|

市場調查報告書

商品編碼

1851488

印度風力發電:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)India Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

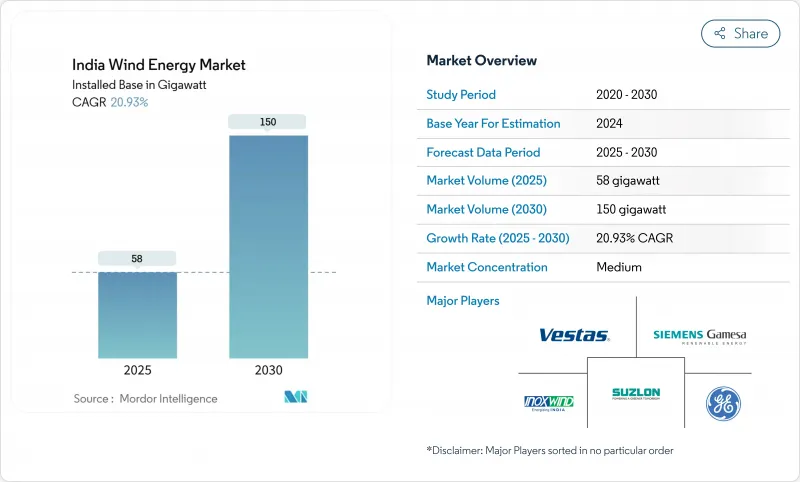

印度風力發電市場規模預計將從 2025 年的 58 吉瓦成長到 2030 年的 150 吉瓦,預測期(2025-2030 年)的複合年成長率為 20.93%。

這一發展勢頭得益於以500吉瓦非化石燃料目標為基礎的政策支持、企業購電協議的增加以及風能和太陽能混合發電項目的競標。資料中心營運商增加電網級採購、老舊風力渦輪機改造的復甦以及首筆離岸風電可行性缺口資金籌措進一步鞏固了成長前景。 2025年6月州際輸電豁免到期以及各州土地資源限制帶來的成本阻力構成了短期挑戰,但鑑於國內製造業的深度和對綠氫的需求,長期前景不應受到影響。

印度風力發電市場趨勢與洞察

加速泰米爾納德邦和古吉拉突邦風能和太陽能可再生發電捆綁式電力競標,以提高發電容量利用率

至2024年,混合能源競標將佔可再生能源總競標的43%,高於2020年的16%。在古吉拉突邦和泰米爾納德邦,每千瓦時2.58-2.67印度盧比的定價展現了其成本競爭力。到2025年,混合能源運作中裝置容量將達到7.7兆瓦,另有300兆瓦正在籌建中。這種模式透過匹配互補的發電特性來增強電網穩定性,確保印度風力發電市場在波動較大的負載曲線下保持強勁的需求。

為古吉拉突邦首輪4GW離岸風力發電計畫提供可行性缺口資金,將促進供應鏈投資

印度聯邦內閣提出的7,453億盧比一攬子計劃,其中包括600億盧比的港口建設資金,將縮小計劃和離岸風電計劃之間的電價差距。古吉拉突邦的坎貝灣和泰米爾納德邦沿海地區合計擁有70吉瓦的技術潛力,使離岸風力發電成為印度長期多元化發展的支柱。港口升級和專用輸電走廊的建設將加速單樁基礎、過渡段和高壓直流輸電線路等供應鏈的本地化。因此,印度的風力發電市場將擁有大量高容量係數的資產,以補充白天太陽能發電的不足。

卡納塔克邦和馬哈拉斯特拉邦的土地分配凍結導致陸上管道建設延誤

卡納塔克邦計劃在2024年新增1135兆瓦發電裝置容量,但邦級土地儲備的枯竭限制了計劃實施進度。儘管有關開放准入的監管改革改善了下游電力需求,但土地用途變更的多部門審批流程仍然漫長。太陽能競標競標進一步縮小了可用地塊的範圍。在新的土地租賃框架最終確定之前,這些瓶頸可能會減緩印度風力發電市場的建設步伐。

細分市場分析

到2024年,陸域風電將佔印度風力發電市場佔有率的100%,這得益於印度國內每年18吉瓦的渦輪機製造產能以及每千瓦時2.68-3.6印度盧比的極具競爭力的價格。離岸風電目前仍處於起步階段,但預計將以35%的複合年成長率成長,這得益於74.53兆印度盧比的資金籌措計畫以及超過40%的優異運轉率。因此,到2030年,印度離岸風力發電計劃的市場規模預計將從目前的小規模成長到兩位數吉瓦的水平。

較高的資本密集度和專業化的物流將使離岸風電的平準化成本在不計補貼的情況下維持在9-12印度盧比/千瓦時左右。擬議的64%本土化率規則將增強陸上風電的經濟效益,同時促進海上基礎設施和陣列的本地供應鏈發展。隨著時間的推移,規模經濟和以港口主導的製造群將縮小成本差距,預計未來十年印度風力發電市場將向陸上-陸下平衡的格局轉型。

印度風力發電市場報告按行業(陸上和海上)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速風能和太陽能混合可再生能源競標;提高泰米爾納德邦和古吉拉突邦的發電容量利用率

- 古吉拉特邦首輪4GW離岸風力發電專案可行性缺口資金籌措古吉拉突邦供應鏈投資

- 改造計畫將釋放5-15吉瓦老舊風電場的容量,用於安裝更大容量的風力渦輪機。

- 綠氫能政策推動工業叢集對高負載率風電的需求

- ISTS費用豁免持升了資源豐富的西部各州風電計劃的內部收益率

- 資料中心營運商尋求風能和太陽能的即時控制組合,企業購電協議(PPA)需求激增,這帶動了企業購電協議的激增。

- 市場限制

- 卡納塔克邦和馬哈拉斯特拉邦的土地分配凍結導致陸上管道建設延誤

- 坎貝灣離岸風力發電電網疏散通道延誤

- 渦輪機零件消費稅的上漲加劇了與太陽能發電的成本競爭

- 各邦電力公司(DISCOM)的銀行限制措施(能源供應低於30%)增加了經濟萎縮的風險。

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 按行業

- 陸上

- 按渦輪機容量

- 小於2兆瓦

- 2~3.5 MW

- 3.5兆瓦或以上

- 透過使用

- 實用規模

- 工業專屬式

- 商業設施

- 離岸

- 按安裝類型

- 固定底部

- 浮體式

- 按深度

- 淺水區(水深小於30公尺)

- 過渡段(30-60公尺)

- 深海(超過60公尺)

- 陸上

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名/佔有率)

- 公司簡介

- Inox Wind Limited

- Suzlon Energy Limited

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- General Electric Company

- Envision Energy

- Wind World(India)Ltd

- Tata Power Renewable Energy Ltd

- Enercon GmbH

- Senvion India

- ReNew Power(ReNew Energy Global PLC)

- Adani Green Energy Ltd

- JSW Energy-Mytrah Cluster

- Amp Energy India Pvt Ltd

- Greenko Group

- Siemens Energy AG

- Mingyang Smart Energy

- Nordex SE

- Leitwind Shriram Manufacturing Ltd

- GE T&D India Ltd

- SKF India

- Hitachi Energy India Ltd

- Bharat Heavy Electricals Ltd

- LM Wind Power(India)

第7章 市場機會與未來展望

The India Wind Energy Market size in terms of installed base is expected to grow from 58 gigawatt in 2025 to 150 gigawatt by 2030, at a CAGR of 20.93% during the forecast period (2025-2030).

Policy support under the 500 GW non-fossil target, rising corporate power-purchase agreements, and hybrid wind-solar auctions underpin this momentum. Increased grid-scale procurement by data-centre operators, resurgence in repowering of aging turbines, and the first offshore viability-gap funding tranche further strengthen growth prospects. Cost headwinds from the June 2025 expiry of interstate-transmission waivers and state-level land constraints pose near-term challenges but do not derail the long-term outlook, as domestic manufacturing depth and green-hydrogen demand create structural upside.

India Wind Energy Market Trends and Insights

Accelerated Hybrid Renewable Auctions Bundling Wind with Solar Enhancing Capacity Utilisation in Tamil Nadu & Gujarat

Hybrid tenders accounted for 43% of all renewable auctions in 2024, up from 16% in 2020. Tariffs of INR 2.58-2.67 / kWh in Gujarat and Tamil Nadu demonstrate cost competitiveness, while capacity-utilisation factors above 60% meet round-the-clock requirements for commercial consumers. Operational hybrid capacity stood at 7.7 GW in 2025 with a 30 GW pipeline, and NTPC's recent 1.2 GW award signals strong institutional backing. The approach enhances grid stability by matching complementary generation profiles, ensuring that the India wind energy market maintains robust demand across volatile load curves.

Viability-Gap Funding for Initial 4 GW Offshore Wind Round in Gujarat Catalyst for Supply-Chain Investments

The Union Cabinet's INR 74.53 billion package, including INR 6 billion for ports, narrows the tariff gap between onshore and offshore projects. Gujarat's Gulf of Khambhat and Tamil Nadu's coast jointly offer 70 GW technical potential, positioning offshore wind as a long-term diversification pillar. Port upgrades and dedicated evacuation corridors accelerate supply-chain localisation for monopiles, transition pieces, and HVDC export lines. As a result, the India wind energy market secures a foundation for high-capacity-factor assets that complement solar-heavy daytime generation.

Land Allotment Freeze in Karnataka & Maharashtra Slowing Onshore Pipeline

State-level land-bank depletion constrains project execution timelines despite Karnataka adding 1,135 MW in 2024. Regulatory reforms around open access improve downstream offtake, yet multi-agency clearances for land conversion remain protracted. Competing solar bids further tighten suitable parcels. These bottlenecks could slow the build rate for the India wind energy market until additional land-leasing frameworks are finalised.

Other drivers and restraints analyzed in the detailed report include:

- Repowering Scheme Opening 5-15 GW of Ageing Wind Farms for High-Capacity Turbines

- Green Hydrogen Policy Driving Demand for High-Load-Factor Wind Power in Industrial Clusters

- Delayed Grid Evacuation Corridors for Offshore Wind at Gulf of Khambhat

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore capacity accounted for 100% India's wind energy market share in 2024, supported by 18 GW of annual domestic turbine manufacturing capacity and competitive tariffs between INR 2.68-3.6/kWh. Offshore wind, although at a nascent stage, is forecast to expand at a 35% CAGR, underpinned by the INR 74.53 billion funding scheme and superior capacity factors exceeding 40%. As a result, the India wind energy market size for offshore projects could rise from a negligible base to a double-digit gigawatt level by 2030.

Higher capital intensity and specialised logistics keep offshore levelised costs near INR 9-12/kWh without subsidies. The draft 64% domestic-content rule strengthens onshore economics while seeding local supply chains for offshore foundations and arrays. Over time, scale economies and port-led manufacturing clusters are expected to narrow cost gaps, allowing the India wind energy market to transition toward a balanced onshore-offshore mix in the next decade.

India Wind Energy Market Report is Segmented by Sector (Onshore and Offshore). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Inox Wind Limited

- Suzlon Energy Limited

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- General Electric Company

- Envision Energy

- Wind World (India) Ltd

- Tata Power Renewable Energy Ltd

- Enercon GmbH

- Senvion India

- ReNew Power (ReNew Energy Global PLC)

- Adani Green Energy Ltd

- JSW Energy - Mytrah Cluster

- Amp Energy India Pvt Ltd

- Greenko Group

- Siemens Energy AG

- Mingyang Smart Energy

- Nordex SE

- Leitwind Shriram Manufacturing Ltd

- GE T&D India Ltd

- SKF India

- Hitachi Energy India Ltd

- Bharat Heavy Electricals Ltd

- LM Wind Power (India)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Hybrid Renewable Auctions Bundling Wind with Solar Enhancing Capacity Utilisation in Tamil Nadu & Gujarat

- 4.2.2 Viability-Gap Funding for Initial 4 GW Offshore Wind Round in Gujarat Catalyst for Supply-Chain Investments

- 4.2.3 Repowering Scheme Opening 5-15 GW of Ageing Wind Farms for High-Capacity Turbines

- 4.2.4 Green Hydrogen Policy Driving Demand for High-Load-Factor Wind Power in Industrial Clusters

- 4.2.5 ISTS Charge Waivers Boosting Wind Project IRRs in Resource-Rich Western States

- 4.2.6 Corporate PPAs Surge from Data-centre Operators Seeking RTC Wind-Solar Mix

- 4.3 Market Restraints

- 4.3.1 Land Allotment Freeze in Karnataka & Maharashtra Slowing Onshore Pipeline

- 4.3.2 Delayed Grid Evacuation Corridors for Offshore Wind at Gulf of Khambhat

- 4.3.3 Rising GST on Turbine Components Eroding Cost Competitiveness vs Solar

- 4.3.4 Banking Restrictions (<30% Energy) by State DISCOMs Increasing Curtailment Risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Onshore

- 5.1.1.1 By Turbine Capacity

- 5.1.1.1.1 Up to 2 MW

- 5.1.1.1.2 2 to 3.5 MW

- 5.1.1.1.3 Above 3.5 MW

- 5.1.1.2 By Application

- 5.1.1.2.1 Utility-scale

- 5.1.1.2.2 Captive Industrial

- 5.1.1.2.3 Commercial and Institutional

- 5.1.2 Offshore

- 5.1.2.1 By Installation Type

- 5.1.2.1.1 Fixed-Bottom

- 5.1.2.1.2 Floating

- 5.1.2.2 By Water Depth

- 5.1.2.2.1 Shallow (Below 30 m)

- 5.1.2.2.2 Transitional (30 to 60 m)

- 5.1.2.2.3 Deepwater (Above 60 m)

- 5.1.1 Onshore

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Inox Wind Limited

- 6.4.2 Suzlon Energy Limited

- 6.4.3 Siemens Gamesa Renewable Energy SA

- 6.4.4 Vestas Wind Systems A/S

- 6.4.5 General Electric Company

- 6.4.6 Envision Energy

- 6.4.7 Wind World (India) Ltd

- 6.4.8 Tata Power Renewable Energy Ltd

- 6.4.9 Enercon GmbH

- 6.4.10 Senvion India

- 6.4.11 ReNew Power (ReNew Energy Global PLC)

- 6.4.12 Adani Green Energy Ltd

- 6.4.13 JSW Energy - Mytrah Cluster

- 6.4.14 Amp Energy India Pvt Ltd

- 6.4.15 Greenko Group

- 6.4.16 Siemens Energy AG

- 6.4.17 Mingyang Smart Energy

- 6.4.18 Nordex SE

- 6.4.19 Leitwind Shriram Manufacturing Ltd

- 6.4.20 GE T&D India Ltd

- 6.4.21 SKF India

- 6.4.22 Hitachi Energy India Ltd

- 6.4.23 Bharat Heavy Electricals Ltd

- 6.4.24 LM Wind Power (India)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

風力發電基礎市場:依渦輪機朝向、安裝類型和應用分類-2026-2032年全球預測

風力發電基礎市場:依渦輪機朝向、安裝類型和應用分類-2026-2032年全球預測 2026年全球風力發電市場報告2026年全球風力發電設備物流市場報告

2026年全球風力發電市場報告2026年全球風力發電設備物流市場報告 風力發電基礎市場-全球產業規模、佔有率、趨勢、機會、預測:按選址、基礎類型、地區和競爭格局分類,2021-2031年

風力發電基礎市場-全球產業規模、佔有率、趨勢、機會、預測:按選址、基礎類型、地區和競爭格局分類,2021-2031年 全球風能市場:依組件、安裝地點、應用和地區劃分-市場規模、產業動態、機會分析和預測(2026-2035 年)風力發電轉換系統市場按組件、技術、安裝類型、功率容量、應用和最終用戶分類,全球預測(2026-2032)全球風能市場-按類型(海上和陸上)、最終用戶(工業、商業和住宅)、地區和競爭格局分類的產業規模、佔有率、趨勢、機會和預測(2021-2031年預測)

全球風能市場:依組件、安裝地點、應用和地區劃分-市場規模、產業動態、機會分析和預測(2026-2035 年)風力發電轉換系統市場按組件、技術、安裝類型、功率容量、應用和最終用戶分類,全球預測(2026-2032)全球風能市場-按類型(海上和陸上)、最終用戶(工業、商業和住宅)、地區和競爭格局分類的產業規模、佔有率、趨勢、機會和預測(2021-2031年預測) 風力發電市場規模、佔有率和成長分析:按組件、渦輪機額定功率、安裝量、技術、性別、最終用戶和地區分類 - 產業預測(2026-2033 年)風能救援系統市場-全球產業規模、佔有率、趨勢、機會和預測(按應用程式、類型、最終用戶、技術、地區和競爭細分,2020-2030 年)

風力發電市場規模、佔有率和成長分析:按組件、渦輪機額定功率、安裝量、技術、性別、最終用戶和地區分類 - 產業預測(2026-2033 年)風能救援系統市場-全球產業規模、佔有率、趨勢、機會和預測(按應用程式、類型、最終用戶、技術、地區和競爭細分,2020-2030 年) 風電轉換系統市場:2025-2030 年預測

風電轉換系統市場:2025-2030 年預測