|

市場調查報告書

商品編碼

1851565

輸送機:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Conveyors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

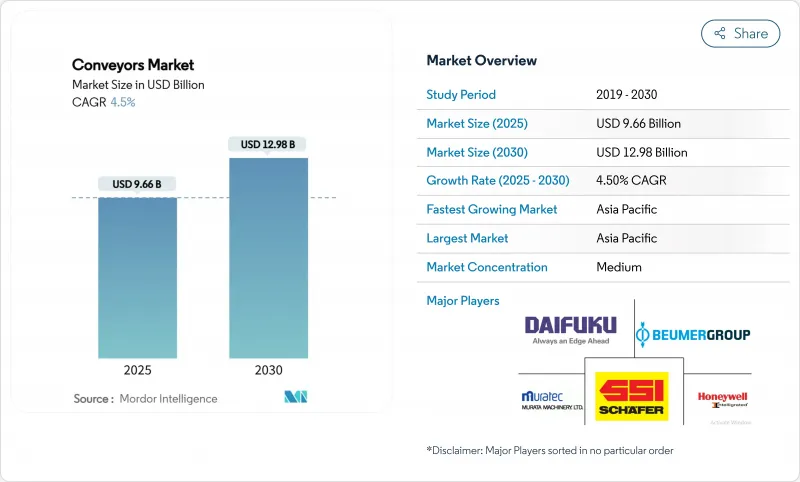

預計到 2025 年,輸送機市場規模將達到 96.6 億美元,到 2030 年將達到 129.8 億美元,預測期(2025-2030 年)複合年成長率為 4.5%。

這一前景受到電子商務快速成長、工業4.0投資以及對能源效率追求的推動,這些因素共同促成了再生驅動技術的應用,該技術在下坡工況下可降低37%至39%的能耗。亞太地區的需求領先,而中東地區則運作大型物流園區的投產而實現了最快的成長。儘管傳送帶技術仍保持較高的裝機量,但隨著工廠尋求減少占地面積,架空式設計正以最快的速度擴張。軟體主導的預測性維護已成為成長最強勁的組件領域,可將非計劃性停機時間減少高達30%,並延長資產壽命。同時,中小企業不願在資本支出上投入資金,導致高階升級的步伐放緩,而AGV/AMR的替代也給傳統的固網帶來了額外的壓力。

全球輸送機市場趨勢與洞察

電子商務履約中心快速成長

都市區微型履約中心需要能夠在最小占地面積內,以每小時處理超過7,200個包裹的輸送機平台。亞馬遜位於泰國的Cafe Amazon配送中心展示了模組化的Interroll系統如何能夠每天在4000家門市處理2萬個包裹。高吞吐量的交叉傳送帶分類機能夠兌現當日送達的承諾,而垂直佈局則最大限度地提高了空間受限的亞洲大都市的立方吞吐量。開發商指定使用即插即用的傳送模組,以便在無需土木工程的情況下重新配置設施。這些要求維持了設備的更新週期,並鞏固了傳送系統市場作為最後一公里物流支柱的地位。

食品飲料工廠對自動化處理的需求日益成長

加工商不僅滿足衛生合規要求,更致力於最佳化端到端的生產效率。 Balaji Wafers 透過採用主動式滾筒傳送帶生產線,實現了零計劃外停機,該生產線能夠輕柔地處理產品。配備視覺功能的輸送機可即時檢測缺陷,進而減少人工檢查。 Diversified Foods 的 DirectDrive 螺旋輸送機如今可在高產量零嘴零食包裝生產線上每天 48 小時連續運作,徹底杜絕了以往的機械故障。模組化塑膠傳送帶延長了使用壽命,而新興的植物來源產品線則需要能夠處理不同濕度易碎物品的靈活佈局。

前期投資額高,投資報酬期長

即使內部報酬率達到15%,能量回收驅動裝置也需要六年才能收回成本,這對資金緊張的公司來說是一個不小的挑戰。鋼材價格在每噸870美元至950美元之間波動,也讓預算編制變得更加複雜。雖然租賃模式已經存在,但在信貸市場緊張的地區,其普及速度仍然緩慢。這種成本壓力限制了高階設備在輸送機系統市場的滲透率。

細分市場分析

到2024年,皮帶輸送機將維持39%的市場佔有率,成為採礦、食品和一般製造業生產線的關鍵組成部分。德克薩斯州的Dune Express公司透過皮帶輸送機,每年輸送1300萬噸貨物,全程42英里,減少了2.5萬次卡車運輸,充分證明了皮帶輸送機的優勢。隨著工廠騰出占地面積並提高工人安全,架空式輸送機的市佔率將以8.1%的複合年成長率成長。滾筒輸送系統受惠於適用於可重構組裝的模組化框架,而托盤輸送線則可滿足汽車產業的精密作業需求。在各個領域,智慧感測器將使預測性維護的準確率提升至95%以上。

隨著永續採礦和散裝物流計劃的推進,皮帶輸送機系統市場規模預計將持續擴大。節能型振動設計僅需傳統驅動功率的20%,體現了各領域的技術創新。板條式和鍊式輸送機仍應用於重型車輛生產,但由於市場對更靈活替代方案的需求不斷成長,其發展受到抑制。

到2024年,單元物料搬運的需求將佔總需求的64.3%,這主要得益於電子商務和離散製造工作流程的發展,這些流程強調寬鬆的產品控制和零壓力堆積。配備視覺輔助缺陷檢測系統的分類系統目前已能勝任分類任務,同時提高了安全性。散裝搬運雖然規模較小,但其年複合成長率將超過單元物料搬運,達到8.7%,這主要得益於快速消費品產業的成長和農業現代化。混合型設備的出現模糊了不同物料搬運方式之間的界限,因為工廠需要能夠在托盤和顆粒飼料之間切換的基礎設施。

在採礦業,TAKRAF 的 Collahuasi計劃體現了對大容量輸送能力的需求。製藥無塵室依靠真空輸送機以每小時超過 11,100 公升的速度輸送物料,同時保持無菌環境。這兩個領域為輸送機系統市場提供了多元化的收入來源。

區域分析

到2024年,亞太地區將佔據輸送機系統市場38%的佔有率,這主要得益於中國、印度和東南亞製造群的擴張。DAIFUKU CO. LTD.在印度新建的工廠印證了汽車和電子產業日益成長的本地需求。中國持續在礦業和港口基礎設施中安裝大型散裝輸送帶,而印度將利用SAMARTH Udyog的設施加速智慧工廠的升級改造。半導體產業的投資將帶動無塵室輸送機需求的成長,而日本310英里長的貨運鐵路計畫則凸顯了其雄心勃勃的計劃工程維修目標。

中東地區物流業將以8.9%的複合年成長率成長,並受惠於物流多元化。沙烏地阿拉伯的「2030願景」計畫將投資1,066億美元用於建造奧克薩貢等貨運走廊,這將推動對高容量分揀和港口的需求。阿拉伯聯合大公國的物流市場預計到2025年將達到200.3億美元,將帶動倉儲自動化領域的投資,預計到2025年,該領域的投資將達到16億美元。

北美和歐洲在能源部能源效率津貼和歐盟碳排放法規的推動下,持續推動老舊設備的現代化改造。翻新硬碟的驅動裝置正在迅速普及,尤其是在歐洲,綠色環保政策提高了投資報酬率。南美和非洲的採礦和港口計劃推動了這一成長,但資金限制減緩了以分析為中心的系統的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務履約中心快速成長

- 食品飲料工廠對自動化處理的需求日益成長

- 機場客流量增加促進了行李搬運輸送帶的使用

- 政府對工業4.0現代化的獎勵

- 城市微型履約需要緊湊型模組化輸送機

- 能量再生輸送機驅動裝置支援ESG目標

- 市場限制

- 初始投資額高,投資回收期長

- 改裝整合可能導致生產停機

- 自主移動機器人(AMR)和自動導引車(AGV)作為替代技術正在興起。

- 輸送機控制網路中的OT-IT網路安全漏洞

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 腰帶

- 滾筒

- 調色盤

- 開賣

- 板條/鏈條

- 螺絲和氣壓

- 按載荷類型

- 單位處理量

- 散裝搬運

- 按最終用戶行業分類

- 飛機場

- 零售與電子商務

- 車

- 飲食

- 製藥

- 採礦和採石

- 製造業(離散型和流程型)

- 其他

- 透過系統配置

- 固定/線性

- 模組化/靈活

- 按組件

- 運輸設備

- 驅動與控制

- 軟體與分析

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daifuku Co., Ltd.

- SSI Schaefer AG

- Murata Machinery Ltd.

- Mecalux SA

- BEUMER Group GmbH & Co. KG

- KNAPP AG

- Swisslog AG(KUKA)

- Honeywell Intelligrated

- Flexco

- Vanderlande Industries

- Dematic(KION Group)

- Interroll Holding AG

- Fives Group

- TGW Logistics Group

- Hytrol Conveyor Company

- Bastian Solutions Inc.

- Siemens Logistics

- Martin Engineering

- Dorner Manufacturing

- Intralox LLC

第7章 市場機會與未來展望

The Conveyors Market size is estimated at USD 9.66 billion in 2025, and is expected to reach USD 12.98 billion by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

The outlook is shaped by rapid e-commerce fulfillment growth, Industry 4.0 investment, and the search for energy efficiency that pushes regenerative-drive adoption capable of 37-39% power savings in downhill duty cycles. Asia-Pacific leads demand, while the Middle East records the fastest expansion as large logistics parks come online. Belt technology retains a plurality of installations, but overhead designs are scaling fastest because factories want floor-space relief. Software-driven predictive maintenance is emerging as the strongest component growth area, cutting unplanned downtime by up to 30% and extending asset life. At the same time, capital-spending hesitancy among smaller enterprises tempers the pace of high-end upgrades, and AGV/AMR substitution places added pressure on traditional fixed lines.

Global Conveyors Market Trends and Insights

Rapid growth of e-commerce fulfillment centres

Urban micro-fulfillment nodes now need conveyor platforms that sort more than 7,200 boxes per hour while occupying minimal floor area. Cafe Amazon's Thailand hub shows the model, handling 20,000 boxes a day across 4,000 outlets via a modular Interroll system. High-throughput crossbelt sorters keep same-day delivery promises, and vertical layouts maximize cubic throughput in space-restricted Asian megacities. Developers specify plug-and-play conveyor modules so that facilities can be re-arranged without civil works. These requirements sustain robust equipment replacement cycles and reinforce the conveyor systems market as a backbone of last-mile logistics.

Increasing demand for automated handling in food and beverage plants

Processors move beyond hygiene compliance toward end-to-end throughput optimization. Balaji Wafers reached zero unplanned downtime by shifting to Activated Roller Belt lines that maintain gentle product handling. Vision-equipped conveyors conduct real-time defect checks, shrinking manual inspection. In high-volume snack packaging, DirectDrive spirals now run for 48 hours straight at Diversified Foods, eliminating historic mechanical failures. Modular plastic belting extends service life, and emerging plant-based product lines require adaptable layouts able to process fragile items with varying moisture profiles.

High upfront CAPEX and long ROI periods

Even with 15% internal rates of return, energy-regenerative drives need six years to recoup capital, a hurdle for cash-constrained firms. Steel price swings between USD 870-950 per ton complicate budgeting. Leasing models exist, yet adoption lags in regions with tight credit markets. This cost tension restrains premium equipment penetration within the conveyor systems market.

Other drivers and restraints analyzed in the detailed report include:

- Rising airport passenger volumes boosting baggage-handling conveyors

- Government incentives for Industry 4.0 modernisation

- AMRs and AGVs emerging as substitute technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Belt conveyors retained 39% share in 2024, a cornerstone of mining, food and general manufacturing lines. The Dune Express in Texas proves belt scale, moving 13 million tons annually across 42 miles and removing 25,000 truck trips. Overhead variants lift at an 8.1% CAGR as factories open floor space and improve worker safety. Roller systems benefit from modular frames suited to reconfigurable assembly, while pallet lines serve precision automotive tasks. Across categories, smart sensors push predictive maintenance accuracy above 95%.

The conveyor systems market size for belt solutions is projected to expand alongside sustainable mining and bulk logistics projects, whereas overhead designs capture incremental share by maximizing cubic utilization. Energy-efficient vibratory designs need only 20% of traditional drive force, reflecting cross-segment innovation. Slat and chain lines remain embedded in heavy vehicle production, yet their growth is tempered by rising demand for flexible alternatives.

Unit handling represented 64.3% of 2024 demand, driven by e-commerce and discrete manufacturing workflows that value gentle product control and zero-pressure accumulation. Systems with vision-assisted defect detection now handle classification tasks while improving safety. Bulk handling, though smaller, will outpace unit growth at 8.7% CAGR, keyed to commodities growth and agriculture modernisation. Hybrid installations blur boundaries as plants seek infrastructure able to switch between pallets and granular feed.

In mining, TAKRAF's Collahuasi project underlines heavy-duty bulk capacity requirements. Pharmaceutical cleanrooms depend on vacuum conveyors transferring more than 11,100 liters per hour while preserving sterility. These dual paths sustain diversified revenue streams within the conveyor systems market.

Conveyor Systems Market Report is Segmented by Product Type (Belt, Roller, Pallet, Overhead, Slat/Chain and More), Load Type (Unit Handling, Bulk Handling), End-User Industry (Airport, Retail & E-Commerce, Automotive and More), System Configuration (Fixed/Linear, Modular/Flexible), Component (Conveying Equipment, Drives & Controls, Software & Analytics), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 38% of the conveyor systems market in 2024, anchored by expanding manufacturing clusters in China, India, and Southeast Asia. Daifuku's new Indian factory underscores rising local demand from automotive and electronics verticals. China continues to install heavy-duty bulk belts in mining and port infrastructure, while India leverages SAMARTH Udyog facilities to accelerate smart-factory retrofits. Cleanroom conveyor demand rises with semiconductor investment, and Japan's 310-mile freight line spotlights megaproject ambition.

The Middle East, growing at an 8.9% CAGR, benefits from logistics diversification agendas. Saudi Vision 2030 dedicates USD 106.6 billion to freight corridors such as Oxagon, driving need for high-capacity sortation and port conveyors. The UAE logistics market, valued at USD 20.03 billion in 2025, underpins warehouse automation outlays forecast at USD 1.6 billion by 2025.

North America and Europe continue to modernize legacy installations, spurred by DOE energy-efficiency grants and EU carbon regulations. Regenerative drives see early uptake, especially in Europe where green mandates elevate ROI calculations. South America and Africa show pockets of growth tied to mining and port projects, yet capital constraints slow adoption of analytics-heavy systems.

- Daifuku Co., Ltd.

- SSI Schaefer AG

- Murata Machinery Ltd.

- Mecalux S.A.

- BEUMER Group GmbH & Co. KG

- KNAPP AG

- Swisslog AG (KUKA)

- Honeywell Intelligrated

- Flexco

- Vanderlande Industries

- Dematic (KION Group)

- Interroll Holding AG

- Fives Group

- TGW Logistics Group

- Hytrol Conveyor Company

- Bastian Solutions Inc.

- Siemens Logistics

- Martin Engineering

- Dorner Manufacturing

- Intralox L.L.C.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of e-commerce fulfilment centres

- 4.2.2 Increasing demand for automated handling in food and beverage plants

- 4.2.3 Rising airport passenger volumes boosting baggage-handling conveyors

- 4.2.4 Government incentives for Industry 4.0 modernisation

- 4.2.5 Urban micro-fulfilment requires compact modular conveyors

- 4.2.6 Energy-regenerative conveyor drives support ESG targets

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX and long ROI periods

- 4.3.2 Retrofit integration risk causing production downtime

- 4.3.3 AMRs and AGVs emerging as substitute technologies

- 4.3.4 OT-IT cyber-vulnerabilities in conveyor control networks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Belt

- 5.1.2 Roller

- 5.1.3 Pallet

- 5.1.4 Overhead

- 5.1.5 Slat / Chain

- 5.1.6 Screw and Pneumatic

- 5.2 By Load Type

- 5.2.1 Unit Handling

- 5.2.2 Bulk Handling

- 5.3 By End-User Industry

- 5.3.1 Airport

- 5.3.2 Retail and E-commerce

- 5.3.3 Automotive

- 5.3.4 Food and Beverage

- 5.3.5 Pharmaceuticals

- 5.3.6 Mining and Quarrying

- 5.3.7 Manufacturing (Discrete and Process)

- 5.3.8 Others

- 5.4 By System Configuration

- 5.4.1 Fixed / Linear

- 5.4.2 Modular / Flexible

- 5.5 By Component

- 5.5.1 Conveying Equipment

- 5.5.2 Drives and Controls

- 5.5.3 Software and Analytics

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 Italy

- 5.6.3.4 United Kingdom

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daifuku Co., Ltd.

- 6.4.2 SSI Schaefer AG

- 6.4.3 Murata Machinery Ltd.

- 6.4.4 Mecalux S.A.

- 6.4.5 BEUMER Group GmbH & Co. KG

- 6.4.6 KNAPP AG

- 6.4.7 Swisslog AG (KUKA)

- 6.4.8 Honeywell Intelligrated

- 6.4.9 Flexco

- 6.4.10 Vanderlande Industries

- 6.4.11 Dematic (KION Group)

- 6.4.12 Interroll Holding AG

- 6.4.13 Fives Group

- 6.4.14 TGW Logistics Group

- 6.4.15 Hytrol Conveyor Company

- 6.4.16 Bastian Solutions Inc.

- 6.4.17 Siemens Logistics

- 6.4.18 Martin Engineering

- 6.4.19 Dorner Manufacturing

- 6.4.20 Intralox L.L.C.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

振動輸送機市場按最終用途產業、輸送機類型、驅動類型和輸送能力範圍分類 - 全球預測 2025-2032輸送機系統市場依產品類型、自動化類型、驅動類型、載重能力、輸送方向、皮帶材料、輸送方式、組件、最終用途產業和銷售管道-全球預測,2025-2032年

振動輸送機市場按最終用途產業、輸送機類型、驅動類型和輸送能力範圍分類 - 全球預測 2025-2032輸送機系統市場依產品類型、自動化類型、驅動類型、載重能力、輸送方向、皮帶材料、輸送方式、組件、最終用途產業和銷售管道-全球預測,2025-2032年 輸送系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(帶式、滾筒式、高架式、托盤式、地板/滑軌式、其他)、按操作方式(手動、半自動、自動)、按地區和競爭情況分類,2020-2030 年預測

輸送系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(帶式、滾筒式、高架式、托盤式、地板/滑軌式、其他)、按操作方式(手動、半自動、自動)、按地區和競爭情況分類,2020-2030 年預測 輸送機系統市場規模、佔有率、成長分析(按應用、類型、最終用途、組件和地區)- 2025 年至 2032 年產業預測

輸送機系統市場規模、佔有率、成長分析(按應用、類型、最終用途、組件和地區)- 2025 年至 2032 年產業預測 2025年全球輸送機系統市場報告

2025年全球輸送機系統市場報告 輸送系統市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、營運模式、產業及地理分類

輸送系統市場規模及預測 2021 - 2031、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:按類型、營運模式、產業及地理分類 全球鍊式輸送機市場2025年包裝輸送機全球市場報告

全球鍊式輸送機市場2025年包裝輸送機全球市場報告 全球輸送機市場規模(按類型、產業、地區和預測)

全球輸送機市場規模(按類型、產業、地區和預測) 全球採礦輸送系統市場(按輸送機類型、服務類型、應用、驅動類型和地區分類)- 預測至 2032 年

全球採礦輸送系統市場(按輸送機類型、服務類型、應用、驅動類型和地區分類)- 預測至 2032 年