|

市場調查報告書

商品編碼

1851492

計劃管理軟體:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Project Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

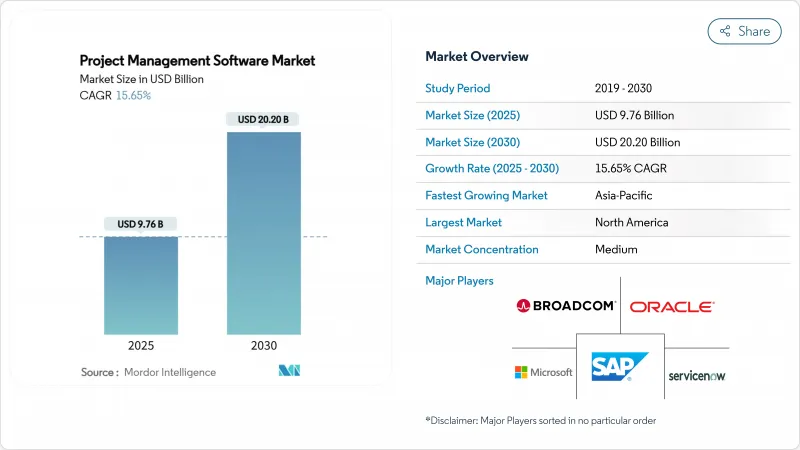

計劃管理軟體市場預計到 2025 年將達到 97.6 億美元,到 2030 年將成長到 202 億美元,複合年成長率為 15.65%。

雲端配置、低程式碼可配置性和預測分析等技術,將計劃監控從任務追蹤升級到策略編配,持續推動市場擴張。隨著分散式團隊需要即時協作,以及企業將專案資料與財務、人力資源和客戶系統整合以實現統一的可視性,市場需求不斷成長。混合部署在受監管行業中成長最快,因為本地資料管理仍然不可或缺。中小企業正在透過繞過傳統的採用障礙來加速採用,而人工智慧原生功能則增強了風險管理和成本預測。隨著供應商整合特定產業的工作流程和開放的API生態系統,競爭日益激烈。

全球計劃管理軟體市場趨勢與洞察

遠端和混合企劃團隊的雲端優先採用

據報道,從桌面工具遷移到雲端原生平台可將任務完成速度提升 54%。計劃管理軟體市場正蓬勃發展,即時同步功能使跨時區的分散式團隊能夠保持工作進度。 IT 部門更青睞雲端的可擴展性,因為它減輕了容量規劃的負擔。隨著受監管行業在可訪問性和數據控制之間尋求平衡,混合模式正以 18.4% 的複合年成長率成長。供應商正積極回應,提供滿足資料主權要求並消除協作摩擦的資料駐留選項。

將您的專案管理平台與企業級 SaaS 堆疊整合

企業平均運行 976 個應用程式,但只有 28% 實現了有效整合,這減緩了計劃資料的流動。現代平台將自身定位為與財務、客戶關係管理 (CRM) 和人力資源 (HR) 系統整合的樞紐,從而提升了計劃管理軟體市場在企業架構中的重要性。預計到 2025 年,SaaS 整合市場規模將超過 150 億美元,而實施全面整合策略的公司則報告生產力提高了 30%。雲端原生供應商透過提供開放的 API 和預先建置連接器來減少昂貴的客製化編碼,從而獲得了競爭優勢。

舊系統遷移和定製成本高昂

由於資料映射、檢驗和使用者培訓需要投入大量精力,企業面臨的實施成本可能高達許可費的三倍。遷移成本平均超支 30%,每Terabyte存檔資料的成本最高可達 15,000 美元。這項障礙會減緩更新週期,並阻礙擁有高度客製化工作流程的現有企業在計劃管理軟體市場的滲透。

細分市場分析

到2024年,雲端部署將佔總營收的75%,但混合配置的複合年成長率將達到18.4%,展現出計劃管理軟體市場最強勁的成長動能。混合解決方案可將本機儲存庫與雲端工作空間同步。本地部署在政府和國防領域仍然佔據主導地位,但隨著雲端區域安全認證要求日益嚴格,其市場佔有率正在萎縮。

混合模式的興起反映了用於管理無縫離線同步、加密隧道和選擇性儲存的工具的出現。建設公司將圖紙儲存在本地伺服器上,同時透過雲端控制面板共用工地現場更新。供應商透過提供精細化的租戶管理以及圍繞合規性建立提升銷售路徑來脫穎而出。

2024年,大型企業將佔專案管理軟體支出的61.1%,而中小企業將以17.2%的複合年成長率成長,這將重塑計劃管理軟體市場規模的格局。成長將主要集中在亞太地區,地方政府正在提供津貼以提升企業的數位技能。日本中小企業正在採用基於人工智慧的排班系統來彌補人手不足。收費系統正在取消最低用戶數量限制,從而降低市場進入門檻。

在市場飽和的地區,隨著企業成長趨於平緩,供應商推出中小企業的精簡版產品和社群活動。但跨國企業仍依賴複雜的整合和高階分析套件來推動營收成長。這種雙重需求迫使產品團隊在維持產品可擴充性的同時,避免使用者上手過程過於複雜。

計劃管理軟體市場報告按配置(雲端部署、本地部署)、組織規模(大型企業、中小企業)、最終用戶行業(IT 和電信、醫療保健、建築和基礎設施、銀行、金融服務和保險、其他)、訂閱類型(月度訂閱、年度訂閱、一次性許可)和地區對行業進行分類。

區域分析

2024年,北美佔據了計劃管理軟體市場36.5%的佔有率。該地區的企業憑藉著強大的基礎設施和充足的IT預算,部署了端到端的計劃生態系統。微軟在Microsoft 365整合計劃管理功能的支援下,2024年營收成長16%,達到2,450億美元。創新中心持續引領人工智慧模組的開發,但應用已接近飽和,導致區域成長放緩。

亞太地區到2030年將以15.3%的複合年成長率成長,成為所有地區中成長最快的地區。隨著跨國公司採用整合的Salesforce和Azure技術堆疊來管理跨境舉措,中國的SaaS市場將以每年近30%的速度成長。在雲端運算普及和新興企業企業蓬勃發展的推動下,印度的SaaS收入預計將從2023年的71.8億美元成長到2032年的629.3億美元。東南亞的中小型企業將採用符合區域合規規範的在地化專案管理套件。

隨著GDPR強制要求在地化能力,歐洲將迎來強勁成長,這將使提供歐盟資料中心和高級加密技術的供應商受益。在南美洲以及中東和非洲,寬頻和支付管道的改善推動了雲端服務的普及,此前基礎設施的不足阻礙了雲端服務的使用。隨著連接成本的進一步下降,供應商預計雲端服務將實現兩位數成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 遠端和混合企劃團隊的雲端優先採用

- 將您的專案管理平台與企業級 SaaS 堆疊整合

- 低程式碼/無程式碼配置方式正被中小企業廣泛採用。

- 人工智慧主導的進度和成本偏差預測分析

- 行業專用專案管理套件(建築、醫療保健等)

- 嵌入計劃工作流程的 ESG 合規報告

- 市場限制

- 遷移和定製到原有系統需要高昂的成本

- 多租戶雲端中的資料主權和隱私問題

- 功能商品化會增加供應商鎖定風險。

- 變更管理疲勞抑制了大規模部署

- 關鍵法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 關鍵相關人員影響評估

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 透過部署

- 雲

- 本地部署

- 按組織規模

- 主要企業

- 小型企業

- 按最終用戶行業分類

- 資訊科技和電訊

- 衛生保健

- 建築和基礎設施

- BFSI

- 政府/公共部門

- 製造業

- 其他

- 按訂閱類型

- 月度訂閱

- 年度訂閱

- 一次許可證

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Adobe Inc.(Workfront)

- AEC Software Inc.

- Asana Inc.

- Atlassian Corporation PLC

- Basecamp LLC

- Broadcom Inc.(Clarity PPM)

- ClickUp(Mango Technologies, Inc.)

- Microsoft Corporation

- Monday.com Ltd.

- Oracle Corporation

- Planview Inc.

- Procore Technologies Inc.

- SAP SE

- ServiceNow Inc.

- Smartsheet Inc.

- Teamwork.com Ltd.

- Trello Enterprise(Atlassian)

- Unit4 NV

- Wrike Inc.(Citrix Systems)

- Zoho Corporation Pvt Ltd.

第7章 市場機會與未來展望

The project management software market stands at USD 9.76 billion in 2025 and is advancing at a 15.65% CAGR toward USD 20.20 billion by 2030.

Expansion remains anchored in cloud-first deployment, low-code configurability, and predictive analytics that collectively upgrade project oversight from task tracking to strategic orchestration. Demand intensifies as distributed teams require real-time collaboration, and enterprises integrate project data with finance, HR, and customer systems for unified visibility. Hybrid deployment registers the fastest growth because regulated industries still need local data control. Small and medium enterprises (SMEs) accelerate adoption by bypassing traditional implementation hurdles, while AI-native features strengthen risk management and cost forecasting. Competitive intensity increases as vendors embed industry-specific workflows and open API ecosystems.

Global Project Management Software Market Trends and Insights

Cloud-First Adoption for Remote and Hybrid Project Teams

Organizations report 54% faster task completion when shifting from desktop tools to cloud-native platforms. The project management software market gains traction because real-time synchronization enables distributed teams to sustain momentum across time zones. IT departments prefer cloud scalability that removes capacity planning burdens. Hybrid models grow at 18.4% CAGR because regulated sectors balance accessibility with data control. Vendors respond by offering data-residency options that satisfy sovereignty mandates while keeping collaboration friction-free.

Integration of PM Platforms with Enterprise SaaS Stacks

Enterprises run an average of 976 applications, yet only 28% are meaningfully integrated, stalling project data flow. Modern platforms position themselves as integration hubs tied to finance, CRM, and HR systems, raising the project management software market relevancy in enterprise architecture. The SaaS integration segment is projected to exceed USD 15 billion by 2025, and firms that deploy comprehensive integration strategies report 30% productivity lifts. Cloud-native vendors gain an advantage through open APIs and pre-built connectors that curb expensive custom coding.

High Migration and Customization Costs for Legacy Estates

Enterprises face implementation bills that triple license fees because data mapping, validation, and user training are labor intensive. Migration overruns average 30% and can reach USD 15,000 per terabyte of archives. The hurdle delays refresh cycles and slows the project management software market uptake among incumbents with heavily customized workflows.

Other drivers and restraints analyzed in the detailed report include:

- SME Uptake Boosted by Low-Code / No-Code Configurability

- AI-Driven Predictive Analytics for Schedule and Cost Variance

- Data-Sovereignty and Privacy Concerns in Multi-Tenant Clouds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment held 75% of revenue in 2024, but hybrid configurations grow at 18.4% CAGR, signalling the strongest momentum inside the project management software market. Hybrid solutions synchronize local repositories with cloud workspaces; this duality attracts firms bound by data residency statutes. On-premise persists in government and defense, yet its share shrinks as security certifications for cloud zones tighten.

The hybrid rise reflects tools that now manage seamless offline sync, encrypted tunnels, and selective storage. Construction companies keep drawings on local servers yet share field updates through cloud dashboards. Vendors differentiate by offering granular tenancy controls, creating upsell paths around compliance.

Large enterprises controlled 61.1% of 2024 spend, but SMEs chart a 17.2% CAGR that reshapes the project management software market size trajectory. Growth centers on Asia-Pacific, where local governments fund digital upskilling grants. Japanese SMEs adopt AI-assisted scheduling to offset labor shortages. Pricing tiers remove user minimums, reducing the barrier to entry.

Enterprise growth plateaus in saturated regions, so vendors launch light editions and community events geared to smaller firms. Yet, multi-national corporations still anchor revenue with complex integrations and premium analytics bundles. Dual focus forces product teams to maintain scalability without complicating onboarding.

The Project Management Software Market Report Segments the Industry Into Deployment (Cloud, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, Healthcare, Construction and Infrastructure, BFSI, and More), Subscription Type (Monthly Subscription, Annual Subscription, and One-Time License), and Geography.

Geography Analysis

North America held 36.5% of the project management software market in 2024. Enterprises there leverage robust infrastructure and sizable IT budgets to roll out end-to-end project ecosystems. Microsoft recorded 16% revenue growth to USD 245 billion in 2024, supported by integrated project functions within Microsoft 365. Innovation hubs continue to pioneer AI modules, yet regional growth moderates as penetration nears saturation.

Asia-Pacific grows at 15.3% CAGR through 2030, the fastest across regions. China's SaaS segment expands near 30% annually, with multinationals installing integrated Salesforce and Azure stacks to manage cross-border initiatives. India's SaaS revenue is forecast to increase from USD 7.18 billion in 2023 to USD 62.93 billion by 2032, driven by cloud adoption and startup momentum. SMEs across Southeast Asia adopt local-language PM suites that embed regional compliance norms.

Europe posts steady gains as GDPR compels localization features, rewarding vendors offering EU data centers and advanced encryption. South America, and Middle East, and Africa now improve broadband and payment rails, nurturing cloud subscriptions previously held back by infrastructure gaps. Vendors anticipate double-digit uptake once connectivity costs fall further.

- Adobe Inc. (Workfront)

- AEC Software Inc.

- Asana Inc.

- Atlassian Corporation PLC

- Basecamp LLC

- Broadcom Inc. (Clarity PPM)

- ClickUp (Mango Technologies, Inc.)

- Microsoft Corporation

- Monday.com Ltd.

- Oracle Corporation

- Planview Inc.

- Procore Technologies Inc.

- SAP SE

- ServiceNow Inc.

- Smartsheet Inc.

- Teamwork.com Ltd.

- Trello Enterprise (Atlassian)

- Unit4 N.V.

- Wrike Inc. (Citrix Systems)

- Zoho Corporation Pvt Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first adoption for remote and hybrid project teams

- 4.2.2 Integration of PM platforms with enterprise SaaS stacks

- 4.2.3 SME uptake boosted by low-code / no-code configurability

- 4.2.4 AI-driven predictive analytics for schedule and cost variance

- 4.2.5 Vertical-specific PM suites (e.g., construction, healthcare)

- 4.2.6 ESG compliance reporting embedded in project workflows

- 4.3 Market Restraints

- 4.3.1 High migration and customization costs for legacy estates

- 4.3.2 Data-sovereignty and privacy concerns in multi-tenant clouds

- 4.3.3 Feature commoditization heightening vendor-lock-in risk

- 4.3.4 Change-management fatigue curbing large-scale roll-outs

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By End-user Industry

- 5.3.1 IT and Telecom

- 5.3.2 Healthcare

- 5.3.3 Construction and Infrastructure

- 5.3.4 BFSI

- 5.3.5 Government and Public Sector

- 5.3.6 Manufacturing

- 5.3.7 Others

- 5.4 By Subscription Type

- 5.4.1 Monthly Subscription

- 5.4.2 Annual Subscription

- 5.4.3 One-time License

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Nigeria

- 5.5.4.2.4 Rest of Africa

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 South Korea

- 5.5.5.5 ASEAN

- 5.5.5.6 Australia

- 5.5.5.7 New Zealand

- 5.5.5.8 Rest of Asia-Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adobe Inc. (Workfront)

- 6.4.2 AEC Software Inc.

- 6.4.3 Asana Inc.

- 6.4.4 Atlassian Corporation PLC

- 6.4.5 Basecamp LLC

- 6.4.6 Broadcom Inc. (Clarity PPM)

- 6.4.7 ClickUp (Mango Technologies, Inc.)

- 6.4.8 Microsoft Corporation

- 6.4.9 Monday.com Ltd.

- 6.4.10 Oracle Corporation

- 6.4.11 Planview Inc.

- 6.4.12 Procore Technologies Inc.

- 6.4.13 SAP SE

- 6.4.14 ServiceNow Inc.

- 6.4.15 Smartsheet Inc.

- 6.4.16 Teamwork.com Ltd.

- 6.4.17 Trello Enterprise (Atlassian)

- 6.4.18 Unit4 N.V.

- 6.4.19 Wrike Inc. (Citrix Systems)

- 6.4.20 Zoho Corporation Pvt Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

即時計劃管理軟體市場按類型、系統整合、部署類型、組織規模、使用者類型和最終用戶用途分類-2025-2032年全球預測線上計劃管理軟體市場按部署類型、組織規模、應用程式類型和最終用戶產業分類 - 全球預測(2025-2032 年)計劃管理人工智慧市場:按應用、元件、部署模式、最終用戶產業和組織規模分類-全球預測(2025-2032年)

即時計劃管理軟體市場按類型、系統整合、部署類型、組織規模、使用者類型和最終用戶用途分類-2025-2032年全球預測線上計劃管理軟體市場按部署類型、組織規模、應用程式類型和最終用戶產業分類 - 全球預測(2025-2032 年)計劃管理人工智慧市場:按應用、元件、部署模式、最終用戶產業和組織規模分類-全球預測(2025-2032年) 2025年全球計劃管理人工智慧市場報告2025年全球計劃管理軟體市場報告

2025年全球計劃管理人工智慧市場報告2025年全球計劃管理軟體市場報告 全球線上專案管理軟體市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測

全球線上專案管理軟體市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測 2025-2029年全球計劃管理市場中的人工智慧

2025-2029年全球計劃管理市場中的人工智慧 計劃管理中的人工智慧市場規模、佔有率、成長分析、按組件、部署模式、組織規模、應用、最終用途產業、地區、產業預測,2025 年至 2032 年

計劃管理中的人工智慧市場規模、佔有率、成長分析、按組件、部署模式、組織規模、應用、最終用途產業、地區、產業預測,2025 年至 2032 年 2025 年至 2033 年線上專案管理軟體市場報告(按部署模式、企業規模、垂直產業和地區分類)

2025 年至 2033 年線上專案管理軟體市場報告(按部署模式、企業規模、垂直產業和地區分類) 漏洞回報獎勵平台市場報告:趨勢、預測與競爭分析(至 2031 年)

漏洞回報獎勵平台市場報告:趨勢、預測與競爭分析(至 2031 年)