|

市場調查報告書

商品編碼

1851802

LTE物聯網:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030年)LTE IoT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

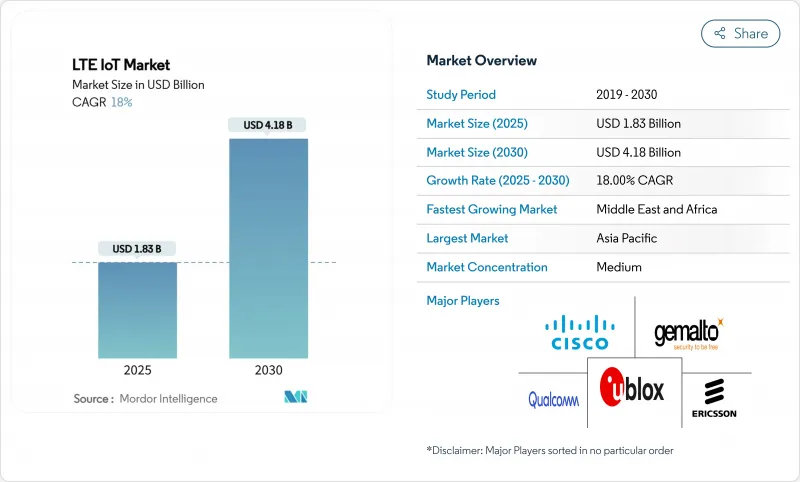

預計到 2025 年,LTE 物聯網市場規模將達到 18.3 億美元,到 2030 年將達到 41.8 億美元,在預測期(2025-2030 年)內,複合年成長率將達到 18%。

這種快速成長反映了2G和3G網路的加速淘汰、低功耗蜂窩模組成本的下降,以及政府強制推行智慧電錶將公用事業公司鎖定在授權頻譜連接上的趨勢。亞太地區目前以55%的收入佔有率領先其他地區的5G市場,這主要得益於中國通訊部署的170萬個5G基地台和5.95億條蜂巢式物聯網電路。中東地區智慧城市建設的同步成長,例如卡達斥資6,000萬美元建設的盧賽爾城項目,推動該地區以19.8%的複合年成長率成為成長最快的地區。企業正在從自有連接轉向託管連接,隨著營運商實現網路切片和自動化配置的商業化,託管服務的複合年成長率將達到15.4%。雖然工業自動化目前的需求最高,但醫療保健領域的成長速度最快,這得益於利用蜂巢式低功耗廣域網路(LPWA)骨幹網路的遠端患者監護計畫。

全球LTE物聯網市場趨勢與洞察

低功耗蜂窩LPWA模組價格跌破4美元

Nordic Semiconductor 的 nRF9151 晶片,憑藉其 64MHz 的 Arm Cortex-M33 處理器和整合的多模數據機,展示瞭如何降低物料清單成本,使產品價格接近 4 美元以下,從而推動農業、物流和環境感測領域的部署,這些領域此前依賴於免許可的 LPWAN 網路。中國供應商已開始以 3 美元的價格提供用於公用事業收費計量表的 NB-IoT 模組,進一步推動了成本下降的趨勢。儘管大多數全球產品目錄中的組件價格仍為 10-15 美元,但歐洲和亞太地區的通訊業者已開始補貼硬體,以加速 LTE 物聯網市場的普及並提高網路利用率。

智慧電錶強制令提升蜂窩網路連接

超過60個地區的燃氣、電力和公共已頒布法規,強制安裝可遠端升級的通訊電錶。 Telia在瑞典部署了200萬個採用NB-IoT和LTE-M技術的電錶,降低了上門服務成本,並建立了5G就緒的配電網。 Netinium的SIM卡設定檔編配和Telit Cinterion實現了遠端配置,打破了以往阻礙公用事業公司使用廣域蜂窩鏈路的廠商鎖定機制。這些項目能夠提供對LTE物聯網市場多年的可視性,並取代專有網狀網路。

Sub-GHz頻段擁塞限制了容量

目前,多種低功耗廣域網路(LPWAN)協定在有限的700-960MHz頻段內競爭。佔空比限制和功率上限制約了小區密度,推高了網路側干擾管理成本。儘管美國聯邦通訊委員會(FCC)在2024年開放了新的6GHz室內頻段分配,但對於地下和農村物聯網而言,Sub-GHz頻段的傳播至關重要。這迫使營運商投資於動態頻譜存取和窄帶濾波技術,從而推高成本並減緩市場動態。

細分市場分析

至2024年,專業服務將透過諮詢、設備認證和邊緣雲端整合計劃,貢獻LTE物聯網市場61%的收入。隨著企業將從SIM卡物流到安全修補程式等生命週期任務轉移給專業服務供應商,託管服務預計將以15.4%的複合年成長率加速成長。德國電信的B2B部門正在將連接和分析與基於結果的合約捆綁在一起,將資本預算轉化為營運支出。隨著時間的推移,人工智慧賦能的編配平台將減少人工工程工時。

標準化的存取API和eUICC配置已經縮短了試點階段,但棕地工業仍需要客製化的無線電方案和通訊協定轉換。因此,雖然新建計劃大多傾向於採用託管式服務包,但對於需要多年時間的維修而言,專家參與仍然至關重要。

LTE IoT 市場按服務類型(專業、主機)、產品類型(NB-IoT、LTE-M)、最終用戶產業(IT 和通訊、消費性電子、零售(數位電子商務)、醫療保健、工業、其他行業)和地區進行細分。

區域分析

中國通訊累計, 2024年前三季通訊收入將達到7,235億元人民幣(約1,012億美元),凸顯了其對頻譜和資本投資的持續投入。日本和韓國正優先推動智慧工廠維修,而東南亞國協正在試辦利用共用的LTE骨幹網基礎設施建設交通管理和洪水預警系統。

中東是成長最快的次區域,預計到2030年將以19.8%的複合年成長率成長。卡達的盧賽爾城計畫將利用NB-IoT和LTE-M感測器進行照明、廢棄物和交通運輸,並將45萬居民整合到即時營運中心。沙烏地阿拉伯的「2030願景」計畫將石油盈餘轉化為農業物聯網,將溫室氣候控制和無人機灌溉與蜂巢式低功耗廣域網路(LPWA)技術相結合,以應對糧食安全風險。

在歐洲和北美,受更嚴格的碳計量和3G網路關閉的推動,傳統儀錶和工業設備的更新換代正穩步推進。 O2 Telefónica的德國分公司報告稱,2025年第一季其M2M用戶增132.4%,其中大部分來自公共。非洲和拉丁美洲仍在發展中,但LTE物聯網在資產追蹤和農業領域的直接應用正在推動固網。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 主流

- 低功耗蜂窩廣域網路(LPWA)標準(NB-IoT、LTE-M)的模組成本低於4美元。

- 目前,超過60個國家強制要求使用公用事業收費電錶。

- 2G/3G時代終將結束,設備將被迫升級到下一代網路。

- 低調行事

- 3GPP Rel-17 RedCap 將 LTE-M 的功耗降低了一半

- 基於網路切片的QoS層級結構提升物聯網平均ARPU值

- 主流

- 市場限制

- 主流

- Sub-GHz頻段壅塞

- 模組價格溢價與 LoRaWAN/BLE 替代方案相比

- 低調行事

- NB-IoT漫遊故障導致韌體分叉

- 碳排放報告推動企業轉向超低能耗低功耗廣域網

- 主流

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過服務

- 專業的

- 管理

- 依產品類型

- NB-IoT(Cat-NB1)

- LTE-M(eMTC Cat-M1)

- 按最終用戶行業分類

- 資訊科技和電信

- 消費性電子產品

- 零售(數位商務)

- 衛生保健

- 工業的

- 其他行業

- 按地區

- 北美洲

- 南美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Qualcomm Technologies

- Gemalto(Thales DIS)

- u-blox AG

- Ericsson

- Cisco(Jasper)

- Cradlepoint

- Sequans Communications

- PureSoftware

- TELUS

- MediaTek

- Verizon

- ATandT

- Vodafone

- China Mobile

- Deutsche Telekom

- Quectel

- Fibocom

- Telit Cinterion

- Semtech

- Sierra Wireless

第7章 市場機會與未來展望

The LTE IoT Market size is estimated at USD 1.83 billion in 2025, and is expected to reach USD 4.18 billion by 2030, at a CAGR of 18% during the forecast period (2025-2030).

This rapid growth reflects accelerating 2G and 3G network sunsets, falling low-power cellular module costs, and government smart-meter mandates that lock utilities into licensed-spectrum connectivity. Asia-Pacific (APAC) leads current adoption with 55% revenue share, propelled by China Mobile's deployment of 1.7 million 5G base stations and 595 million cellular IoT lines. Parallel smart-city spending in the Middle East, exemplified by Qatar's USD 60 million Lusail City contract, positions the region as the fastest climber at 19.8% CAGR. Enterprises are shifting from outright ownership toward managed connectivity, lifting the managed-services CAGR to 15.4% as operators monetize network slicing and automated provisioning. Demand is strongest in industrial automation today, yet healthcare registers the sharpest upswing thanks to remote patient-monitoring programs riding cellular LPWA backbones.

Global LTE IoT Market Trends and Insights

Low-power cellular LPWA modules fall below USD 4

Nordic Semiconductor's nRF9151 shows how a 64 MHz Arm Cortex-M33 and integrated multimode modem can cut bill-of-materials and approach a sub-USD 4 headline price, encouraging agriculture, logistics, and environmental-sensing deployments that once relied on unlicensed LPWAN. Chinese vendors already quote USD 3 NB-IoT modules for utility meters, reinforcing cost-down momentum . While most global catalogs still list USD 10-15 parts, operators in Europe and APAC have begun subsidizing hardware to accelerate LTE IoT market uptake and lift network utilization.

Smart-meter mandates reinforce cellular connectivity

Over 60 jurisdictions have enacted regulations that oblige gas, electricity, or water utilities to install communicating meters able to upgrade remotely. Telia's rollout of 2 million Swedish electric meters on NB-IoT and LTE-M cut truck-roll costs and established a 5G-ready distribution grid. Netinium's SIM-profile orchestration with Telit Cinterion allows remote provisioning, solving the historic lock-in that deterred utilities from wide-area cellular links. These programs create multiyear visibility for the LTE IoT market while displacing proprietary mesh networks.

Sub-GHz spectrum congestion limits capacity

Multiple LPWAN formats now compete inside finite 700-960 MHz slices. Duty-cycle rules and power caps curb cell density, and network-side interference management costs rise sharply. The FCC opened new 6 GHz indoor allocations in 2024, yet sub-GHz propagation remains critical for underground or rural IoT reach. Operators,, therefore,, invest in dynamic-spectrum access and narrowband filtering, adding expense and slowing LTE IoT market rollouts imegacitiess.

Other drivers and restraints analyzed in the detailed report include:

- Legacy network sunsets stimulate immediate migration

- RedCap improves LTE-M energy profile

- Carbon-footprint rules favor ultra-low-energy designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Professional services generated 61% of LTE IoT market revenue in 2024 through consulting, device certification, and edge-cloud integration projects. Managed-service uptake is forecast to accelerate at 15.4% CAGR as enterprises transfer lifecycle tasks, from SIM logistics to security patching, to specialist providers. Deutsche Telekom's business-to-business arm bundles connectivity with analytics in outcome-based contracts that shift capital budgets into operating fees. Over time, AI-enabled orchestration platforms will trim manual engineering hours, yet the transition itself fuels recurring revenue for managed-service vendors.

Standardized \onboarding APIs and eUICC provisioning already shorten pilot phases, but brownfield industrial estates still need bespoke radio-planning and protocol translation. As a result, professional engagements remain pivotal for multiyear retrofits even while new-build projects lean more heavily on managed packages. The LTE IoT market size for managed services is projected to reach USD X million by 2030, outgrowing professional income streams beyond 2028, though both categories together reinforce operator stickiness.

LTE IoT Market Market is Segmented by Service (Professional, Managed), Product Type (NB-IoT, LTE-M), End-User Industry (IT and Telecommunication, Consumer Electronics, Retail (Digital Ecommerce), Healthcare, Industrial and Other Industries), and Geography.

Geography Analysis

APAC contributed 55% of global revenue in 2024 as China scaled NB-IoT coverage to 100,000 connections per sector and subsidized module production below USD 3. China Mobile booked CNY 723.5 billion (USD 101.2 billion) telecom income in the first three quarters of 2024, underscoring sustained spectrum and capex commitments. Japan and Korea emphasize smart-factory retrofits, while ASEAN nations pilot traffic management and flood-alert systems riding shared LTE backbone infrastructure.

The Middle East is the fastest-expanding sub-region, projected at 19.8% CAGR to 2030. Qatar's Lusail City program integrates 450,000 residents into a real-time operations center using NB-IoT and LTE-M sensors for lighting, waste, and transport. Saudi Vision 2030 channels petro surplus into agricultural IoT that combats food-security risks, with cellular LPWA linking greenhouse climate controls and drone irrigation.

Europe and North America display steady renewal of legacy meters and industrial gear, aided by stricter carbon accounting and 3G shutdowns. Telia's conversion of Swedish meters shows the blueprint: swap proprietary PLC for licensed LTE radios, enable eUICC, and guarantee 15-year contracts. o2 Telefonica's German footprint reported 132.4% year-over-year M2M subscriber growth in Q1 2025, mostly utility driven . Africa and Latin America remain nascent but are leapfrogging fixed lines with direct LTE IoT adoption in asset-tracking and agriculture.

- Qualcomm Technologies

- Gemalto (Thales DIS)

- u-blox AG

- Ericsson

- Cisco (Jasper)

- Cradlepoint

- Sequans Communications

- PureSoftware

- TELUS

- MediaTek

- Verizon

- ATandT

- Vodafone

- China Mobile

- Deutsche Telekom

- Quectel

- Fibocom

- Telit Cinterion

- Semtech

- Sierra Wireless

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 MAINSTREAM

- 4.2.1.1 Low-power cellular LPWA standards (NB-IoT, LTE-M) reach sub-USD 4 module cost

- 4.2.1.2 Smart utility-meter mandates in more than 60 countries

- 4.2.1.3 2G/3G sunsets forcing device migration to LTE IoT

- 4.2.2 UNDER-THE-RADAR

- 4.2.2.1 3GPP Rel-17 RedCap halves LTE-M power draw

- 4.2.2.2 Network-slicing-based QoS tiers lift average IoT ARPU

- 4.2.1 MAINSTREAM

- 4.3 Market Restraints

- 4.3.1 MAINSTREAM

- 4.3.1.1 Sub-GHz spectrum congestion

- 4.3.1.2 Module price premium vs LoRaWAN/BLE alternatives

- 4.3.2 UNDER-THE-RADAR

- 4.3.2.1 Patchy NB-IoT roaming causing firmware forks

- 4.3.2.2 Carbon-emission reporting pushes firms toward ultra-low-energy LPWAN

- 4.3.1 MAINSTREAM

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysi

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service

- 5.1.1 Professional

- 5.1.2 Managed

- 5.2 By Product Type

- 5.2.1 NB-IoT (Cat-NB1)

- 5.2.2 LTE-M (eMTC Cat-M1)

- 5.3 By End-user Industry

- 5.3.1 IT and Telecom

- 5.3.2 Consumer Electronics

- 5.3.3 Retail (Digital Commerce)

- 5.3.4 Healthcare

- 5.3.5 Industrial

- 5.3.6 Other Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 South America

- 5.4.3 Europe

- 5.4.4 Asia-Pacific

- 5.4.5 Middle East

- 5.4.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Qualcomm Technologies

- 6.4.2 Gemalto (Thales DIS)

- 6.4.3 u-blox AG

- 6.4.4 Ericsson

- 6.4.5 Cisco (Jasper)

- 6.4.6 Cradlepoint

- 6.4.7 Sequans Communications

- 6.4.8 PureSoftware

- 6.4.9 TELUS

- 6.4.10 MediaTek

- 6.4.11 Verizon

- 6.4.12 ATandT

- 6.4.13 Vodafone

- 6.4.14 China Mobile

- 6.4.15 Deutsche Telekom

- 6.4.16 Quectel

- 6.4.17 Fibocom

- 6.4.18 Telit Cinterion

- 6.4.19 Semtech

- 6.4.20 Sierra Wireless

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment