|

市場調查報告書

商品編碼

1851766

六氟化硫:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)Sulfur Hexafluoride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

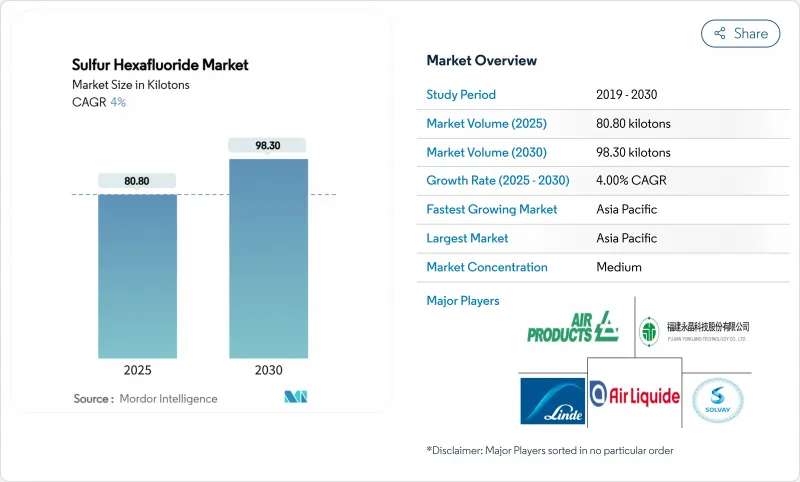

預計到 2025 年,六氟化硫市場規模將達到 80.80 千噸,到 2030 年將達到 98.30 千噸,預測期(2025-2030 年)複合年成長率為 4%。

新興國家積極的電網發展計畫、半導體製造能力的快速擴張以及離岸風電輸電計劃,在日益嚴格的環境法規下,支撐著市場需求。由於SF6具有無與倫比的介電強度、緊湊的尺寸和快速通電等優點,電力公司繼續指定將其用於氣體絕緣開關設備,而現有替代品則缺乏類似的優勢。半導體製造商需要超高純度的SF6來進行快速、潔淨的等離子蝕刻,隨著特徵尺寸的縮小,這項需求只會更加迫切。同時,醫療和鎂壓鑄應用正在推動市場進一步成長,創造了多元化的終端市場,有助於緩解監管衝擊。

全球六氟化硫市場趨勢及洞察

新興國家的併網需求

隨著輸電業者安裝緊湊型氣體絕緣變電站以適應創紀錄的電網擴張,中國的六氟化硫(SF6)排放將從2011年的2.6吉克(Gg)增加到2021年的5.1吉克(Gg)。印度已累計200億盧比用於電網現代化改造,並指定使用SF6開關設備,以確保在快速都市化中保持電壓穩定。典型的變電站使用壽命為25至50年,因此每一次安裝決策都鎖定了未來對六氟化硫的市場需求。氣體絕緣變電站的通電速度比空氣絕緣變電站快45%,為急於緩解電網擁塞的電力公司節省了時間。因此,儘管環境政策的爭論日益激烈,但亞太地區的六氟化硫市場仍在持續成長。

半導體和液晶顯示器等離子體蝕刻技術的發展

韓國價值4,710億美元的半導體產業叢集計畫到2047年新增16家工廠,顯示資本流動將推動超高純度六氟化硫(SF6)的消耗。在深溝槽矽蝕刻中,SF6產生的氟自由基去除材料的速度比其他氣體快100倍,從而確保3奈米及以下節點的產能目標。雖然減排系統可以減少直接排放,但仍有部分原料進入大氣,因此隨著產能的擴張,監管力道必須加強。儘管如此,在可直接替代的氣體能夠達到其蝕刻精度之前,製程工程師仍將繼續指定使用SF6,這使得六氟化硫市場牢牢地嵌入到先進製造價值鏈中。

嚴格的全球暖化法規

歐盟將從2026年起禁止在中壓開關設備中使用六氟化硫(SF6),並從2032年起禁止在高壓開關設備中使用SF6,這將迫使電力公司加快維修計畫。加州強制要求在2033年前全面淘汰SF6,並將年洩漏率限制在1%。紐約州和麻州的類似政策將縮短依賴SF6設備的投資壽命,並減少已開發地區的採購量。這些重疊的政策將使六氟化硫市場的成長前景下降1.8個百分點。

細分市場分析

預計到2024年,電子/技術級六氟化硫市場佔有率將達到61.18%,因為電力公司優先考慮開關設備、斷路器和氣體絕緣線路中經過驗證的絕緣性能。技術級六氟化硫的價格波動與商品價格密切相關,並受益於成熟的全球通路,這些管道能夠透過油罐車向變電站批量運輸。隨著維修計劃在預測期內持續進行,此細分市場將維持較大的基本負載需求,以支撐整個六氟化硫市場。

超高純度六氟化硫(SF6)雖然絕對噸位較小,但預計將以4.90%的複合年成長率成為所有產品類型中成長最快的,這主要得益於先進半導體和液晶顯示器(LCD)製造行業的推動。將污染物閾值控制在十億分之一以下需要多道純化工序、專用鋼瓶和專屬供應鏈。精通這些生產通訊協定的供應商能夠獲得更高的利潤,抵消產量下降的影響,並在環保政策降低傳統公用事業需求的情況下提供策略性對沖。將這兩種等級的產品結合起來,有助於六氟化硫市場維持大宗商品和特殊產品之間的平衡組合。

六氟化硫市場報告按產品類型(電子及技術級、超高純度級)、應用領域(電力能源、電子、金屬製造、醫療及其他應用)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2024年,亞太地區將佔六氟化硫(SF6)市場47.65%的佔有率,到2030年將以4.75%的複合年成長率成長。中國電網營運商正在超高壓走廊安裝緊湊型550kV氣體絕緣變電站,以適應創紀錄的可再生能源裝置容量,這一戰略鞏固了數十年來對SF6的需求。印度的跨邦輸電強化計畫採用SF6環路開關來提高快速都市化負載中心的可靠性。在韓國,半導體產業的擴張正在推動區域超高純度SF6的需求,而日本則將自身定位為無SF6解決方案的技術示範者,從而形成了成熟技術和新興技術並存的雙軌格局。

在北美,公用事業公司在更換老舊設備與遵守監管規定之間尋求平衡,因此其消費量成長為個位數中段。在加州,2033 年的逐步淘汰計畫和洩漏量上限迫使電力公司提前部署監測和捕集系統,而其他州的電網營運商仍在高壓等級中使用六氟化硫(SF6),因為現場可用的替代技術十分稀缺。聯邦基礎設施資金的投入提高了電網的韌性,並穩定了整體需求,而不斷提高的回收率也限制了對新供應的需求。加拿大與加州的總量管制與交易計畫開展合作,促進了跨境政策協調,使加拿大公用事業公司能夠在保留大量舊設備備用庫存的同時,探索無六氟化硫試點計畫。

歐洲面臨最嚴峻的政策環境。氟化氣體法規的修訂將禁止從2026年起安裝新的中壓SF6開關設備設備,並自2032年起禁止安裝新的高壓開關設備。輸電系統營運商,主要集中在德國和斯堪的納維亞半島,正在試驗真空斷路器和清潔空氣技術,但在棕地擴建項目中仍依賴SF6。英國的維修計畫預計將增加1億至2.8億英鎊的合規成本,以應對歐盟的限制。南歐和東歐的公用事業公司由於設備更換週期較慢,面臨成本壓力,這可能導致SF6的有限採購持續到本世紀中期以後。拉丁美洲以及中東和非洲地區雖然規模較小,但成長強勁,正在擴大其幹線電氣化和工業產能,為六氟化硫市場帶來了未來的成長空間。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新興國家的併網需求

- 半導體和液晶電漿蝕刻的發展

- 可再生能源併網高壓直流輸電及海上變電站

- 防止鎂合金壓鑄件氧化

- 醫療領域需求不斷成長

- 市場限制

- 嚴格的全球暖化法規

- 價格波動和出口配額

- 半導體製程可能被禁止

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 電子/技術級

- 超高純度

- 透過使用

- 電力和能源

- 電子學

- 金屬製造

- 醫療保健

- 其他用途(例如窗戶隔熱材料等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Advanced Specialty Gases

- Air Liquide

- Air Products and Chemicals, Inc.

- AIR WATER INC

- Airgas, Inc.

- Concorde Specialty Gases, Inc.,

- Fujian Yongjing Technology Co., Ltd

- Guangdong Huate Gas Co., Ltd.

- Honeywell International Inc.

- Kanto Denka Kogyo Co., Ltd.

- Linde plc

- Matheson Tri-Gas, Inc.

- Messer SE & Co. KGaA

- Resonac Holdings Corporation

- Solvay SA

第7章 市場機會與未來展望

The Sulfur Hexafluoride Market size is estimated at 80.80 kilotons in 2025, and is expected to reach 98.30 kilotons by 2030, at a CAGR of 4% during the forecast period (2025-2030).

Robust grid-upgrade programs in emerging economies, surging semiconductor fabrication capacity, and offshore wind transmission projects are sustaining demand even as environmental regulations tighten. Electrical utilities continue to specify SF6 for gas-insulated switchgear because it delivers unrivalled dielectric strength, compact footprints, and rapid energization, advantages that existing alternatives still struggle to match. Semiconductor manufacturers require ultra-high-purity SF6 to achieve fast, clean plasma etching, and this requirement deepens as feature sizes shrink. Meanwhile, medical and magnesium die-casting uses provide incremental growth, creating diversified end-markets that help buffer regulatory shocks.

Global Sulfur Hexafluoride Market Trends and Insights

Grid-upgrade demand in emerging economies

China's SF6 emissions climbed from 2.6 Gg in 2011 to 5.1 Gg in 2021 as transmission developers installed compact gas-insulated substations to keep pace with record-setting grid expansions. India has earmarked INR 2,000 crore for network modernization that specifies SF6 switchgear to secure voltage stability during rapid urbanization. Because typical substation assets remain in service for 25 to 50 years, every installation decision effectively locks in future sulfur hexafluoride market demand. Gas-insulated stations can be energized 45% faster than air-insulated yards, a time saving valued by utilities racing to alleviate congestion. As a result, the sulfur hexafluoride market continues to deepen its presence across Asia-Pacific despite intensifying environmental policy debates.

Semiconductor and LCD plasma-etching growth

Korea's USD 471 billion semiconductor cluster, slated to add 16 fabs by 2047, exemplifies capital flows that elevate consumption of ultra-high-purity SF6. In deep-trench silicon etching, SF6 generates fluorine radicals that remove material up to 100 times faster than rival gases, ensuring throughput targets for 3 nm and below nodes. Although abatement systems curb direct emissions, a portion of feedstock still reaches the atmosphere, prompting regulatory scrutiny as fabrication capacity scales. Even so, process engineers continue to specify SF6 until drop-in alternatives can replicate its etching precision, keeping the sulfur hexafluoride market firmly embedded in advanced manufacturing value chains.

Stringent global-warming regulations

The European Union has banned SF6 in medium-voltage switchgear from 2026 and in high-voltage gear from 2032, forcing utilities to accelerate retrofit plans. California mandates complete phase-out by 2033 and restricts annual leak rates to 1%, compelling asset owners to fund costly monitoring systems. Similar trajectories in New York and Massachusetts compress investment horizons for SF6-dependent assets, dampening procurement volumes in developed regions. These overlapping policies subtract 1.8 percentage points from the sulfur hexafluoride market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-integrated HVDC and offshore substations

- Magnesium die-casting oxidation prevention

- Price volatility and export quotas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The electronic/technical-grade segment accounted for 61.18% of sulfur hexafluoride market share in 2024 as utilities prioritize proven insulation performance for switchgear, breakers, and gas-insulated lines. Technical-grade SF6 follows commodity price dynamics and benefits from established global distribution channels that permit bulk tanker deliveries to substation sites. Because retrofit projects continue through the forecast period, the segment maintains a sizable base-load volume that anchors the overall sulfur hexafluoride market.

Ultra-high-purity SF6, while representing a smaller absolute tonnage, is forecast to expand at 4.90% CAGR, the fastest among product types, propelled by advanced semiconductor and LCD fabrication. Maintaining contaminant thresholds below parts-per-billion requires multiple purification stages, specialised cylinders, and dedicated supply chains. Suppliers that master these production protocols secure higher margins, offsetting lower volumes and providing a strategic hedge as environmental policy squeezes traditional utility demand. Collectively, the two grade tiers ensure that the sulfur hexafluoride market retains a balanced portfolio across commodity and specialty niches.

The Sulfur Hexafluoride Market Report is Segmented by Product Type (Electronic/Technical Grade, Ultra-High Purity Grade), Application (Power and Energy, Electronics, Metal Manufacturing, Medical, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific dominated the sulfur hexafluoride market with 47.65% share in 2024 and is projected to log a 4.75% CAGR through 2030. China's grid operators are installing compact 550 kV gas-insulated substations across ultrahigh-voltage corridors to accommodate record renewable capacity, a strategy that cements multi-decade SF6 demand. India's program to reinforce inter-state transmission uses SF6 ring-main units to improve reliability in rapidly urbanizing load centers. South Korea's semiconductor expansion amplifies regional ultra-high-purity volumes, while Japan positions itself as a technology demonstrator for SF6-free solutions, creating a dual-track landscape that blends incumbent and emerging technologies.

North America shows mid-single-digit consumption growth as utilities balance ageing-asset replacements with regulatory compliance. California's 2033 phase-out and leak caps compel early adoption of monitoring and capture systems, but grid operators in other states continue to specify SF6 in high-voltage classes where field-ready alternatives remain scarce. Federal infrastructure funding for resilience upgrades keeps overall demand stable, although rising recycling rates help temper fresh supply needs. Canada's linkages to California's cap-and-trade system drive cross-border policy alignment, nudging Canadian utilities to explore SF6-free pilots while maintaining critical spares for legacy equipment.

Europe faces the most stringent policy environment: the revised F-gas regulation bans new medium-voltage SF6 switchgear from 2026 and high-voltage installations from 2032. Transmission system operators, led by entities in Germany and the Nordics, are piloting vacuum-interrupter and clean-air technologies but still rely on SF6 for brownfield extensions. The United Kingdom mirrors EU limits, adding compliance costs estimated at GBP 100-280 million for retrofit programs. Southern and Eastern European utilities with slower replacement cycles face cost pressures, potentially extending limited SF6 procurement beyond mid-decade. Latin America, the Middle East, and Africa collectively remain smaller yet high-growth territories as they expand base-line electrification and industrial capacity, offering future upside for the sulfur hexafluoride market.

- Advanced Specialty Gases

- Air Liquide

- Air Products and Chemicals, Inc.

- AIR WATER INC

- Airgas, Inc.

- Concorde Specialty Gases, Inc.,

- Fujian Yongjing Technology Co., Ltd

- Guangdong Huate Gas Co., Ltd.

- Honeywell International Inc.

- Kanto Denka Kogyo Co., Ltd.

- Linde plc

- Matheson Tri-Gas, Inc.

- Messer SE & Co. KGaA

- Resonac Holdings Corporation

- Solvay S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-Upgrade Demand in Emerging Economies

- 4.2.2 Semiconductor and LCD Plasma-Etching Growth

- 4.2.3 Renewable-Integrated HVDC and Offshore Substations

- 4.2.4 Magnesium Die-Casting Oxidation Prevention

- 4.2.5 Increasing Demand in the Medical Sector

- 4.3 Market Restraints

- 4.3.1 Stringent Global-Warming Regulations

- 4.3.2 Price Volatility and Export Quotas

- 4.3.3 Potential Semiconductor-Process Bans

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Electronic / Technical Grade

- 5.1.2 Ultra-High Purity Grade

- 5.2 By Application

- 5.2.1 Power and Energy

- 5.2.2 Electronics

- 5.2.3 Metal Manufacturing

- 5.2.4 Medical

- 5.2.5 Other Applications (Window Insulation, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Advanced Specialty Gases

- 6.4.2 Air Liquide

- 6.4.3 Air Products and Chemicals, Inc.

- 6.4.4 AIR WATER INC

- 6.4.5 Airgas, Inc.

- 6.4.6 Concorde Specialty Gases, Inc.,

- 6.4.7 Fujian Yongjing Technology Co., Ltd

- 6.4.8 Guangdong Huate Gas Co., Ltd.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Kanto Denka Kogyo Co., Ltd.

- 6.4.11 Linde plc

- 6.4.12 Matheson Tri-Gas, Inc.

- 6.4.13 Messer SE & Co. KGaA

- 6.4.14 Resonac Holdings Corporation

- 6.4.15 Solvay S.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

六氟化硫市場:2026-2032年全球市場預測(依等級、包裝、應用、終端用戶產業及通路分類)六氟化硫 (SF6) 氣體回收設備市場:按設備類型、技術、流量、壓力範圍、應用、終端用戶產業和銷售管道,全球預測,2026-2032 年六氟化硫混合氣體回收設備市場(按產品類型、氣體流量、技術、最終用途和銷售管道),全球預測(2026-2032年)

六氟化硫市場:2026-2032年全球市場預測(依等級、包裝、應用、終端用戶產業及通路分類)六氟化硫 (SF6) 氣體回收設備市場:按設備類型、技術、流量、壓力範圍、應用、終端用戶產業和銷售管道,全球預測,2026-2032 年六氟化硫混合氣體回收設備市場(按產品類型、氣體流量、技術、最終用途和銷售管道),全球預測(2026-2032年) 六氟化硫市場規模、佔有率、成長分析(按等級、應用和地區)- 產業預測,2025 年至 2032 年

六氟化硫市場規模、佔有率、成長分析(按等級、應用和地區)- 產業預測,2025 年至 2032 年 全球六氟化硫市場規模:依產品、應用、地區及預測

全球六氟化硫市場規模:依產品、應用、地區及預測 六氟化硫(SF6)的全球市場2024-2028

六氟化硫(SF6)的全球市場2024-2028