|

市場調查報告書

商品編碼

1851583

阻變式隨機存取記憶體(ReRAM):市場佔有率分析、產業趨勢、統計資料和成長預測(2025-2030 年)Resistive RAM - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

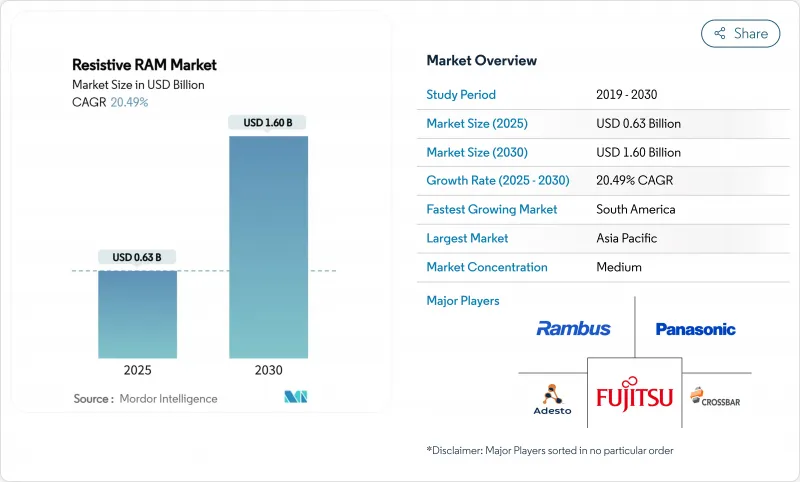

預計到 2025 年,電阻式隨機存取記憶體 (ReRAM) 市場規模將達到 6.3 億美元,到 2030 年將達到 16 億美元,2025 年至 2030 年的複合年成長率為 20.49%。

這種快速成長是由多種因素所驅動的。超過 10¹² 次循環的生產級耐久性解鎖了關鍵任務型、寫入密集型工作負載,而低於 1V 的開關電壓則為電池供電的邊緣設備提供了餘量。亞太地區的晶圓代工基地加速了 28nm 及以下製程嵌入式 ReRAM 的流片,而汽車 ADAS 專案則推動了對傳統快閃記憶體無法滿足的高溫非揮發性解決方案的需求。此外,對神經型態計算新興企業的資金籌措創業投資勢頭強勁。這些趨勢表明,ReRAM 正從實驗室概念驗證走向主流量產應用階段。

全球電阻式隨機存取記憶體(ReRAM)市場趨勢與洞察

突破性耐久性,超過 1012 次循環

ReRAM 的耐久性超過 10¹² 次循環,使其成為寫入密集型企業工作負載中快閃記憶體的可行替代方案。學術團隊已報導,鋁-氮化鐵電堆疊結構在保持極化狀態的同時,可承受高達 10¹° 的循環次數。隨後,WeeBit Nano 在汽車級測試中檢驗了其在 150 度C下可承受 10 萬次編程循環。這種耐久性使得儲存廠商可以考慮將 ReRAM 用於熱層快取,而傳統上,DRAM 一直是熱層快取的預設選擇。

超低功耗邊緣裝置的低於1V開關

維吉尼亞大學的研究表明,0.6V 導電橋 ReRAM 巨集可以消除電荷泵開銷,每次寫入僅消耗 8pJ 的能量。英特爾已在 22FFL 節點上展示了基於 FinFET 的嵌入式 ReRAM,其工作電壓低於 1V。提高電池續航時間對於穿戴式裝置、感測器節點和智慧電錶至關重要。

細絲變化導致寫入雜訊和位元錯誤

在高可靠性製造過程中,導電路徑的變異性會降低產量比率。在Ta2O5裝置研究中,電壓相關的雜訊會導致神經陣列的重力解析度劣化。交叉陣列尺度的熱相互作用會增加不確定性。 Al2O3疊層的喚醒增值回收可以緩解這個問題,但代價是延長了製程。

細分市場分析

2024年,氧化物基元件在電阻式隨機存取記憶體(RRAM)市場中佔據46.3%的佔有率。 HfO2和Al2O3疊層結構已整合到主流CMOS製程中,降低了採用風險。銅基導電橋可在低於1V的電壓下寫入,適用於穿戴式裝置和微功耗節點,其複合年成長率(CAGR)達到26.2%。預計到2030年,導電橋裝置的RRAM市場規模將達到4.9億美元。奈米金屬絲技術滿足了對極緻小型化和高抗輻射性能的特定需求。混合碳纖維絲在37nm製程下實現了超過10⁷次的無成型循環操作。

基於氧化物的供應商透過採用空隙加工層來提高耐用性,從而減少週期間差異。代工廠庫現在將基於氧化物的ReRAM巨集與邏輯IP捆綁在一起,以簡化MCU流片。另一方面,導電橋的支持者則利用較低的編程電流來延長電池壽命。雙方都投資於神經網路模擬權重儲存演示,以利用AI加速器。

到2024年,嵌入式解決方案將佔總收入的55.4%,因為晶片系統設計人員晶粒晶片面積的節省和材料清單清單的簡化。 MCU供應商已整合1-4Mbit宏,用於安全代碼儲存、韌體更新和即時啟動功能。即使獨立式記憶體的密度不斷提高,到2030年,電阻式隨機存取記憶體(ReRAM)在嵌入式裝置中的市佔率預計仍將維持在50%以上。

由於人工智慧和高效能運算 (HPC) 客戶對客製化記憶體模組的需求,獨立式 ReRAM 的複合年成長率 (CAGR) 預計為 25.2%。設計人員可以調整陣列幾何結構和選擇器堆疊,而無需考慮邏輯約束,從而實現更大的字線,以進行並行模擬乘法和累加運算。一款 4Mbit、8 位元精度的記憶體運算巨集晶片展示了在微焦耳能量水平下進行推理的能力。雲端供應商已將這款獨立晶片評估為 DRAM 快取的補充,用於那些受益於動態權重更新的訓練工作負載。

電阻式隨機存取記憶體 (ReRAM)材料類型(氧化物基、導電橋、奈米金屬絲)、外形尺寸(嵌入式 ReRAM、獨立式 ReRAM)、應用(記憶體內運算、持久存儲、快速啟動/代碼存儲)、最終用戶(工業和物聯網設備、汽車和移動出行、其他)以及地區(北美、南美、歐洲、亞太地區、中東和非洲)進行細分。

區域分析

亞太地區將在2024年佔據41.3%的營收佔有率。三星、SK海力士和鎧俠等公司的大規模晶圓代工投資將推動28奈米以下嵌入式ReRAM設計套件的普及。韓國已撥款750億美元用於先進記憶體產能建設,投資範圍涵蓋高頻寬和下一代非揮發性記憶體(NVM)生產線,投資期至2028年。日本正大力推進其670億美元的半導體復興計劃,其中ReRAM將應用於人工智慧邊緣設備。

南美洲成為成長最快的產業集群,複合年成長率高達22.2%。巴西向阿提拜亞和馬瑙斯兩地提供了6.5億雷亞爾(約1.3億美元)的擴建資金,用於實現針對ReRAM和DRAM封裝的本地化封裝和測試。該地區政府還增加了用於氧化膜的稀土礦物供應。因此,南美洲電阻式隨機存取記憶體市場受益於垂直整合。

北美保持了其設計主導,這得益於汽車和航太航太領域對抗輻射加固的需求。隨著ADAS(高級駕駛輔助系統)記憶體組合的轉變,美國和加拿大的電阻式隨機存取記憶體(RRAM)市場規模預計將會成長。歐洲的工業控制供應商對整合記憶體計算宏以實現即時分析的關注度顯著提升。中東和非洲地區率先採用了低功耗持久性記憶體,用於建立智慧城市感測器網路,從而縮短了維護週期。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 革命性的耐久性提升,循環次數超過1012次

- 低於 1V 的開關特性可實現超低功耗邊緣元件

- 28nm以下嵌入式ReRAM的代工廠支持

- 汽車ADAS對高溫非揮發性記憶體的需求

- 資金籌措湧入神經形態計算新興企業

- 市場限制

- 細絲變化導致寫入雜訊和位元錯誤

- 除了少數授權方之外,智慧財產權/專有技術非常有限。

- 與 3D NAND BEOL 堆疊整合是一項挑戰

- 宏觀經濟因素的影響

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依材料類型

- 基於氧化物的(OxRRAM)

- 導電橋(CBRAM)

- 奈米金屬絲

- 按外形規格

- 嵌入式ReRAM

- 獨立 ReRAM

- 透過使用

- 記憶體內運算

- 持久性儲存

- 快速啟動/代碼存儲

- 最終用戶

- 工業和物聯網設備

- 汽車與出行

- 資料中心與企業級固態硬碟

- 穿戴式裝置和消費性電子產品

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 南美洲其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 台灣

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Crossbar Inc.

- Weebit Nano Ltd.

- 4DS Memory Limited

- Fujitsu Semiconductor Memory Solution Ltd.

- Xinyuan Semiconductor(Shanghai)Co., Ltd.

- Dialog Semiconductor Ltd.(Renesas)

- Panasonic Holdings Corp.

- Sony Semiconductor Solutions Corp.

- Micron Technology Inc.

- Intel Corporation

- IBM Corporation

- Western Digital Technologies, Inc.

- SK hynix Inc.

- Samsung Electronics Co., Ltd.

- TDK Corporation

- Infineon Technologies AG

- Renesas Electronics Corp.

- SMIC

- TetraMem Inc.

- ReRam Nanotech Ltd.

- Adesto Technologies Corp.(Dialog)

- Avalanche Technology Inc.

- RRAMTech Srl

- CEA-Leti

- GigaDevice Semiconductor Inc.

第7章 市場機會與未來展望

The resistive random access memory market size stood at USD 0.63 billion in 2025 and is forecast to reach USD 1.60 billion by 2030, expanding at a 20.49% CAGR over 2025-2030.

Multiple factors drove this steep climb. Production-grade endurance above 1012 cycles unlocked mission-critical and high-write-frequency workloads, while sub-1V switching created headroom for battery-powered edge devices. Asia-Pacific's deep foundry base accelerated embedded ReRAM tape-outs below 28 nm, and automotive ADAS programs raised demand for high-temperature non-volatile options that conventional flash could not meet. Venture capital funding for neuromorphic compute start-ups also added momentum. Together, these trends signaled that ReRAM was moving from laboratory proof-of-concept to mainstream volume adoption.

Global Resistive RAM Market Trends and Insights

Breakthrough endurance beyond 1012 cycles

Endurance exceeding 1012 cycles positioned ReRAM as a realistic flash replacement for write-intensive enterprise workloads. Academic teams reported aluminum-scandium nitride ferroelectric stacks persisting through 101° cycles while retaining polarization.Weebit Nano later validated 100,000 program cycles at 150 °C during automotive tests. This durability lets storage vendors contemplate using ReRAM for hot-tier caching that had previously defaulted to DRAM.

Sub-1 V switching for ultra-low-power edge devices

Research from the University of Virginia showed a 0.6 V conductive-bridge ReRAM macro consuming 8 pJ per write, eliminating charge-pump overhead. Intel echoed the feasibility of sub-1V operation when it demonstrated FinFET-based embedded ReRAM on 22FFL nodes. Battery life gains mattered across wearables, sensor nodes, and smart meters.

Filament variability causing write-noise and bit-error

Variability in conductive paths hampered yield during high-reliability production. Studies on Ta2O5 devices linked voltage-dependent noise to degraded weight resolution in neural arrays. Crossbar-scale thermal interactions added uncertainty. Wake-up cycling in Al2O3 stacks offered mitigation but lengthened process flows.

Other drivers and restraints analyzed in the detailed report include:

- Foundry support for embedded ReRAM at 28 nm and below

- Automotive ADAS demand for high-temperature NVM

- Limited IP and know-how outside a few licensors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oxide-based devices retained 46.3% share of the resistive random access memory market in 2024. HfO2 and Al2O3 stacks were already part of mainstream CMOS flows, which lowered adoption risk. Conductive-bridge variants, often copper-based, registered a 26.2% CAGR outlook because their sub-1V write capability aligned with wearables and micro-power nodes. The resistive random access memory market size for conductive-bridge devices is projected to reach USD 0.49 billion by 2030, reflecting designers' preference for energy headroom in edge architectures. Nanometal filament approaches captured niche demand where extreme miniaturization or high radiation tolerance mattered. Hybrid carbon filaments demonstrated forming-free operation at 37 nm with >107 cycles.

Oxide-based suppliers responded by enhancing endurance through vacancy-engineered layers that reduced cycle-to-cycle variability. Foundry libraries now bundle oxide-based ReRAM macros alongside logic IP, simplifying MCU tape-outs. Conversely, conductive-bridge proponents leveraged lower programming currents to market battery-life gains. Both camps invested in neural-network analog weight storage demonstrations to tap AI accelerators.

Embedded solutions held 55.4% of revenue in 2024 because system-on-chip designers valued die-space savings and simplified bills of materials. MCU vendors embedded 1-4 Mbit macros for secure code storage, firmware updates, and instant-on features. The resistive random access memory market share of embedded devices is expected to remain above 50% through 2030, even as stand-alone density rises.

Stand-alone ReRAM recorded a 25.2% CAGR projection as AI and HPC customers sought bespoke memory modules. Designers could tune array geometry and selector stacks without logic constraints, enabling larger word lines for parallel analog multiply-accumulate. A 4 Mbit compute-in-memory macro with 8-bit precision demonstrated inference at micro-joule energy levels. Cloud vendors evaluated these stand-alone chips as DRAM cache complements for training workloads that benefit from in-situ weight updates.

Resistive Random Access Memory (ReRAM) is Segmented by Material Type (Oxide-Based, Conductive-Bridge, and Nanometal Filament), Form Factor (Embedded ReRAM, and Stand-Alone ReRAM), Application (In-Memory Computing, Persistent Storage, and Fast Boot/Code Storage), End-User (Industrial and IoT Devices, Automotive and Mobility, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific commanded 41.3% revenue in 2024. Massive foundry investments by Samsung, SK Hynix, and Kioxia expanded embedded ReRAM design kits below 28 nm. South Korea allocated USD 75 billion for advanced memory capacity through 2028, funneling funds into high-bandwidth and next-generation NVM lines. Japan pursued a USD 67 billion semiconductor renaissance plan with ReRAM earmarked for AI edge devices.

South America emerged as the fastest-growing cluster, posting 22.2% CAGR. Brazil funded a R$650 million (USD 130 million) expansion in Atibaia and Manaus to localize encapsulation and test, targeting both ReRAM and DRAM packaging. Regional governments also facilitated the rare-earth mineral supply for oxide films. The resistive random access memory market in South America, therefore, benefited from vertical integration incentives.

North America retained design leadership, leveraging automotive and aerospace use cases that demand radiation hardening. The resistive random access memory market size for the US and Canada is forecast to climb alongside ADAS memory mix shifts. Europe focused on industrial control vendors integrating compute-in-memory macros for real-time analytics. The Middle East and Africa saw early traction in smart-city sensor grids where low-power persistent memory reduced maintenance cycles.

- Crossbar Inc.

- Weebit Nano Ltd.

- 4DS Memory Limited

- Fujitsu Semiconductor Memory Solution Ltd.

- Xinyuan Semiconductor (Shanghai) Co., Ltd.

- Dialog Semiconductor Ltd. (Renesas)

- Panasonic Holdings Corp.

- Sony Semiconductor Solutions Corp.

- Micron Technology Inc.

- Intel Corporation

- IBM Corporation

- Western Digital Technologies, Inc.

- SK hynix Inc.

- Samsung Electronics Co., Ltd.

- TDK Corporation

- Infineon Technologies AG

- Renesas Electronics Corp.

- SMIC

- TetraMem Inc.

- ReRam Nanotech Ltd.

- Adesto Technologies Corp. (Dialog)

- Avalanche Technology Inc.

- RRAMTech S.r.l.

- CEA-Leti

- GigaDevice Semiconductor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Break-through endurance improvements beyond 1012 cycles

- 4.2.2 Sub-1 V switching enabling ultra-low-power edge devices

- 4.2.3 Foundry support for embedded ReRAM at 28 nm and below

- 4.2.4 Automotive ADAS demand for high-temperature NVM

- 4.2.5 VC funding surge in neuromorphic compute start-ups

- 4.3 Market Restraints

- 4.3.1 Filament variability causing write-noise and bit-error

- 4.3.2 Limited IP/know-how outside a handful of licensors

- 4.3.3 Challenging integration with 3D NAND BEOL stacks

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Oxide-based (OxRRAM)

- 5.1.2 Conductive-Bridge (CBRAM)

- 5.1.3 Nanometal Filament

- 5.2 By Form Factor

- 5.2.1 Embedded ReRAM

- 5.2.2 Stand-alone ReRAM

- 5.3 By Application

- 5.3.1 In-Memory Computing

- 5.3.2 Persistent Storage

- 5.3.3 Fast Boot / Code Storage

- 5.4 By End-user

- 5.4.1 Industrial and IoT Devices

- 5.4.2 Automotive and Mobility

- 5.4.3 Datacentres and Enterprise SSD

- 5.4.4 Wearables and Consumer Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Taiwan

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Crossbar Inc.

- 6.4.2 Weebit Nano Ltd.

- 6.4.3 4DS Memory Limited

- 6.4.4 Fujitsu Semiconductor Memory Solution Ltd.

- 6.4.5 Xinyuan Semiconductor (Shanghai) Co., Ltd.

- 6.4.6 Dialog Semiconductor Ltd. (Renesas)

- 6.4.7 Panasonic Holdings Corp.

- 6.4.8 Sony Semiconductor Solutions Corp.

- 6.4.9 Micron Technology Inc.

- 6.4.10 Intel Corporation

- 6.4.11 IBM Corporation

- 6.4.12 Western Digital Technologies, Inc.

- 6.4.13 SK hynix Inc.

- 6.4.14 Samsung Electronics Co., Ltd.

- 6.4.15 TDK Corporation

- 6.4.16 Infineon Technologies AG

- 6.4.17 Renesas Electronics Corp.

- 6.4.18 SMIC

- 6.4.19 TetraMem Inc.

- 6.4.20 ReRam Nanotech Ltd.

- 6.4.21 Adesto Technologies Corp. (Dialog)

- 6.4.22 Avalanche Technology Inc.

- 6.4.23 RRAMTech S.r.l.

- 6.4.24 CEA-Leti

- 6.4.25 GigaDevice Semiconductor Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment