|

市場調查報告書

商品編碼

1851607

液壓泵:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Hydraulic Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

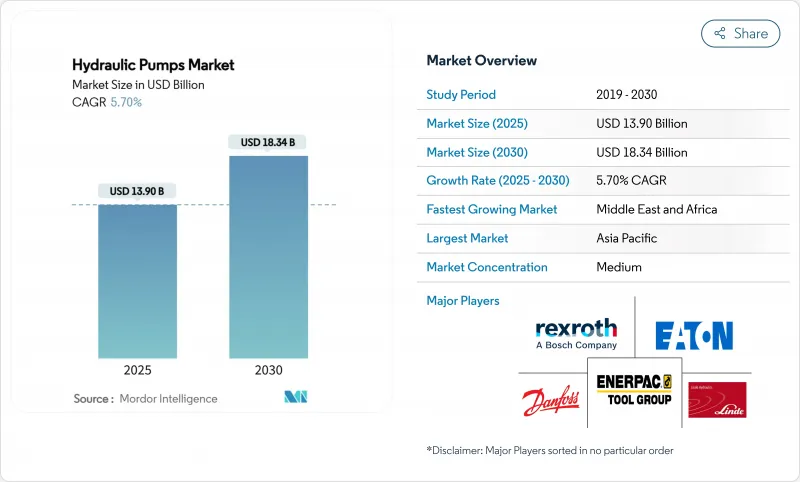

預計到 2025 年,液壓幫浦市場規模將達到 139 億美元,到 2030 年將成長至 183.4 億美元,複合年成長率為 5.70%。

建築、可再生能源和自動化製造業對大容量流體動力設備的強勁需求正推動市場穩步擴張。中國和印度的基礎設施更新計畫以及歐盟和北美流程工業的升級改造持續支撐著基準需求。能源轉型投資正在為風力發電機變槳和偏航系統、氫電解槽壓縮模組以及電網級電池冷卻迴路等領域創造新的機會。製造商正積極回應,推出更有效率的活塞泵設計、智慧控制包以及符合循環經濟指令的再製造服務。市場競爭依然適中,全球領導企業正著力強化其數位化產品組合,而區域供應商則專注於成本敏感應用領域。

全球液壓幫浦市場趨勢與洞察

中國和印度的基礎設施更新計劃

預計到2025年,兩國政府資助的在建工程將推動每年對液壓泵的需求超過1,350萬台。公共部門計劃的在地化政策鼓勵合資企業,並將約42億美元引入高科技幫浦的生產領域,加速國內產能建設。採用中國設備標準的區域承包商正在將其供應鏈擴展到中東和非洲,從而拓寬亞太地區製造商的出口前景。預計這些項目將支撐到2027年的基準需求,特別是對額定壓力高於5000 psi的液壓泵的需求。

工業自動化(工業4.0維修)

採用變頻驅動的智慧電源單元可將待機能耗降低 25%。物聯網閘道可將即時資料傳輸至預測性維護平台,降低營運成本 45%,並將計畫外排放事件減少 75%。數位雙胞胎模型可遠端最佳化,從而節能 30%,並將總擁有成本降低 20%。美國網路安全與基礎設施安全局 (CISA) 發布了關於泵浦控制器漏洞的建議,該漏洞的 CVSS 評分為 9.8,網路安全問題日益受到關注。

鎳鋼價格波動劇烈

隨著美國基礎設施建設支出恢復,含鎳合金成本在2024年底前持續上漲,隨後開始回落,並在2025年初反彈,這擠壓了泵浦製造商的利潤空間,並使庫存計劃變得更加複雜。高壓(3000 psi以上)型號的泵浦將受到最大衝擊,因為安全標準要求使用優質鋼材。依賴進口優質合金的中國製造商面臨外匯風險和物流額外費用。

細分市場分析

受移動機械需求的推動,齒輪泵預計在2024年將保持37%的市場佔有率。活塞泵的成長速度將超過市場平均水平,到2030年將以6.80%的複合年成長率成長,因為原始設備製造商(OEM)正朝著更高的容積效率和更精確的排氣量控制方向發展。派克漢尼汾的PV140系列活塞螺旋泵將繼續服務那些需要平穩流量和船用級可靠性的特定應用領域。

第二代活塞式液壓幫浦採用硬化滑閥和強化斜盤,將平均故障間隔時間延長至15,000小時,使用壽命是上一代產品的兩倍。此技術在加長型堆高機、挖土機和射出成型機的應用,凸顯了系統在能源最佳化和排放減排方面的專注。預計活塞式液壓泵在工業和可再生能源領域的市場佔有率將持續擴大。

到2024年,3000-5000 psi等級的泵浦將佔全球市場價值的42%,涵蓋主流建築和農業鑽機。 5000 psi以上的泵浦市場正以每年8.30%的速度成長,主要受氫氣壓縮、離岸風電和先進加工中心等產業的推動。 North Ridge Pumps公司獲得ATEX防爆認證的多級增壓幫浦可滿足電解槽開發商在1000 bar壓力下連續運作的需求。而3000 psi以下的泵浦則可在對成本敏感且性能閾值的市場中保持產能穩定性。

上游創新主要集中在密封系統和精細加工表面,以限制極端壓力下的洩漏。雙相不銹鋼和奈米塗層等材料科學突破旨在提高抗疲勞性,而即時壓力衰減演算法則可防止災難性故障。這些進步正在增強高壓液壓泵專家在能源轉型計劃中的市場佔有率。

液壓泵市場按泵浦類型(齒輪泵浦、葉片泵浦及其他)、工作壓力範圍(<3,000 psi、3,000-5,000 psi、>5,000 psi)、應用領域(移動液壓、工業機械、流程、能源)、天然氣使用者產業(建築、石油及其他)及地區進行細分。市場預測以美元計價。

區域分析

亞太地區的領先地位源自於其無與倫比的生產規模和國內消費能力,光是中國在2025年就計畫採購1,350萬台。印度的智慧城市計畫等政府項目正在資助水資源管理、地鐵建設和經濟適用房計劃,這些項目都需要高壓液壓系統。川崎的K3VL軸向柱塞系列液壓系統經常被指定用於高階挖土機。供應鏈中斷和技術純熟勞工短缺正在推動自動化和區域分散化向越南和印尼轉移。

中東的快速成長依賴石油和天然氣再投資以及可再生能源多元化發展。沙烏地阿拉伯公共投資基金正投入數十億美元建造太陽能和風力發電場,液壓偏航變槳驅動裝置有助於確保渦輪機的運作。阿拉伯聯合大公國的電網升級改造正在進口高壓泵,用於變電站冷卻和海水淡化。在達曼和阿布達比的聯合生產縮短了前置作業時間,並滿足了在地採購的要求。

北美和歐洲擁有技術先進的設備車隊。美國的《基礎設施投資與就業法案》重振了土木工程支出,推動了滑移裝載機和攤舖機的更換。歐盟促進循環經濟的法規正在創造新的再製造收入,並增加對符合EN ISO 14971認證的環保泵浦的需求。這兩個地區都面臨技術人員老化的挑戰,因此遠距離診斷的應用日益普及,以緩解服務瓶頸。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 中印基礎設施更新計劃

- 工業自動化(工業4.0改裝)

- 非公路用電氣化需要電動液壓泵

- 對風力發電機偏航和變槳系統的需求

- 氫氣電解槽的建造(泵壓超過1000巴)

- 強制性再製造配額(歐盟循環經濟)

- 市場限制

- 鎳和鋼鐵價格波動劇烈

- 全電動致動器的快速普及

- 智慧型幫浦的網路安全風險

- 註冊流體動力工程師短缺

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按泵類型

- 齒輪

- 葉片

- 活塞

- 擰緊

- 按工作壓力範圍

- 小於3000磅/平方英寸

- 3,000-5,000 psi

- 超過5000磅/平方英寸

- 按最終用戶行業分類

- 建造

- 石油和天然氣

- 發電業務

- 飲食

- 水和污水

- 化學

- 其他(農業、礦業、汽車業)

- 透過使用

- 移動式油壓設備

- 工業機械

- 過程能源(包括風能、水能和氫能)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他拉丁美洲地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bosch Rexroth AG

- Eaton Corporation plc

- Danfoss Power Solutions A/S

- Enerpac Tool Group Corp.

- Linde Hydraulics GmbH and Co. KG

- Dynamatic Technologies Limited

- HYDAC International GmbH

- Parker Hannifin Corporation

- Kawasaki Heavy Industries Ltd.

- Daikin Industries Ltd.

- Bucher Hydraulics GmbH

- KYB Corporation

- Shimadzu Corporation

- Permco Inc.

- Casappa SpA

- Ningbo Baichi Hydraulic

- HAWE Hydraulik SE

- Sun Hydraulics LLC

- Bosch Mahle Turbosystems Hydraulic(BMT)

- Bosch Rexroth India Pvt Ltd(regional)

第7章 市場機會與未來展望

The hydraulic pumps market size is estimated at USD 13.9 billion in 2025 and is forecast to climb to USD 18.34 billion by 2030, advancing at a 5.70% CAGR.

Robust demand for high-capacity fluid-power equipment in construction, renewable energy, and automated manufacturing keeps the market on a steady expansion path. Infrastructure renewal programmes in China and India, combined with process-industry upgrades in the European Union and North America, continue to anchor baseline demand. Energy transition investments are unlocking new opportunities in wind-turbine pitch and yaw systems, hydrogen electrolyser compression modules, and grid-scale battery storage cooling circuits. Manufacturers are responding with higher-efficiency piston pump designs, intelligent control packages, and remanufacturing services that align with circular-economy mandates. Competition remains moderate, with global leaders reinforcing digital portfolios while regional suppliers target cost-sensitive applications.

Global Hydraulic Pumps Market Trends and Insights

Infrastructure renewal programs in China and India

Government-funded construction pipelines in both nations sustain annual demand for more than 13.5 million hydraulic pump units by 2025. Localization rules for public-sector projects incentivise joint ventures, channelling roughly USD 4.2 billion into high-tech pump production and accelerating domestic capability building. Regional contractors adopting Chinese equipment standards are extending the supply chain into the Middle East and Africa, broadening export prospects for APAC manufacturers. These programmes are expected to underpin baseline demand through 2027, particularly for units rated above 5000 psi.

Industrial automation (Industry 4.0 retrofits)

Smart power units equipped with variable-frequency drives trim idle-time energy consumption by 25%. IoT gateways stream real-time data into predictive-maintenance platforms, cutting operating costs by 45% and reducing unplanned emissions events by 75%, as shown in UK water-utility trials with Sulzer controllers. Digital twin models enable remote optimisation that delivers 30% energy savings and 20% reduction in total cost of ownership. Cyber-security remains a rising concern following US CISA advisories on pump-controller vulnerabilities carrying CVSS scores up to 9.8.

Volatile nickel-steel prices

Nickel-bearing alloy costs climbed through late-2024 on renewed US infrastructure spending before receding, then rebounded in early-2025, compressing pump-maker margins and complicating inventory planning. High-pressure (>3000 psi) models suffer the most, as safety codes mandate premium steel grades. Chinese producers, reliant on imported high-grade alloy, face added currency risk and logistics surcharges.

Other drivers and restraints analyzed in the detailed report include:

- Off-highway electrification needs electro-hydraulic pumps

- Hydrogen electrolyser build-out (>1000 bar pumps)

- Rapid penetration of all-electric actuators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gear pumps retained 37% revenue share in 2024 on the strength of mobile-machinery demand. Piston pumps are outpacing at 6.80% CAGR to 2030 as OEMs migrate toward higher volumetric efficiency and precise displacement control. Parker Hannifin's PV140 piston series recorded 14,000 operating hours between overhauls in Australian mining vehicles, illustrating lifecycle cost advantages. Vane and screw pumps continue serving niche applications requiring smooth flow or marine-grade reliability.

Second-generation piston designs use hardened spool valves and reinforced swash plates to extend mean-time-between-failure to 15,000 hours, doubling service life relative to legacy units. Their adoption in telehandlers, excavators, and injection-moulding machines underscores a systemic pivot toward energy optimisation and reduced CO2 footprints. The hydraulic pumps market size for piston technology is expected to capture an incremental share in both industrial and renewable-energy installations.

The 3000-5000 psi class represented 42% of global value in 2024, covering mainstream construction and agricultural rigs. Pumps rated above 5000 psi are growing 8.30% annually, propelled by hydrogen compression, offshore wind, and advanced machining centres. North Ridge Pumps' multi-stage boosters, certified for ATEX zones, meet electrolyser developers' need for continuous duty at 1000 bar. Below-3000-psi units maintain volume stability in cost-sensitive markets where performance thresholds remain modest.

Upstream innovation focuses on sealing systems and micro-finish surfaces to curb leakage at extreme pressures. Material-science breakthroughs in duplex stainless and nano-coatings aim to raise fatigue resistance, while real-time pressure-derating algorithms prevent catastrophic failures. These advances reinforce the hydraulic pumps market share held by high-pressure specialists amid energy-transition projects.

Hydraulic Pumps Market Segmented by Pump Type (Gear, Vane, and More), Operating-Pressure Range (<3, 000 Psi, 3, 000 - 5, 000 Psi, >5, 000 Psi), Application (Mobile Hydraulics, Industrial Machinery, Process and Energy), End-User Vertical (Construction, Oil and Gas, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

APAC's leadership derives from unmatched production scale and domestic consumption, with China alone purchasing 13.5 million units in 2025. Government programmes such as India's Smart Cities Mission funnel capital into water-management, metro-rail, and affordable-housing projects requiring high-pressure hydraulic systems. Japanese suppliers continue to set benchmarks for reliability; Kawasaki's K3VL axial piston line is frequently specified on premium excavators. Supply-chain disruptions and skilled-labour shortages encourage automation and regional diversification into Vietnam and Indonesia.

The Middle East's swift growth rests on oil-and-gas reinvestment and renewable diversification agendas. Saudi Arabia's Public Investment Fund channels billions into solar- and wind-farm construction, where hydraulic yaw and pitch drives underpin turbine uptime. UAE's transmission grid upgrades import high-pressure pumps for substation cooling and seawater desalination. Joint-venture manufacturing in Dammam and Abu Dhabi shortens lead times and meets local-content mandates.

North America and Europe maintain technologically advanced fleets. The US Infrastructure Investment and Jobs Act revived civil works outlays, fuelling replacements across skid-steer loaders and pavers. EU regulations promoting circular-economy compliance create new remanufacturing revenue and elevate demand for eco-design pumps certified under EN ISO 14971. Both regions contend with an ageing technician workforce, prompting wider deployment of remote diagnostics to ease service bottlenecks.

- Bosch Rexroth AG

- Eaton Corporation plc

- Danfoss Power Solutions A/S

- Enerpac Tool Group Corp.

- Linde Hydraulics GmbH and Co. KG

- Dynamatic Technologies Limited

- HYDAC International GmbH

- Parker Hannifin Corporation

- Kawasaki Heavy Industries Ltd.

- Daikin Industries Ltd.

- Bucher Hydraulics GmbH

- KYB Corporation

- Shimadzu Corporation

- Permco Inc.

- Casappa S.p.A.

- Ningbo Baichi Hydraulic

- HAWE Hydraulik SE

- Sun Hydraulics LLC

- Bosch Mahle Turbosystems Hydraulic (BMT)

- Bosch Rexroth India Pvt Ltd (regional)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure renewal programmes in China and India

- 4.2.2 Industrial automation (Industry 4.0 retrofits)

- 4.2.3 Off-highway electrification needs electro-hydraulic pumps

- 4.2.4 Wind-turbine yaw and pitch system demand

- 4.2.5 Hydrogen electrolyser build-out (>1 000 bar pumps)

- 4.2.6 Mandatory remanufacturing quotas (EU Circular Economy)

- 4.3 Market Restraints

- 4.3.1 Volatile nickel-steel prices

- 4.3.2 Rapid penetration of all-electric actuators

- 4.3.3 Cyber-security risks in smart pumps

- 4.3.4 Shortage of certified fluid-power technicians

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Pump Type

- 5.1.1 Gear

- 5.1.2 Vane

- 5.1.3 Piston

- 5.1.4 Screw

- 5.2 By Operating-Pressure Range

- 5.2.1 <3,000 psi

- 5.2.2 3,000 - 5,000 psi

- 5.2.3 >5,000 psi

- 5.3 By End-user Vertical

- 5.3.1 Construction

- 5.3.2 Oil and Gas

- 5.3.3 Power Generation

- 5.3.4 Food and Beverage

- 5.3.5 Water and Waste-water

- 5.3.6 Chemicals

- 5.3.7 Others (Agriculture, Mining, Automotive)

- 5.4 By Application

- 5.4.1 Mobile Hydraulics

- 5.4.2 Industrial Machinery

- 5.4.3 Process and Energy (incl. wind, hydro, hydrogen)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bosch Rexroth AG

- 6.4.2 Eaton Corporation plc

- 6.4.3 Danfoss Power Solutions A/S

- 6.4.4 Enerpac Tool Group Corp.

- 6.4.5 Linde Hydraulics GmbH and Co. KG

- 6.4.6 Dynamatic Technologies Limited

- 6.4.7 HYDAC International GmbH

- 6.4.8 Parker Hannifin Corporation

- 6.4.9 Kawasaki Heavy Industries Ltd.

- 6.4.10 Daikin Industries Ltd.

- 6.4.11 Bucher Hydraulics GmbH

- 6.4.12 KYB Corporation

- 6.4.13 Shimadzu Corporation

- 6.4.14 Permco Inc.

- 6.4.15 Casappa S.p.A.

- 6.4.16 Ningbo Baichi Hydraulic

- 6.4.17 HAWE Hydraulik SE

- 6.4.18 Sun Hydraulics LLC

- 6.4.19 Bosch Mahle Turbosystems Hydraulic (BMT)

- 6.4.20 Bosch Rexroth India Pvt Ltd (regional)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

液壓泵市場:按泵浦類型、排氣量類型、額定壓力和最終用途產業分類-2026-2032年全球市場預測

液壓泵市場:按泵浦類型、排氣量類型、額定壓力和最終用途產業分類-2026-2032年全球市場預測 液壓幫浦市場:策略性洞察與預測(2026-2031年)

液壓幫浦市場:策略性洞察與預測(2026-2031年) 日本液壓泵市場規模、佔有率、趨勢和預測:按產品類型、壓力範圍、應用、最終用戶和地區分類,2026-2034年

日本液壓泵市場規模、佔有率、趨勢和預測:按產品類型、壓力範圍、應用、最終用戶和地區分類,2026-2034年 2026年全球液壓幫浦市場報告

2026年全球液壓幫浦市場報告 液壓泵市場規模、佔有率和成長分析(按類型、壓力範圍、控制方式、應用、最終用途和地區分類)-2026-2033年產業預測

液壓泵市場規模、佔有率和成長分析(按類型、壓力範圍、控制方式、應用、最終用途和地區分類)-2026-2033年產業預測 亞太地區火箭電動幫浦市場:按最終用戶、火箭等級、幫浦類型和國家分類的分析與預測(2025-2035)

亞太地區火箭電動幫浦市場:按最終用戶、火箭等級、幫浦類型和國家分類的分析與預測(2025-2035) 歐洲電動火箭幫浦市場按最終用戶、火箭等級、幫浦和國家分類-分析與預測(2025-2035年)

歐洲電動火箭幫浦市場按最終用戶、火箭等級、幫浦和國家分類-分析與預測(2025-2035年) 火箭電動幫浦市場 - 全球與區域分析:按最終用戶、火箭類別、幫浦類型和國家的分析和預測(2025-2035年)

火箭電動幫浦市場 - 全球與區域分析:按最終用戶、火箭類別、幫浦類型和國家的分析和預測(2025-2035年) 2032 年全球液壓幫浦市場預測(依產品類型、壓力範圍、排氣量類型、控制類型、動力來源、應用和地區)

2032 年全球液壓幫浦市場預測(依產品類型、壓力範圍、排氣量類型、控制類型、動力來源、應用和地區) 全球液壓幫浦市場:市場規模、佔有率、趨勢分析(按類型、工作壓力、最終用途和地區)、細分市場預測(2025-2030 年)

全球液壓幫浦市場:市場規模、佔有率、趨勢分析(按類型、工作壓力、最終用途和地區)、細分市場預測(2025-2030 年)