|

市場調查報告書

商品編碼

1851855

資料處理和託管服務:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Data Processing And Hosting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

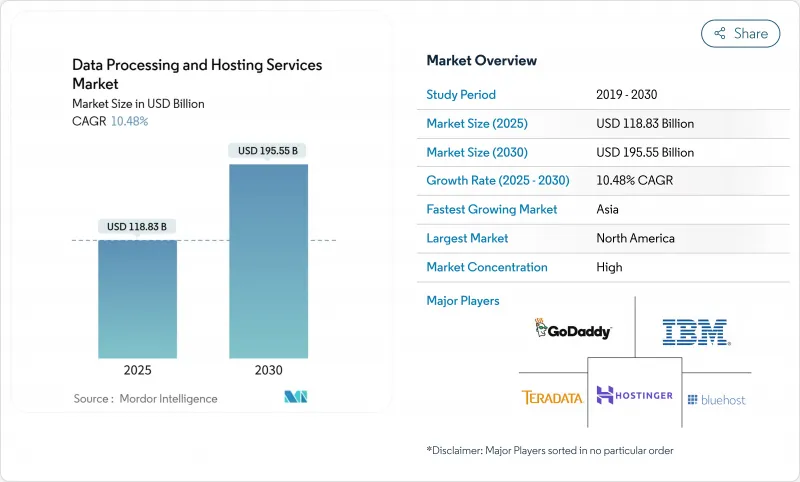

預計到 2025 年,資料處理和託管服務市場規模將達到 1,188.3 億美元,到 2030 年將達到 1,955.5 億美元,在預測期(2025-2030 年)內,複合年成長率將達到 10.48%。

企業大規模轉向託管運算、加速向人工智慧賦能的基礎設施轉型以及持續的超大規模資本支出,是推動雲端服務擴張的主要因素。企業正將預算從本地機架更新轉向高GPU密度的雲端實例、承包託管套件以及能夠縮短資料到洞察週期的區域邊緣節點。同時,歐洲和中東地區正在推行強制自主雲端部署的政策,迫使全球企業將工作負載在地化,並在當地建立新的容量池。此外,三大公有雲平台取消出口費用,降低了切換成本,並為那些在晶片技術、接近性或特定行業合規性方面脫穎而出的專業挑戰者創造了機會。

關鍵技術和監管因素重塑了競爭格局。北美憑藉其深厚的光纖網路、可靠的電力供應和高密度超大規模叢集,目前佔據了39%的收入佔有率。同時,亞洲正以13.4%的複合年成長率快速成長,這主要得益於5G的普及、人工智慧新興企業的活躍以及政府的稅收優惠政策,這些政策推動了新建資料中心的建設。託管服務繼續主導資料處理和託管服務市場,佔據64%的佔有率,但以IaaS、PaaS和SaaS為核心的雲端原生產品正以14.1%的最高複合年成長率成長,因為客戶越來越重視系統的彈性。混合雲和多重雲端策略正以12.5%的複合年成長率快速成長,顯示企業正在將雲端視為一個整體,而非單一架構。

全球數據處理及託管服務市場趨勢及洞察

企業工作負載正擴大遷移到超大規模雲端資料中心

企業正透過將關鍵業務系統遷移到超大規模資料中心來降低資本預算風險,預計到2030年,美國資料中心的電力需求將翻倍,達到35吉瓦。這一趨勢日益受到容量驅動,其核心在於獲取人工智慧加速器和主導保全服務,而這些服務在本地部署的成本仍然高得令人望而卻步。預租協議使得企業能夠在實際交付前數年就鎖定所需容量,尤其是在電力資源緊張的城市,例如阿什本、鳳凰城、都柏林和法蘭克福。

人工智慧/機器學習工作負載的爆炸性成長推動了對高密度GPU託管的需求

到 2025 年,將有超過 4 萬家公司在獨立 GPU 上運行生產級 AI,這將提高運算密度並增加散熱需求。 Lambda 和 CoreWeave 等專用 GPU 雲端平台正經歷三位數的成長,因為它們能夠保證 H100 和 MI300 的資源,用於訓練、微調和推理工作負載。

電網不穩定和能源價格上漲限制了資料中心的擴張。

南亞和非洲的電力供不應求和附加稅阻礙了新建資料中心的建設。預計到2023年,美國資料中心將消耗176太瓦時(TWh)的電力,佔全國電力需求的4.4%,凸顯了不斷成長的運算能力與電網容量之間的緊張關係。營運商正轉向現場太陽能+電池儲能和微電網解決方案,這增加了資本投入並延長了部署週期。

細分市場分析

大型企業將佔2024年收入的71%,它們憑藉雄厚的資金實力,致力於大型主機現代化、容器編配和建構全球災難復原副本。相較之下,中小企業正以11.7%的複合年成長率快速發展,這得益於簡化的遷移工具、市場積分和託管式DevOps服務降低了技術壁壘。在非洲和拉丁美洲市場,超過90%的中小企業已採用數位支付,這表明數位支付的普及程度很高。政府對培訓和雲端服務券的補貼進一步推動了數位支付的普及。雖然預計2030年中小企業市場規模將翻倍,但由於大型企業持續擴張業務,中小企業的總支出佔比將不足30%。

中小企業的雲端服務日趨成熟,正催生一個全新的合作夥伴生態系統。經銷商將銷售點 (POS) 系統、分析工具和本地語言支援捆綁銷售,並將計算成本計入服務費用。先進的可觀測性技術堆疊能夠發現異常情況並自動應用修復腳本,從而緩解了曾經阻礙中小企業發展的技能差距。這些效率的提升推動了訂閱續約率和提升銷售的成長,使中小企業成為更廣泛的資料處理和託管服務市場中持續成長的引擎。

到2024年,由可靠的運算、儲存和網路基礎架構驅動的託管服務將佔該行業收入的64%。雲端託管(IaaS、PaaS、SaaS)細分市場到2030年將以14.1%的複合年成長率成長。客戶越來越傾向於工作負載最佳化層、用於人工智慧的GPU叢集、用於Web層的ARM核心以及用於財務帳簿的z-parity CICS即服務。同時,隨著越來越多的企業尋求雲端原生重構、資料管道重構和FinOps管治,專業服務收入也在成長。邊緣運算和託管服務供應商正在將類似雲端的配置方式融入其入口網站,模糊了核心託管和分散式託管之間的界限。隨著時間的推移,連接資料準備和運算的整合管道將削弱獨立ETL供應商的競爭力,並將資料處理和託管服務市場的安全隔離網閘置於其核心地位。

財務靈活性依然具有吸引力。按秒收費和持續用電量抵扣降低了整體擁有成本。隨著能源成本波動,工作負載會根據即時電力現貨價格在各區域之間重新平衡。結果是,利用率結構性地提高,供應商利潤率增加,租戶成本更可預測。

區域分析

北美地區在2024年貢獻了39%的收入,這主要得益於其廣泛的光纖骨幹網、豐厚的稅收優惠以及高密度的超大規模叢集。光是維吉尼亞的勞登縣就擁有超過3000萬平方英尺的架空地板空間,並因變壓器容量限制而面臨電網互聯禁令。為了應對永續性的審查,服務提供者正透過園區級微電網、全天候可再生能源購電協議(PPA)以及熱能再生利用計畫來應對挑戰。 AWS、微軟和Google已總合2025年在美國新建資料中心累計了超過2,550億美元的資金,鞏固了它們在該地區的容量領先地位。各州層級的隱私立法,例如加州的《消費者隱私法案》(CCPA)和德克薩斯州的《隱私法案》,要求資料副本必須保留在州內,這可能會潛移默化地再形成資料處理和託管服務市場的部署格局。

隨著5G普及、數位銀行和人工智慧Start-Ups生態系統的融合,亞洲將迎來13.4%的年複合成長率,成為全球成長最快的地區。新加坡暫停發放新的資料中心許可證將推動資本投資流向柔佛、巴淡島、曼谷和海德拉巴。日本營運商將利用北海道尚未開發的地熱能源,而中國的超大規模資料中心營運商將在東南亞複製國內的超級應用架構,將運算、支付和物流融合起來。智慧型手機的普及和即時翻譯服務的興起將增加數據流量,並支持持續的需求。

歐洲的主權議程正在引導採購趨勢。歐盟的「數位歐洲」計畫已撥款9億歐元用於雲端市場和安全中心,以提升國內能力。德國和法國將利用核能發電和水力發電結合的方式來建造人工智慧訓練叢集。 Gaia-X已製定了互通性標準,儘管進度比最初預期的要慢。北歐國家正在利用廉價的水力發電,但光纖線路有限,難以覆蓋。東歐國家正透過經濟特區吸引投資者,但地緣政治風險仍是一大障礙。值得注意的是,英國脫歐後,放寬了資料中心設備的增值稅,吸引了跨大西洋投資,並鞏固了倫敦的領先地位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 企業工作負載日益成長到超大規模雲端資料中心(北美和歐洲)的遷移

- 邊緣原生應用程式激增,需要分散式微託管(亞洲/大洋洲)

- 主權雲端指令的出現將促進國內託管服務的發展(歐盟和中東地區)

- 零信任和資料駐留合規性驅動託管處理協議(銀行、金融服務和醫療保健)

- 人工智慧/機器學習工作負載的爆炸性成長推動了對高密度GPU託管的需求(全球範圍)

- 中小企業的數位化優先策略推動主機套餐捆綁式處理(南美和非洲)

- 市場限制

- 不穩定的電網和不斷上漲的能源價格限制了資料中心的擴張(非洲和南亞)

- 雲端使用費用不斷上漲引發了人們對供應商鎖定問題的擔憂(全球)

- 資料主權衝突阻礙跨境託管(歐洲與美國)

- 缺乏認證的雲端技術人才導致遷移計劃延期(北歐和海灣合作理事會國家)

- 價值/供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 技術展望

- 容器原生託管和 Kubernetes 自動化

- 無伺服器資料處理平台

- 矽晶片專用化(DPU/G晶片)

- 投資分析

- 監理展望

第5章 市場規模與成長預測

- 按公司規模

- 主要企業

- 中小企業

- 報價

- 資料處理服務

- 資料輸入服務

- 資料探勘服務

- 資料清洗和格式化

- 資料掃描和索引

- 管理 ETL 和分析

- 託管服務

- 共用(經銷商)主機

- 虛擬專用伺服器 (VPS) 主機

- 專用伺服器託管

- 雲端託管

- IaaS

- PaaS

- SaaS

- 託管式 WordPress 主機

- 應用程式託管

- 託管和裸機

- 資料處理服務

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲和多重雲端

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 零售與電子商務

- 製造業

- 醫療保健和生命科學

- 媒體與娛樂

- 政府/公共部門

- 其他(教育、飯店等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲國家

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(MandA、夥伴關係、資金籌措)

- 市佔率分析

- 公司簡介

- Amazon Web Services Inc.

- Microsoft Corporation(Azure)

- Alphabet Inc.(Google Cloud Platform)

- International Business Machines Corporation

- Alibaba Cloud

- Oracle Corporation

- SAP SE

- Teradata Corporation

- Hewlett Packard Enterprise Development LP

- GoDaddy Operating Company LLC

- Bluehost(Newfold Digital Inc.)

- HostGator.com LLC

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting Inc.

- DreamHost LLC

- GreenGeeks LLC

- DigitalOcean Holdings Inc.

- OVHcloud

- Equinix Inc.

- Hetzner Online GmbH

- Cloudflare Inc.

- Salesforce.com Inc.

- Alteryx Inc.

- Cloudera Inc.

第7章 市場機會與未來展望

The Data Processing And Hosting Services Market size is estimated at USD 118.83 billion in 2025, and is expected to reach USD 195.55 billion by 2030, at a CAGR of 10.48% during the forecast period (2025-2030).

Expansion is propelled by large-scale enterprise migrations to managed compute, an accelerating shift toward AI-ready infrastructure, and unrelenting hyperscale capital expenditure. Enterprises are diverting budgets from refreshed on-prem racks to GPU-dense cloud instances, turnkey colocation suites, and regional edge nodes that compress data-to-insight cycles. Parallel policy shifts in Europe and the Middle East mandate sovereign-cloud deployments, prompting global corporations to localize workloads and create fresh pools of in-country capacity. Meanwhile, the removal of egress fees by the three largest public clouds has lowered switching costs, opening opportunities for specialist challengers that differentiate on stacked silicon, proximity, or sector-specific compliance.

Key technology and regulatory catalysts have reshaped the competitive balance. North America currently commands a 39% revenue share, underpinned by deep fiber networks, reliable power, and dense hyperscale clusters. Asia, in contrast, is expanding the fastest at a 13.4% CAGR as 5G penetration, AI start-up activity, and government tax incentives converge to boost new datacenter builds. Hosting services continue to dominate the data processing and hosting services market with a 64% share, yet cloud-native offerings within that category, especially IaaS, PaaS, and SaaS, post the strongest 14.1% CAGR as customers prioritize elasticity. Hybrid and multi-cloud strategies are surging at 12.5% CAGR, signaling that enterprises now view cloud as a portfolio rather than a monolith.

Global Data Processing And Hosting Services Market Trends and Insights

Growing Migration of Enterprise Workloads to Hyperscale Cloud Data-Centers

Enterprises continue to de-risk capital budgets by shifting mission-critical systems to hyperscale regions, with U.S. datacenter power demand expected to double to 35 GW by 2030. The move is increasingly capability-driven, anchored in access to AI accelerators and managed security services that remain prohibitively expensive on-prem. Pre-lease agreements now secure capacity years ahead of physical handover, particularly in Ashburn, Phoenix, Dublin, and Frankfurt, where power allotments are constrained.

AI/ML Workload Explosion Elevating Demand for High-Density GPU Hosting

By 2025, over 40,000 companies will run production AI on discrete GPUs, raising computational density and cooling requirements. Dedicated GPU clouds such as Lambda and CoreWeave post triple-digit growth as they guarantee H100 and MI300 inventory for training, fine-tuning, and inference workloads.

Power-Grid Instability and Rising Energy Tariffs Limiting Data-Center Expansion

Electricity supply shortfalls and surcharges in South Asia and Africa throttle new builds. Data centers consumed 176 TWh of U.S. power in 2023, or 4.4% of national demand, underscoring the tension between compute growth and grid capacity. Operators pivot to onsite solar-plus-battery and micro-grid solutions, inflating capital requirements and elongating deployment schedules.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Edge-Native Applications Requiring Distributed Micro-Hosting

- Emergence of Sovereign-Cloud Mandates Boosting In-Country Hosting

- Data-Sovereignty Conflicts Hindering Cross-Border Hosting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large enterprises controlled 71% of 2024 revenue, leveraging deep coffers to modernize mainframes, adopt container orchestration, and spin up global DR replicas. In contrast, SMEs are the fastest movers, accelerating at 11.7% CAGR as simplified migration tooling, marketplace credits, and managed DevOps services flatten technical barriers. In African and Latin American markets, more than 90% of SMEs have adopted digital payments, underscoring widespread digital adoption. Governments subsidize training and cloud vouchers, further broadening reach. The absolute data processing and hosting services market size for SMEs is projected to double by 2030, while their slice of overall spending remains under 30% because large-enterprise estates also keep expanding.

SME cloud maturation creates new partner ecosystems. Resellers bundle point-of-sale, analytics, and local-language support, embedding compute costs into service fees. Advanced observability stacks surface anomalies and auto-apply remediation scripts, mitigating the skill gap that once stymied smaller firms. Those efficiencies, in turn, reinforce subscription renewals and incremental upsell, positioning the SME segment as a durable growth flywheel within the broader data processing and hosting services market.

Hosting services delivered 64% of sector revenue in 2024, anchored by reliable compute, storage, and network primitives. The sub-segment of cloud hosting (IaaS, PaaS, SaaS) commands a 14.1% CAGR to 2030, fueled by elastic scaling, bundled APIs, and declining unit pricing as hyperscalers aggregate demand. Customers increasingly favor workload-optimized tiers, GPU clusters for AI, ARM cores for web tier, and z-parity CICS as a service for financial ledgers. Concurrently, professional services revenue grows as firms seek cloud-native redesign, data pipeline refactor, and FinOps governance. Edge and colocation providers embed cloud-like provisioning into portals, blurring the lines between core and distributed hosting. Over time, integrated pipelines that marry data preparation with compute will erode standalone ETL vendors, folding their economics into the data processing and hosting services market gatekeepers.

Financial flexibility remains a draw. Pay-by-the-second billing and sustained-usage credits lower the total cost of ownership. As energy costs fluctuate, workloads re-balance across regions based on real-time power spot prices, a capability accessible only through cloud automation. The result is a structurally higher utilization rate, translating to margin expansion for providers and cost predictability for tenants.

The Data Processing and Hosting Services Market Report is Segmented by Organisation (Large Enterprise and Small and Medium Enterprises [SME]), Offering (Data Processing Services and Hosting Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid and Multi-Cloud), End-User Industry (IT and Telecommunication, BFSI, Retail and E-Commerce, Manufacturing, Healthcare and Life Sciences, and More), and Geography

Geography Analysis

North America claimed 39% of 2024 revenue on the back of vast fiber backbones, generous tax incentives, and dense hyperscale clusters. Loudoun County, Virginia, alone hosts over 30 million square feet of raised floor and is now facing grid-interconnection pauses due to transformer constraints. Providers respond with campus-scale micro-grids, 24X7 renewable PPAs, and reclaimed-heat reuse programs to counter sustainability scrutiny. AWS, Microsoft, and Google collectively earmarked more than USD 255 billion for new U.S. halls in 2025, ensuring the region's capacity lead. Privacy legislation at the state level, such as California CCPA and Texas privacy bills, could demand that data copies remain in-state, subtly reshaping deployment footprints inside the data processing and hosting services market.

Asia records the fastest 13.4% CAGR as 5G proliferation, digital banking, and AI start-up ecosystems converge. Singapore's moratorium on new datacenter permits diverts cap-ex toward Johor, Batam, Bangkok, and Hyderabad, all vying to become the region's latency hubs. Japanese operators exploit underused geothermal in Hokkaido while Chinese hyperscalers replicate domestic super-app stacks to Southeast Asia, blending compute with payments and logistics. Smartphone saturation and real-time translation services multiply data flows, anchoring durable demand.

Europe's sovereignty agenda steers procurement trends. The EU's Digital Europe Programme has allocated EUR 900 million to cloud marketplaces and security centers, catalysing domestic capacity. Germany and France vie for AI training clusters by touting nuclear and hydro power mixes. Gaia-X lays interoperability standards, albeit slower than first envisioned. Nordic states leverage cheap hydroelectricity yet grapple with limited fiber routes; Eastern European states woo investors through special economic zones, though geopolitical risk remains a hurdle. Notably, post-Brexit UK relaxes VAT on datacenter gear, attracting trans-Atlantic investment and reinforcing London's pole position.

- Amazon Web Services Inc.

- Microsoft Corporation (Azure)

- Alphabet Inc. (Google Cloud Platform)

- International Business Machines Corporation

- Alibaba Cloud

- Oracle Corporation

- SAP SE

- Teradata Corporation

- Hewlett Packard Enterprise Development LP

- GoDaddy Operating Company LLC

- Bluehost (Newfold Digital Inc.)

- HostGator.com LLC

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting Inc.

- DreamHost LLC

- GreenGeeks LLC

- DigitalOcean Holdings Inc.

- OVHcloud

- Equinix Inc.

- Hetzner Online GmbH

- Cloudflare Inc.

- Salesforce.com Inc.

- Alteryx Inc.

- Cloudera Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Migration of Enterprise Workloads to Hyperscale Cloud Data-Centers (North America and Europe)

- 4.2.2 Proliferation of Edge-Native Applications Requiring Distributed Micro-Hosting (Asia and Oceania)

- 4.2.3 Emergence of Sovereign Cloud Mandates Boosting In-Country Hosting (EU and Middle-East)

- 4.2.4 Zero-Trust and Data-Residency Compliance Driving Managed Processing Contracts (BFSI and Healthcare)

- 4.2.5 AI/ML Workload Explosion Elevating Demand for High-Density GPU Hosting (Global)

- 4.2.6 SME Digital-First Strategies Fueling Bundled Processing?Hosting Packages (South America and Africa)

- 4.3 Market Restraints

- 4.3.1 Power-Grid Instability and Rising Energy Tariffs Limiting Data-Center Expansion (Africa and South Asia)

- 4.3.2 Escalating Cloud Egress Fees Creating Vendor-Lock Concerns (Global)

- 4.3.3 Data-Sovereignty Conflicts Hindering Cross-Border Hosting (Europe vs US)

- 4.3.4 Shortage of Certified Cloud Talent Delaying Migration Projects (Nordics and GCC)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Technological Outlook

- 4.6.1 Container-Native Hosting and Kubernetes Automation

- 4.6.2 Serverless Data-Processing Platforms

- 4.6.3 Silicon Specialisation (DPUs/G-chips)

- 4.7 Investment Analysis

- 4.8 Regulatory Outlook

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Organisation Size

- 5.1.1 Large Enterprises

- 5.1.2 Small and Medium Enterprises (SME)

- 5.2 By Offering

- 5.2.1 Data Processing Services

- 5.2.1.1 Data Entry Services

- 5.2.1.2 Data Mining Services

- 5.2.1.3 Data Cleansing and Formatting

- 5.2.1.4 Data Scanning and Indexing

- 5.2.1.5 Managed ETL and Analytics

- 5.2.2 Hosting Services

- 5.2.2.1 Shared (Reseller) Hosting

- 5.2.2.2 Virtual Private Server (VPS) Hosting

- 5.2.2.3 Dedicated Server Hosting

- 5.2.2.4 Cloud Hosting

- 5.2.2.4.1 IaaS

- 5.2.2.4.2 PaaS

- 5.2.2.4.3 SaaS

- 5.2.2.5 Managed WordPress Hosting

- 5.2.2.6 Application Hosting

- 5.2.2.7 Colocation and Bare-Metal

- 5.2.1 Data Processing Services

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid and Multi-Cloud

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunication

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Manufacturing

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Media and Entertainment

- 5.4.7 Government and Public Sector

- 5.4.8 Others (Education, Hospitality, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 UAE

- 5.5.4.3 Turkey

- 5.5.4.4 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.5.3 Rest of Africa

- 5.5.6 Asia Pacific

- 5.5.6.1 China

- 5.5.6.2 India

- 5.5.6.3 Japan

- 5.5.6.4 South Korea

- 5.5.6.5 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Partnerships, Funding)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation (Azure)

- 6.4.3 Alphabet Inc. (Google Cloud Platform)

- 6.4.4 International Business Machines Corporation

- 6.4.5 Alibaba Cloud

- 6.4.6 Oracle Corporation

- 6.4.7 SAP SE

- 6.4.8 Teradata Corporation

- 6.4.9 Hewlett Packard Enterprise Development LP

- 6.4.10 GoDaddy Operating Company LLC

- 6.4.11 Bluehost (Newfold Digital Inc.)

- 6.4.12 HostGator.com LLC

- 6.4.13 Hostinger International Ltd.

- 6.4.14 SiteGround Hosting Ltd.

- 6.4.15 A2 Hosting Inc.

- 6.4.16 DreamHost LLC

- 6.4.17 GreenGeeks LLC

- 6.4.18 DigitalOcean Holdings Inc.

- 6.4.19 OVHcloud

- 6.4.20 Equinix Inc.

- 6.4.21 Hetzner Online GmbH

- 6.4.22 Cloudflare Inc.

- 6.4.23 Salesforce.com Inc.

- 6.4.24 Alteryx Inc.

- 6.4.25 Cloudera Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

資料處理和託管服務市場規模、佔有率和成長分析:按核心服務分類、部署架構模型、客戶分類、最終用戶產業和地區分類-2026-2033年產業預測

資料處理和託管服務市場規模、佔有率和成長分析:按核心服務分類、部署架構模型、客戶分類、最終用戶產業和地區分類-2026-2033年產業預測 資料處理與託管服務市場:定價模式、組織規模、部署模式、服務類型和產業分類-2026-2032年全球市場預測

資料處理與託管服務市場:定價模式、組織規模、部署模式、服務類型和產業分類-2026-2032年全球市場預測 全球資料處理和託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料處理和託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 資料處理和託管服務的全球市場:市場規模、佔有率、趨勢分析 - 按產品、公司規模、最終用途、區域前景、預測,2024-2031 年

資料處理和託管服務的全球市場:市場規模、佔有率、趨勢分析 - 按產品、公司規模、最終用途、區域前景、預測,2024-2031 年 資料處理和託管服務市場規模、佔有率和趨勢分析報告:按產品、按企業規模、按最終用途、按地區、細分趨勢:2024-2030

資料處理和託管服務市場規模、佔有率和趨勢分析報告:按產品、按企業規模、按最終用途、按地區、細分趨勢:2024-2030