|

市場調查報告書

商品編碼

1851495

菸草包裝:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Tobacco Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

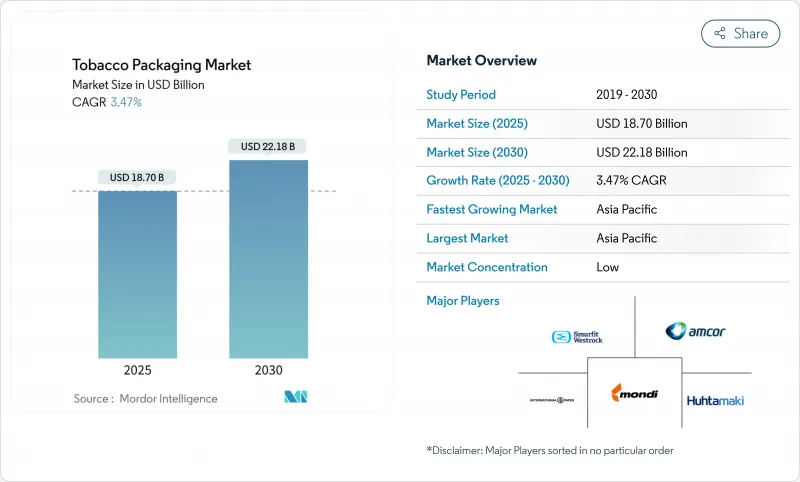

預計到 2025 年,菸草包裝市場規模將達到 187 億美元,到 2030 年將達到 221.8 億美元,年複合成長率為 3.47%。

強制簡易包裝法規已在25個司法管轄區生效,歐盟《包裝和包裝廢棄物法規》推動100%使用可回收材料,以及對溯源解決方案的加速投資,共同構成了菸草包裝市場最強勁的成長動力。隨著高所得地區吸菸率的下降,能夠整合防偽技術、紙基阻隔材料和自動化包裝形式的供應商將有機會搶佔原本停滯不前的市場佔有率。向紙板和生物分解性塑膠的材料轉型,既降低了監管風險,又增加了對防潮和防香材料的需求,並維持了鋁箔襯墊和全像撕膜等組件的優質化。亞太地區憑藉中國、日本和韓國的大規模消費以及熱撕式包裝(菸草包裝)技術的快速普及,保持主導地位。這些因素將支撐菸草包裝市場在2030年之前保持穩定且受監管主導的成長軌跡。

全球菸草包裝市場趨勢與洞察

強制推行簡易包裝及加強圖形警示

目前已有25個國家強制要求使用簡易包裝,澳洲將於2025年要求將警示訊息直接印在香菸上,實際上會消除品牌識別。供應商必須重新設計包裝結構,以保持包裝的完整性,即使超過75%的包裝面積都用於健康警示圖,也能確保在香菸銷售趨於平穩的情況下獲得可預測的合規收入。加拿大的滑動式包裝系統將警示面積擴大了41%,顯示監管變化正在推動全新的包裝結構出現。英國也正在推動這項進程,目前正在就2024年前將標準化範圍擴大到所有菸草產品進行磋商。

為了永續性和降低成本,改用紙板。

歐盟的《一次性塑膠指令》將香菸過濾嘴列為海灘上第二大常見垃圾,敦促各品牌重新評估其層壓材料,並採用能夠穩定水分含量並取代金屬化薄膜的高阻隔紙塗層。 ITC 旗下的 InnovPack 目前每年將超過 10 萬噸可回收紙板轉化為 Bioseal 和 Oxyblock 產品,證明其大規模成本與多層塑膠相當。雙層水性塗佈紙板的研究表明,鍍鋁紙在滿足可堆肥性目標的同時,還能實現與聚合物薄膜相當的香氣保護效果。

商品稅上漲抑制消費

加拿大2025年菸附加稅條例要求製造商繳納與銷售額掛鉤的年度附加稅,將給包裝預算帶來成本壓力。印尼的法規也反映了類似的增稅措施,該法規規定2024年起香菸包裝的最小規格為20支,這表明稅收和包裝設計之間存在相互作用。

細分市場分析

到2024年,紙和紙板將佔菸草包裝市場83.26%的佔有率,這反映了監管政策的偏好以及阻隔塗層技術的日趨成熟。塑膠包裝市場佔有率較小,但其複合年成長率將達到7.45%,成為成長最快的細分市場,這主要得益於專為加熱菸草煙彈和兒童電子煙油煙彈設計的多層薄膜不斷擴大市場佔有率。預計2025年至2030年間,塑膠菸草包裝市場將新增11億美元,主要得益於自動化相容的複合機能夠以每分鐘600包的速度高效運作且密封無損。鋁箔在高階產品線(例如Treasurer London Aluminum)中仍然扮演著重要的保鮮角色,其作用範圍雖窄但穩定。

對木質素-高密度聚乙烯(HDPE)共混物和海藻基薄膜的快速研究表明,到2030年,有望將原生塑膠的體積減少5%,這與歐盟100%可回收包裝的目標相符。 Smurfit Westlock公司研發的金屬化阻隔整合混合板材可進行路邊回收,且氧氣透過率已低於1克/平方米,這表明加工商如何利用規模效應,將實驗室的突破性技術迅速商業化。

到2024年,初級包裝將佔菸草包裝市場佔有率的65.78%。受免稅捆綁包裝形式以及嵌入式RFID和QR碼追蹤技術的需求成長推動,二次性紙盒預計將以5.63%的複合年成長率超越初級包裝。到2030年,菸草包裝二級解決方案的市場規模預計將達到62億美元,這主要得益於採用線上序列化技術的高速裝箱機的普及。

供應商正在透過智慧撕開膠帶提升產品價值,這種膠帶打開後會顯現全像圖,並防止重複使用。運輸紙板採用至少含有30%消費後回收成分的再生紙板,以滿足企業的範圍3排放義務。高階硬紙盒,例如大衛杜夫的溫斯頓邱吉爾2025版,採用再生紙板核心材料,並且限量生產。

煙草包裝市場報告按材料(紙/紙板、塑膠、金屬、玻璃、生質塑膠)、包裝類型(初級包裝、二級包裝、散裝包裝、高檔硬盒包裝)、產品形式(軟包裝、硬包裝、袋裝、管裝、條狀包裝)、煙草類型(捲菸、無菸煙草、新一代煙草、歐洲雪茄)和地區(北美、歐洲、亞洲、中東和地區)。市場預測以美元計價。

區域分析

亞太地區預計到2024年將佔全球銷售額的38.34%,年均成長率達6.82%。這主要得益於中國、印度和印尼等吸菸人口數量居全球首位,同時電子煙監管標準也日益嚴格。亞太地區菸草包裝市場預計在2025年至2030年間達到18億美元,主要驅動力是國內紙板廠擴大阻隔塗佈紙板的生產。此外,中國一線城市不斷推進的都市化和高階消費的興起,也將帶動節慶期間金屬禮品罐的需求成長。

北美在材料創新方面繼續保持領先地位,Amcor 的 AmFiber 紙計劃於 2025 年在歐洲獲得專利並在美國進行商業推廣,並將供應給希望在香菸外包裝中替代 PVdC 薄膜的加工商。

歐洲面臨嚴格的 PFAS 禁令以及 2040 年無菸目標,這迫使加工商投資於水性阻隔化學品和閉合迴路回收技術。中東和非洲的高階市場在海灣地區呈現成長態勢,免稅店偏好燙金紙盒。受經濟波動影響,南美洲的成長有所放緩,但巴西計劃於 2026 年對其國家健康警示進行改革,預計將推動該地區印刷品質的提升。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 統一包裝規定及加強圖形警示

- 為了追求永續性和成本控制,轉向使用紙板。

- 引入單元級防偽技術

- 適用於HTP/電子煙的自動化相容包裝格式

- 文化活動限量版

- 市場限制

- 提高消費稅將減少消費

- 全球簡易包裝的普及性降低了品牌投資報酬率

- 歐盟和美國收緊了對PFAS和塑膠的禁令

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 材料

- 紙和紙板

- 塑膠(BOPP、PET、PVC)

- 金屬(鋁箔、馬口鐵)

- 玻璃和陶瓷

- 生質塑膠和可堆肥塑膠

- 按包裝類型

- 基本的

- 二次性

- 散裝/轉運

- 高階豪華硬盒

- 按產品形式

- 菸草軟包

- 香菸硬盒/鉸鏈鏈蓋紙盒

- 小袋和包裝袋

- 管狀、棒狀、加熱不燃燒棒

- 依煙草類型

- 吸煙

- 無煙煙草

- 下一代產品(加熱不燃燒菸草製品和電子煙)

- 雪茄和小雪茄

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲、紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Smurfit Westrock

- International Paper Company

- Mondi Group

- Innovia Films Ltd.

- Philip Morris International Inc.

- Sonoco Products Company

- Siegwerk Druckfarben AG & Co. KGaA

- Japan Tobacco International

- Treofan Film International

- Stora Enso Oyj

- ITC Limited(Packaging & Printing)

- British American Tobacco plc

- Shenzhen Jinjia Group Co. Ltd.

- Huhtamaki Oyj

- Uflex Ltd.

- DS Smith plc

- Jindal Poly Films Ltd.

- Oji Holdings Corp.

- SCHUR Flexibles Holding

第7章 市場機會與未來展望

The tobacco packaging market size is valued at USD 18.70 billion in 2025 and is forecast to reach USD 22.18 billion by 2030, advancing at a 3.47% CAGR.

Mandatory plain-pack rules now enforced in 25 jurisdictions, the drive for 100% recyclable materials under the EU Packaging and Packaging Waste Regulation, and accelerating investment in track-and-trace solutions together shape the most powerful growth levers for the tobacco packaging market. Suppliers able to integrate anti-counterfeit technology, paper-based barrier materials and automation-ready formats capture volume that would otherwise stagnate as smoking prevalence edges down in high-income regions. Material shifts toward paperboard and biodegradable plastics lower regulatory risk yet increase demand for moisture and aroma barriers, sustaining premiumisation in components such as foil liners and hologram tear tapes. Asia-Pacific retains leadership thanks to large-scale consumption and rapid harmonisation of heated-tobacco packaging laws in China, Japan, and South Korea. Together, these forces keep the tobacco packaging market on a steady yet regulation-dominated growth path through 2030.

Global Tobacco Packaging Market Trends and Insights

Rising plain-pack mandates and graphic warnings

Twenty-five countries now enforce plain packaging, and Australia moved warnings directly onto cigarette sticks in 2025, leaving brand imagery almost obsolete. Suppliers must redesign structural features to preserve pack integrity despite 75 %-plus panel space devoted to health graphics, ensuring predictable compliance revenue even where cigarette volumes plateau. Canada's slide-and-shell format enlarged warning area by 41 %, illustrating how rule changes prompt entirely new pack architectures. The UK's 2024 consultation to extend standardisation to all tobacco products signals further momentum.

Paperboard shift for sustainability and cost

The EU Single-Use Plastics Directive ranks cigarette filters as the second most littered beach item, prompting brands to overhaul laminates and adopt high-barrier paper coatings that replace metallised films while keeping moisture content stable. ITC's InnovPack now converts more than 100,000 tonnes of recyclable board into Bioseal and Oxyblock formats annually, demonstrating large-scale cost parity with multi-layer plastics. Research on double-layer water-based coated boards shows aluminium-plated paper achieving comparable aroma protection to polymer films yet meeting compostability targets.

Escalating excise taxes shrink consumption

Canada's 2025 Tobacco Charges Regulations oblige manufacturers to pay annual levies indexed to sales, adding cost pressure that trickles into packaging budgets. Similar hikes appear in Indonesia's 2024 rule mandating minimum pack sizes of 20 cigarettes, showing how tax policy and packaging design interact.

Other drivers and restraints analyzed in the detailed report include:

- Unit-level anti-counterfeit technology adoption

- Automation-ready pack formats for HTP/e-cig

- Global plain-pack roll-out reduces branding ROI

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper & paperboard captured 83.26 % of the tobacco packaging market in 2024, reflecting both regulatory preference and maturing barrier-coating technology. The plastics segment, though smaller, will post the highest 7.45 % CAGR as multilayer films tailored for heated-tobacco cartridges and child-resistant e-liquid pods gain share. The tobacco packaging market size for plastics is forecast to add USD 1.1 billion between 2025 and 2030, buoyed by automation-ready laminates that run at 600 packs/minute without seal failure. Aluminium foil maintains a narrow but stable role for aroma retention in premium lines such as Treasurer London Aluminum.

Rapid research into lignin-HDPE blends and seaweed-based films indicates potential to shift a further 5 % volume away from virgin plastic by 2030, aligning with the EU target of 100 % recyclable packs. Smurfit WestRock's hybrid board with integrated metallised barrier already satisfies <1 g/m2 oxygen transmission while remaining curb-side recyclable, demonstrating how converters use scale to commercialise lab breakthroughs swiftly.

Primary packs delivered 65.78 % of the tobacco packaging market share in 2024 thanks to regulatory mandates for health messaging on every retail unit. Secondary cartons will outpace at 5.63 % CAGR, driven by duty-free bundle formats and growing need to embed RFID or QR codes for track-and-trace. Tobacco packaging market size for secondary solutions is projected to touch USD 6.2 billion by 2030, supported by high-speed case packers integrating on-line serialisation.

Suppliers add value through smart tear tapes that reveal holograms when opened, deterring reuse. In line haul, transit packaging leverages recycled corrugated grades exceeding 30 % post-consumer content to meet corporate scope-3 emission commitments. Luxury rigid boxes endure in limited runs, such as Davidoff's Winston Churchill 2025 edition using layered beech veneer over recycled board cores.

The Tobacco Packaging Market Report is Segmented by Material (Paper and Paperboard, Plastics, Metals, Glass, Bioplastics), Packaging Type (Primary, Secondary, Bulk, Luxury Rigid Boxes), Product Form (Soft Pack, Hard Pack, Pouch, Tube and Stick), Tobacco Type (Smoking, Smokeless, Next-Generation Products, Cigars), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Geography Analysis

Asia-Pacific commanded 38.34 % of revenue in 2024 and will expand 6.82 % annually as China, India and Indonesia tighten e-cigarette standards yet maintain the world's largest smoking populations. Tobacco packaging market size additions in Asia-Pacific will reach USD 1.8 billion over 2025-2030, supported by domestic board mills scaling barrier-coated grades. Urbanisation and premiumisation in tier-one Chinese cities also fuel demand for metallicised gift tins during festival peaks.

North America stays material-innovation leader, with Amcor's AmFiber paper gaining European patent in 2025 and slated for US commercial roll-out, supplying converters aiming to replace PVdC films in cigarette overwrap.Canada's annual tobacco charges and large graphic warnings will lift compliance spend per pack by an estimated 2 US cents, modestly boosting packaging value despite flat cigarette volumes.

Europe faces stringent PFAS bans and the 2040 tobacco-free goal, compelling converters to invest in water-based barrier chemistries and closed-loop recycling. The Middle East & Africa offer pockets of premium growth in the Gulf, where duty-free outlets favour gold-foil embossed cartons. South America's progress is slower amid economic volatility but Brazil's national health-warning refresh slated for 2026 should spark regional print-quality upgrades.

- Amcor plc

- Smurfit Westrock

- International Paper Company

- Mondi Group

- Innovia Films Ltd.

- Philip Morris International Inc.

- Sonoco Products Company

- Siegwerk Druckfarben AG & Co. KGaA

- Japan Tobacco International

- Treofan Film International

- Stora Enso Oyj

- ITC Limited (Packaging & Printing)

- British American Tobacco plc

- Shenzhen Jinjia Group Co. Ltd.

- Huhtamaki Oyj

- Uflex Ltd.

- DS Smith plc

- Jindal Poly Films Ltd.

- Oji Holdings Corp.

- SCHUR Flexibles Holding

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising plain-pack mandates and graphic warnings

- 4.2.2 Paperboard shift for sustainability and cost

- 4.2.3 Unit-level anti-counterfeit tech adoption

- 4.2.4 Automation-ready pack formats for HTP/e-cig

- 4.2.5 Cultural-event limited-edition packs

- 4.3 Market Restraints

- 4.3.1 Escalating excise taxes shrink consumption

- 4.3.2 Global plain-pack roll-out erodes branding ROI

- 4.3.3 PFAS and plastics bans tightening in EU and US

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Paper and Paperboard

- 5.1.2 Plastics (BOPP, PET, PVC)

- 5.1.3 Metals (Al Foil, Tinplate)

- 5.1.4 Glass and Ceramics

- 5.1.5 Bioplastics and Compostables

- 5.2 By Packaging Type

- 5.2.1 Primary

- 5.2.2 Secondary

- 5.2.3 Bulk / Transit

- 5.2.4 High-End Luxury Rigid Boxes

- 5.3 By Product Form

- 5.3.1 Cigarette Soft Pack

- 5.3.2 Cigarette Hard Pack / Hinge-lid Carton

- 5.3.3 Pouch and Sachet

- 5.3.4 Tube, Stick and Heat-Not-Burn Sticks

- 5.4 By Tobacco Type

- 5.4.1 Smoking Tobacco

- 5.4.2 Smokeless Tobacco

- 5.4.3 Next-Generation Products (HTP and e-cig)

- 5.4.4 Cigars and Cigarillos

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Smurfit Westrock

- 6.4.3 International Paper Company

- 6.4.4 Mondi Group

- 6.4.5 Innovia Films Ltd.

- 6.4.6 Philip Morris International Inc.

- 6.4.7 Sonoco Products Company

- 6.4.8 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.9 Japan Tobacco International

- 6.4.10 Treofan Film International

- 6.4.11 Stora Enso Oyj

- 6.4.12 ITC Limited (Packaging & Printing)

- 6.4.13 British American Tobacco plc

- 6.4.14 Shenzhen Jinjia Group Co. Ltd.

- 6.4.15 Huhtamaki Oyj

- 6.4.16 Uflex Ltd.

- 6.4.17 DS Smith plc

- 6.4.18 Jindal Poly Films Ltd.

- 6.4.19 Oji Holdings Corp.

- 6.4.20 SCHUR Flexibles Holding

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

菸草包裝:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

菸草包裝:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球菸草包裝市場:市場規模、佔有率和趨勢分析(按材料、包裝類型、產品和地區)、細分市場預測(2025-2030 年)

全球菸草包裝市場:市場規模、佔有率和趨勢分析(按材料、包裝類型、產品和地區)、細分市場預測(2025-2030 年) 2025-2033年菸草包裝市場報告(依材料類型、包裝類型、最終用途和地區)

2025-2033年菸草包裝市場報告(依材料類型、包裝類型、最終用途和地區) 全球菸草包裝市場:2025年

全球菸草包裝市場:2025年 全球菸草包裝市場:市場規模、佔有率、趨勢、產業分析(依包裝材料、產品、材料類型和地區)、未來預測(2025-2034)

全球菸草包裝市場:市場規模、佔有率、趨勢、產業分析(依包裝材料、產品、材料類型和地區)、未來預測(2025-2034) 全球菸草包裝市場按類型、材料、最終用戶和地區分類(2026-2032 年)

全球菸草包裝市場按類型、材料、最終用戶和地區分類(2026-2032 年) 菸草包裝市場規模、佔有率、成長分析、按材料類型、按包裝類型、按最終用戶、按地區 - 行業預測,2024-2031 年

菸草包裝市場規模、佔有率、成長分析、按材料類型、按包裝類型、按最終用戶、按地區 - 行業預測,2024-2031 年 菸草包裝市場、機會、成長動力、產業趨勢分析與預測,2024-2032

菸草包裝市場、機會、成長動力、產業趨勢分析與預測,2024-2032 全球菸草和菸草製品包裝產業的機會:2024 年

全球菸草和菸草製品包裝產業的機會:2024 年