan Company

- 6.4.18 Syensqo

- 6.4.19 Thai Ethoxylate Co., Ltd. (TEX)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

醇醚市場:依產品類型、實體形態、最終用途產業及通路分類-2026-2032年全球市場預測

醇醚市場:依產品類型、實體形態、最終用途產業及通路分類-2026-2032年全球市場預測 2026年全球烷氧基化物市場報告2026年全球醇醚市場報告

2026年全球烷氧基化物市場報告2026年全球醇醚市場報告 烷氧基化物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用戶、地區和競爭格局分類,2020-2030年預測

烷氧基化物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用戶、地區和競爭格局分類,2020-2030年預測 烷氧基化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

烷氧基化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 醇乙氧基化物市場規模、佔有率、成長分析(按產品、應用、最終用途和地區)- 產業預測,2025 年至 2032 年

醇乙氧基化物市場規模、佔有率、成長分析(按產品、應用、最終用途和地區)- 產業預測,2025 年至 2032 年 烷氧基化物市場報告:2031 年趨勢、預測與競爭分析

烷氧基化物市場報告:2031 年趨勢、預測與競爭分析 全球醇乙氧基化物市場(按產品、應用、最終用途和地區分類)脂肪醇聚氧乙烯醚市場報告:2030 年趨勢、預測與競爭分析

全球醇乙氧基化物市場(按產品、應用、最終用途和地區分類)脂肪醇聚氧乙烯醚市場報告:2030 年趨勢、預測與競爭分析 全球烷氧基化物市場:市場規模、佔有率、趨勢分析報告 - 按等級、按類型、按應用、按最終用途行業、按地區、展望、預測,2024-2031 年

全球烷氧基化物市場:市場規模、佔有率、趨勢分析報告 - 按等級、按類型、按應用、按最終用途行業、按地區、展望、預測,2024-2031 年