|

市場調查報告書

商品編碼

1851664

水泵:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

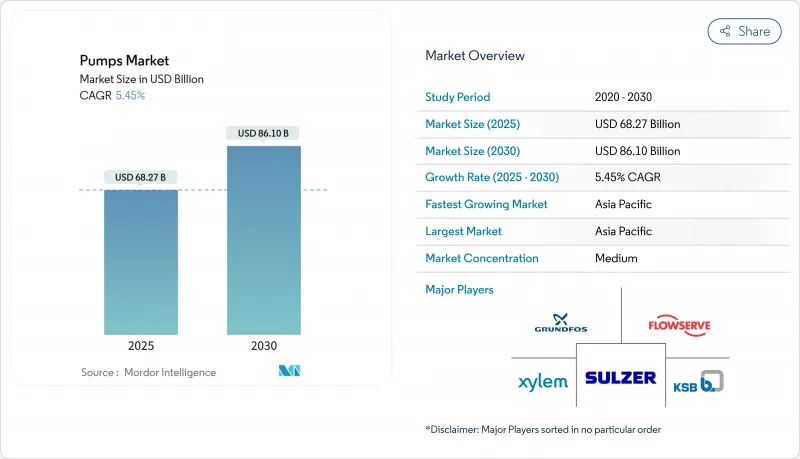

預計到 2025 年,泵浦市場規模將達到 682.7 億美元,到 2030 年將達到 861 億美元,預測期(2025-2030 年)的複合年成長率為 5.45%。

成長主要得益於大型水利基礎設施升級、強勁的工業資本投資以及對節能設備的普遍需求。儘管電氣化仍然是主要的能源來源,但太陽能發電系統在農業和離網環境中正迅速發展。技術規範正朝著智慧化、配備豐富感測器的水泵方向發展,這些水泵能夠降低能耗、實現預測性維護並符合更嚴格的環境法規。隨著現有供應商透過收購擴大產品組合,以及來自亞洲的低成本參與企業在價格和交貨速度方面展開競爭,競爭日益加劇。為了因應原物料價格的波動,供應鏈策略越來越重視材料節約和多區域採購。

全球泵浦市場趨勢與洞察

中東、非洲和亞太地區海水淡化計劃的資本投資不斷成長

預計到2024年,沙烏地阿拉伯和阿拉伯聯合大公國的海水淡化計劃總投資將超過48億美元,這將刺激對高壓泵的需求,這種高壓泵的陶瓷複合材料濕潤部件的使用壽命比同等不銹鋼部件長40%。能源回收設備現已成為新建工廠的標配,可將營業成本降低高達60%,這提高了技術門檻,使擁有成熟的船用級材料技術專長的供應商更具優勢。擁有海水淡化專案案例的製造商可以享受溢價,而競爭對手則競相獲取類似的資格。

歐洲和北美嚴格的污水再利用規定

修訂後的歐盟都市廢水處理指令旨在大幅降低磷和全氟烷基和多氟烷基物質(PFAS)的含量,加速採用精密噴射泵和變流量循環泵,以支援高級氧化和薄膜過濾。市政當局正在增加整合泵組的預算,平均訂單金額增加了27%。隨著公用事業公司轉向基於結果的採購模式,能夠提供控制和遠端監控功能的供應商在競標中脫穎而出。

鎳和不銹鋼價格波動導致物料清單成本上升。

據泵浦製造商稱,容積式泵浦含有30-40%的不銹鋼,因此價格上漲正在擠壓利潤淨利率。知名品牌目前正利用計算流體力學,在某些型號中將合金重量減少15%,並透過從多個地區採購來分散風險。

細分市場分析

到2024年,離心泵將佔據泵浦市場56.8%的佔有率。葉輪形狀和導葉輪廓的不斷改進,使水力效率提高了15%。預計該細分市場將以6.2%的複合年成長率成長,超過泵浦市場整體成長速度。離心泵在供水、暖通空調和煉油廠等領域的廣泛應用為其提供了穩定的基礎,而新興的碳捕集裝置則需要配備先進密封件和耐腐蝕合金的客製化二氧化碳處理裝置。

專用離心式幫浦正逐漸應用於捕碳封存(CCS)迴路,此迴路處理液態與超臨界二氧化碳時,會表現出複雜的動態行為。整合感測器陣列的供應商能夠幫助營運商降低能耗和維護成本,並使泵浦的運作更接近最佳效率點。容積式泵浦在計量、化學藥劑注入和高壓漿料操作中仍然至關重要,並且由於這些特定領域對性能公差要求更高,因此價格也更高。

由於水平泵浦因其普及性、易於維護和初始成本低等優點,目前仍佔據泵浦市場60%的佔有率。然而,隨著都市區公共和資料中心建設者面臨占地面積限制,立式直列泵浦和潛水泵浦預計將以5.8%的複合年成長率成長。 ABB即將收購Aurora Motors,這將增強其垂直馬達產品線,顯示該供應商對長期成長充滿信心。

立式泵浦在驅動裝置位於流體上方的應用中將得到更廣泛的應用,例如深井給水、礦井排水和污水濕井裝置。升級的軸承系統和耐磨塗層可以延長泵送運作的間隔時間。此外,更嚴格的建築規範也促進了這一領域的需求,這些規範鼓勵採用緊湊型機房和堆疊式機械空間。

泵浦市場報告按泵浦類型(離心泵浦、容積式泵浦、其他)、軸向(水平、垂直)、驅動動力(電力、引擎、氣動、太陽能)、最終用戶(水和污水公共產業、化學和石化、發電、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。

區域分析

預計亞太地區將在2024年以51.60%的市佔率引領全球水泵市場,並在2030年之前維持6.0%的複合年成長率。大規模的都市化、雄心勃勃的海水淡化項目以及強勁的農業現代化是推動市場成長的主要動力。中國的國家藍圖和印度的太陽能水泵推廣計畫將持續維持強勁的需求。區域製造商正向價值鏈上游轉型,開發配備感測器的設備,加劇了區域內的競爭。

北美依然是創新主導。 2024會計年度聯邦政府撥款30億美元用於鉛水管更換,將刺激先進飲用水設備的訂單。美國墨西哥灣沿岸頁岩氣開發將推動對10,000磅/平方英吋壓裂設備的需求,而加拿大礦業公司則採購重型泥漿設備。到2024年,熱泵的性能將比燃氣爐高出27%,凸顯了電氣化對水泵選擇的影響。

歐洲高度重視生命週期效率和環境合規性。歐盟污水指令已更新,為精密噴射泵和膜泵創造了巨大的市場。北歐區域供熱網路正在快速擴張,需要能夠在低溫下運作的大型循環泵。德國和英國的公共產業正在實施預測性維護軟體,以提高資產運轉率並延長更換週期。中東正大力投資海水淡化和區域冷卻。同時,許多非洲國家正在優先發展離網太陽能灌溉解決方案,以提高作物產量並減少對柴油燃料的依賴。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 最新進展

- 市場促進因素

- 中東、非洲和亞太地區海水淡化計劃的資本投資不斷成長

- 歐洲和北美更嚴格的污水再利用規定

- 美國墨西哥灣沿岸和巴西頁岩油氣和深水油氣計劃快速擴張

- 北歐和中東地區區域供暖和製冷設施迅速成長

- 印度和非洲農業灌溉電氣化(太陽能水泵)

- 市場限制

- 鎳和不銹鋼價格波動導致物料清單成本上升。

- 中國低成本製造商的激增正在擠壓淨利率。

- 減少經合組織國家的火力發電管路和循環泵

- 地方政府的更換週期較長(15-20年),限制了年銷售額。

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按泵類型

- 離心式(徑流式、軸流式、混合流式)

- 容積式(旋轉式(齒輪、凸輪、葉片、螺桿)、往復式(活塞、膜片、柱塞))

- 其他(特殊用途,噴射幫浦)

- 按軸方向

- 水平的

- 垂直的

- 驅動力

- 電的

- 引擎驅動

- 氣動/空氣驅動

- 太陽能發電

- 最終用戶

- 用水和污水業務

- 石油和天然氣(上游、中游、下游)

- 化工/石油化工

- 發電(火力發電、核能、可再生能源發電)

- 採礦和金屬

- 暖通空調和建築服務

- 農業與灌溉

- 建築和基礎設施

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Flowserve Corporation

- Grundfos Holding A/S

- KSB SE & Co. KGaA

- ITT Inc.

- Sulzer Ltd.

- Ebara Corporation

- Weir Group plc

- Xylem Inc.

- Wilo SE

- Pentair plc

- Tsurumi Manufacturing Co. Ltd.

- Torishima Pump Mfg. Co. Ltd.

- Baker Hughes Company

- Schlumberger Limited

- Celeros Flow Technology LLC

- Atlas Copco AB

- Kirloskar Brothers Ltd.

- Ruhrpumpen Group

- Desmi A/S

- Zoeller Pump Co.

第7章 市場機會與未來展望

The Pumps Market size is estimated at USD 68.27 billion in 2025, and is expected to reach USD 86.10 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

Growth is supported by large-scale water infrastructure upgrades, steady industrial capital spending, and the universal push for energy-efficient equipment. Electrification remains the dominant power source, while solar-powered systems create a fast-growing niche in agriculture and off-grid settings. Technical specifications are shifting toward smart, sensor-rich pumps that lower energy consumption, enable predictive maintenance, and meet tightening environmental rules. Competitive intensity is rising as established suppliers broaden portfolios through acquisitions and low-cost Asian entrants compete on price and delivery speed. Supply-chain strategies increasingly emphasize material savings and multi-regional sourcing to counter raw-material price swings.

Global Pumps Market Trends and Insights

Escalating CAPEX in Desalination Projects across MENA & APAC

Seawater-desalination build-outs in Saudi Arabia and the UAE exceeded USD 4.8 billion in 2024, spurring demand for high-pressure pumps with ceramic composite wetted parts that last 40% longer than stainless-steel equivalents. Energy-recovery devices now standardize in new plants, trimming operating costs by up to 60% and raising technical barriers that favor suppliers with proven marine-grade materials expertise. Manufacturers with desalination references are capitalizing on premium pricing while competitors race to secure similar credentials.

Stringent Wastewater Reuse Mandates in Europe & North America

The revised EU Urban Waste Water Treatment Directive targets steep cuts in phosphorus and PFAS, accelerating adoption of precision-dosing and variable-flow circulation pumps able to support advanced oxidation and membrane filtration. Municipalities allocate more budget to integrated pump packages, raising the average order value by 27%. Suppliers offering controls and remote-monitoring capabilities are winning bids as utilities shift to outcome-based procurement.

Volatility in Nickel & Stainless-Steel Prices Inflating BoM

Pump producers report stainless-steel content of 30-40% in positive-displacement designs, so price spikes squeeze margins. Leading European brands now use computational fluid dynamics to reduce alloy weight by 15% in selected models and hedge exposure through multi-regional sourcing.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Shale & Deep-water O&G Projects in US Gulf & Brazil

- Surging District Cooling & Heating Installations in Nordics & Middle East

- Proliferation of Low-cost Chinese Manufacturers Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps accounted for 56.8% of pumps market share in 2024. Continuous improvements in impeller geometry and guide-blade profiles have lifted hydraulic efficiency by up to 15%. The segment is forecast to post a 6.2% CAGR, outpacing the overall pumps market. Widespread use in water supply, HVAC and refinery services provides a stable base, while emerging carbon-capture plants require tailored CO2-handling models with advanced seals and corrosion-resistant alloys.

Specialized centrifugal variants now enter carbon-capture and storage (CCS) circuits, where liquid and supercritical CO2 present complex thermodynamic behavior. Vendors integrating sensor arrays enable operators to run close to best-efficiency points, cutting energy consumption and maintenance costs. Positive-displacement designs remain indispensable in metering, chemical injection and high-pressure slurry duties, commanding premium pricing due to stricter performance tolerances across these niches.

Horizontal machines still dominate 60% of the pumps market share due to familiarity, straightforward maintenance, and lower initial cost. However, vertical inline and submersible models are set to grow by 5.8% CAGR as urban utilities and data-center builders confront floor-space constraints. ABB's pending addition of Aurora Motors strengthens its vertical-motor lineup, signaling supplier confidence in long-term upside.

Vertical pumps thrive in deep-well water supply, mining dewatering ,and wastewater wet-well installations where the driver remains above the fluid. Upgraded bearing systems and abrasion-resistant coatings allow longer run times between pulls. Segment demand also benefits from stricter building codes that favor compact plantrooms and stacked mechanical spaces.

The Pumps Market Report is Segmented by Pump Type (Centrifugal, Positive Displacement, and Others), Shaft Orientation (Horizontal and Vertical), Driving Force (Electric-Driven, Engine-Driven, Pneumatic, and Solar-Powered), End User (Water and Waste-Water Utilities, Chemicals and Petrochemicals, Power Generation, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific leads the pumps market with 51.60% share in 2024 and is expected to post a 6.0% CAGR through 2030. Massive urbanization, ambitious desalination pipelines, and strong agricultural modernization underpin growth. China's national heat-pump roadmap and India's solar-pump rollout sustain high-volume demand. Regional manufacturers move up the value chain toward sensor-enabled units, intensifying local competition.

North America remains innovation-driven. Federal water-infrastructure funding of USD 3.0 billion for lead-service-line replacement in FY2024 stimulates advanced potable-water equipment orders. Shale development in the US Gulf boosts demand for 10,000-psi fracturing pumps, while Canadian miners procure hard-wearing slurry units. Heat pumps outsold gas furnaces by 27% in 2024, highlighting electrification's ripple effect on pump selection.

Europe emphasizes lifecycle efficiency and environmental compliance. The updated EU wastewater directive creates a sizeable market for precision-dosing and membrane-feed pumps. Nordic district-heating networks scale rapidly, requiring large circulation pumps compatible with low-temperature operation. Utilities in Germany and the United Kingdom deploy predictive-maintenance software to lift asset availability and stretch replacement intervals. The Middle East channels heavy investment into desalination and district cooling, whereas many African economies prioritize off-grid solar irrigation solutions to raise farm yields and reduce diesel dependence.

- Flowserve Corporation

- Grundfos Holding A/S

- KSB SE & Co. KGaA

- ITT Inc.

- Sulzer Ltd.

- Ebara Corporation

- Weir Group plc

- Xylem Inc.

- Wilo SE

- Pentair plc

- Tsurumi Manufacturing Co. Ltd.

- Torishima Pump Mfg. Co. Ltd.

- Baker Hughes Company

- Schlumberger Limited

- Celeros Flow Technology LLC

- Atlas Copco AB

- Kirloskar Brothers Ltd.

- Ruhrpumpen Group

- Desmi A/S

- Zoeller Pump Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends & Developments

- 4.3 Market Drivers

- 4.3.1 Escalating CAPEX in Desalination Projects across MENA & APAC

- 4.3.2 Stringent Waste-water Reuse Mandates in Europe & North America

- 4.3.3 Rapid Expansion of Shale & Deep-water O&G Projects in US Gulf & Brazil

- 4.3.4 Surging District Cooling & Heating Installations in Nordics & Middle East

- 4.3.5 Electrification of Agricultural Irrigation (Solar Pumps) in India & Africa

- 4.4 Market Restraints

- 4.4.1 Volatility in Nickel & Stainless-Steel Prices Inflating BoM

- 4.4.2 Proliferation of Low-cost Chinese Manufacturers Compressing Margins

- 4.4.3 Declining Thermal Power Pipeline in OECD Curtailing Circulation Pumps

- 4.4.4 Long Municipal Replacement Cycles (15?20 yrs) Limiting Annual Sales

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Investment Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Pump Type

- 5.1.1 Centrifugal (Radial-flow, Axial-flow and Mixed-flow)

- 5.1.2 Positive Displacement (Rotary (Gear, Lobe, Vane, Screw), and Reciprocating (Piston, Diaphragm, Plunger))

- 5.1.3 Others (Specialty, Jet Pumps)

- 5.2 By Shaft Orientation

- 5.2.1 Horizontal

- 5.2.2 Vertical

- 5.3 By Driving Force

- 5.3.1 Electric-driven

- 5.3.2 Engine-driven

- 5.3.3 Pneumatic/Air-operated

- 5.3.4 Solar-powered

- 5.4 By End-user

- 5.4.1 Water and Waste-water Utilities

- 5.4.2 Oil and Gas (Upstream, Midstream, Downstream)

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Power Generation (Thermal, Nuclear, Renewables)

- 5.4.5 Mining and Metals

- 5.4.6 HVAC and Building Services

- 5.4.7 Agriculture and Irrigation

- 5.4.8 Construction and Infrastructure

- 5.4.9 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Nordic Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Thailand

- 5.5.3.7 Indonesia

- 5.5.3.8 Vietnam

- 5.5.3.9 Australia

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Flowserve Corporation

- 6.4.2 Grundfos Holding A/S

- 6.4.3 KSB SE & Co. KGaA

- 6.4.4 ITT Inc.

- 6.4.5 Sulzer Ltd.

- 6.4.6 Ebara Corporation

- 6.4.7 Weir Group plc

- 6.4.8 Xylem Inc.

- 6.4.9 Wilo SE

- 6.4.10 Pentair plc

- 6.4.11 Tsurumi Manufacturing Co. Ltd.

- 6.4.12 Torishima Pump Mfg. Co. Ltd.

- 6.4.13 Baker Hughes Company

- 6.4.14 Schlumberger Limited

- 6.4.15 Celeros Flow Technology LLC

- 6.4.16 Atlas Copco AB

- 6.4.17 Kirloskar Brothers Ltd.

- 6.4.18 Ruhrpumpen Group

- 6.4.19 Desmi A/S

- 6.4.20 Zoeller Pump Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

ATEX幫浦市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶產業、地區和競爭格局分類,2021-2031年

ATEX幫浦市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶產業、地區和競爭格局分類,2021-2031年 泵浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。

泵浦市場機會、成長要素、產業趨勢分析及2026-2035年預測。 固態廢棄物處理用防堵塞幫浦市場預測至2034年-按類型、材質、最終用戶和地區分類的全球分析工業氣動幫浦市場預測至2034年-按產品、類型、材質、應用、最終用戶和地區分類的全球分析

固態廢棄物處理用防堵塞幫浦市場預測至2034年-按類型、材質、最終用戶和地區分類的全球分析工業氣動幫浦市場預測至2034年-按產品、類型、材質、應用、最終用戶和地區分類的全球分析 農業泵浦市場:2026-2032年全球市場預測(按泵浦類型、驅動系統、額定功率、材質、應用、最終用戶和分銷管道分類)地熱流體幫浦市場:2026年至2032年全球市場預測(按泵浦類型、能源來源、部署模式、輸出、材質、應用和最終用戶分類)

農業泵浦市場:2026-2032年全球市場預測(按泵浦類型、驅動系統、額定功率、材質、應用、最終用戶和分銷管道分類)地熱流體幫浦市場:2026年至2032年全球市場預測(按泵浦類型、能源來源、部署模式、輸出、材質、應用和最終用戶分類) 液冷泵市場規模、佔有率和趨勢分析報告:按產品、電源、最終用途、應用、地區和細分市場分類 - 預測,2026-2033年

液冷泵市場規模、佔有率和趨勢分析報告:按產品、電源、最終用途、應用、地區和細分市場分類 - 預測,2026-2033年 全球商用建築幫浦市場(2024-2030 年)2025-2026年全球柴油幫浦市場固態處理用潛水泵市場:2026年至2032年全球預測(按泵類型、額定功率、安裝方式、驅動系統、排出口尺寸、材質、葉輪類型、級數、應用和最終用戶分類)

全球商用建築幫浦市場(2024-2030 年)2025-2026年全球柴油幫浦市場固態處理用潛水泵市場:2026年至2032年全球預測(按泵類型、額定功率、安裝方式、驅動系統、排出口尺寸、材質、葉輪類型、級數、應用和最終用戶分類)