|

市場調查報告書

商品編碼

1851904

門窗:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Windows And Doors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

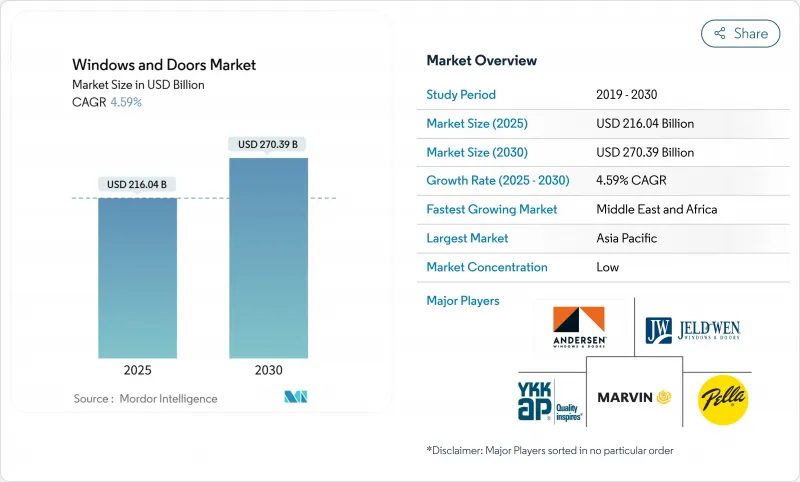

預計到 2025 年,門窗市場價值將達到 2,160.4 億美元,到 2030 年將達到 2,703.9 億美元,複合年成長率為 4.59%。

對節能建築圍護結構的強勁需求、日益嚴格的性能法規以及穩定的維修支出,共同支撐著這一成長。美國能源之星7.0版更新已將寒冷地區的U值上限提高至0.22,從而促進了三層玻璃和先進框架技術的應用。同時,歐盟《建築能源性能指令》(EPBD)也在推動建築規範朝著2030年實現零排放建築的目標邁進,加速了高性能玻璃在住宅和商業計劃的應用。儘管面臨鋁材和勞動力短缺的持續挑戰,供應側的轉變,特別是輕質框架、模組化結構和智慧玻璃的升級,仍在不斷拓展設計選擇並縮短前置作業時間。能夠將材料創新、自動化製造和在地化履約相結合的製造商,將更有利於掌握下一波規範主導的門窗市場需求浪潮。

全球門窗市場趨勢與洞察

房屋翻新熱潮及老舊住宅存量。

不斷上漲的借貸成本鎖定了有利的利率,促使大多數屋主將可支配資金用於房屋升級而非搬遷。 2024年房屋翻新支出激增,預計2025年將維持5%的成長。這主要是由於北美和歐洲的住房基礎設施老化,許多房屋的窗框使用年限在20至39年之間。美國沿海縣近一半的颶風災後重建計劃都包括門窗維修,凸顯了門窗兼具防護和節能功能的雙重價值。翻新專家也注意到,「居家養老」的需求激增,人們傾向於選擇更寬的開口、更低的門檻高度和符合人體工學的金屬製品。這些使用模式使門窗市場與消費者對健康和適應性的重視緊密契合。

能源效率法規(能源之星 V7.0、歐盟 EPBD)

主要經濟體正以協調一致的方式加強性能標準。在美國,能源之星V7.0將U值較上一版本降低了15%,有效實現了寒冷氣候下三層玻璃結構的標準化。 2024年國際能源效率標準將空氣洩漏上限設定為0.35立方英尺/分鐘/平方英尺,並強制要求改善密封條和框架設計。在歐洲,建築能源性能指令(EPBD)已修訂,納入了2030年起新建建築的零排放要求,以及現有建築的分階段維修目標。稅額扣抵和公用事業折扣等市場優惠政策可以抵消部分初始成本,加快投資回收期,並促進門窗市場的產品差異化。

原物料價格波動(鋁、PVC)

能源成本上漲和冶煉廠停產導致鋁供應減少,推高了平均溢價,延長了前置作業時間,而此時疫情後的需求剛開始復甦。聚氯乙烯(PVC)生產商也面臨原料成本上漲和更嚴格的氯氣生產法規的雙重壓力,尤其是在環境監管嚴格的歐洲。為了避免價格波動,生產商開始轉向使用回收鋁坯、熱塑性增強型材以及區域採購協議。輕質複合材料框架在不犧牲強度的前提下減少了金屬用量,市佔率持續成長。然而,價格波動正在擠壓小型加工商的淨利率,減緩計劃訂單,並限制門窗市場部分領域的成長。

細分市場分析

2024年,門將佔據門窗銷售額的58.56%,進一步鞏固了其在各類建築物中的基礎性地位。安全門、防火組件和智慧鎖具的持續高更換頻率,即使在經濟週期放緩期間也能保持相對穩定的需求。相較之下,窗戶的年複合成長率將達到7.49%,這主要得益於嚴格的熱增益限制以及建築整合光伏技術的興起——該技術可直接透過玻璃吸收太陽能。這種拉動效應使窗戶在門窗市場中處於技術前沿。

儘管門窗製造商正大力投資多點鎖、抗衝擊面板和智慧家居無縫整合,但利潤最高的淨利率正轉向結合電致變色塗層和太陽能收集夾層的先進窗戶解決方案。勞倫斯柏克萊國家實驗室表明,此類窗戶安裝可使整棟建築的能源消耗降低高達15.9%,這項指標足以支撐其高價和較短的投資回收期。因此,預計窗戶市場的細分規模將從2025年的890億美元擴大到2030年的1,230億美元。

金屬框架,尤其是鋁材,由於其優異的強度重量比、纖細的視覺效果和可回收性,預計到2024年將佔銷售額的46.62%。鋁框架最常用於高層建築、醫院和交通樞紐的門窗和玻璃建築幕牆。然而,在快速發展的郊區和近郊住宅區,塑膠/uPVC型材的成長速度最快,達到8.73%,這些地區的預算意識和快速施工至關重要。現代配方中嵌入了玻璃纖維或鋼微增強材料,在不犧牲剛度的前提下實現了良好的隔熱性能,解決了先前人們對PVC結構局限性的批評。

對產品生命週期的嚴格審查正促使生產商轉向不含鄰苯二甲酸酯和鉛的穩定劑,並採用閉迴路回收方式,將型材邊角料轉化為新的擠出產品。同時,新興的木塑複合材料和玻璃纖維框架兼具鋁材的剛性和乙烯基的隔熱性能。在此背景下,預計2025年至2030年間, 封閉式門窗市場規模將成長140億美元,而由於原鋁產能受限,金屬市場的成長預計將會放緩。歐盟關於2030年後可能逐步淘汰PVC的監管討論,既帶來了戰略風險,也推動了可回收和生物基聚合物混合物的創新。

門窗市場按產品類型(門、窗)、材料類型(木材、金屬、塑膠/UPVC/複合材料)、應用方式(平開、推拉、其他)、最終用戶(住宅和非住宅(商業、工業、機構))、安裝類型(新建、更換/維修)以及地區進行細分。市場預測以價值(美元)和數量(台)為單位。

區域分析

亞太地區預計到2024年將佔全球銷售額的42.13%,這主要得益於快速的城市建設以及政府對節能環保建築的政策獎勵。中國、印度和印尼等國的國家建築規範正逐步降低U值(傳熱係數),為抗熱裂紋框架和低輻射隔熱玻璃設定了有利的基準。當地製造商正擴大向周邊市場出口單元式建築幕牆,不僅加強了區域供應鏈,也降低了門窗市場的物流成本。

北美市場規模位居第二,這主要得益於強勁的房屋維修支出和日益成熟的異地住宅市場。儘管房屋開工量有所波動,但能源之星稅額扣抵和州級雨水補貼政策仍支撐著強勁的需求。技術純熟勞工短缺仍然是限制成長的主要瓶頸,但大型工廠自動化程度的提高和一體化安裝專案的實施正在緩解週期放緩的問題。在加拿大和美國北部,三層玻璃窗正迅速成為多用戶住宅計劃的主流選擇,以降低暖氣負荷。

在歐洲,雖然絕對佔有率較小,但利潤空間卻很大,因為歐盟的《能源性能指令》(EPBD)規定,從2030年起,新建建築必須達到零排放目標。最低能源效率標準也確保了維修工程的持續進行,屆時,能源效率最差的16%的非住宅存量將完成升級改造。擁有檢驗的環境產品聲明和循環經濟框架的製造商可以獲得優先採購評分。在巴黎和柏林等人口稠密的城市,門窗市場對隔音產品的需求旺盛,而自適應遮光系統在地中海度假勝地也逐漸成為標配。

到2030年,中東和非洲將以7.10%的複合年成長率實現最快成長,這主要得益於大規模的酒店、醫療保健和教育計劃。炎熱的氣候需要採用太陽能控制嵌裝玻璃,並配合可適應室內外混合居住模式的寬搖擺門系統。政府對綠建築認證的強制性要求以及不斷上漲的能源費用正在加速向低輻射塗層的轉變。海灣國家的本地組裝基地已開始為東非走廊提供服務,縮短了前置作業時間,並增強了門窗市場的區域韌性。

南美洲經濟成長強勁,巴西、哥倫比亞和智利的都市化進程為其提供了有力支撐。高通膨限制了短期可自由支配支出,但長期基礎建設的權益正在推動各項基礎設施計劃向前發展。智利和秘魯已修訂建築性能規範,要求高海拔地區的新建築必須使用雙層玻璃,這進一步擴大了節能窗戶的潛在市場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 房屋翻新熱潮及老舊住宅存量。

- 能源效率法規(能源之星 V7.0、歐盟 EPBD)

- 亞太地區的快速都市化和基礎設施投資

- 模組化建築促進了單元式建築幕牆的採用

- 抗衝擊玻璃窗的保險福利

- 建築一體成型光伏(BIPV)窗的滲透率

- 市場限制

- 原物料價格波動(鋁、PVC)

- 安裝工人短缺,缺乏熟練勞動力

- 對黑膠唱片生命週期排放的ESG(環境、社會和治理)審查

- 高階商業建築的智慧玻璃化

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 依產品類型

- 門

- 視窗

- 材料

- 木頭

- 金屬

- 塑膠/PVC/複合材料

- 透過使用

- 搖擺

- 滑動

- 折疊式的

- 旋轉和其他

- 最終用戶

- 住宅

- 非住宅(商業、工業、機構)

- 按安裝類型

- 新建工程

- 更換/改裝

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- Nordix(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Andersen Corporation

- JELD-WEN Holding Inc.

- Pella Corporation

- YKK AP Inc.

- Marvin Windows & Doors

- Masonite International

- Cornerstone Building Brands/Ply Gem

- MI Windows and Doors

- LIXIL Corporation

- ASSA ABLOY Group

- Rehau Group

- VEKA AG

- Deceuninck NV

- Profine GmbH(Kommerling)

- Saint-Gobain Building Glass & Solutions

- Schuco International

- Aluplast GmbH

- Fenesta Building Systems(DCM Shriram)

- PGT Innovations

- Atrium Corporation

第7章 市場機會與未來展望

The windows and doors market was valued at USD 216.04 billion in 2025 and is forecast to reach USD 270.39 billion by 2030, posting a 4.59% CAGR.

Strong demand for energy-efficient building envelopes, tighter performance codes, and steady renovation spend underpin this growth. The ENERGY STAR Version 7.0 update is already pushing U-factor limits toward 0.22 in colder U.S. zones, motivating triple-pane glazing and advanced framing. Parallel momentum in the EU's Energy Performance of Buildings Directive (EPBD) is steering specifications toward zero-emission buildings by 2030, accelerating adoption of high-performance fenestration across both residential and commercial projects. Supply-side shifts-especially light-weight framing options, modular construction, and smart-glass upgrades-continue to widen design choices and shorten lead times, even as aluminum and labor shortages remain persistent headwinds. Manufacturers able to combine material innovation, automated fabrication, and regional fulfillment are positioned to capture the next wave of specification-driven demand in the windows and doors market.

Global Windows And Doors Market Trends and Insights

Residential renovation boom and aging housing stock

Elevated borrowing costs have locked most homeowners into favorable rates, channeling discretionary capital toward upgrades rather than relocation. Remodel spending grew sharply in 2024 and is projected to maintain 5% growth in 2025, supported by an aging North American and European housing base, much of which crosses the 20- to 39-year prime replacement window for fenestration. Nearly half of hurricane recovery projects in coastal U.S. counties now include window or door upgrades, highlighting the dual value of protective and energy-saving features. Remodeling professionals also note a surge in "aging-in-place" requests that favor wider clear openings, lower sill heights, and ergonomic hardware. These usage patterns keep the windows and doors market firmly aligned with consumer wellness and resilience priorities.

Energy-efficiency regulations (ENERGY STAR V7.0, EU EPBD)

Performance codes are tightening in a coordinated fashion across major economies. In the United States, ENERGY STAR V7.0 pushes U-factors down 15% from the previous cycle, practically standardizing triple-pane construction in cold climates. The 2024 International Energy Conservation Code now caps air leakage at 0.35 cfm/ft2, demanding improved weather-stripping and frame design. Europe's revised EPBD locks in zero-emission requirements for new buildings starting 2030, along with staged renovation targets for the existing stock. Attractive tax credits and utility rebates offset part of the upfront cost, fostering faster payback and heightening product differentiation within the windows and doors market.

Raw-material price volatility (aluminum, PVC)

Energy cost spikes and smelter curtailments have trimmed aluminum supply just as post-pandemic demand recovered, lifting average premiums and lengthening lead times. PVC producers also struggle with higher input costs and stricter chlorine-production rules, especially in Europe, where environmental scrutiny is intense. To hedge volatility, manufacturers are pivoting toward recycled billet, thermoplastic-reinforced profiles, and regional sourcing agreements. Lightweight composite frames, which reduce metal use without sacrificing strength, continue to gain share. Nonetheless, price swings squeeze smaller fabricators' margins, slowing project awards and tempering growth in parts of the windows and doors market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid urbanization and infrastructure spend in Asia-Pacific

- Modular construction driving unitized facades

- Skilled-labor shortage for installation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Doors generated the majority of 2024 revenue at 58.56%, confirming their foundational role in every building type. Security doors, fire-rated assemblies, and smart locks sustain a replacement cadence that keeps demand relatively stable even during cyclical slowdowns. Conversely, windows outpace in growth at a 7.49% CAGR thanks to stringent heat-gain limits and the rise of building-integrated photovoltaics, which capture solar energy directly through glass. This pull-through effect positions windows as the technological spearhead of the windows and doors market.

Door makers invest in multi-point locking, impact-rated panels, and seamless smart-home integration; however, the highest margins are migrating to advanced window solutions that fuse electro-chromic coatings with solar-harvesting interlayers. Lawrence Berkeley National Laboratory recorded up to 15.9% whole-building energy savings from such installations, a metric that drives premium pricing and short paybacks. As a result, the windows and doors market size for the window segment is projected to rise from USD 89 billion in 2025 to USD 123 billion by 2030, even though the door segment will still dominate on volume.

Metal frames, particularly aluminum, held 46.62% revenue in 2024 because of their favorable strength-to-weight ratio, slim sightlines, and recyclability. Curtain-wall high-rises, hospitals, and transport hubs nearly always specify aluminum frames for both doors and glazed facades. Yet plastic/uPVC profiles are capturing the fastest gains-8.73% CAGR-inside fast-growing suburban and peri-urban housing corridors where budget sensitivity and quick installation matter most. Updated formulations featuring embedded fiberglass or steel micro-reinforcements deliver thermal performance without compromising rigidity, answering earlier criticisms of PVC's structural limits.

Lifecycle scrutiny is pushing producers toward phthalate-free, lead-free stabilizers and closed-loop recycling commitments that turn profile off-cuts into new extrusions. Meanwhile, emerging wood-plastic composites and fiberglass frames offer a middle ground between aluminum's stiffness and vinyl's insulative edge. Against this backdrop, the windows and doors market size for PVC systems is projected to add USD 14 billion between 2025 and 2030, while metal growth moderates in line with primary-aluminum capacity constraints. Regulatory debates in the EU about potential PVC phase-downs beyond 2030 create strategic risk but also encourage innovation in recyclable and bio-based polymer blends.

The Windows and Doors Market is Segmented by Product Type (Doors, Windows), Material Type (Wood, Metal, Plastic / UPVC / Composite), Application (Swinging, Sliding, and More), End User (Residential and Non-Residential (Commercial, Industrial, Institutional)), Installation Type (New Construction, Replacement / Retrofit), Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific held 42.13% of 2024 revenue, anchored by rapid urban build-outs and policy incentives for energy-conserving, climate-resilient construction. National building codes in China, India, and Indonesia have progressively lowered allowable U-values, setting a lucrative baseline for thermally broken frames and low-e insulated glass. Indigenous fabricators increasingly export unitised facades to neighboring markets, strengthening intra-regional supply chains and shaving logistics costs for the windows and doors market.

North America ranks second in size, propelled by strong renovation expenditure and a maturing off-site housing segment. ENERGY STAR tax credits and state-level storm hardening grants keep demand solid despite fluctuating housing starts. Skilled-labor scarcity remains the main growth bottleneck; however, rising automation rates at major plants, plus integrated installation programs, are mitigating cycle delays. Across Canada and the northern United States, triple glazing is fast becoming the baseline for multi-family projects seeking lower heating loads.

Europe commands a smaller absolute slice but offers high margin potential because the EPBD mandates zero-emission targets for new builds from 2030. Minimum energy performance standards also force upgrades of the worst 16% of non-residential stock by that same year, ensuring a steady retrofit pipeline. Manufacturers with verifiable environmental product declarations and circular-economy frameworks stand to gain preferential procurement scores. The windows and doors market sees premium demand for noise-attenuating units in dense cities such as Paris and Berlin, while adaptive shading packages become standard in Mediterranean resorts.

Middle East & Africa records the fastest CAGR at 7.10% through 2030, underpinned by large-scale hospitality, healthcare, and education projects. Extreme heat zones require solar-control glazing paired with wide-swing door systems that accommodate mixed indoor-outdoor occupancy patterns. Government mandates for green-building certifications, plus rising energy tariffs, hasten the shift to low-emissivity coatings. Local assembly hubs in the Gulf are beginning to serve East African corridors, reducing lead times and bolstering regional resilience within the windows and doors market.

South America shows a steadier climb, supported by urban densification in Brazil, Colombia, and Chile. High inflation limits short-term discretionary spend, yet long-term infrastructure concessions keep institutional projects moving forward. Revised performance codes in Chile and Peru now prescribe double-glazing for new high-altitude construction, further enlarging the addressable market for energy-conscious fenestration.

- Andersen Corporation

- JELD-WEN Holding Inc.

- Pella Corporation

- YKK AP Inc.

- Marvin Windows & Doors

- Masonite International

- Cornerstone Building Brands / Ply Gem

- MI Windows and Doors

- LIXIL Corporation

- ASSA ABLOY Group

- Rehau Group

- VEKA AG

- Deceuninck NV

- Profine GmbH (Kommerling)

- Saint-Gobain Building Glass & Solutions

- Schuco International

- Aluplast GmbH

- Fenesta Building Systems (DCM Shriram)

- PGT Innovations

- Atrium Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Residential renovation boom and aging housing stock

- 4.2.2 Energy-efficiency regulations (ENERGY STAR V7.0, EU EPBD)

- 4.2.3 Rapid urbanisation and infra spend in APAC

- 4.2.4 Modular construction driving unitised facades

- 4.2.5 Insurance incentives for impact-rated fenestration

- 4.2.6 Building-integrated PV (BIPV) window uptake

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (aluminium, PVC)

- 4.3.2 Skilled-labour shortage for installation

- 4.3.3 ESG scrutiny on vinyl lifecycle emissions

- 4.3.4 Smart-glass shift in high-end commercial builds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Doors

- 5.1.2 Windows

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic / uPVC / Composite

- 5.3 By Application

- 5.3.1 Swinging

- 5.3.2 Sliding

- 5.3.3 Folding

- 5.3.4 Revolving and Others

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Non-Residential (Commercial, Industrial, Institutional)

- 5.5 By Installation Type

- 5.5.1 New Construction

- 5.5.2 Replacement / Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Andersen Corporation

- 6.4.2 JELD-WEN Holding Inc.

- 6.4.3 Pella Corporation

- 6.4.4 YKK AP Inc.

- 6.4.5 Marvin Windows & Doors

- 6.4.6 Masonite International

- 6.4.7 Cornerstone Building Brands / Ply Gem

- 6.4.8 MI Windows and Doors

- 6.4.9 LIXIL Corporation

- 6.4.10 ASSA ABLOY Group

- 6.4.11 Rehau Group

- 6.4.12 VEKA AG

- 6.4.13 Deceuninck NV

- 6.4.14 Profine GmbH (Kommerling)

- 6.4.15 Saint-Gobain Building Glass & Solutions

- 6.4.16 Schuco International

- 6.4.17 Aluplast GmbH

- 6.4.18 Fenesta Building Systems (DCM Shriram)

- 6.4.19 PGT Innovations

- 6.4.20 Atrium Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

門窗市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

門窗市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 美國單戶住宅窗戶和滑動玻璃門市場規模、佔有率和趨勢分析報告:按產品、應用和細分市場預測(2025-2033 年)

美國單戶住宅窗戶和滑動玻璃門市場規模、佔有率和趨勢分析報告:按產品、應用和細分市場預測(2025-2033 年) 2025年門窗維修服務全球市場報告2025年全球鋁門窗市場報告

2025年門窗維修服務全球市場報告2025年全球鋁門窗市場報告 2021-2031年亞太地區門窗自動化市場報告:範圍、細分、動態與競爭分析

2021-2031年亞太地區門窗自動化市場報告:範圍、細分、動態與競爭分析 全球門窗密封條市場全球門窗金屬製品市場

全球門窗密封條市場全球門窗金屬製品市場 塑膠門窗市場-全球產業規模、佔有率、趨勢、機會及預測(細分、按材料類型、按應用、按設計、按玻璃類型、按地區及競爭情況,2020-2030 年預測)

塑膠門窗市場-全球產業規模、佔有率、趨勢、機會及預測(細分、按材料類型、按應用、按設計、按玻璃類型、按地區及競爭情況,2020-2030 年預測) 隔音密封條市場報告:趨勢、預測與競爭分析(至 2031 年)

隔音密封條市場報告:趨勢、預測與競爭分析(至 2031 年) 隔音密封條市場:按材料類型、按產品類型、按應用、按最終用途行業、按分銷管道、按地區

隔音密封條市場:按材料類型、按產品類型、按應用、按最終用途行業、按分銷管道、按地區