|

市場調查報告書

商品編碼

1851587

情境感知計算:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Context Aware Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

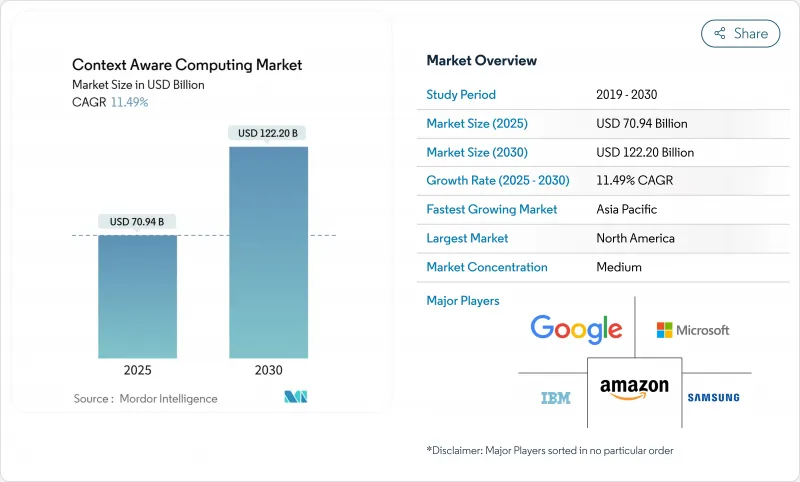

預計到 2025 年,情境感知計算市場規模將達到 709.4 億美元,到 2030 年將達到 1,222 億美元,年複合成長率為 11.49%。

這種前景反映了數位體驗從被動響應式向預測式、意圖驅動型服務的根本性轉變,後者能夠在用戶明確輸入之前就預判其需求。人工智慧推理引擎的廣泛部署、邊緣硬體成本的下降以及5G在全國範圍內的普及,使得跨越數十億個終端進行即時情境分析成為可能。企業對高度個人化的互動、營運效率以及以隱私為先的架構(確保敏感資料在地化)的需求日益成長。儘管硬體仍然是收入的主要驅動力,但軟體編配層正成為情境感知市場競爭優勢的主要來源。

全球情境感知計算市場趨勢與洞察

人工智慧驅動的意圖預測可提升使用者體驗。

智慧型手機、汽車和零售終端內建的大規模語言模型和機器學習管道能夠預測使用者目標,並提案下一步或自動執行任務。 Apple Intelligence 分析裝置內的行為、周圍環境和通訊風格,從而產生提示並自動執行工作流程。部署類似模型的公司由於其直覺且便利的使用者體驗,用戶留存率更高。隨著每次互動不斷完善模型並增強網路效應,其價值迅速成長。人工智慧基礎設施的資本投資正呈指數級成長, Oracle和 OpenAI 斥資 300 億美元合作開發高密度 GPU叢集便是最好的例證。隨著預測準確度的提高,消費者將越來越期望現役成為情境感知運算市場的基礎功能。

邊緣運算成本下降推動了其普及。

領先的 3nm 和 4nm 製程節點降低了每兆次運算的成本,並提高了每瓦效能。高通最新的驍龍平台整合了專用 NPU,支援在電池供電設備上進行多模態情境分析,因此無需持續連接雲端。更低的整體擁有成本使得中小企業能夠輕鬆部署,例如智慧零售貨架、工廠自動化和現場服務穿戴式裝置。不斷擴大的市場規模將加速感測器和閘道器的出貨,從而增強產業情境感知運算的需求。

以隱私為先的法規限制了資料的使用。

GDPR式的強制規定要求用戶明確同意、資料最小化以及擁有刪除權,這遏制了行動應用中曾經普遍存在的無限資料收集。為了合規,企業目前正在尋求聯邦學習、差分隱私和本地推理等技術,但這些技術往往會降低模型精度並延緩部署速度。能夠提供隱私設計框架的供應商可以獲得信任優勢,但必須承擔更高的工程成本。監管的影響使一些公司變得謹慎,限制了情境感知計算市場近期的成長。

細分市場分析

到2024年,硬體將佔總收入的52%,這主要得益於支援推理工作負載的感測器、邊緣閘道器和智慧穿戴裝置。運動感測器、生物辨識感測器和環境感測器是最大的細分市場。閘道器聚合這些輸入並執行初步分析,從而縮短情境感知運算市場的回饋週期。同時,軟體的成長速度將超過硬體,到2030年將以13.20%的複合年成長率成長。情境管理中介軟體協調不同的資料流,分析引擎將原始訊號轉換為預測性建議。專業服務收入反映了企業在協調資料管道、安全性和合規性方面所面臨的陡峭學習曲線。隨著企業將日常營運外包以專注於業務邏輯,託管服務的採用率正在不斷提高。

如今,軟體驅動著終端用戶價值的創造。中間件供應商將模式映射、身分解析和策略執行等功能捆綁在一起,使平台選擇成為一項策略決策。人工智慧推理庫透過將工作負載分配到 CPU、GPU 和 NPU 資源上來最佳化功耗。這些技術突破使開發人員能夠創建精細化的體驗,例如自適應車載資訊娛樂系統,而無需為每個晶片組重寫程式碼。這將促進上游感測器和閘道器的出貨量,從而擴大整合解決方案的情境感知運算市場規模。

區域分析

2024年,北美將佔全球營收的39%,這主要得益於強勁的創投、5G的早期部署以及雲端運算的普及。美國企業正在開發以情境為基礎的客戶旅程,以提高客戶留存率和交叉銷售率。在加拿大,公共部門的數位化策略將推動對以隱私為先的部署方案的需求。

預計到2030年,亞太地區將以14.80%的複合年成長率實現最高成長。各國5G普及率、設備製造地以及數位原民人口規模將推動情境感知計算市場的發展。中國25.7億個物聯網終端機展現了本地生態系參與者可取得的豐富情境數據。政府對智慧城市、醫療健康和產業升級計劃的獎勵策略將進一步加速情境感知運算的普及。

歐洲正以差異化的優先事項推動發展,力求在創新與嚴格的隱私合規之間取得平衡。整合用戶授權管理和資料本地化的供應商正在贏得企業合約。中東地區正利用沙烏地阿拉伯的NEOM等智慧城市計劃,試驗大規模情境感知平台。在非洲,雲端原生行動服務展現出巨大的潛力,即使在傳統基礎設施匱乏的地區,它們也能提供切實可行的解決方案。南美洲的智慧型手機普及率正在穩定成長,通訊業者正大力推廣邊緣運算節點,以支援低延遲的情境感知應用。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 人工智慧驅動的意圖預測可提升使用者體驗。

- 邊緣運算成本下降推動了其普及。

- 5G的部署實現了即時情境數據。

- 物聯網終端的激增造成了資料洪流。

- 車載資訊娛樂系統個人化需求

- 面向小型企業應用的上下文即服務 API

- 市場限制

- 以隱私為先的法規限制了資料的使用。

- 與傳統IT系統高度整合複雜

- 情境推論中模型偏差的風險

- 穿戴式裝置的電池續航力有限。

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 硬體

- 感應器

- 邊緣閘道器

- 智慧型穿戴裝置

- 軟體

- 內容管理中介軟體

- 分析與推理引擎

- 服務

- 專業服務

- 託管服務

- 硬體

- 按供應商

- 設備製造商

- 行動網路營運商

- 線上社交平臺

- 獨立軟體供應商

- 按最終用戶行業分類

- BFSI

- 消費性電子產品

- 媒體與娛樂

- 車

- 衛生保健

- 電訊

- 物流/運輸

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Google LLC(Alphabet)

- Oracle Corporation

- Amazon Web Services Inc.

- Verizon Communications Inc.

- Samsung Electronics Co. Ltd.

- Intel Corporation

- Apple Inc.

- Qualcomm Inc.

- Ericsson AB

- Huawei Technologies Co. Ltd.

- Bosch Sensortec GmbH(Robert Bosch GmbH)

- Honeywell International Inc.

- SAP SE

- ATandT Inc.

- Telefonica SA

- LG Electronics Inc.

- Baidu Inc.

第7章 市場機會與未來展望

The context-aware computing market size is valued at USD 70.94 billion in 2025 and is forecast to reach USD 122.20 billion by 2030, advancing at an 11.49% CAGR.

This outlook reflects the structural shift from reactive digital experiences toward predictive, intent-driven services that anticipate a user's needs before explicit input. Widespread deployment of AI inference engines, falling edge hardware costs, and nationwide 5G coverage now permit real-time contextual analytics on billions of endpoints. Demand intensifies as enterprises seek hyper-personalised engagement, operational efficiency, and privacy-first architectures that keep sensitive data local. Hardware remains the revenue backbone, yet software orchestration layers are becoming the main source of competitive differentiation in the context aware computing market.

Global Context Aware Computing Market Trends and Insights

AI-powered Intent Prediction Boosts UX

Large language models and machine-learning pipelines embedded in smartphones, vehicles, and retail kiosks now anticipate user goals, suggesting next actions or auto-completing tasks. Apple Intelligence analyses in-device behaviour, ambient conditions, and messaging style to curate prompts and automate workflows. Organisations deploying comparable models gain higher user retention because experiences feel intuitive and effortless. Value scales rapidly because each interaction refines the model, reinforcing network effects. Capital expenditure on AI infrastructure is rising sharply, evidenced by Oracle's USD 30 billion partnership with OpenAI focused on high-density GPU clusters. As predictive accuracy improves, consumers increasingly expect proactive services as a baseline capability in the context aware computing market.

Edge-computing Cost Decline Widens Adoption

Advanced 3 nm and 4 nm process nodes have reduced cost per tera-ops and improved performance-per-watt. Qualcomm's latest Snapdragon platform embeds a dedicated NPU that supports multimodal context analysis on battery-powered devices, eliminating constant cloud calls. Lower total ownership cost unlocks small and medium-enterprise deployment across smart retail shelving, factory automation, and field-service wearables. This broadening addressable base accelerates unit shipments of sensors and gateways, reinforcing demand in the context aware computing industry.

Privacy-first Regulations Restrict Data Use

GDPR-style mandates require explicit consent, data minimisation, and erasure rights that curtail the unfettered data harvesting once common in mobile applications. Firms now pursue federated learning, differential privacy, and on-premises inference to comply, but these techniques often reduce model accuracy and slow roll-outs. Vendors able to deliver privacy-by-design frameworks gain a trust advantage yet must absorb higher engineering costs. The regulatory swing keeps some enterprises cautious, tempering the near-term growth of the context aware computing market.

Other drivers and restraints analyzed in the detailed report include:

- 5G Rollout Enables Real-time Context Data

- Surge in IoT Endpoints Creates Data Deluge

- High Integration Complexity with Legacy IT

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 52% revenue share in 2024 on the strength of sensors, edge gateways, and smart wearables that underpin inference workloads. Sensors for motion, biometrics, and environment represent the largest line-item because every contextual decision starts with precise data capture. Gateways aggregate this input and run first-pass analytics, shortening feedback loops in the context aware computing market. Meanwhile, software outpaces hardware growth at 13.20% CAGR through 2030. Context management middleware harmonises disparate streams, while analytics engines transform raw signals into predictive recommendations. Professional services revenue reflects the steep learning curve enterprises face when tuning data pipelines, security, and compliance. Managed services adoption rises as firms outsource daily operations to focus on business logic.

Software now determines end-user value creation. Middleware vendors bundle schema mapping, identity resolution, and policy enforcement, turning platform choice into a strategic decision. AI inference libraries optimise power draw by splitting workloads across CPU, GPU, and NPU resources. These technical breakthroughs let developers craft granular experiences-such as adaptive in-car infotainment-without rewriting code for every chipset. Resulting demand reinforces upstream sensor and gateway shipments, advancing the context aware computing market size for integrated solutions.

The Context Aware Computing Market is Segmented by Type (Hardware, Software), Vendor (Device Manufacturers, Mobile Network Operators, and More), End-User Industry (BFSI, Consumer Electronics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Size and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 39% of global revenue in 2024, buoyed by robust venture investment, early 5G rollout, and cloud adoption. Enterprises in the United States deploy context-rich customer journeys to lift retention and cross-sell rates. Canada's public-sector digital strategies add to base demand for privacy-centric deployments.

Asia-Pacific records the highest growth trajectory at 14.80% CAGR through 2030. National 5G coverage, device manufacturing hubs, and sizeable digital-native populations combine to expand the context aware computing market. China's 2.57 billion IoT endpoints demonstrate the depth of contextual data available to local ecosystem players. Government stimulus for smart city, healthcare, and industrial upgrade projects further accelerates uptake.

Europe advances on differentiated priorities, balancing innovation with strict privacy law compliance. Vendors that integrate consent management and data localisation win enterprise contracts. The Middle East leverages smart-city megaprojects-such as NEOM in Saudi Arabia-to trial large-scale context platforms. Africa shows leapfrog potential because cloud-native mobile services offer practical solutions where legacy infrastructure is thin. South America's steady smartphone adoption rounds out global demand, with telcos pushing edge computing nodes to support low-latency contextual apps.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Google LLC (Alphabet)

- Oracle Corporation

- Amazon Web Services Inc.

- Verizon Communications Inc.

- Samsung Electronics Co. Ltd.

- Intel Corporation

- Apple Inc.

- Qualcomm Inc.

- Ericsson AB

- Huawei Technologies Co. Ltd.

- Bosch Sensortec GmbH (Robert Bosch GmbH)

- Honeywell International Inc.

- SAP SE

- ATandT Inc.

- Telefonica S.A.

- LG Electronics Inc.

- Baidu Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-powered intent prediction boosts UX

- 4.2.2 Edge-computing cost decline widens adoption

- 4.2.3 5G rollout enables real-time context data

- 4.2.4 Surge in IoT endpoints creates data deluge

- 4.2.5 In-car infotainment personalisation demand

- 4.2.6 Context-as-a-Service APIs for SME apps

- 4.3 Market Restraints

- 4.3.1 Privacy-first regulations restrict data use

- 4.3.2 High integration complexity with legacy IT

- 4.3.3 Model bias risks in context inference

- 4.3.4 Limited battery life on wearable devices

- 4.4 Industry Value-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 Sensors

- 5.1.1.2 Edge Gateways

- 5.1.1.3 Smart Wearables

- 5.1.2 Software

- 5.1.2.1 Context Management Middleware

- 5.1.2.2 Analytics and Inference Engines

- 5.1.3 Services

- 5.1.3.1 Professional Services

- 5.1.3.2 Managed Services

- 5.1.1 Hardware

- 5.2 By Vendor

- 5.2.1 Device Manufacturers

- 5.2.2 Mobile Network Operators

- 5.2.3 Online and Social Platforms

- 5.2.4 Independent Software Vendors

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Consumer Electronics

- 5.3.3 Media and Entertainment

- 5.3.4 Automotive

- 5.3.5 Healthcare

- 5.3.6 Telecommunication

- 5.3.7 Logistics and Transportation

- 5.3.8 Other Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Google LLC (Alphabet)

- 6.4.5 Oracle Corporation

- 6.4.6 Amazon Web Services Inc.

- 6.4.7 Verizon Communications Inc.

- 6.4.8 Samsung Electronics Co. Ltd.

- 6.4.9 Intel Corporation

- 6.4.10 Apple Inc.

- 6.4.11 Qualcomm Inc.

- 6.4.12 Ericsson AB

- 6.4.13 Huawei Technologies Co. Ltd.

- 6.4.14 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 6.4.15 Honeywell International Inc.

- 6.4.16 SAP SE

- 6.4.17 ATandT Inc.

- 6.4.18 Telefonica S.A.

- 6.4.19 LG Electronics Inc.

- 6.4.20 Baidu Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

情境感知計算市場規模、佔有率、趨勢和預測:按產品類型、供應商類型、情境類型、網路類型、產業垂直領域和地區分類(2026-2034 年)

情境感知計算市場規模、佔有率、趨勢和預測:按產品類型、供應商類型、情境類型、網路類型、產業垂直領域和地區分類(2026-2034 年) 全球情境感知計算市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球情境感知計算市場規模、佔有率、趨勢和成長分析報告(2026-2034) 情境感知計算市場:按組件、技術、最終用戶和地區分類

情境感知計算市場:按組件、技術、最終用戶和地區分類 情境感知計算市場:按組件、技術、產業、應用和最終用戶分類 - 2026-2032 年全球預測

情境感知計算市場:按組件、技術、產業、應用和最終用戶分類 - 2026-2032 年全球預測 2026年全球情境感知計算市場報告情境感知計算市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

2026年全球情境感知計算市場報告情境感知計算市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 情境感知計算市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類

情境感知計算市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類 到 2030 年的情境感知計算市場預測:按產品類型、組件、網路類型、情境類型、最終用戶和地區進行的全球分析

到 2030 年的情境感知計算市場預測:按產品類型、組件、網路類型、情境類型、最終用戶和地區進行的全球分析