|

市場調查報告書

商品編碼

1851456

奈米物聯網:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Internet Of Nano Things - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

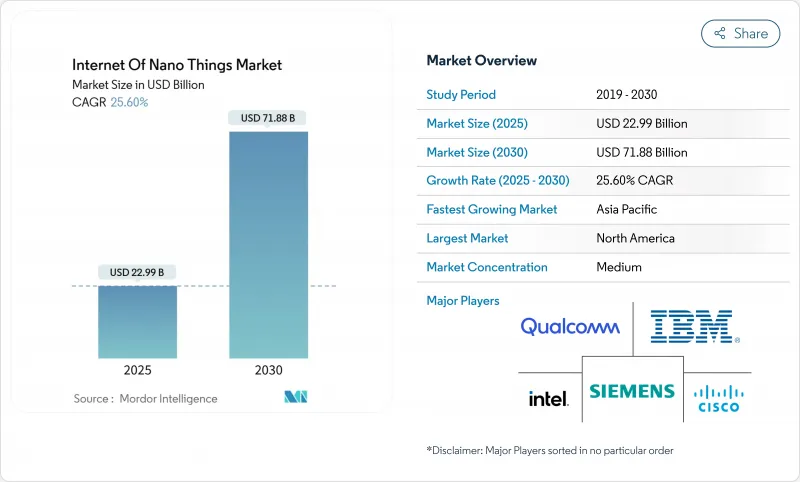

預計到 2025 年,奈米物聯網市場規模將達到 229.9 億美元,到 2030 年將達到 718.8 億美元,預測期(2025-2030 年)複合年成長率為 25.60%。

這一成長反映了兆赫波段奈米天線設計的商業化、超低功耗奈米碳管管感測器的部署,以及奈米級通訊協定快速融入主流無線網路。各國政府正在資助基於奈米感測器的疫情監測框架,而私人投資則加速了人工智慧主導的編配平台的發展,這些平台能夠將分子級數據轉化為可操作的洞察。儘管硬體支出仍佔總總支出的近一半,但隨著企業將分析置於設備之上,軟體平台的擴張速度明顯更快。從區域來看,北美在聯邦研究津貼和早期兆赫頻譜分配方面處於領先地位,而亞太地區則展現出最強勁的成長勢頭,因為半導體中心正在將奈米感測器網路納入其工業4.0藍圖。隨著半導體巨頭利用現有晶圓廠和新興企業部署顛覆性的分子通訊協定棧,競爭壓力正在加劇,但高昂的製造成本和分散的頻譜政策仍然是顯著的阻力。

全球奈米物聯網市場趨勢與洞察

奈米技術的快速發展使得超低功耗感測器成為可能。

基於奈米碳管的裝置能夠利用環境能量,克服了傳統電池的局限性,並縮短了維護週期。麻省理工學院的工程師已經展示了植物驅動的奈米感測器,它們透過光合作用產生自身能量,檢驗了其遠端部署的能源自主性。氮化硼奈米管纖維構成了耐熱網路,能夠在嚴苛的工業環境中保持性能劣化。結合人工智慧加速的材料發現技術(例如Material Nexus公司在無稀土永磁體方面的突破性進展),技術創新週期已從數年縮短至數月。這些進步催生了從精密農業到危險環境監測等廣泛的應用,推動了奈米物聯網市場的長期成長。

即時健康監測穿戴式裝置的需求日益成長

Nanowear公司奈米感測器心臟貼片獲得FDA批准,凸顯了奈米技術醫療設備在監管方面的重要性。採用奈米碳管薄膜製成的連續血糖監測儀,在保持皮膚貼片般隱蔽外形規格的同時,其精度已可媲美實驗室水平。多分析物貼片可同時監測電解質、乳酸和皮質醇水平,從而支持降低慢性病治療成本的預防保健模式。部署這些設備的醫療機構報告稱,敗血症的檢出率更高,重症監護室(ICU)住院時間更短,這進一步鞏固了醫療保健行業對不斷成長的奈米物聯網市場的重要貢獻。預計到2024年,該細分市場的收入佔有率將達到30.3%,顯示市場需求根深蒂固,其他產業也必須重視這一領域。

奈米尺度下嚴重的資料安全與隱私風險

奈米感測器缺乏傳統加密所需的運算餘量,這使其面臨巨大的攻擊面,可能危及醫院、工廠和市政網路的安全。植入式醫療奈米感測器尤其脆弱;被劫持的血糖監測儀可能篡改測量結果,危及患者健康。 GDPR 將奈米感測器數據視為高風險數據,並要求獲得明確同意,而這對於自主運作的亞毫米級設備而言難以實現。量子抗性輕量級加密技術仍處於概念驗證階段,進一步擴大了安全漏洞,並導致奈米物聯網市場的預期複合年成長率下降 4.3%。

細分市場分析

預計到2024年,硬體將佔奈米物聯網市場總收入的47.6%,該市場主要集中在關鍵的實體設備、天線和閘道器。然而,隨著分析平台利用大量的分子數據,軟體領域正以28.6%的複合年成長率蓬勃發展。服務領域雖然仍處於起步階段,但正經歷兩位數的成長,因為企業需要諮詢專業知識來將奈米設備與舊有系統整合。陶氏化學和卡維斯公司在熱感界面材料方面的合作,展現了專業知識如何轉化為利潤豐厚的服務領域。

軟體繁榮正在重新定義價值獲取方式。硬體商品化導致硬體淨利率萎縮,而管理數十億個終端的編配堆疊則需要高額授權。雲端供應商正在整合奈米設備API,吸引開發者使用整合安全、人工智慧和生命週期管理的平台。在預測期內,奈米物聯網市場規模及其軟體收入將縮小與硬體的差距,從而重塑整個生態系統的競爭格局。

醫療保健產業仍將是奈米感測器應用最廣泛的領域,預計2024年將佔總收入的30.3%,該產業將利用奈米感測器進行持續的生命徵象監測、植入監測和智慧藥物輸送。同時,智慧城市計畫到2030年將以27.6%的複合年成長率成長,市政當局將部署奈米感測器網路用於空氣品質分析、洩漏檢測和智慧交通控制。在製造業,嵌入生產線的奈米感測器可將即時分子資料傳輸到預測性維護系統;而物流公司則會在貨櫃內安裝奈米感測器,以檢驗低溫運輸合規性。

環保機構將採用奈米感測器浮標,以傳統感測器無法企及的十億分之一解析度檢測污染物。農業相關企業將噴灑植物組織奈米感測器,以便及早發現營養缺乏情況,從而減少化肥用量和水資源浪費。這些發展表明,垂直多元化正在加速奈米物聯網在實體經濟中的市場滲透。

奈米物聯網市場按組件(硬體、軟體、服務)、最終用戶(醫療保健、物流和運輸、國防和航太、製造業及其他)、通訊技術(電磁波、分子通訊、奈米RFID/NFC及其他)、部署模式(本地部署、雲端部署、混合部署)和地區進行細分。市場預測以美元計價。

區域分析

2024年,北美將維持38.6%的收入佔有率,這主要得益於聯邦津貼、兆赫頻段的早期分配以及具備奈米級生產能力的半導體晶圓廠的建立。美國國家標準與技術研究院(NIST)物聯網諮詢委員會將明確相關標準並加速商業試點計畫。然而,高昂的人事費用和資本支出正在擠壓淨利率,奈米製造工程師的人才儲備也面臨挑戰。美國將重點發展國防、航太和先進醫療植入,而加拿大則將投資於自然資源管理的環境監測。

到2030年,亞太地區將以28.1%的複合年成長率成長,這反映了該地區積極的工業4.0計劃、強大的電子供應鏈以及不斷擴大的5G覆蓋範圍。中國將透過將奈米感測器整合到製造和化學工廠中來提高產量比率和安全性,從而推動製造業採用奈米技術;而日本的醫療技術公司將率先開發生物相容性植入。韓國將在電訊展現領先地位,試辦建設支持6G的奈米網狀網路。區域各國政府正在補貼奈米研發,加速產品上市速度,並加劇市場競爭。由此產生的規模優勢將在本十年末縮小亞太地區和北美地區奈米物聯網市場規模之間的差距。

歐洲持續支持並影響塑造全球規範的資料隱私和永續性框架。 「地平線歐洲」計畫已累計1億歐元用於邊緣人工智慧和物聯網研究,其中一部分將用於奈米裝置互通性研究。德國正在精密製造業部署奈米感測器,英國則在測試基於石墨烯的健康貼片。南美洲以及中東和非洲等新興地區正選擇性地投資環境和基礎設施監測,利用奈米感測器以低生命週期成本實現高精度監測的優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 奈米技術的快速發展使得超低功耗感測器成為可能。

- 即時健康監測穿戴式裝置的需求日益成長

- 工業4.0和智慧製造的日益普及

- 5G/6G和邊緣運算基礎設施的普及

- 兆赫波段奈米天線突破性進展可降低訊號衰減

- 政府資助的利用奈米感測器的疫情監測網路

- 市場限制

- 奈米尺度下嚴重的資料安全與隱私風險

- 奈米製造的高資本成本和複雜性

- 應用於人體時,生物相容性和長期細胞毒性是需要考慮的問題。

- 缺乏標準化的兆赫頻率法規阻礙了其應用。

- 產業價值鏈分析

- 監管環境

- 技術展望

- 產業吸引力:波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 最終用戶

- 衛生保健

- 物流/運輸

- 國防/航太

- 製造業

- 能源與電力

- 環境監測

- 零售

- 農業

- 智慧城市和基礎設施

- 其他最終用戶

- 透過通訊技術

- 電磁

- 分子通訊

- Nano RFID/NFC

- 奈米感測器網路

- 奈米衛星通訊

- 其他

- 按部署模式

- 本地部署

- 雲

- 混合

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 馬來西亞

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Intel Corporation

- Cisco Systems, Inc.

- Qualcomm Technologies, Inc.

- Siemens AG

- Schneider Electric SE

- SAP SE

- Juniper Networks, Inc.

- Nokia Corporation

- Honeywell International Inc.

- Analog Devices, Inc.

- STMicroelectronics NV

- Nanoscale Components, Inc.

- NanoSensors, Inc.

- Agilent Technologies, Inc.

- TeraSense Group, Inc.

- Graphenea, Inc.

- Litmus Automation, Inc.

- ON Semiconductor Corporation

- Microchip Technology Inc.

- Camtek Ltd.

- NeuraLace Medical, Inc.

- Nanolike SAS

- Ambiq Micro, Inc.

- Synapse Wireless, Inc.

第7章 投資分析

第8章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The Internet of Nano Things Market size is estimated at USD 22.99 billion in 2025, and is expected to reach USD 71.88 billion by 2030, at a CAGR of 25.60% during the forecast period (2025-2030).

The surge reflects the commercialisation of terahertz-band nano-antenna designs, the roll-out of ultra-low power carbon-nanotube sensors, and the rapid convergence of nanoscale communication protocols with mainstream wireless networks. Governments are funding pandemic surveillance frameworks built on nanosensors, while private investment is accelerating AI-driven orchestration platforms that translate molecular-level data into actionable insight. Hardware continues to account for almost half of all spending, but software platforms are expanding at a markedly faster pace as enterprises prioritise analytics over devices. Regionally, North America leads on account of federal research grants and early terahertz spectrum allocation, yet Asia-Pacific exhibits the strongest growth as semiconductor hubs embed nanosensor networks into Industry 4.0 roadmaps. Competitive pressure is intensifying as semiconductor majors leverage existing fabs while start-ups introduce disruptive molecular communication stacks, but steep fabrication costs and fragmented spectrum policies remain notable headwinds.

Global Internet Of Nano Things Market Trends and Insights

Rapid Advancements in Nanotechnology Enabling Ultra-Low Power Sensors

Carbon-nanotube-based devices now harvest ambient energy, removing conventional battery constraints and slashing maintenance cycles. MIT engineers demonstrated plant-powered nanosensors that self-energize through photosynthesis, validating energy autonomy for remote deployments. Boron nitride nanotube fibres provide heat-tolerant networks that withstand harsh industrial settings without degradation. Coupled with AI-accelerated materials discovery, exemplified by Materials Nexus' rare-earth-free permanent magnet breakthrough, innovation cycles have shrunk from years to months. These advances unlock applications ranging from precision agriculture to hazardous-environment monitoring, underpinning the long-term growth of the Internet of Nano Things market.

Growing Demand for Real-Time Health Monitoring Wearables

FDA clearance of Nanowear's nanosensor cardiac patch underscores regulatory validation for nano-enabled medical devices. Continuous glucose monitors built on carbon-nanotube films now rival laboratory accuracy while retaining discreet, skin-patch form factors. Multi-analyte patches track electrolytes, lactate, and cortisol simultaneously, supporting preventive care models that lower chronic-disease costs. Hospitals integrating these devices report earlier sepsis detection and shorter ICU stays, reinforcing healthcare's contribution to the Internet of Nano Things market expansion. The sector's 30.3% revenue share in 2024 signals entrenched demand that other verticals must challenge.

Severe Data Security and Privacy Risks at Nanoscale

Nanosensors lack the compute headroom for traditional encryption, exposing attack surfaces that could compromise hospital, factory, or municipal networks. Implantable medical nanosensors are especially vulnerable; a hijacked glucose monitor can falsify readings, endangering patients. GDPR treats nanosensor data as high-risk, mandating explicit consent that is difficult to implement on autonomous sub-millimetre devices. Quantum-resistant lightweight ciphers remain at proof-of-concept stages, widening the security gap and exerting a negative 4.3% pull on forecast CAGR for the Internet of Nano Things market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Industry 4.0 and Smart Manufacturing

- Proliferation of 5G/6G and Edge Computing Infrastructure

- High Capital Costs and Complexity of Nano-Fabrication

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware generated 47.6% of 2024 revenue, anchoring the Internet of Nano Things market in essential physical devices, antennas, and gateways. Yet the software segment is racing ahead at a 28.6% CAGR as analytics platforms capitalise on torrents of molecular data. Services remain nascent but record double-digit growth because enterprises require consulting expertise to integrate nano-devices with legacy systems. Dow's collaboration with Carbice on thermal interface materials shows how specialised know-how is turning into high-margin service lines.

The software boom is redefining value capture: hardware margins compress as commoditisation sets in, while orchestration stacks that manage billions of endpoints command premium licences. Cloud vendors embed nano-device APIs, drawing developers into unified platforms that bundle security, AI, and lifecycle management. Over the forecast horizon, the Internet of Nano Things market size linked to software revenues is projected to narrow the gap on hardware, recalibrating competitive strategies across the ecosystem.

Healthcare contributed 30.3% of 2024 revenue and remains the largest adopter, leveraging nanosensors for continuous vitals monitoring, implant surveillance, and smart drug delivery. Smart-city programmes, however, will expand at 27.6% CAGR to 2030 as municipalities deploy nanosensor meshes for air-quality analytics, water-leak detection, and intelligent traffic control. In manufacturing, nanosensors embedded on production lines feed real-time molecular data into predictive-maintenance engines, while logistics firms fit nanosensors inside containers to verify cold-chain compliance.

Environmental agencies adopt nanosensor buoys that detect pollutants at parts-per-billion resolution, a capability classical sensors lack. Agriculture outfits scatter plant-tissue nanosensors that signal nutrient deficits early, cutting fertiliser usage and water waste. These deployments illustrate how vertical diversification is accelerating overall Internet of Nano Things market penetration across the real economy.

Internet of Nano Things Market is Segmented by Component (Hardware, Software, and Services), End-User (Healthcare, Logistics and Transportation, Defense and Aerospace, Manufacturing, and More), Communication Technology (Electromagnetic, Molecular Communication, Nano RFID/NFC, and More), Deployment Model (On-Premise, Cloud, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.6% revenue share in 2024, buoyed by federal grants, early terahertz spectrum allocation, and entrenched semiconductor fabs capable of nano-class production. The NIST IoT Advisory Board provides clarity around standards, accelerating commercial pilots. However, high labour costs and capital outlays squeeze margins, and the talent pipeline struggles to supply nano-manufacturing technicians. The United States focuses on defence, aerospace, and advanced healthcare implants, while Canada channels resources into environmental monitoring for natural-resource stewardship.

Asia-Pacific will post a 28.1% CAGR to 2030, reflecting aggressive Industry 4.0 incentives, deep electronics supply chains, and expansive 5G footprints. China drives manufacturing uptake, embedding nanosensors inside fabs and chemical plants to boost yield and safety, while Japan's med-tech firms pioneer bio-compatible nano implants. South Korea exploits telecom leadership to pilot 6G-ready nano-mesh networks. Regional governments subsidise nano R&D, compressing time-to-market and intensifying competition. The resulting scale advantages will narrow the Internet of Nano Things market size gap between Asia-Pacific and North America by decade end.

Europe remains influential, championing data privacy and sustainability frameworks that shape global norms. Horizon Europe has earmarked EUR 100 million for edge-AI and IoT research, with part allocated to nano-device interoperability. Germany deploys nanosensors in precision manufacturing, and the United Kingdom tests graphene-based health patches. Emerging regions in South America and the Middle East, and Africa invest selectively in environmental and infrastructure monitoring, capitalising on nanosensors' ability to deliver high granularity at lower lifecycle costs.

- IBM Corporation

- Intel Corporation

- Cisco Systems, Inc.

- Qualcomm Technologies, Inc.

- Siemens AG

- Schneider Electric SE

- SAP SE

- Juniper Networks, Inc.

- Nokia Corporation

- Honeywell International Inc.

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Nanoscale Components, Inc.

- NanoSensors, Inc.

- Agilent Technologies, Inc.

- TeraSense Group, Inc.

- Graphenea, Inc.

- Litmus Automation, Inc.

- ON Semiconductor Corporation

- Microchip Technology Inc.

- Camtek Ltd.

- NeuraLace Medical, Inc.

- Nanolike SAS

- Ambiq Micro, Inc.

- Synapse Wireless, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid advancements in nanotechnology enabling ultra-low power sensors

- 4.2.2 Growing demand for real-time health monitoring wearables

- 4.2.3 Increasing adoption of Industry 4.0 and smart manufacturing

- 4.2.4 Proliferation of 5G/6G and edge computing infrastructure

- 4.2.5 Emerging terahertz-band nano-antenna breakthroughs reducing signal attenuation

- 4.2.6 Government-funded pandemic surveillance networks leveraging nanosensors

- 4.3 Market Restraints

- 4.3.1 Severe data security and privacy risks at nanoscale

- 4.3.2 High capital costs and complexity of nano-fabrication

- 4.3.3 Biocompatibility and long-term cytotoxicity concerns in human body deployments

- 4.3.4 Lack of standardized terahertz spectrum regulations causing deployment delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By End-user

- 5.2.1 Healthcare

- 5.2.2 Logistics and Transportation

- 5.2.3 Defense and Aerospace

- 5.2.4 Manufacturing

- 5.2.5 Energy and Power

- 5.2.6 Environmental Monitoring

- 5.2.7 Retail

- 5.2.8 Agriculture

- 5.2.9 Smart Cities and Infrastructure

- 5.2.10 Other End-users

- 5.3 By Communication Technology

- 5.3.1 Electromagnetic

- 5.3.2 Molecular Communication

- 5.3.3 Nano RFID/NFC

- 5.3.4 Nano Sensor Networks

- 5.3.5 Nano Satellite Communication

- 5.3.6 Others

- 5.4 By Deployment Model

- 5.4.1 On-Premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Intel Corporation

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Siemens AG

- 6.4.6 Schneider Electric SE

- 6.4.7 SAP SE

- 6.4.8 Juniper Networks, Inc.

- 6.4.9 Nokia Corporation

- 6.4.10 Honeywell International Inc.

- 6.4.11 Analog Devices, Inc.

- 6.4.12 STMicroelectronics N.V.

- 6.4.13 Nanoscale Components, Inc.

- 6.4.14 NanoSensors, Inc.

- 6.4.15 Agilent Technologies, Inc.

- 6.4.16 TeraSense Group, Inc.

- 6.4.17 Graphenea, Inc.

- 6.4.18 Litmus Automation, Inc.

- 6.4.19 ON Semiconductor Corporation

- 6.4.20 Microchip Technology Inc.

- 6.4.21 Camtek Ltd.

- 6.4.22 NeuraLace Medical, Inc.

- 6.4.23 Nanolike SAS

- 6.4.24 Ambiq Micro, Inc.

- 6.4.25 Synapse Wireless, Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 White-Space and Unmet-Need Assessment