|

市場調查報告書

商品編碼

1851525

醯胺纖維:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Aramid Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

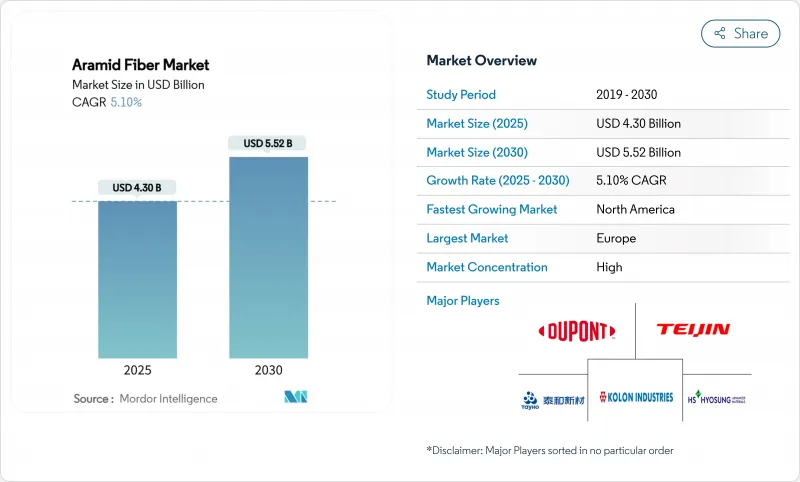

預計到 2025 年,醯胺纖維市場規模將達到 43 億美元,到 2030 年將達到 55.2 億美元,預測期內(2025-2030 年)複合年成長率為 5.10%。

該纖維在汽車、航太、電訊和先進個人防護設備等領域的廣泛應用推動了市場需求,而其優異的強度重量比和熱穩定性也確保了其長期應用前景。電動車、5G網路建設以及高超音速和太空專案投資的增加,都對輕量化材料提出了更高的要求,這也持續推動市場機會。同時,原料價格(主要是MPD和PPD)的波動擠壓了淨利率,並促使領先製造商進行垂直整合。智慧財產權限制進一步影響競爭動態,鞏固了那些能夠投入研發資金並利用交叉授權機制的現有企業的地位。

全球醯胺纖維市場趨勢與洞察

亞洲製造地加強個人防護裝備安全強制措施

中國、印度和東南亞新興經濟體工業安全法規的實施,推動了芳香聚醯胺增強手套、頭盔和耐熱工作服訂單的成長。芳香聚醯胺材料製成的工業頭盔比ABS材質的頭盔抗衝擊性高出37%,加速了其在工廠的普及。對位芳香聚醯胺製成的防切割手套在重量減輕30%的情況下,防護等級達到5級,且更適合長時間配戴。間位芳香聚醯胺製成的阻燃工作服在425°C高溫下仍能保持結構完整性,並符合更嚴格的鑄造和石化安全標準。因此,供該地區的製造商正在增加芳香聚醯胺紗線和織物的配額,從而鞏固了醯胺纖維市場的成長勢頭。

芳香聚醯胺增強型輕量化電動車輪胎推動歐盟綠色新政

歐洲汽車製造商正在加速輪胎重新設計項目,以減輕車輛重量,從而延長電動車的續航里程。芳香聚醯胺增強輪胎汽車胎體可達到高達25%的減重,直接輔助實現「綠色交易」的交通運輸脫碳目標。每減輕1公斤重量,就能增加0.7公里的續航里程,這促使汽車製造商使用芳香聚醯胺代替聚酯或鋼絲。橡膠混煉商正在將芳香聚醯胺增強橡膠混合物商業化,這種混合物在降低滾動阻力的同時,還能保持耐久性,從而增強了歐洲乃至北美對醯胺纖維的需求。

MPD和PPD原物料價格波動

原油價格高企和區域供應中斷推高了MPD和PPD的成本,擠壓了生產商的利潤空間,並使長期合約面臨風險。美國商務部已將芳香族二胺列為生產高度集中、具有重要化學價值的原料之一,加劇了供應安全風險。儘管製造商正透過探索生物基中間體和芳香聚醯胺廢料的閉合迴路回收來應對,但短期波動仍持續抑制醯胺纖維市場的成長動能。

細分市場分析

到2024年,對位芳香聚醯胺將佔據醯胺纖維市場65%的佔有率,這主要得益於彈道防護、航太和摩擦材料領域的需求成長。對位芳香聚醯胺紗線的抗張強度接近3.8 GPa,使其在防護衣和航空蜂窩材料領域保持領先地位。美國不斷成長的國防預算以及對輕質汽車複合材料的重新關注,為對位芳香聚醯胺在醯胺纖維市場提供了穩定的銷售來源。東麗公司在韓國工廠擴建3,000噸產能等重大投資,凸顯了對該類纖維的巨額資本投入。

儘管間位芳香聚醯胺的市佔率目前較小,但其成長速度驚人,預計到2030年將以5.42%的複合年成長率成長。先進的濕式紡絲長絲目前的拉伸強度可達1255兆帕,並且在長時間紫外線照射後仍能保持90%以上的強度,這為電力線護套等戶外應用開闢了新的前景。間位芳香聚醯胺也可用於阻燃織物、絕緣紙和過濾袋,滿足電子、工業安全和環境保護領域對熱穩定性的需求。由於亞洲半導體產能的擴張以及歐盟綠色轉型計劃的推進,間位醯胺纖維市場預計將穩步成長,這將形成一種競爭動態,在這種格局下,材料性能而非價格將成為決定客戶轉換率的關鍵因素。

到2024年,濕式紡絲將佔據醯胺纖維市場60%的佔有率,並繼續以5.87%的複合年成長率超越主要市場。此製程可實現均勻的聚合物凝固,以產生密度均勻、介電穩定性高的纖維,這是製造電工紙和過濾介質的先決條件。升級後的溶劑回收模組可降低排放和成本,並正被注重永續性的終端用戶所採用。隨著電氣化程度的提高和對濾材需求的成長,濕式紡絲醯胺纖維的市場規模預計將持續擴大。

對於對位芳綸芳香聚醯胺,乾噴濕紡製程仍然至關重要,因為鏈取向決定了其極高的拉伸性能。對聚醯亞胺類似物的實驗表明,其拉伸強度可達 2.72 GPa,模量超過 114 GPa,這為未來對位芳香聚醯胺增強材料的發展指明了方向。儘管該工藝目前市場佔有率較小,但它為高階彈道紗線的供應提供了保障,滿足了國防部門和奢侈運動品牌的需求。持續的生產線升級,旨在提高生產效率和改進溶劑捕集技術,將有助於鞏固其在醯胺纖維市場中的這一獨特地位。

區域分析

到2024年,歐洲將佔醯胺纖維市場35%的佔有率。嚴格的工人安全法規、符合ISO標準的阻燃標準以及歐盟的綠色新政正在推動芳綸纖維在汽車和工業領域的高價值應用。德國憑藉其出口導向的汽車產業基礎,將引領該地區的銷售成長,而法國和荷蘭則專注於先進的過濾和航太層壓材料。政府對電動車電池工廠的激勵措施將進一步促進聚合物複合材料的應用。

從2025年到2030年,北美將以5.34%的複合年成長率實現最快成長。聯邦國防預算將持續推動對位芳香聚醯胺彈道飛彈材料的需求,而美國國家航空暨太空總署(美國國家航空暨太空總署)和商業發射服務供應商則將投資轉向間位芳香聚醯胺隔熱罩。美國通訊業者正在升級颶風易發走廊的航空光纖骨幹網,並指定使用芳香聚醯胺強度的組件以減輕風暴造成的損失。加拿大也呈現類似的趨勢,其重點在於公共,尤其是在採礦和能源基礎設施領域。

亞太地區將成為醯胺纖維市場的下一個前線。中國正在擴大國內生產規模,以減少對進口的依賴,並力爭在本世紀中期實現對對位芳香聚醯胺的自給自足。智慧工廠、電動車電池廠和可再生能源基礎設施的大規模建設將增加對輕質耐熱材料的需求。日本和韓國正在加速推進半導體和5G硬體的高科技部署,這需要芳香聚醯胺所具備的介電穩定性和機械韌性。印度的「印度製造」國防計畫和更新後的職業安全規範將促進該地區個人防護裝備和防護用品的消費,從而進一步推動區域成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲製造地加強個人防護裝備安全強制措施

- 芳香聚醯胺增強型輕量化電動車輪胎是歐盟綠色交易的基礎。

- 5G部署激增推動了對芳香聚醯胺增強光纖電纜的需求

- 各國增加國防支出

- 高超音速和太空防禦領域的投資推動了間位芳香聚醯胺隔熱罩的消耗。

- 市場限制

- MPD和PPD原料的價格波動

- 對位芳香聚醯胺:專利交叉許可壁壘阻礙新進入者

- 高昂的生產成本

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 依產品類型

- 對位芳香聚醯胺

- 間位芳香聚醯胺

- 透過紡絲工藝

- 濕紡

- 乾噴濕紡

- 透過使用

- 安全防護設備

- 摩擦和煞車材料

- 光纖電纜

- 航太零件

- 汽車複合材料

- 電氣絕緣

- 其他(工業過濾、橡膠和輪胎加固)

- 按最終用戶行業分類

- 安全防護裝置

- 航太

- 車

- 電子與通訊

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aramid Hpm, LLC.

- China National Bluestar(Group)Co. Ltd.

- DuPont

- HS HYOSUNG ADVANCED MATERIALS

- Huvis Corp.

- Kolon Industries, Inc.

- Sinochem Internation Corporation

- SINOPEC YIZHENG CHEMICAL FIBRE LIMITED

- SRO Aramid

- Suzhou Zhaoda Specially Fiber Technical Co.,Ltd.

- TAEKWANG INDUSTRIAL CO., LTD.

- Teijin Limited

- Toray Industries Inc.

- TOYOBO MC Corporation

- Wuxi City Shengte Carbon Fiber Products Co.,Ltd

- X-FIPER NEW MATERIAL CO.,LTD

- Yantai Tayho Advanced Materials Co.,Ltd.

第7章 市場機會與未來展望

The Aramid Fiber Market size is estimated at USD 4.30 billion in 2025, and is expected to reach USD 5.52 billion by 2030, at a CAGR of 5.10% during the forecast period (2025-2030).

Increasing penetration in automotive, aerospace, telecom, and advanced personal protective equipment elevates demand, while the fiber's strength-to-weight ratio and thermal stability anchor long-term relevance. Material-lightweighting targets in electric mobility, the build-out of 5G networks, and rising investment in hypersonic and space programs continuously widen commercial opportunities. At the same time, feedstock price swings, mainly for MPD and PPD, keep margins under pressure, prompting vertical-integration moves by large producers. Intellectual-property constraints further shape competitive dynamics, cementing the position of incumbents that can finance R&D and navigate cross-licensing frameworks.

Global Aramid Fiber Market Trends and Insights

Escalating PPE Safety Mandates Across Asian Manufacturing Hubs

Growing enforcement of industrial-safety rules in China, India, and emerging Southeast Asian economies is lifting orders for aramid-reinforced gloves, helmets, and heat-resistant workwear. Industrial helmets made with aramid composites show 37% higher impact resistance than ABS counterparts, a performance gap that accelerates factory adoption. Cut-resistant gloves incorporating para-aramid deliver Level 5 protection with 30% less weight, improving comfort for continuous wear. Fire-retardant workwear formulated with meta-aramid maintains structural integrity at 425 °C, aligning with stricter foundry and petrochemical safety codes. Manufacturers supplying this region therefore raise allocation for aramid yarns and fabrics, strengthening the growth profile of the aramid fiber market.

EU Green-Deal Push for Lightweight EV Tires Reinforced with Aramid

European automakers accelerate tire redesign programs that shave vehicle mass to extend electric-car range. Aramid-reinforced tire carcasses cut weight by up to 25%, a saving directly linked to the Green Deal's transport decarbonization targets . Every kilogram trimmed offers a 0.7 km range gain, motivating OEMs to substitute polyester or steel cords with aramid. Compounders are commercializing aramid-filled rubber mixes that lower rolling resistance yet keep durability, reinforcing demand for the aramid fiber market in Europe and soon North America.

MPD & PPD Feedstock Price Volatility

Surging crude-oil swings and regional supply disruptions elevate MPD and PPD cost curves, compressing producer margins and unsettling long-term contracts. The U.S. Department of Commerce lists aromatic diamines among chemically critical inputs subject to geopolitically concentrated production, heightening supply-security risks . Manufacturers counter by exploring bio-based intermediates and closed-loop recovery of aramid scrap, yet near-term volatility still shaves growth momentum within the aramid fiber market.

Other drivers and restraints analyzed in the detailed report include:

- 5G Roll-out Surge Elevating Demand for Aramid-Reinforced Optical-Fiber Cables

- Hypersonic & Space Defense Investments Raising Meta-Aramid Thermal-Shield Consumption

- Patent Cross-Licensing Barriers Deterring New Para-Aramid Entrants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The para-aramid segment held a commanding 65% aramid fiber market share in 2024, supported by ballistic protection, aerospace, and friction-material demand. Para-aramid yarns deliver tensile strength near 3.8 GPa, sustaining their position in body armor and aviation honeycombs. Defense-budget uplifts in the United States and renewed interest in lightweight automotive composites ensure stable volume pipelines for para-aramid within the aramid fiber market. Significant investments, such as a 3,000-ton capacity addition at Toray's South Korea site, underscore the scale of capital allocation toward this fiber class.

Meta-aramid, while smaller in base, stages the fastest trajectory at a 5.42% CAGR through 2030. Advanced wet-spun filaments now reach 1,255 MPa tensile strength and retain over 90% strength after prolonged UV exposure, unlocking outdoor applications like transmission-line covers. Embedded in fire-retardant fabrics, insulation papers, and filtration bags, meta-aramid addresses thermal stability demands in electronics, industrial safety, and environmental protection. The aramid fiber market size for meta-aramid is forecast to expand steadily because of expanding semiconductor capacity across Asia and EU green-transition projects, setting a competitive dynamic where material attributes, not only price, decide customer conversion.

Wet spinning captured 60% of aramid fiber market share in 2024 and continues to out-pace the headline market with a 5.87% CAGR. The process offers homogeneous polymer coagulation, producing uniformly dense fibers that achieve high dielectric stability, a prerequisite for electrical papers and filtration media. Upgraded solvent-recycling modules reduce emissions and cost, supporting adoption even among sustainability-minded end-users. The aramid fiber market size for wet-spun output is projected to widen in line with electrification and filter-media demand growth.

Dry-jet wet spinning remains indispensable for para-aramid where chain orientation drives extreme tensile metrics. Lab runs of polyimide analogues display tensile strength up to 2.72 GPa and modulus above 114 GPa, confirming pathway headroom for future para-aramid enhancement. Although overall share is smaller, the process anchors high-end ballistic yarn supply, aligning with the needs of defense ministries and premium sports-equipment brands. Continuous line upgrades aimed at throughput efficiency and solvent-capture technology will safeguard its niche contribution to the aramid fiber market.

The Aramid Fiber Market Report Segments the Industry by Product Type (Para-Aramid, Meta-Aramid), Spinning Process (Wet Spinning, Dry Wet Spinning), Application (Security and Protection Equipment, Frictional and Brake Materials, and More), End-User Industry (Safety and Protection Equipment, Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe anchors the global aramid fiber market with 35% revenue in 2024. Stringent worker-safety laws, ISO-aligned flame standards, and the European Union's Green Deal propel high-value adoption in automotive and industrial settings. Germany, with its export-oriented automotive base, leads regional volume expansion, while France and the Netherlands specialize in advanced filtration and aerospace laminates. Government incentives for electric-vehicle battery plants further stimulate polymer-composite uptake.

North America posts the fastest CAGR at 5.34% for 2025-2030. Federal defense appropriations feed continuous demand for para-aramid ballistic materials, whereas NASA and private launch providers channel investments into meta-aramid thermal shields. U.S. telecom carriers renew aerial fiber backbones across hurricane-prone corridors, specifying aramid strength members to mitigate storm damage. Canada follows similar trends with a public-safety focus, particularly in mining and energy infrastructure.

Asia-Pacific represents the next frontier of scale for the aramid fiber market. China escalates domestic output to cut reliance on imports and targets self-sufficiency in para-aramid by mid-decade. Massive construction of smart factories, EV battery plants, and renewable infrastructure multiplies demand for lightweight, heat-resistant materials. Japan and South Korea refine high-tech deployment in semiconductors and 5G hardware, requiring dielectric stability and mechanical resilience that aramid delivers. India's Make-in-India defense program and updated occupational-safety codes build local PPE and armor consumption, adding depth to regional growth.

- Aramid Hpm, LLC.

- China National Bluestar (Group) Co. Ltd.

- DuPont

- HS HYOSUNG ADVANCED MATERIALS

- Huvis Corp.

- Kolon Industries, Inc.

- Sinochem Internation Corporation

- SINOPEC YIZHENG CHEMICAL FIBRE LIMITED

- SRO Aramid

- Suzhou Zhaoda Specially Fiber Technical Co.,Ltd.

- TAEKWANG INDUSTRIAL CO., LTD.

- Teijin Limited

- Toray Industries Inc.

- TOYOBO MC Corporation

- Wuxi City Shengte Carbon Fiber Products Co.,Ltd

- X-FIPER NEW MATERIAL CO.,LTD

- Yantai Tayho Advanced Materials Co.,Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating PPE Safety Mandates Across Asian Manufacturing Hubs

- 4.2.2 EU Green Deal Push for Lightweight EV Tires Reinforced with Aramid

- 4.2.3 5G Rollout Surge Elevating Demand for Aramid-Reinforced Optical-Fiber Cables

- 4.2.4 Increase in Defense Spending by Many Countries

- 4.2.5 Hypersonic and Space Defense Investments Raising Meta Aramid Thermal Shield Consumption

- 4.3 Market Restraints

- 4.3.1 MPD and PPD Feedstock Price Volatility

- 4.3.2 Patent Cross Licensing Barriers Deterring New Para-Aramid Entrants

- 4.3.3 High Production Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Para Aramid

- 5.1.2 Meta Aramid

- 5.2 By Spinning Process

- 5.2.1 Wet Spinning

- 5.2.2 Dry Jet Wet Spinning

- 5.3 By Application

- 5.3.1 Security and Protection Equipment

- 5.3.2 Frictional and Brake Materials

- 5.3.3 Optical Fiber Cables

- 5.3.4 Aerospace Components

- 5.3.5 Automotive Composites

- 5.3.6 Electrical Insulation

- 5.3.7 Others (industrial filtration, rubber and tire reinforcement)

- 5.4 By End User Industry

- 5.4.1 Safety and Protection Equipment

- 5.4.2 Aerospace

- 5.4.3 Automotive

- 5.4.4 Electronics and Telecommunication

- 5.4.5 Other End User Industries

- 5.5 Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aramid Hpm, LLC.

- 6.4.2 China National Bluestar (Group) Co. Ltd.

- 6.4.3 DuPont

- 6.4.4 HS HYOSUNG ADVANCED MATERIALS

- 6.4.5 Huvis Corp.

- 6.4.6 Kolon Industries, Inc.

- 6.4.7 Sinochem Internation Corporation

- 6.4.8 SINOPEC YIZHENG CHEMICAL FIBRE LIMITED

- 6.4.9 SRO Aramid

- 6.4.10 Suzhou Zhaoda Specially Fiber Technical Co.,Ltd.

- 6.4.11 TAEKWANG INDUSTRIAL CO., LTD.

- 6.4.12 Teijin Limited

- 6.4.13 Toray Industries Inc.

- 6.4.14 TOYOBO MC Corporation

- 6.4.15 Wuxi City Shengte Carbon Fiber Products Co.,Ltd

- 6.4.16 X-FIPER NEW MATERIAL CO.,LTD

- 6.4.17 Yantai Tayho Advanced Materials Co.,Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Market Expansion of Unmanned Aerial Vehicles (UAV)

間位芳香聚醯胺纖維市場:依產品類型、終端用途產業及應用分類-2026-2032年全球市場預測

間位芳香聚醯胺纖維市場:依產品類型、終端用途產業及應用分類-2026-2032年全球市場預測 2026-2030全球醯胺纖維市場

2026-2030全球醯胺纖維市場 全球醯胺纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醯胺纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026全球醯胺纖維市場報告

2026全球醯胺纖維市場報告 醯胺纖維市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、區域和競爭格局分類,2021-2031年防切割纖維市場:依纖維類型、應用、終端用戶產業和銷售管道-全球預測,2026-2032年

醯胺纖維市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、區域和競爭格局分類,2021-2031年防切割纖維市場:依纖維類型、應用、終端用戶產業和銷售管道-全球預測,2026-2032年 醯胺纖維市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

醯胺纖維市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 間位芳香聚醯胺纖維市場規模、佔有率和成長分析(按等級、應用、纖維類型、終端用戶產業和地區分類)-2026-2033年產業預測

間位芳香聚醯胺纖維市場規模、佔有率和成長分析(按等級、應用、纖維類型、終端用戶產業和地區分類)-2026-2033年產業預測 芳綸纖維市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

芳綸纖維市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 全球芳綸纖維市場(至 2035 年):依產品、生產流程、形態、銷售通路、環境因素、應用領域、最終用戶、公司、主要地區、產業趨勢及預測

全球芳綸纖維市場(至 2035 年):依產品、生產流程、形態、銷售通路、環境因素、應用領域、最終用戶、公司、主要地區、產業趨勢及預測