|

市場調查報告書

商品編碼

1851799

無伺服器運算:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Serverless Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

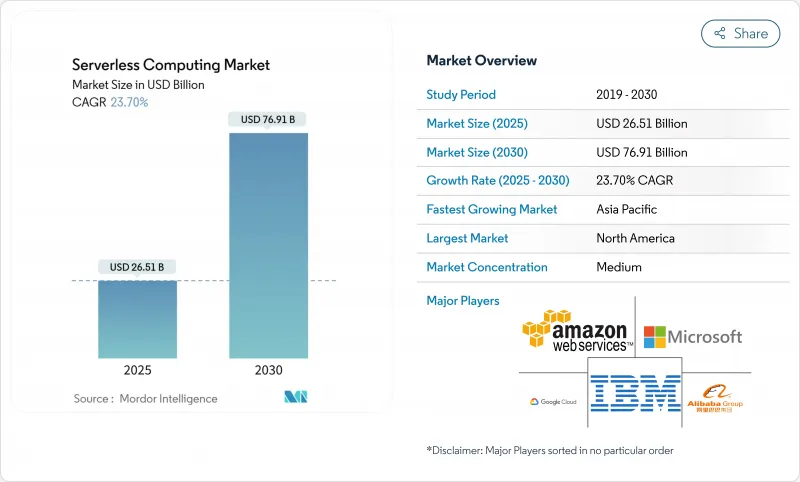

無伺服器運算市場預計將從 2025 年的 265.1 億美元成長到 2030 年的 769.1 億美元,複合年成長率為 23.7%。

隨著開發團隊希望無需管理基礎架構即可編寫程式碼,超大規模雲端如今已具備強大的可觀測性、安全性和整合能力,因此對無伺服器架構的需求日益成長。事件驅動型微服務、邊緣原生 5G配置以及需要亞秒級響應時間且規模龐大的即時 AI 工作負載進一步推動了這一趨勢。隨著企業目標從降低成本轉向創新,他們正在利用無伺服器架構來加速推出新的數位化產品、實現 DevSecOps 自動化並支援資料主權架構。雖然公共雲端仍然是主流部署模式,但隨著企業在權衡最佳功能和供應商風險之間尋求平衡,多重雲端策略正在興起。

全球無伺服器運算市場趨勢與洞察

北美銀行、金融服務和保險(BFSI)現代化加速向事件驅動型微服務轉型

銀行和保險公司正在用細粒度服務取代單體架構,這些服務能夠近乎即時地回應刷卡、貸款報價和詐騙訊號。一家北美大型金融機構透過使用無伺服器函數,將開發週期縮短了 35% 至 40%,並將基礎設施成本降低了 28.3%。這種以執行次數收費的模式非常適合支付和財富管理平台常見的非規律性交易量。 API 優先的設計也簡化了監管審核,因為每個函數都可以單獨記錄、加密和版本控制。隨著零信任規則日益嚴格,銀行、金融服務和保險 (BFSI) 團隊傾向於使用臨時計算,這種計算方式既能減少攻擊面,又能滿足嚴格的審核追蹤要求。

歐洲零售和電子商務對支援DevSecOps的多重雲端管道的需求激增

歐洲零售商正競相支援即時結帳和個人化優惠,同時遵守 GDPR 法規。 89% 的零售商將無伺服器工作負載分佈在至少兩個雲端平台上,以避免被供應商鎖定並保持區域資料駐留。內建策略引擎會在每次提交程式碼時進行掃描,將安全性測試整合到 CI/CD 流程中,並自動加密金鑰以縮短漏洞視窗。分散式安全策略使團隊能夠縮短修復時間,並在諸如雙十一和黑色星期五等銷售高峰期更快地推送新功能。

高度分佈式微函數中的調試和可觀測性差距

傳統的應用效能管理 (APM) 代理程式無法追蹤毫秒級的瞬態函數,導致根本原因分析存在盲點。企業反映,排查無伺服器應用的故障所需時間是單體應用的 2.4 倍,因為日誌分散在各個服務中,冷啟動也會掩蓋延遲異常。目前,新興解決方案會注入輕量級的 span ID 並將其匯出到開放標準的後端,但其成熟度落後於主流工具。在追蹤、指標和日誌實現無縫整合之前,規避風險的部門可能會對遷移關鍵業務系統猶豫不決。

細分市場分析

到2024年,隨著企業優先考慮承包營運,託管服務將佔總收入的62%;而隨著企業開展複雜的現代化項目,專業服務到2030年將以18.4%的複合年成長率成長。許多受監管的企業正在聘請諮詢合作夥伴,以重新設計事件模式、重構單體架構並在運作前檢驗合規性。諮詢團隊將無伺服器安全模式、策略即代碼和財務營運儀表板整合起來,以最大限度地提高業務價值。

專業服務也透過培訓產品團隊掌握非同步設計和可觀測性的最佳實踐,來支持這種文化轉變。隨著無伺服器架構的應用範圍擴展到分析、人工智慧和邊緣運算領域,持續的管治和平台工程服務也與開發支援一起納入捆綁式服務。這種演變既能為整合商保持獲利成長,又能縮短企業實現價值的時間。

到 2024 年,函數即服務 (FaaS) 將佔總支出的 58%,並將持續支撐無伺服器運算市場至 2030 年。然而,後端即服務 (BaaS) 是一個成長迅速的細分市場,年複合成長率 (CAGR) 高達 25%,這主要得益於團隊尋求更高級的架構,將身份驗證、儲存和即時同步等功能整合到 API 呼叫中。行動開發者尤其青睞登入和推播通知的單行整合,這可以將推出週期從數週縮短至數小時。

BaaS 透過卸載例行任務來補充 FaaS,使函數能夠專注於差異化邏輯。統一的 API 閘道可在兩種範式之間統一路由流量,而無伺服器容器則可彌補需要更長時間運行的程序的效能差距。架構師可以根據成本、延遲和合規性需求,靈活地組合不同的抽象層。

區域分析

到2024年,北美將佔據無伺服器架構收入的38%,這主要得益於北美豐富的雲端運算人才、積極的數位銀行發展藍圖,以及美國聯邦政府推行的零信任政策,該政策鼓勵使用臨時運算來減少攻擊面。企業正在利用無伺服器架構來升級傳統架構、採用事件流實現客戶個人化,並運行符合合規要求的日誌記錄管道。加拿大也呈現類似的趨勢,尤其是在通訊業者整合5G邊緣運算能力方面。同時,墨西哥的金融科技新興企業正在採用無伺服器架構來安全地擴展支付API。

亞太地區是成長最快的區域,預計到2030年將以19.8%的複合年成長率成長。中國網際網路巨頭正在投資原生無伺服器人工智慧服務;印度蓬勃發展的SaaS產業正在採用計量收費模式來應對難以預測的全球需求;日本和韓國的製造商正在整合邊緣運算能力以進行預測性維護;東協的金融科技和電子商務企業正在部署多重雲端無伺服器架構,以低延遲的方式觸達區域客戶。 5G MEC、價格合理的雲端空間以及開發人員技能的提升,正在加速全部區域的採用。

為了滿足 GDPR 和國家主權法規的要求,企業紛紛採用多重雲端,歐洲仍保持強勁的勢頭。英國、德國和法國在零售、銀行和公共部門試點計畫中處於領先地位,這些試點計畫共用一套通用的加密、審核和駐留藍圖。北歐國家則在綠色資料中心整合和事件驅動型能源網路方面不斷突破創新。供應商也積極回應,推出在地化區域和可攜式運行時環境,在日益嚴格的合規環境下,依然推動了業務成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美銀行、金融服務和保險(BFSI)現代化加速向事件驅動型微服務轉型

- 歐洲零售和電子商務對支援DevSecOps的多重雲端的需求激增

- 邊緣原生 5G MEC 部署推動亞洲通訊業者採用無伺服器技術

- 即時人工智慧/機器學習推理工作負載推動醫療保健領域函數即服務 (FaaS) 的採用

- 美國聯邦政府的零信任指令活性化在IT領域應用無伺服器安全工具鏈。

- 拉丁美洲金融科技生態系中API貨幣化平台的快速擴張

- 市場限制

- 高度分佈式微函數中的調試和可觀測性差距

- 專有事件編配引擎會加劇供應商鎖定風險。

- 多區域無伺服器資料儲存中的資料駐留合規性障礙

- 高頻交易和遊戲工作負載中的冷啟動延遲限制

- 價值鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

- 技術概覽

- API 閘道器

- 函數即服務 (FaaS)

- 後端即服務 (BaaS)

- 資料庫即服務 (DBaaS)

第5章 市場規模與成長預測

- 按服務模式

- 專業服務

- 託管服務

- 按服務類型

- 函數即服務 (FaaS)

- 後端即服務 (BaaS)

- API 閘道器

- 容器即服務 (CaaS)

- 按部署模式

- 公有雲

- 私有雲端

- 混合雲

- 多重雲端

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 零售與電子商務

- 政府/公共部門

- 醫療保健和生命科學

- 工業和製造業

- 媒體與娛樂

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 北歐國家

- 瑞典

- 挪威

- 丹麥

- 芬蘭

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Alibaba Group Holding Ltd.

- IBM Corp.

- Oracle Corp.

- SAP SE

- VMware Inc.

- Red Hat Inc.

- Cloudflare Inc.

- Fastly Inc.

- Tencent Cloud

- Huawei Cloud

- Netlify Inc.

- Vercel Inc.

- DigitalOcean Inc.

- Iron.io

- TriggerMesh Inc.

- Serverless Inc.

- Stackery Inc.

第7章 市場機會與未來展望

The serverless computing market is valued at USD 26.51 billion in 2025 and is forecast to touch USD 76.91 billion by 2030, advancing at a 23.7% CAGR.

Demand is rising because development teams want to write code without managing infrastructure, and hyperscale clouds now bundle robust observability, security and integration capabilities. Momentum is reinforced by event-driven microservices, edge-native 5G deployments, and real-time AI workloads that scale irregularly yet require sub-second response. Enterprises are moving from cost savings to innovation goals, using serverless to speed new digital products, automate DevSecOps and support data-sovereign architectures. Public cloud remains the dominant deployment model, but multi-cloud strategies are gaining ground as enterprises look to balance best-of-breed features with vendor risk.

Global Serverless Computing Market Trends and Insights

Accelerating Shift to Event-Driven Microservices in North American BFSI Modernization

Banks and insurers are replacing monoliths with granular services that react to card swipes, loan quotes and fraud signals in near real time. Using serverless functions, leading North American institutions trimmed development cycles by 35-40% and shaved 28.3% off infrastructure spend, freeing budget for new digital features. The model's pay-per-execute billing fits irregular transaction volumes common in payments and wealth platforms. API-first designs also simplify regulatory audits because each function can log, encrypt and version individually. As zero-trust rules tighten, BFSI teams prefer ephemeral compute that reduces attack surface while meeting stringent audit trails.

Surging Demand for DevSecOps-Ready Multi-Cloud Pipelines Across European Retail and E-commerce

European retailers race to match instant checkout and personalized offers while obeying GDPR. Eighty-nine percent now distribute serverless workloads across at least two clouds to avoid lock-in and maintain regional data residency. Built-in policy engines scan code on every commit, integrate security tests into CI/CD and auto-encrypt secrets, shrinking vulnerability windows. By shifting security left, teams cut remediation time and push features faster during seasonal peaks such as Singles' Day and Black Friday.

Debugging and Observability Gaps in Highly Distributed Micro-Functions

Traditional APM agents cannot trace ephemeral functions that live for milliseconds, leaving blind spots during root-cause analysis. Enterprises report troubleshooting serverless apps takes 2.4 times longer than monoliths because logs scatter across services and cold-starts mask latency outliers. Emerging solutions now inject lightweight span IDs and export them to open-standard back ends, yet maturity lags mainstream tooling. Until traces, metrics and logs consolidate seamlessly, risk-averse sectors will hesitate to migrate mission-critical systems.

Other drivers and restraints analyzed in the detailed report include:

- Roll-out of Edge-Native 5G MEC Driving Serverless Adoption Among Asia Telecom Operators

- Real-Time AI/ML Inference Workloads Propelling Function-as-a-Service Uptake in Healthcare

- Vendor Lock-In Risk Amplified by Proprietary Event Orchestration Engines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Services held 62% of 2024 revenue as organizations prioritized turnkey operations, but Professional Services is expanding at an 18.4% CAGR to 2030 as firms tackle complex modernization programs. Many regulated enterprises hire consulting partners to redesign event schemas, refactor monoliths and validate compliance before going live. Advisory teams integrate serverless security patterns, policy-as-code and FinOps dashboards to maximize business value.

Professional Services also support culture change, training product squads on asynchronous design and observability best practices. As serverless footprints widen to analytics, AI and edge, continuous governance and platform engineering join development assistance in bundled engagements. This evolution sustains high-margin growth for integrators while improving enterprise time-to-value.

Function-as-a-Service captured 58% of spending in 2024 and will keep anchoring the serverless computing market through 2030. Yet Backend-as-a-Service is the star growth segment at 25% CAGR as teams seek higher-level constructs that collapse authentication, storage and real-time sync into API calls. Mobile developers in particular appreciate one-line integration for login and push notifications, cutting launch cycles from weeks to hours.

BaaS complements FaaS by offloading boilerplate tasks, letting functions focus on differentiated logic. Unified API gateways route traffic uniformly across both paradigms, while serverless containers fill performance gaps that demand longer-lived processes. The spectrum of abstractions allows architects to mix and match for cost, latency and compliance needs.

The Serverless Computing Market Report is Segmented by Service Model (Professional Services and Managed Services), Service Type (Function-As-A-Service (FaaS), Backend-As-A-Service (BaaS), and More), Deployment Model (Public Cloud, Private Cloud, and More), End-User Industry (IT and Telecommunications, BFSI, and More), and Geography

Geography Analysis

North America drove 38% of 2024 serverless revenue, supported by abundant cloud talent, aggressive digital banking roadmaps, and U.S. federal zero-trust directives that favor ephemeral compute for reduced attack surface. Enterprises leverage serverless to modernize legacy stacks, employ event streams for customer personalization, and run compliance-ready logging pipelines. Canada mirrors these patterns, especially among telcos integrating 5G edge functions, while Mexico's fintech startups adopt serverless to scale payment APIs securely.

Asia Pacific is the fastest-growing region, projected at 19.8% CAGR to 2030. China's internet majors invest in native serverless AI services, and India's booming SaaS sector embraces the pay-as-you-go model to manage unpredictable global demand. Japanese and South Korean manufacturers integrate edge functions for predictive maintenance, whereas ASEAN fintech and e-commerce players deploy multi-cloud serverless stacks to reach regional customers with low latency. The confluence of 5G MEC, affordable cloud spots and developer upskilling accelerates uptake across the region.

Europe maintains a strong position as organizations adopt multi-cloud to satisfy GDPR and state sovereignty rules. The United Kingdom, Germany and France lead with retail, banking and public-sector pilots that share common blueprints for encryption, audit and residency. Nordic countries push boundaries with green data-center integrations and event-driven energy grids. Vendors respond with localized zones and portable runtimes, reinforcing growth despite stricter compliance landscapes.

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Alibaba Group Holding Ltd.

- IBM Corp.

- Oracle Corp.

- SAP SE

- VMware Inc.

- Red Hat Inc.

- Cloudflare Inc.

- Fastly Inc.

- Tencent Cloud

- Huawei Cloud

- Netlify Inc.

- Vercel Inc.

- DigitalOcean Inc.

- Iron.io

- TriggerMesh Inc.

- Serverless Inc.

- Stackery Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating shift to event-driven microservices in North American BFSI modernisation

- 4.2.2 Surging demand for DevSecOps-ready multi-cloud pipelines across European retail and e-commerce

- 4.2.3 Roll-out of edge-native 5G MEC driving serverless adoption among Asia telecom operators

- 4.2.4 Real-time AI/ML inference workloads propelling Function-as-a-Service uptake in healthcare

- 4.2.5 Government Zero-Trust mandates boosting serverless security toolchains in US federal IT

- 4.2.6 Rapid expansion of API monetisation platforms in LATAM fintech ecosystems

- 4.3 Market Restraints

- 4.3.1 Debugging and observability gaps in highly distributed micro-functions

- 4.3.2 Vendor lock-in risk amplified by proprietary event orchestration engines

- 4.3.3 Data residency compliance hurdles for multi-region serverless data stores

- 4.3.4 Cold-start latency constraints in high-frequency trading and gaming workloads

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Technology Snapshot

- 4.9.1 API Gateway

- 4.9.2 Function-as-a-Service (FaaS)

- 4.9.3 Backend-as-a-Service (BaaS)

- 4.9.4 Database-as-a-Service (DBaaS)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Model

- 5.1.1 Professional Services

- 5.1.2 Managed Services

- 5.2 By Service Type

- 5.2.1 Function-as-a-Service (FaaS)

- 5.2.2 Backend-as-a-Service (BaaS)

- 5.2.3 API Gateway

- 5.2.4 Container-as-a-Service (CaaS)

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid Cloud

- 5.3.4 Multi-Cloud

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Government and Public Sector

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Industrial and Manufacturing

- 5.4.7 Media and Entertainment

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Nordics

- 5.5.4.1 Sweden

- 5.5.4.2 Norway

- 5.5.4.3 Denmark

- 5.5.4.4 Finland

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.7 Asia Pacific

- 5.5.7.1 China

- 5.5.7.2 India

- 5.5.7.3 Japan

- 5.5.7.4 South Korea

- 5.5.7.5 ASEAN

- 5.5.7.6 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corp.

- 6.4.3 Google LLC

- 6.4.4 Alibaba Group Holding Ltd.

- 6.4.5 IBM Corp.

- 6.4.6 Oracle Corp.

- 6.4.7 SAP SE

- 6.4.8 VMware Inc.

- 6.4.9 Red Hat Inc.

- 6.4.10 Cloudflare Inc.

- 6.4.11 Fastly Inc.

- 6.4.12 Tencent Cloud

- 6.4.13 Huawei Cloud

- 6.4.14 Netlify Inc.

- 6.4.15 Vercel Inc.

- 6.4.16 DigitalOcean Inc.

- 6.4.17 Iron.io

- 6.4.18 TriggerMesh Inc.

- 6.4.19 Serverless Inc.

- 6.4.20 Stackery Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球無伺服器PostgreSQL市場報告2026年全球無伺服器運算平台市場報告

2026年全球無伺服器PostgreSQL市場報告2026年全球無伺服器運算平台市場報告 全球無伺服器運算市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無伺服器運算市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球GPU加速AI伺服器市場(按伺服器類型、散熱技術、部署方式、應用領域和最終用戶產業分類)預測(2026-2032年)無伺服器運算市場:按元件、部署模型、組織規模和最終用戶產業分類,全球預測,2026-2032 年無伺服器運算市場 - 2026-2031 年預測

全球GPU加速AI伺服器市場(按伺服器類型、散熱技術、部署方式、應用領域和最終用戶產業分類)預測(2026-2032年)無伺服器運算市場:按元件、部署模型、組織規模和最終用戶產業分類,全球預測,2026-2032 年無伺服器運算市場 - 2026-2031 年預測 無伺服器運算市場按服務模式、部署類型、最終用戶和地區分類

無伺服器運算市場按服務模式、部署類型、最終用戶和地區分類 無伺服器運算市場預測至 2032 年:按服務類型、部署模式、企業規模、最終用戶和地區分類的全球分析

無伺服器運算市場預測至 2032 年:按服務類型、部署模式、企業規模、最終用戶和地區分類的全球分析 無伺服器運算市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032)

無伺服器運算市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032) 全球無伺服器運算市場

全球無伺服器運算市場