|

市場調查報告書

商品編碼

1851712

預防資料外泄(DLP):市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Data Loss Prevention (DLP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

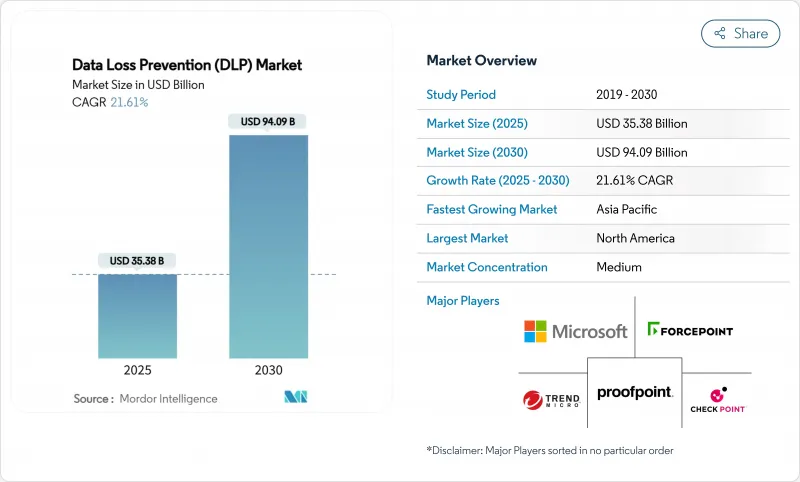

預計到 2025 年,預防資料外泄市場規模將達到 353.8 億美元,到 2030 年將達到 940.9 億美元,在此期間的複合年成長率為 21.61%。

監管處罰力度加大、混合職場中敏感資料的分散以及將資料防洩漏 (DLP) 控制整合到零信任和安全存取服務邊際平台,是推動 DLP 快速發展的因素。人工智慧驅動的策略調整透過降低誤報率和減輕分析師疲勞,進一步加速了 DLP 的普及;而雲端交付部署模式則為企業提供了保護其分散式使用者所需的彈性。透過收購將 DLP 整合到更廣泛的資料安全解決方案中的供應商整合,凸顯了向統一平台策略的轉變,該平台能夠跨端點、網路和多重雲端環境進行檢測、分類和保護。

全球預防資料外泄(DLP) 市場趨勢與洞察

GDPR 2.0 和 CCPA 修正案加強了對網路安全違規行為的處罰力度

巨額罰款正在改變監管機構的支出重點:TikTok 因違反資料傳輸控制規定而被處以 5.3 億歐元(約 6.2418 億美元)的罰款,這凸顯了監管機構願意對此類違規行為處以創紀錄的罰款。同時,英國的《數據(使用和存取)法案》加強了資料處理規則,歐盟的人工智慧法案引入了強制性透明度審核。在加州,《加州消費者隱私法案》(CCPA) 的最新修訂擴大了敏感個人資訊的定義,加強了消費者權益,同時也增加了在全美範圍內營運的公司的合規風險。如今,企業主管普遍將強大的資料防洩漏 (DLP) 能力視為一項切實有效的風險緩解措施,而非可有可無的網路安全措施,這推動了預防資料外泄市場的成長。

混合辦公模式的資料激增增加了終端和雲端風險。

IBM 發布的《2023 年資料外洩報告》顯示,82% 的資料外洩事件涉及雲端數據,凸顯了該公司邊界防禦的薄弱環節。員工擴大使用個人設備和核准的SaaS 工具,導致傳統控制措施無法有效監控盲點。在製造業等操作技術與 IT 系統融合的產業,生產設備也接入網路,進一步擴大了攻擊面。因此,企業正在採用端點資料防洩漏 (DLP) 來實現設備級控制,同時也在多個雲端服務供應商之間擴展雲端 DLP 規則,從而推動了預防資料外泄市場的需求成長。

多重雲端部署的複雜性與技能差距

企業通常經營三到五個雲端平台,每個平台都有各自的存取控制和加密方案。安全團隊缺乏必要的專業知識,難以協調各項策略,導致引進週期延長,營運成本上升。因此,雲端安全人才短缺正在阻礙預防資料外泄市場轉型為完全編配的多重雲端保護。

細分市場分析

預計到2024年,雲端基礎的部署模式將佔據67.3%的市場佔有率,並且到2030年,該細分市場預計將保持22.1%的複合年成長率。因此,隨著企業採用SASE(安全應用安全擴展)技術,雲端服務的預防資料外泄市場規模也將同步成長。雲端服務支援遠端使用者進行單一主機管理和彈性策略執行,從而減輕了修補程式和硬體更新周期的負擔。在國防和關鍵基礎設施等高度監管的產業,本地部署解決方案仍然佔據主導地位,因為這些產業的資料必須儲存在受實體控制的位置。然而,混合辦公模式的現實需求是無處不在的存取檢查,而純粹的本地配置無法有效地滿足這一需求,從而限制了其相對成長。

Cloudflare 的 SASE 框架展示了整合式 DLP 如何偵測並阻止安全 Web 閘道和 CASB 流中的政策違規行為,這標誌著架構偏好正向聚合服務轉變。快速擴展或應對季節性資料高峰的組織可以從計量型的消費模式中受益,這種模式將成本與使用量掛鉤,從而增強了預防資料外泄市場的需求成長動能。

到2024年,端點控制將佔總收入的46.7%,並以22.4%的複合年成長率保持成長最快的解決方案地位,這反映了以設備為中心的數據處理的爆炸性成長。生成式人工智慧編碼助理的日益普及引入了新的資料外洩途徑,而端點代理可以獨特地阻止這些途徑。研究人員已經展示了“規則文件後門”,這種後門可以繞過傳統的審查,並通過看似無害的配置文件走私機密資訊。供應商現在正在將行為人工智慧融入資料保護中,以監控剪貼簿使用情況、螢幕截圖和程式碼產生模式,從而提高保護的準確性並推動預防資料外泄市場的成長。

網路資料防洩漏 (DLP) 在傳輸過程中的資料審查方面仍然至關重要,尤其是在複雜的園區網路中;而以儲存為中心的工具則用於保護資料中心的大型檔案共用。儘管如此,隨著員工在筆記型電腦、行動裝置和虛擬桌面上直接接觸敏感數據,企業正逐漸傾向採用以終端為先的策略。微軟的 Purview 套件將終端策略擴展到瀏覽器流量和 SaaS 會話,展示了平台供應商如何將資料管治與終端遙測結合。

預防資料外泄市場按部署方式(本地部署、雲端基礎)、解決方案(網路資料防洩漏、終端資料防洩漏及其他)、最終用戶產業(銀行、金融服務和保險、IT與通訊、製造業及其他)、應用領域(雲端儲存安全、電子郵件與協作保護及其他)以及地區進行細分。市場預測以美元計價。

區域分析

預計到2024年,北美將佔全球收入的24.2%,這得益於嚴格的聯邦和州政府法規以及資金雄厚的私營部門對零信任項目的投入。美國在網路安全和基礎設施安全局的SASE藍圖中納入了資料防洩漏(DLP)技術,加拿大的隱私權政策體係以及墨西哥不斷發展的金融科技生態系統都在推動這一成長。高昂的資料外洩成本和成熟的網路保險市場維持了高階控制措施的溢價,進一步鞏固了北美作為預防資料外泄市場技術試驗場的地位。

亞太地區預計將以21.1%的複合年成長率加速成長,這主要得益於快速的數位化進程和各國主權雲端法律對資料駐留的強制性要求。中國的《網路安全法》和印度的《數位個人資料保護法》要求進行在地化政策編配,從而推動了該地區對雲端交付且符合當地管轄範圍的解決方案的需求。日本和韓國正在採用終端資料防洩漏(DLP)技術來保護其製造技術,而東南亞國協則正在轉向將DLP與安全Web閘道器捆綁在一起的雲端原生架構。這些法規和威脅的交織使得亞太地區成為預防資料外泄市場最具活力的地區。

歐洲的成長取決於GDPR及其配套法規(例如《數位營運彈性法案》)的實施,該法案提高了金融機構的最低控制標準。德國和英國正透過強勁的銀行業和產業部門來支持支出,而法國則在推進其主權雲端計劃,以支援本地託管的資料防洩漏(DLP)服務。儘管南歐國家的DLP採用速度保持穩定,但歐盟範圍內強制執行的「隱私設計」政策正對供應商的DLP產品產生重大影響。雲端外包指南中的資料在地化條款正在推動對能夠跨國保持策略一致性的平台的興趣,從而維持預防資料外泄市場的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- GDPR 2.0 和 CCPA 修正案加強了對網路安全違規行為的處罰力度

- 混合辦公模式的資料蔓延加劇了終端和雲端風險

- 融合型資料防洩漏 (DLP)、雲端存取安全代理程式 (CASB) 和數位訊號處理管理 (DSPM) 平台

- AI輔助策略調整可降低誤報率

- 零信任和 SASE藍圖要求整合資料防洩漏

- Gen-AI程式碼複製批次會產生新的洩漏途徑

- 市場限制

- 多重雲端部署的複雜性與技能差距

- 傳統本地部署政策的總擁有成本高昂

- 隱私設計促進了對深度內容檢查的限制

- 主權雲端指令將導致全球政策碎片化

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場的宏觀經濟因素

第5章 市場規模與成長預測

- 透過部署

- 本地部署

- 雲端基礎的

- 透過解決方案

- 網路資料防洩漏

- 端點資料防洩漏

- 儲存/資料中心 DLP

- 其他

- 按最終用戶行業分類

- BFSI

- 資訊科技和電訊

- 政府/國防

- 衛生保健

- 零售和物流

- 製造業

- 其他

- 透過使用

- 雲端儲存安全

- 安全的電子郵件和協作

- 智慧財產權保護與原始碼管治

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Broadcom(Symantec)

- Microsoft

- Forcepoint

- Proofpoint

- Zscaler

- Trend Micro

- Check Point

- Cisco

- Palo Alto Networks

- CrowdStrike

- Netskope

- Trellix

- Digital Guardian(Fortra)

- CoSoSys

- GTB Technologies

- Spirion

- Safetica

- Code42

- Nightfall AI

- Cyera

- Fortinet

第7章 市場機會與未來展望

The data loss prevention market is valued at USD 35.38 billion in 2025 and is forecast to reach USD 94.09 billion by 2030, translating into a vigorous 21.61% CAGR over the period.

Rapid expansion is rooted in mounting regulatory penalties, the dispersal of sensitive data across hybrid workplaces, and the embedding of DLP controls inside zero-trust and Secure Access Service Edge platforms. Artificial-intelligence policy tuning is further accelerating adoption by trimming false-positive rates and reducing analyst fatigue, while cloud-delivered deployment models deliver the elasticity enterprises need to secure distributed users. Vendor consolidation driven by acquisitions that fold DLP into broader data-security posture offerings underscores a strategic pivot toward unified platforms capable of discovery, classification, and protection across endpoints, networks, and multicloud estates.

Global Data Loss Prevention (DLP) Market Trends and Insights

Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

Maximum penalties are reshaping spending priorities: TikTok's EUR 530 million (USD 624.18 million) fine in 2025 spotlighted regulators' readiness to levy record sanctions for lax data-transfer controls. In parallel, the UK Data (Use and Access) Bill tightens data-handling rules, and the EU AI Act introduces mandatory transparency audits, both driving proactive DLP investment. California's latest CCPA amendments widen the definition of sensitive personal information and strengthen consumer rights, expanding compliance exposure for enterprises operating nationwide. Across jurisdictions, executives now view robust DLP capability as a demonstrable risk-mitigation measure rather than a discretionary cybersecurity layer, propelling the data loss prevention market toward accelerated growth.

Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

IBM's 2023 breach report revealed that 82% of incidents involved cloud-resident data, underscoring the erosion of perimeter defenses IBM. Employees increasingly use personal devices and unsanctioned SaaS tools, creating blind spots that traditional controls cannot monitor. In sectors such as manufacturing where operational technology merges with IT systems the attack surface widens as production gear becomes network-connected. Organizations therefore adopt endpoint DLP for device-level controls while extending cloud DLP rules across multiple providers, fuelling demand in the data loss prevention market.

Complexity and Skills Gap in Multi-Cloud Roll-Outs

Firms commonly operate three to five cloud platforms, each with unique access controls and encryption schemes. Security teams struggle to harmonize policies without dedicated expertise, lengthening deployment cycles and inflating operating costs. The shortage of cloud-security talent therefore restrains the pace at which the data loss prevention market can transition toward fully orchestrated multicloud protection.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of DLP with CASB and DSPM Platforms

- AI-Assisted Policy Tuning Slashing False-Positive Rates

- High TCO for Legacy On-Prem Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment models secured 67.3% market share in 2024, and this segment is projected to sustain a 22.1% CAGR through 2030. The data loss prevention market size for cloud services will therefore scale in parallel with enterprise SASE adoption. Cloud delivery enables single console management and elastic policy enforcement across remote users, mitigating the burdens of patching and hardware refresh cycles. On-prem solutions persist in heavily regulated sectors such as defense or critical infrastructure where data must remain within physically controlled locations. Yet their relative growth is subdued because hybrid-work realities demand anywhere-access inspection that pure on-site deployments cannot deliver efficiently.

Cloudflare's SASE framework illustrates how integrated DLP detects and blocks policy violations within secure web gateway and CASB streams, demonstrating the architectural preference shift toward converged services. Organizations scaling rapidly or dealing with seasonal data spikes benefit from metered consumption models that align cost with usage, thereby reinforcing the demand trajectory of the data loss prevention market.

Endpoint controls accounted for 46.7% of revenue in 2024 and remain the fastest advancing solution at 22.4% CAGR, reflecting the surge in device-centric data handling. The rising prevalence of generative-AI coding assistants introduces novel exfiltration vectors that endpoint agents are uniquely positioned to intercept. Researchers demonstrated a "rules file backdoor" that smuggles secrets via benign-looking configuration files, bypassing conventional reviews. Vendors now embed behavioral AI to monitor clipboard use, screen capture, and code-generation patterns, increasing protection precision and powering growth in the data loss prevention market.

Network DLP preserves relevance for in-flight data scrutiny, especially in complex campus networks. Meanwhile, storage-centric tools protect high-volume file shares inside data centers. Nonetheless, enterprises gravitate toward endpoint-first strategies because employees engage with sensitive data directly on laptops, mobiles, and virtual desktops. Microsoft's Purview suite extends endpoint policies into browser traffic and SaaS sessions, signalling how platform vendors fuse data governance with endpoint telemetry.

Data Loss Prevention Market is Segmented by Deployment (On-Premises, Cloud-Based), Solution (Network DLP, Endpoint DLP, and More), End-User Industry (BFSI, IT and Telecom, Manufacturing, and More), Application (Cloud Storage Security, Email and Collaboration Protection, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 24.2% of global revenue in 2024, anchored by stringent federal and state regulations plus a well-capitalized private sector that budgets for zero-trust programs. United States agencies embrace DLP inside SASE blueprints published by the Cybersecurity and Infrastructure Security Agency, while Canada's privacy regime and Mexico's expanding fintech ecosystem add regional momentum. High breach costs and mature cyber-insurance markets sustain a premium on advanced controls, consolidating North America's role as a technology proving ground for the data loss prevention market.

Asia-Pacific is forecast to accelerate at 21.1% CAGR, catalyzed by rapid digitization and sovereign-cloud laws that mandate resident data storage. China's Cybersecurity Law and India's Digital Personal Data Protection Act compel localized policy orchestration, driving regional demand for cloud-delivered yet jurisdiction-aware solutions. Japan and South Korea deploy endpoint DLP to safeguard manufacturing know-how, while ASEAN economies leapfrog to cloud-native stacks that bundle DLP with secure web gateways. This regulatory and threat-exposure cocktail positions APAC as the most dynamic arena within the data loss prevention market.

Europe's growth rests on GDPR enforcement and complementary statutes such as the Digital Operational Resilience Act, which raise minimum control baselines for financial entities. Germany and the United Kingdom anchor spending through robust banking and industrial sectors, whereas France advances sovereign-cloud projects that favor locally hosted DLP services. Southern European economies adopt DLP at a steadier pace, yet pan-EU privacy-by-design mandates universally influence vendor offerings. Data localization clauses inside cloud-outsourcing guidelines spur interest in platforms capable of maintaining policy fidelity across borders, sustaining incremental gains for the data loss prevention market.

- Broadcom (Symantec)

- Microsoft

- Forcepoint

- Proofpoint

- Zscaler

- Trend Micro

- Check Point

- Cisco

- Palo Alto Networks

- CrowdStrike

- Netskope

- Trellix

- Digital Guardian (Fortra)

- CoSoSys

- GTB Technologies

- Spirion

- Safetica

- Code42

- Nightfall AI

- Cyera

- Fortinet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating cyber-breach fines under GDPR 2.0 and CCPA amendments

- 4.2.2 Hybrid-work data sprawl raising endpoint and cloud risk

- 4.2.3 Convergence of DLP with CASB and DSPM platforms

- 4.2.4 AI-assisted policy tuning slashing false-positive rates

- 4.2.5 Zero-trust and SASE road-maps mandating integrated DLP

- 4.2.6 Gen-AI code copilots creating new exfiltration vectors

- 4.3 Market Restraints

- 4.3.1 Complexity and skills gap in multi-cloud roll-outs

- 4.3.2 High TCO for legacy on-prem policies

- 4.3.3 Privacy-by-design push limiting deep content inspection

- 4.3.4 Sovereign-cloud mandates fragmenting global policy sets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud-based

- 5.2 By Solution

- 5.2.1 Network DLP

- 5.2.2 Endpoint DLP

- 5.2.3 Storage / Datacenter DLP

- 5.2.4 Others

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Retail and Logistics

- 5.3.6 Manufacturing

- 5.3.7 Others

- 5.4 By Application

- 5.4.1 Cloud Storage Security

- 5.4.2 Email and Collaboration Protection

- 5.4.3 IP Protection and Source-code Governance

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Broadcom (Symantec)

- 6.4.2 Microsoft

- 6.4.3 Forcepoint

- 6.4.4 Proofpoint

- 6.4.5 Zscaler

- 6.4.6 Trend Micro

- 6.4.7 Check Point

- 6.4.8 Cisco

- 6.4.9 Palo Alto Networks

- 6.4.10 CrowdStrike

- 6.4.11 Netskope

- 6.4.12 Trellix

- 6.4.13 Digital Guardian (Fortra)

- 6.4.14 CoSoSys

- 6.4.15 GTB Technologies

- 6.4.16 Spirion

- 6.4.17 Safetica

- 6.4.18 Code42

- 6.4.19 Nightfall AI

- 6.4.20 Cyera

- 6.4.21 Fortinet

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

雲端預防資料外泄市場(按組件、部署模型、組織規模和垂直產業)—全球預測 2025-2032預防資料外泄市場按組件、部署模型、組織規模和行業分類 - 全球預測 2025-2032 年

雲端預防資料外泄市場(按組件、部署模型、組織規模和垂直產業)—全球預測 2025-2032預防資料外泄市場按組件、部署模型、組織規模和行業分類 - 全球預測 2025-2032 年 企業 DLP 市場:2025-2030 年預測全球資料遺失預防市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球雲端 DLP 市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

企業 DLP 市場:2025-2030 年預測全球資料遺失預防市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球雲端 DLP 市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 預防資料外泄(DLP) 市場:2025-2029 年全球

預防資料外泄(DLP) 市場:2025-2029 年全球 2025 年至 2033 年資料遺失預防市場規模、佔有率、趨勢及預測(按類型、服務、規模、部署類型、應用程式和地區)

2025 年至 2033 年資料遺失預防市場規模、佔有率、趨勢及預測(按類型、服務、規模、部署類型、應用程式和地區) 2025年預防資料外泄全球市場報告

2025年預防資料外泄全球市場報告 資料遺失防護市場 - 全球產業規模、佔有率、趨勢、機會和預測(按軟體、服務、部署、企業規模、應用、最終用途、地區和競爭細分,2020-2030 年)

資料遺失防護市場 - 全球產業規模、佔有率、趨勢、機會和預測(按軟體、服務、部署、企業規模、應用、最終用途、地區和競爭細分,2020-2030 年) 全球資料外洩通知軟體市場

全球資料外洩通知軟體市場