|

市場調查報告書

商品編碼

1851808

醫藥玻璃包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Pharmaceutical Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

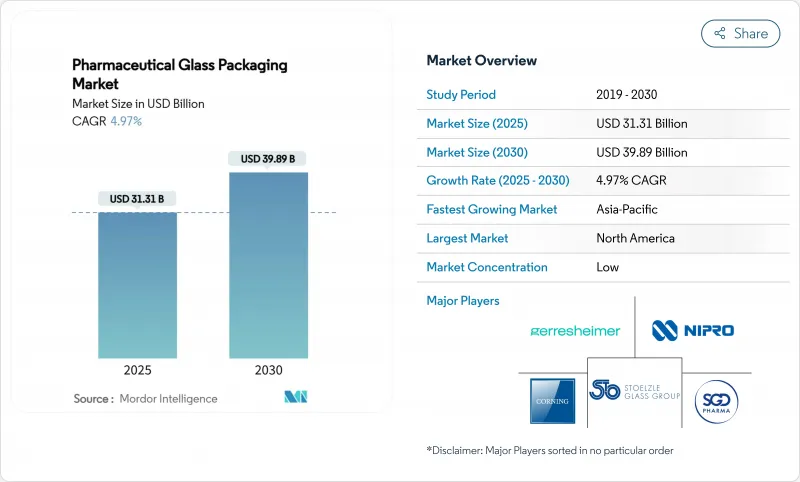

預計到 2025 年,醫藥玻璃包裝市場規模將達到 313.1 億美元,到 2030 年將達到 398.9 億美元,年複合成長率為 4.97%。

這一趨勢反映出市場正穩步轉向高價值容器系統,這些系統既能滿足嚴格的無菌和洗脫標準,又能支持生物製劑的快速規模化生產、分散式疫苗生產以及自行注射的偏好。美國食品藥物管理局 (FDA) 和生技藥品管理局 (EMA) 不斷收緊的指導方針持續推動對 I 型硼矽酸玻璃的需求,而人工智慧檢測技術則可在降低缺陷風險的同時提高生產效率。同時,熔爐現代化和回收率的提高使生產商能夠在不影響監管合規性的前提下實現永續性。因此,儘管原料成本波動和來自先進聚合物日益激烈的競爭有所限制,但醫藥玻璃包裝市場仍蘊藏著穩健的成長機會。

全球醫藥玻璃包裝市場趨勢與洞察

擴大生技藥品和注射產品線

監管數據顯示,2024年FDA核准的55種新藥中,將有17種為生技藥品,凸顯了生技藥品的持續成長動能。因此,製造商正在加速升級其i型包裝能力,以確保蛋白質穩定性並降低分層風險。 Stevanart集團的營收飆升至11.04億歐元,其中38%來自高價值解決方案,凸顯了高階包裝容器如何抓住這一機會。腫瘤和自體免疫療法越來越傾向於使用可進行皮下注射的大容量藥筒,這進一步強化了醫藥玻璃包裝市場在支持以患者為中心的給藥方式方面的關鍵作用。基因療法的持續突破將推動對能夠在整個冷凍供應鏈中保持無菌狀態的包裝容器的更大依賴。這些趨勢共同為生技藥品提供了結構性利好,並將顯著提升2030年後的基準需求。

新冠疫情後擴大疫苗填充及包裝產能

隨著各國政府持續建立戰略疫苗儲備,全球管瓶消費量依然居高不下。 Shots公司已生產超過10億支新冠疫苗管瓶,展現了基準的永續性。歐洲藥品管理局(EMA)為緩解GLP-1促效劑短缺而做出的調整,進一步凸顯了建構韌性供應鏈的重要性。在北美,Bormioli Pharma公司新增的FDA核准的儲存能力提振了需求,推動區域銷售額成長了47%。此外,印度和東南亞的工廠擴建也促進了對當地加工商的銷售量,並鞏固了新興樞紐地區的醫藥玻璃包裝市場。這些投資在支持廣泛疫苗接種目標的同時,也緩解了疫情初期出現的訂單波動。

COP/COC聚合物注射器的快速普及

格雷斯海默公司的ClearJect聚合物注射器採用防碎、無黏合劑的設計,非常適合自行注射治療。肖特製藥公司的TOPPAC Freeze注射器則是針對需要深度冷凍保存的mRNA藥物,凸顯了聚合物的多功能性。由於患者對家用玻璃注射器安全性的擔憂,聚合物在高價值細分市場的應用正在加速普及。雖然玻璃注射器在傳統注射劑領域仍佔據主導地位,但聚合物注射器在黏稠生技藥品和大容量自動注射器領域正逐漸獲得市場佔有率。這種競爭格局的轉變可能會在中期內阻礙市場競爭。

細分市場分析

由於在疫苗、冷凍乾燥生技藥品和臨床批次製劑方面的靈活性,管瓶預計在2024年將維持35.42%的銷售額。穩定的需求使得SGD Pharma能夠在五家工廠每天生產超過800萬支管瓶,確保全球供應的連續性。隨著庫存調整的結束和腫瘤藥物研發管線補充商業庫存,管瓶的醫藥玻璃包裝市場預計將會擴大。預灌封注射器和藥筒預計將以7.53%的複合年成長率快速成長,主要受皮下注射生技藥品和GLP-1受體拮抗劑的推動。 BD最新推出的8毫米針頭適用於高黏度製劑,消除了推廣應用的一大障礙。瓶裝製劑在口服混懸液和兒科電解質溶液領域表現良好,而安瓿則在耐熱麻醉劑領域中保持著一定的市場需求。包括雙腔系統在內的特殊規格包裝以及複雜的聯合治療的需求正在成長。在醫藥玻璃包裝市場,人工智慧偵測持續降低產品報廢率,保護利潤率。

以病人為中心的醫療保健模式促使藥物研發人員優先考慮用藥的便利性、依從性和減少就診次數。注射筆可容納多劑量,而自動注射器則無需專業人員指導即可實現精準給藥。為了保持競爭力,管瓶生產商正轉向模組化填充生產線,提供可在透明瓶和琥珀色瓶之間快速切換的混合批次填充方案,以最大限度地減少停機時間。可減少顆粒生成並促進矽化的塗層技術正在拓展玻璃的性能範圍。因此,如今每個產品類型都在監管合規性、加工性能和整體擁有成本方面競爭,進一步加劇了醫藥玻璃包裝市場的差異化。

2024年,I型硼硼矽酸玻璃的銷售額將佔總銷售額的55.32%,這主要得益於其優異的耐化學性和全球藥典的認可。隨著高濃度生技藥品和抗體藥物複合體對惰性表面的需求日益成長,I型硼矽酸鹽玻璃的市場主導地位將持續維持。此外,I型玻璃容器的醫藥玻璃包裝市場也將受益於新型配方,例如不含硼的Valor玻璃,它幾乎完全消除了分層風險。同時,II型鈉鈣玻璃的複合年成長率將達到6.86%,這主要得益於表面塗層的改進,使其能夠以低成本的方式適用於弱酸性注射劑,從而在性能和預算之間取得理想的平衡。 Gerresheimer公司最新推出的II型玻璃為那些無法承受硼矽酸玻璃高價的中檔治療藥物提供了更多選擇。

III型玻璃因其優異的pH中性性能(而非水解應力),常用於口服液、止咳糖漿和滴瓶的包裝。同時,琥珀色玻璃則用於保護滲透性藥物和眼科抗病毒藥物的延長管線。 SGD Pharma目前在部分產品中採用20%的消費後玻璃屑,且不影響監管合規性。在預測期內,永續性評分將有助於採購決策,而生命週期分析將成為醫藥玻璃包裝市場中所有類型玻璃的綜合價值提案。

區域分析

北美地區將佔2024年銷售額的38.98%,這主要得益於活躍的研發開發平臺、強勁的創業投資資金以及嚴格的合規文化。肖特製藥在北卡羅來納州投資3.71億美元,預計到2030年將使美國即用型注射器(RTU注射器)的國內產量增加兩倍,這將進一步鞏固其在該地區的領先地位。聯邦政府對先進製造業的誘因也將加速爐窯向電混合動力汽車爐的轉型,從而符合二氧化碳減量目標。對GLP-1療法和生物製藥的強勁需求將促使主要製劑生產商運作多班制生產,並為學名藥的銷售波動做好準備。

在嚴格的法規環境和早期永續性指令的支持下,歐洲保持著均衡成長。儘管歐盟新的《包裝和包裝廢棄物條例2025/40》將關鍵的醫藥玻璃排除在回收配額之外,但品牌所有者正自願承諾將碎玻璃納入玻璃屑利用,以實現其公司的淨零排放目標。對後疫情時代戰略藥品儲備的政治支持正在推動區域管瓶和藥筒的生產能力。然而,能源成本仍然是競爭的一大障礙,除非綠色電力價格趨於穩定,否則一些生產商會將產能轉移到成本較低的地區。

亞太地區將以8.12%的複合年成長率成為成長最快的地區,主要得益於中國和印度不斷擴大的產能。預計2023年生物製藥市場規模將達6,506億元人民幣,到2029年將翻倍。政府的獎勵策略將鼓勵高階玻璃的進口,同時,國內企業也加緊改造熔爐。跨國合約研發生產企業(CDMO)正在新加坡和韓國建立灌裝包裝工廠,將區域標準提升至美國和歐盟水平,從而擴大潛在的醫藥玻璃包裝市場。東南亞的疫苗企業正在利用優惠資金建造灌裝包裝生產線,進一步刺激了對管瓶的需求。

儘管南美洲和中東及非洲在絕對數量上落後於其他地區,但隨著當地學名藥生產商擴大生產規模以減少對進口的依賴,這些地區的成長勢頭正在增強。巴西面臨巴西國家衛生監督局(ANVISA)的嚴格監管,這迫使其升級包裝;而海灣國家則將醫療保健投資納入其經濟多元化計畫。值得注意的是,區域內堿灰和液化石油氣能源的輸送緩解了人們對爐灶燃料的擔憂,並使某些新興市場成為醫藥玻璃包裝市場中面向出口的生產中心。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大生技藥品和注射產品線

- 新冠疫情後擴大疫苗填充及包裝產能

- 改用即用型(RTU)管瓶和注射器

- 高附加價值i型硼矽酸玻璃的需求不斷成長

- 醫藥永續性指令提高了玻璃的可回收性

- 人工智慧驅動的線上品質控制降低了玻璃缺陷率(漏報率)

- 市場限制

- COP/COC聚合物注射器的快速普及

- 堿灰和能源價格的波動會推高玻璃成本。

- 超強效藥物的分層與斷裂問題

- 區域容器玻璃熔爐產能短缺(未充分報告)

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品

- 瓶子

- 管瓶

- 安瓿

- 藥筒和預灌封注射器

- 其他產品

- 按玻璃類型

- i型硼矽酸

- II 型處理鈉石灰

- 第三型鈉石灰

- 其他玻璃

- 按劑型

- 注射

- 口服液

- 眼科/鼻科

- 話題

- 最終用戶

- 製藥創新公司

- 學名藥和合約生產商

- 生技公司

- 配藥藥房

- 動物用藥品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲、紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Gerresheimer AG

- Schott AG

- SGD Pharma

- Stevanato Group

- Corning Inc.

- Nipro Corp.

- West Pharmaceutical Services

- Bormioli Pharma

- Owens-Illinois(Ardagh Glass Pharma)

- Stolzle Glass Group

- Beatson Clark

- Shandong Medicinal Glass

- Arab Pharmaceutical Glass

- Piramal Glass

- Sisecam Group

- Baxter BioPharma Solutions

- Kindeva Drug Delivery

- Origin Pharma Packaging

- DWK Life Sciences

- GerroMed(under-reported niche)

第7章 市場機會與未來展望

The pharmaceutical glass packaging market size reached USD 31.31 billion in 2025 and is forecast to climb to USD 39.89 billion by 2030, expanding at a 4.97% CAGR.

This outlook reflects a steady pivot toward high-value container systems that can meet rigorous sterility and leachables limits while supporting rapid biologics scale-up, decentralized vaccine production and growing self-injection preferences. Tightened guidelines from the FDA and the European Medicines Agency continue to elevate demand for Type I borosilicate formats, while AI-enabled inspection unlocks higher throughput with lower defect risk. At the same time, furnace modernization and greater recycled content help producers manage sustainability mandates without compromising regulatory compliance. As a result, the pharmaceutical glass packaging market continues to offer reliable growth opportunities, tempered only by raw-material cost swings and rising competition from advanced polymers.

Global Pharmaceutical Glass Packaging Market Trends and Insights

Expansion of Biologics and Injectable Drugs Pipeline

Regulatory data show 17 biologics approvals among 55 new FDA drugs in 2024, underscoring sustained biologics momentum. Manufacturers therefore accelerate Type I capacity upgrades that ensure protein stability and mitigate delamination risk. A revenue jump to EUR 1,104 million at Stevanato Group, with 38% from high-value solutions, highlights how premium containers capture this wave. Oncology and autoimmune therapies increasingly favor large-volume cartridges that enable subcutaneous dosing, reinforcing the critical role of the pharmaceutical glass packaging market in supporting patient-centric delivery. Continued gene-therapy breakthroughs will deepen reliance on containers that maintain sterility across frozen supply chains. Together these trends give biologics a structural tailwind that raises baseline demand well beyond 2030.

Mounting Vaccine Fill-Finish Capacity Post-COVID

Global vial consumption remains elevated as governments keep strategic vaccine reserves. SCHOTT produced enough vials for more than 1 billion COVID-19 doses, illustrating the sustained baseline. EMA coordination to ease GLP-1 agonist shortages further spotlights the drive for resilient supply chains. North American demand strengthened when Bormioli Pharma lifted regional sales 47% after adding FDA-approved storage capacity. Facility expansions across India and Southeast Asia also push incremental volume to local converters, reinforcing the pharmaceutical glass packaging market across emerging hubs. These investments support broad immunization goals while smoothing order volatility seen during the initial pandemic surge.

Rapid Adoption of COP/COC Polymer Syringes

ClearJect polymer syringes from Gerresheimer deliver break-resistant, glue-free formats that appeal to self-injection therapies. SCHOTT Pharma's TOPPAC Freeze targets mRNA drugs that need deep-cold durability, underscoring polymer versatility. Patient safety concerns for fragile glass in at-home settings accelerate polymer acceptance in high-value niches. While glass maintains dominance for conventional injectables, polymers now capture incremental share in viscous biologics and high-volume autoinjectors. This competitive encroachment creates a modest drag on the pharmaceutical glass packaging market over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Ready-to-Use (RTU) Vials and Syringes

- Rising Demand for High-Value Borosilicate Type I Glass

- Volatile Soda-Ash and Energy Prices Inflating Glass Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vials retained 35.42% revenue in 2024 as their flexibility spans vaccines, lyophilized biologics and clinical batches. Steady demand lets SGD Pharma run more than 8 million vials daily across five plants, safeguarding global supply continuity. The pharmaceutical glass packaging market size for vials is projected to grow as destocking subsides and oncology pipelines refill commercial inventories. Prefillable syringes and cartridges expand fastest at a 7.53% CAGR, propelled by subcutaneous biologics and GLP-1 antagonists that favor ready-to-inject formats. BD's latest eight-millimeter needles address higher viscosity formulations, removing one adoption hurdle. Bottles hold steady in oral suspensions and pediatric electrolytes, whereas ampoules preserve niche demand for heat-stable anesthetics. Specialty formats, including dual-chamber systems, rise alongside complex combination therapies. Across products, AI inspection continues to trim scrap rates, protecting margins within the pharmaceutical glass packaging market.

The shift toward patient-centric care pushes drug developers to prioritize convenience, adherence and reduced clinic visits. Cartridge-based pens accommodate multi-dose regimes, while autoinjectors ensure accurate dose delivery without professional oversight. Vial makers lean on modular filling lines to remain competitive, offering hybrid batches that switch between clear and amber containers with minimal downtime. Coating technologies that reduce particle generation and ease siliconization broaden the performance envelope for glass. Consequently, every product category now competes on a mix of regulatory robustness, machinability and total cost of ownership, heightening differentiation within the pharmaceutical glass packaging market.

Type I borosilicate captured 55.32% revenue in 2024 thanks to sterling chemical resistance and global pharmacopeia acceptance. Its dominance will persist as high-concentration biologics and antibody-drug conjugates demand inert surfaces. The pharmaceutical glass packaging market size for Type I containers benefits further from new compositions like boron-free Valor that virtually eliminate delamination risk. Treated Type II soda-lime glass, however, posts a 6.86% CAGR as surface coatings extend suitability to mildly acidic injectables at lower cost, offering an attractive balance between performance and budget. Gerresheimer's latest Type II lines broaden options for mid-tier therapies that cannot justify premium borosilicate pricing.

Type III glass remains common for oral liquids, cough syrups and dropper bottles where pH neutrality dominates over hydrolytic stress. Meanwhile, colored amber variants shield photolabile drugs and line extensions of ophthalmic antivirals. Recycled content climbs as large pharma institutes Scope 3 emission targets; SGD Pharma now offers 20% post-consumer cullet in selected ranges without compromising regulatory compliance. Over the forecast horizon, sustainability scoring will intensify procurement decisions, making life-cycle analysis an embedded value proposition across all glass types of the pharmaceutical glass packaging market.

The Pharmaceutical Glass Packaging Market Report is Segmented by Product (Bottles, Vials, Ampoules, and More), Glass Type (Type I Borosilicate, Type II Treated Soda-Lime, and More), Drug Formulation (Injectables, Oral Liquids, Ophthalmic/Nasal, Topical), End-User (Pharma Innovator Companies, Generic and CMOs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.98% of 2024 revenue, fueled by intense R&D pipelines, strong venture funding and strict compliance culture. SCHOTT Pharma's USD 371 million investment in North Carolina is slated to triple domestic output of RTU syringes by 2030, further cementing regional leadership. Federal incentives for advanced manufacturing also speed furnace rebuilds into electric hybrids, aligning with carbon-reduction targets. Robust demand for GLP-1 therapeutics and oncology biologics sustains multi-shift operations at major converters, guarding against volume swings in legacy generics.

Europe maintains balanced growth, underpinned by its stringent regulatory environment and early sustainability mandates. The new EU Packaging and Packaging Waste Regulation 2025/40 exempts critical pharma glass from some recycling quotas, yet brand owners voluntarily pledge to integrate cullet to meet corporate net-zero goals. Political support for strategic drug reserves post-COVID fosters local vial and cartridge capacity. However, energy costs remain a competitive thorn, pushing some producers to relocate capacity to lower-cost regions unless green power tariffs stabilize.

Asia-Pacific records the fastest 8.12% CAGR, powered by manufacturing scale-ups in China and India where the 2023 biopharma market stood at 650.6 billion yuan and is forecast to double by 2029. Government stimulus packages encourage high-end glass imports even as domestic players ramp furnace rebuilds. Multinational CDMOs establish fill-finish sites in Singapore and South Korea, raising regional specifications to US and EU levels and enlarging the addressable pharmaceutical glass packaging market. Southeast Asian vaccine institutes leverage concessional funding to build fill-finish lines, further lifting vial demand.

South America and the Middle East & Africa trail in absolute numbers but gain momentum as local generics houses expand facility footprints to cut import reliance. Brazil's stringent ANVISA rules compel packaging upgrades, and Gulf states pursue health-care investment drives as part of economic diversification plans. Importantly, regional arteries for soda ash and LPG energy ease furnace-fuel concerns, positioning select emerging markets as secondary hubs for export-oriented production within the pharmaceutical glass packaging market.

- Gerresheimer AG

- Schott AG

- SGD Pharma

- Stevanato Group

- Corning Inc.

- Nipro Corp.

- West Pharmaceutical Services

- Bormioli Pharma

- Owens-Illinois (Ardagh Glass Pharma)

- Stolzle Glass Group

- Beatson Clark

- Shandong Medicinal Glass

- Arab Pharmaceutical Glass

- Piramal Glass

- Sisecam Group

- Baxter BioPharma Solutions

- Kindeva Drug Delivery

- Origin Pharma Packaging

- DWK Life Sciences

- GerroMed (under-reported niche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of biologics and injectable drugs pipeline

- 4.2.2 Mounting vaccine fill-finish capacity post-COVID

- 4.2.3 Shift to ready-to-use (RTU) vials and syringes

- 4.2.4 Rising demand for high-value borosilicate Type-I glass

- 4.2.5 Pharma sustainability mandates boosting glass recyclability

- 4.2.6 AI-enabled inline QC reducing glass defect rates (under-reported)

- 4.3 Market Restraints

- 4.3.1 Rapid adoption of COP/COC polymer syringes

- 4.3.2 Volatile soda-ash and energy prices inflating glass cost

- 4.3.3 Delamination and breakage concerns in ultra-potent drugs

- 4.3.4 Regional container-glass furnace capacity shortages (under-reported)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Bottles

- 5.1.2 Vials

- 5.1.3 Ampoules

- 5.1.4 Cartridges and Prefillable Syringes

- 5.1.5 Other Product

- 5.2 By Glass Type

- 5.2.1 Type I Borosilicate

- 5.2.2 Type II Treated Soda-Lime

- 5.2.3 Type III Soda-Lime

- 5.2.4 Other Glass Type

- 5.3 By Drug Formulation

- 5.3.1 Injectables

- 5.3.2 Oral Liquids

- 5.3.3 Ophthalmic / Nasal

- 5.3.4 Topical

- 5.4 By End-User

- 5.4.1 Pharma Innovator Companies

- 5.4.2 Generic and CMOs

- 5.4.3 Biotech Firms

- 5.4.4 Compounding Pharmacies

- 5.4.5 Veterinary Pharma

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, and others)

- 6.4.1 Gerresheimer AG

- 6.4.2 Schott AG

- 6.4.3 SGD Pharma

- 6.4.4 Stevanato Group

- 6.4.5 Corning Inc.

- 6.4.6 Nipro Corp.

- 6.4.7 West Pharmaceutical Services

- 6.4.8 Bormioli Pharma

- 6.4.9 Owens-Illinois (Ardagh Glass Pharma)

- 6.4.10 Stolzle Glass Group

- 6.4.11 Beatson Clark

- 6.4.12 Shandong Medicinal Glass

- 6.4.13 Arab Pharmaceutical Glass

- 6.4.14 Piramal Glass

- 6.4.15 Sisecam Group

- 6.4.16 Baxter BioPharma Solutions

- 6.4.17 Kindeva Drug Delivery

- 6.4.18 Origin Pharma Packaging

- 6.4.19 DWK Life Sciences

- 6.4.20 GerroMed (under-reported niche)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球醫藥玻璃市場-市場佔有率及排名、總收入及需求預測(2025-2031年)

全球醫藥玻璃市場-市場佔有率及排名、總收入及需求預測(2025-2031年) 醫藥玻璃包裝市場:按容器類型、玻璃類型、最終用途、封蓋類型和分銷管道分類-2025-2032年全球預測

醫藥玻璃包裝市場:按容器類型、玻璃類型、最終用途、封蓋類型和分銷管道分類-2025-2032年全球預測 2025年全球藥用玻璃包裝市場報告2025年全球低硼矽酸玻璃瓶市場報告2025年全球醫用玻璃疫苗瓶市場報告

2025年全球藥用玻璃包裝市場報告2025年全球低硼矽酸玻璃瓶市場報告2025年全球醫用玻璃疫苗瓶市場報告 全球藥用管瓶市場:市場規模(按數量、分銷類型、瓶蓋尺寸和地區分類)、未來預測

全球藥用管瓶市場:市場規模(按數量、分銷類型、瓶蓋尺寸和地區分類)、未來預測 2032 年藥用管瓶和安瓿瓶市場預測:按產品、材料、產能、應用、最終用戶和地區進行的全球分析

2032 年藥用管瓶和安瓿瓶市場預測:按產品、材料、產能、應用、最終用戶和地區進行的全球分析 藥用玻璃包裝市場報告(依產品(藥瓶、藥水瓶、安瓿瓶、藥筒、注射器等)、藥品類型(學名藥、品牌藥、生物製劑)、應用(口服、注射、鼻腔等)及地區分類)2025-2033

藥用玻璃包裝市場報告(依產品(藥瓶、藥水瓶、安瓿瓶、藥筒、注射器等)、藥品類型(學名藥、品牌藥、生物製劑)、應用(口服、注射、鼻腔等)及地區分類)2025-2033 硼矽酸管瓶市場報告:2031 年趨勢、預測與競爭分析

硼矽酸管瓶市場報告:2031 年趨勢、預測與競爭分析 藥用管瓶和安瓿瓶:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

藥用管瓶和安瓿瓶:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)