|

市場調查報告書

商品編碼

1851728

LED驅動器:市場佔有率分析、產業趨勢及促進因素、成長預測(2025-2030年)LED Driver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

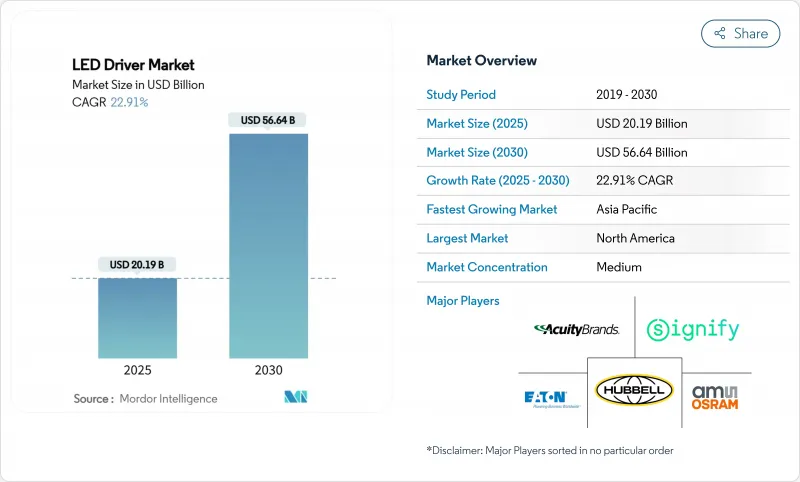

預計到 2025 年,LED 驅動器市場規模將達到 201.9 億美元,到 2030 年將成長至 566.4 億美元,複合年成長率為 22.91%。

這項擴張得益於各國能源效率標準的統一、無線控制技術的加速普及,以及碳化矽和氮化鎵半導體的應用——這些半導體能夠提高轉換效率並縮小驅動器尺寸。尤其是在亞太地區,政府資助的維修項目與淨零排放承諾相輔相成,推動了大規模的更換需求;同時,北美和歐洲的新建築標準正在推動智慧照明的整合規範。車輛電氣化擴大了小型化、耐高溫驅動器的應用範圍,而Matter/Thread標準化則消除了長期存在的互通性障礙。總而言之,這些轉變正在將LED驅動器市場從組件供應商提升為互聯建築平台和能源管理服務的策略推動者。

全球LED驅動器市場趨勢及促進因素

補貼型LED改裝計畫有助於加速市場發展

印度的UJALA舉措表明,大規模推廣高效節能燈具每年可減少20吉瓦的電力需求,並避免8,000萬噸二氧化碳排放。與以往的折扣計劃不同,該計劃的市場促進因素維持了供應商的淨利率,並鼓勵產品持續升級,重點關注具備能量監控功能的高級驅動器。中國、馬來西亞和歐盟的類似計畫正在從燈泡更換轉向整套燈具更換,從而推動了對支援無線控制、功率因數達到0.9或更高、並符合IEC防閃爍標準的驅動器的需求。隨著第一批LED燈具於2015年左右投入使用,第二輪58億台的更換週期將在2025年至2028年間達到高峰。這些計劃將確保在整個預測期內擁有可預測的、大批量的採購管道,從而為LED驅動器市場注入新的動力。

氮化鎵矽基驅動積體電路價格的快速下降使其得以大規模應用。

德克薩斯(TI) 從 6 吋到 8 吋 GaN 晶圓的過渡降低了晶粒成本,同時提高了產量比率,將功率轉換效率提升至 92% 以上,並縮小了散熱預算。英飛凌的 300 毫米試驗線預計 2025 年與矽晶片價格持平,從而開拓零售軌道照明和家電照明等主流通路。 GaN 更高的開關頻率可將磁鐵尺寸縮小高達 40%,從而實現更薄的燈具和更低的機殼溫度,這對於板載晶片 ) 模組至關重要。汽車頭燈系統受益於 GaN 對高結溫的耐受性,支援電動車的自我調整光束架構。這些經濟優勢促進了良性循環的整合:隨著產量增加,成本進一步下降,從而進一步擴大 LED 驅動器市場。

矽供應限制導致驅動晶片生產出現瓶頸

Wolfspeed的流動性壓力威脅到其用於高功率照明和電動車應用的碳化矽晶圓供應。代工廠優先生產先進的3nm邏輯晶片,導致用於LED驅動器的16-90nm混合訊號製程產能短缺。典型MOSFET的前置作業時間超過40週,而專用PMIC的交貨週期則長達一年,迫使廠商重新設計並採用多供應商策略。這些限制導致價格波動,擠壓了中端OEM廠商的利潤空間,並削弱了戶外照明計劃等競標上限明確的領域的近期出貨前景。在東南亞產能擴張啟動之前,矽短缺問題可能會持續阻礙LED驅動器市場的發展。

細分市場分析

2024年,恆定電流裝置佔據了LED驅動器市場61.2%的比重。然而,轉換效率高達92%且無需更改設計即可適應可變電壓LED負載的恒定功率驅動器,預計在2025年至2030年間將以23.1%的複合年成長率成長。在汽車頭燈這一細分市場,英飛凌的Litix Power Flex系列代表了性能的飛躍:SPI控制的調光和多串保護功能使其能夠在不增加散熱負擔的情況下擴展功能。

自我調整照明場景的興起強化了這一轉變。建築建築幕牆、體育場館和可調白光辦公燈具等,如果能夠動態調節輸出,同時將電流保持在二極體的容差範圍內,則可從中受益。這種多功能性減少了產品型號的繁多,並增強了燈具製造商的現場升級途徑。隨著無線通訊協定的日益普及,韌體可選的輸出曲線使得恒定功率設計成為不斷發展的LED驅動器市場中的首選平台。

以DALI和0-10V為主導的有線系統將在2024年佔據LED驅動器市場規模的65.4%。然而,無線技術的普及速度更快,預計到2030年將以24.3%的複合年成長率成長。羅格朗獲得Matter認證的牆盒調光器表明,消費者對基於應用程式的性能驗證充滿熱情。

從總成本角度來看,取消控制線可節省商業維修預算的15%至25%的人力成本,而且在許多情況下,LED加控制系統的投資報酬率更高。 Thread的IPv6基礎架構便於建築管理系統整合,而BLE網狀網路則為緊急照明檢查提供低功耗備用方案。隨著空中韌體更新的普及,無線韌體透過相容未來功能來延長使用壽命。這些優勢已使無線技術穩固地成為LED驅動器市場的支柱。

區域分析

北美地區在2024年銷售額中佔據32.3%的佔有率,這主要得益於更嚴格的燈具能源效率標準,將標準提高到83-195流明/瓦,引導設計者選擇高效驅動器。企業改造項目,例如可口可樂公司對其六家工廠的維修,每年可節省97,063美元,凸顯了快速的投資回報。 CHIPS法案撥款2000億美元用於國內工廠,以提高類比和電源組件的可靠性。加拿大和墨西哥利用一體化的供應鏈共用技術標準和認證實驗室,促進跨境運輸。

亞太地區將呈現最快的結構性成長,預計到2030年複合年成長率將達到24.2%。中國製造業的深度將降低零件成本,而政府的智慧城市津貼將刺激當地對配備NB-IoT和LoRa閘道器的駕駛者的需求。印度創紀錄的UJALA計畫將補充二手燈具庫存,並啟動第二波燈具升級週期。日本、韓國和台灣將把電動車頭燈的創新轉化為可出口的自我調整光束驅動器。東協市場將吸收供應鏈多元化,而越南將成為北美品牌的精加工和組裝中心。

歐洲將透過「生態設計2019/2020」計畫保持發展勢頭,該計畫的目標是到2030年實現每年96太瓦時(TWh)的節能。德國復興信貸銀行(KfW Bank)的撥款將優惠利率與智慧照明的部署掛鉤,以加快物流倉庫驅動器的更新換代。東歐的維修計畫得到了凝聚基金的支持,英國的建築法規L部分也提及了動態照明指南,該指南鼓勵使用支持開放通訊協定通訊的驅動器。中東和非洲地區,尤其是沙烏地阿拉伯,其「2030願景」計畫預測LED採用率將以10%的複合年成長率成長,這為全球LED驅動器市場提供了補充,並得到了當地組裝企業的支持。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 補貼型LED維修計畫(2025年及以後)

- 氮化鎵矽基驅動積體電路價格快速下降

- 新建築標準中強制要求智慧照明

- Matter/Thread無線控制的主流應用

- 電動車頭燈LED驅動器的需求激增

- 企業淨零排放目標加速產業升級

- 市場限制

- 驅動積體電路矽供應持續受限

- 傳統有線通訊協定的互通性有限。

- 非隔離式驅動器設計的複雜性

- 對中國製造的恆流模組徵收高額進口關稅

- 供應鏈分析

- 技術展望

- 監管環境

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場的宏觀經濟因素

第5章 市場規模與成長預測

- 依產品類型

- 恆定電流LED驅動器

- 恆壓LED驅動器

- 恒定功率LED驅動器

- 透過控制功能

- 用電線

- 0-10 V

- DALI

- DMX

- PLC

- Trailing-Edge

- 無線的

- Wi-Fi

- Bluetooth/BLE

- Zigbee

- Thread /Matter

- Li-Fi

- 用電線

- 透過輸出

- 小於25瓦

- 25-65 W

- 65-150 W

- 150瓦或以上

- 按外形規格

- 外部獨立

- 整合/入職

- 線性驅動器

- 緊湊/模組驅動程式

- 按最終用途

- 住房

- 商業和辦公

- 零售和酒店

- 戶外和街道照明

- 產業

- 醫療保健和教育

- 汽車照明系統

- 園藝和農業

- 消費性電子產品背光

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 卡達

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify

- ams OSRAM

- Acuity Brands Lighting

- Hubbell Incorporated

- Eaton(Cooper Lighting)

- Lutron Electronics

- Cree LED(SGH)

- MEAN WELL Enterprises

- Inventronics

- Tridonic(Zumtobel)

- Delta Electronics

- Shenzhen Done Power

- ERP Power

- Lifud Technology

- Helvar

- Murata Manufacturing

- Texas Instruments

- ON Semi

- Allegro MicroSystems

- ROHM Semiconductor

- Macroblock Inc.

- TCI Srl

- MOSO Power

- Current(GE)

第7章 市場機會與未來展望

第8章 投資分析

The LED driver market is valued at USD 20.19 billion in 2025 and is forecast to grow to USD 56.64 billion by 2030, reflecting a CAGR of 22.91%.

This expansion is underpinned by the alignment of national energy-efficiency mandates, accelerating wireless-control adoption and the deployment of silicon-carbide and gallium-nitride semiconductors that raise conversion efficiency and shrink driver footprints. Government-funded retrofit programs, particularly in Asia-Pacific, intersect with net-zero commitments to lift large-scale replacement demand, while new-build codes in North America and Europe push integrated intelligent-lighting specifications. Automotive electrification further widens the addressable base for compact, high-temperature drivers, and Matter/Thread standardization dismantles long-standing interoperability barriers. Collectively, these shifts elevate the LED driver market from a component-supply business to a strategic enabler of connected-building platforms and energy-management services.

Global LED Driver Market Trends and Insights

Subsidy-fuelled LED Retrofit Programs Drive Market Acceleration

India's UJALA initiative illustrates how large-scale distribution of efficient lamps can slash electricity demand by 20 GW and avoid 80 million t of CO2 annually. Unlike earlier discount schemes, the program's market-based approach sustained vendor margins, encouraging continual product upgrades that now emphasize advanced drivers with energy-monitoring functions. Similar schemes in China, Malaysia and the European Union are moving from bulb replacements toward holistic luminaire swaps, triggering demand for drivers that support wireless controls, target power factors above 0.9 and meet IEC flicker criteria. Because early LED waves entered service around 2015, a secondary replacement cycle of 5.8 billion units begins peaking between 2025 and 2028. These programs collectively add momentum to the LED driver market by ensuring predictable, large-volume procurement pipelines over the forecast period.

Rapid Price Declines in GaN-on-Si Driver ICs Enable Mass Adoption

Texas Instruments' migration from 6-inch to 8-inch GaN wafers cuts die cost while improving yield consistency, pushing power-conversion efficiency beyond 92% and shrinking thermal budgets.Infineon's 300 mm pilot line is expected to reach silicon-parity pricing in 2025, opening mainstream channels such as retail track lighting and appliance illumination. GaN's higher switching frequencies reduce magnetics size by up to 40%, enabling slimmer luminaire profiles and lowering enclosure temperatures, a critical factor for chip-on-board modules. Automotive headlamp systems benefit from GaN's resilience at high junction temperatures, supporting adaptive-beam architectures in electric vehicles. These economics support a virtuous cycle of integration: as volumes climb, cost drops deepen, broadening the LED driver market even further.

Persistent Silicon Supply Constraints Create Bottlenecks in Driver IC Production

Wolfspeed's liquidity pressures threaten silicon-carbide wafer availability for high-power lighting and EV applications. Foundries prioritize advanced 3-nm logic, leaving 16-90 nm capacity thin for the mixed-signal processes used in LED drivers. Lead times exceed 40 weeks for common MOSFETs; speciality PMICs stretch beyond a year, forcing design pivots and multi-sourcing strategies. The constraint drives price volatility that squeezes mid-tier OEM margins, dampening near-term shipment potential in segments such as outdoor lighting projects with firm bid ceilings. Until capacity additions in Southeast Asia come online, silicon shortfalls remain a measurable drag on the LED driver market.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Lighting Mandates in New-Build Codes Create Compliance-Driven Demand

- Mainstream Adoption of Matter/Thread Wireless Controls Standardizes Connectivity

- Limited Interoperability Across Legacy Wired Protocols Fragments Market Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Constant current devices held 61.2% LED driver market share in 2024, driven by decades of design familiarity in high-lumen applications. However, constant power drivers deliver up to 92% conversion efficiency and accommodate variable-voltage LED loads without redesign, supporting a projected 23.1% CAGR between 2025 and 2030. In the automotive front-lighting niche, Infineon's Litix Power Flex series illustrates the performance jump: SPI-controlled dimming and multi-string protection broaden functionality without thermal penalty.

The rise of adaptive lighting scenarios reinforces the shift. Architectural facades, sports arenas and tunable-white office fixtures benefit when output can adjust dynamically while current remains within diode tolerances. This versatility lowers SKU proliferation for luminaire makers and enhances field-upgrade paths. As wireless protocols proliferate, firmware-selectable power curves make constant power designs the preferred platform in the evolving LED driver market.

Wired systems, led by DALI and 0-10 V, accounted for 65.4% of the LED driver market size in 2024 because existing-bearing structures embed control cabling. Yet wireless features head into the steep part of the adoption curve, with a 24.3% CAGR through 2030. Legrand's Matter-approved wall-box dimmers demonstrate consumer enthusiasm for app-based commissioning.

From a total-cost lens, eliminating control wires trims labour 15-25% in commercial retrofit budgets, often swinging ROI in favour of LED plus controls. Thread's IPv6 foundation eases building-management integration, and BLE mesh provides low-energy fallback for emergency lighting checks. With over-the-air firmware updates now mainstream, wireless drivers extend operating lifetimes by accommodating future features. These advantages cement wireless as a pillar of the LED driver market.

LED Driver Market Report is Segmented by Product Type (Constant Current LED Drivers, and More), Control Feature (Wired, Wireless), Power Output (Less Than25W, 25-65W, and More), Form Factor (External Stand-Alone, Integrated/On-Board, and More), End-Use Application (Residential, Commercial and Office, Retail and Hospitality, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 32.3% revenue share in 2024 derives from rigorous lamp-efficacy rules that raise the bar to 83-195 lm/W, steering specifiers toward high-efficiency drivers. Corporate retrofits such as Coca-Cola Consolidated's six-facility upgrade realize USD 97,063 annual savings and underline the quick payback narrative. The CHIPS Act allocates USD 200 billion for domestic fabs, improving resilience for analog and power components. Canada and Mexico leverage integrated supply chains to share technical standards and qualification labs, smoothing cross-border shipments.

Asia-Pacific exhibits the fastest structural rise, projecting a 24.2% CAGR through 2030. China's manufacturing depth slashes BOM costs, and its municipal smart-city grants stimulate local demand for drivers with NB-IoT or LoRa gateways. India's record-scale UJALA program replenishes lamp inventories at end-of-life, kick-starting a second-wave luminaire upgrade cycle. Japan, South Korea and Taiwan channel EV-led headlamp innovations into exportable adaptive-beam drivers. ASEAN markets absorb supply-chain diversification, with Vietnam emerging as a finish-and-assembly hub for North American brands.

Europe sustains momentum through Ecodesign 2019/2020, which targets 96 TWh savings annually by 2030. Germany's KfW-bank subsidies tie preferential interest rates to intelligent-lighting deployment, accelerating driver replacements in logistics warehouses. Eastern European retrofit pipelines receive cohesion-fund backing, while the United Kingdom's Building Regulations Part L references dynamic-lighting guidance that favours drivers capable of open-protocol communication. The Middle East and Africa supplement the global LED driver market with Vision 2030 programs, typified by Saudi Arabia's 10% CAGR LED adoption outlook underpinned by local assembly ventures.

- Signify

- ams OSRAM

- Acuity Brands Lighting

- Hubbell Incorporated

- Eaton (Cooper Lighting)

- Lutron Electronics

- Cree LED (SGH)

- MEAN WELL Enterprises

- Inventronics

- Tridonic (Zumtobel)

- Delta Electronics

- Shenzhen Done Power

- ERP Power

- Lifud Technology

- Helvar

- Murata Manufacturing

- Texas Instruments

- ON Semi

- Allegro MicroSystems

- ROHM Semiconductor

- Macroblock Inc.

- TCI Srl

- MOSO Power

- Current (GE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-fuelled LED retrofit programs (post-2025 roll-outs)

- 4.2.2 Rapid price declines in GaN-on-Si driver ICs

- 4.2.3 Smart-lighting mandates in new-build codes

- 4.2.4 Mainstream adoption of Matter/Thread wireless controls

- 4.2.5 Surge in EV headlamp LED driver demand

- 4.2.6 Corporate net-zero targets accelerating industrial upgrades

- 4.3 Market Restraints

- 4.3.1 Persistent silicon supply constraints for driver ICs

- 4.3.2 Limited interoperability across legacy wired protocols

- 4.3.3 Design-in complexity for non-isolated drivers

- 4.3.4 High import tariffs on Chinese constant-current modules

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Constant Current LED Drivers

- 5.1.2 Constant Voltage LED Drivers

- 5.1.3 Constant Power LED Drivers

- 5.2 By Control Feature

- 5.2.1 Wired

- 5.2.1.1 0-10 V

- 5.2.1.2 DALI

- 5.2.1.3 DMX

- 5.2.1.4 PLC

- 5.2.1.5 Trailing-Edge

- 5.2.2 Wireless

- 5.2.2.1 Wi-Fi

- 5.2.2.2 Bluetooth/BLE

- 5.2.2.3 Zigbee

- 5.2.2.4 Thread / Matter

- 5.2.2.5 Li-Fi

- 5.2.1 Wired

- 5.3 By Power Output

- 5.3.1 Less than 25 W

- 5.3.2 25 - 65 W

- 5.3.3 65 -150 W

- 5.3.4 Greater than 150 W

- 5.4 By Form Factor

- 5.4.1 External Stand-Alone

- 5.4.2 Integrated / On-Board

- 5.4.3 Linear Drivers

- 5.4.4 Compact / Module Drivers

- 5.5 By End-Use Application

- 5.5.1 Residential

- 5.5.2 Commercial and Office

- 5.5.3 Retail and Hospitality

- 5.5.4 Outdoor and Street Lighting

- 5.5.5 Industrial

- 5.5.6 Healthcare and Education

- 5.5.7 Automotive Lighting Systems

- 5.5.8 Horticulture and Agriculture

- 5.5.9 Consumer-Electronics Backlighting

- 5.5.10 Other Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Qatar

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Kenya

- 5.6.5.2.5 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify

- 6.4.2 ams OSRAM

- 6.4.3 Acuity Brands Lighting

- 6.4.4 Hubbell Incorporated

- 6.4.5 Eaton (Cooper Lighting)

- 6.4.6 Lutron Electronics

- 6.4.7 Cree LED (SGH)

- 6.4.8 MEAN WELL Enterprises

- 6.4.9 Inventronics

- 6.4.10 Tridonic (Zumtobel)

- 6.4.11 Delta Electronics

- 6.4.12 Shenzhen Done Power

- 6.4.13 ERP Power

- 6.4.14 Lifud Technology

- 6.4.15 Helvar

- 6.4.16 Murata Manufacturing

- 6.4.17 Texas Instruments

- 6.4.18 ON Semi

- 6.4.19 Allegro MicroSystems

- 6.4.20 ROHM Semiconductor

- 6.4.21 Macroblock Inc.

- 6.4.22 TCI Srl

- 6.4.23 MOSO Power

- 6.4.24 Current (GE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Opportunities in Non-Isolated Drivers

- 7.3 Visible-Light Communication Integration

- 7.4 GaN and SiC-based Driver IC Adoption

8 INVESTMENT ANALYSIS

全球LED驅動器市場:依照明燈具類型、控制功能、最終用途、應用、組件、產品、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032)

全球LED驅動器市場:依照明燈具類型、控制功能、最終用途、應用、組件、產品、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032) LED驅動器市場規模、佔有率和趨勢分析報告:按照明燈具類型、組件、供應類型、應用、地區和細分市場預測,2026-2033年

LED驅動器市場規模、佔有率和趨勢分析報告:按照明燈具類型、組件、供應類型、應用、地區和細分市場預測,2026-2033年 2026年全球LED驅動器市場報告LED照明驅動器全球市場報告(2026年)

2026年全球LED驅動器市場報告LED照明驅動器全球市場報告(2026年) LED驅動燈市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、技術、最終用戶、地區和競爭格局分類,2021-2031年預測

LED驅動燈市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、技術、最終用戶、地區和競爭格局分類,2021-2031年預測 LED驅動器市場規模、佔有率及成長分析(按組件、燈具、應用、最終用戶和地區分類)-2026-2033年產業預測

LED驅動器市場規模、佔有率及成長分析(按組件、燈具、應用、最終用戶和地區分類)-2026-2033年產業預測 LED 驅動器市場(按輸出電流、產品類型、調光、輸入類型、應用、最終用戶、實施和分銷管道)- 全球預測,2025 年至 2032 年

LED 驅動器市場(按輸出電流、產品類型、調光、輸入類型、應用、最終用戶、實施和分銷管道)- 全球預測,2025 年至 2032 年 LED 驅動器和 T 燈的全球市場LED驅動器反射器的全球市場

LED 驅動器和 T 燈的全球市場LED驅動器反射器的全球市場 全球 LED 驅動器市場規模(按類型、應用、最終用戶、區域範圍和預測)

全球 LED 驅動器市場規模(按類型、應用、最終用戶、區域範圍和預測)