|

市場調查報告書

商品編碼

1851439

虛擬視網膜顯示器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Virtual Retinal Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

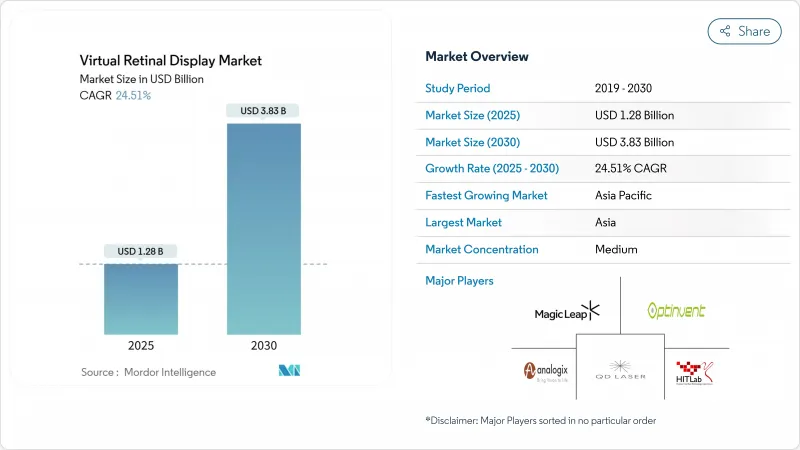

預計到 2025 年,虛擬視網膜顯示器市場規模將達到 12.8 億美元,到 2030 年將達到 38.3 億美元,複合年成長率為 24.51%。

輕量級視網膜投影技術正從實驗室走向主流生產,這主要得益於矽光電成本的下降、軍方訂單的加速成長以及已開發國家醫療機構對視力保健工作流程的數位轉型。從基於螢幕的擴增實境架構轉向無螢幕架構的轉變,消除了視角和環境光線的限制,同時實現了眼鏡級的外形尺寸。美國的「士兵彩色微型LED計畫」和日本的「老年人視力復健津貼」等採購計畫正在推動市場需求。同時,組件製造商正在對控制器、雷射和波導管進行小型化改造,以降低功耗並開拓消費性電子市場。

全球虛擬視網膜顯示器市場趨勢與洞察

軍用智慧頭盔對超緊湊型近眼顯示器的需求激增

國防專案優先考慮能夠躲避夜視探測器探測、但在日光下依然明亮的顯示器。美國的「輕型安全特種作戰顯示器」計劃正在資助一個原型機的研發,該原型機能夠直接照亮視網膜並消除外部漏光。 Kopin公司價值超過750萬美元的彩色MicroLED士兵顯示器合約凸顯了堅固耐用的視網膜投影技術如何滿足野戰應用所需的尺寸、重量和功耗要求。

在日本和荷蘭,用於輔助低視力患者的視網膜投影設備正迅速普及。

隨機對照試驗表明,視網膜投射雷射眼鏡產品能夠改善無法使用隱形眼鏡患者的視力,日本的保險公司和德國的診所也已開始報銷高階系統。簡化的歐盟醫療器材法規(EU-MDR)核准和瑞士優厚的保險覆蓋範圍為高階治療設備提供了支持,鼓勵製造商優先考慮以醫療為導向的設計。

高單價雷射掃描儀的平均售價給低於400美元的AR玻璃價格帶來了BOM壓力。

由於化合物半導體晶圓和精密MEMS掃描器缺乏大規模生產能力,RGB雷射引擎仍佔設備總成本的40%。汽車產業的經驗表明,AEC-Q100反射鏡也存在類似的定價僵化問題,迫使消費品牌要麼補貼光學元件,要麼放棄低於400美元的價格目標。

細分市場分析

2024年,顯示光源元件(主要是RGB雷射和MicroLED引擎)佔據了虛擬視網膜顯示器市場34.5%的佔有率。它們的領先地位歸功於光學效率與電池壽命之間的直接聯繫。眼動追蹤和校準模組正以26.7%的複合年成長率快速成長。隨著MEMS微鏡供應持續受限以及整合商轉向以軟體為中心的高精度監控,眼動追蹤虛擬視網膜顯示器的市場規模預計將會擴大。德克薩斯(TI)的DLPC8445控制器在驅動4K超高清顯示的同時,體積縮小了90%,證明後端晶片的發展速度與前端雷射不相上下。

DigiLens 和 Avegant 等公司將透明波導管與視網膜投影儀相結合的合作項目正在推動光學組合器和波導管的發展,而 Q-Pixel 的 10,000 PPI 可調多色 LED 則展現了單像素架構的優勢,降低了對準誤差並提高了產量比率。隨著垂直整合的加深,能夠同時掌控發光裝置和控制電子元件的元件供應商正在獲得永續的利潤。

到2024年,AR智慧眼鏡將佔據虛擬視網膜顯示器市場41%的收入佔有率,鞏固其作為核心硬體類別的地位。植入式/低視力輔助設備將因人口老化和保險報銷的推動而得到更廣泛的應用,預計到2030年將達到27.2%的複合年成長率。隨著臨床證據的不斷積累,虛擬視網膜顯示器在治療輔助器具領域的市場規模預計將持續成長。廣達電腦向Vuzix追加500萬美元投資以提高波導吞吐量等措施表明,契約製造的影響力日益增強。

獨立式視網膜投影頭顯在國防和工業模擬等細分領域仍佔有一席之地,因為在這些領域,長時間的任務需要專用電源組。儘管德克薩斯(TI) 已宣布將於 2025 年 3 月推出 DLP4620S-Q1 車載微鏡,但車載抬頭顯示器 (HUD) 的銷售成長仍然有限。這種市場失衡表明,消費者的便利性與專業技術之間存在矛盾,供應商必須平衡這兩種藍圖。

區域分析

預計亞太地區2024年將佔全球營收的27.8%,並在2030年前維持27.6%的年均成長率。這反映了該地區無與倫比的半導體晶圓廠、光學拋光供應鏈以及國內消費者的強勁需求。中國的晶圓代工獎勵正在降低雷射晶粒價格;日本的醫療保健系統正積極引進治療老齡化疾病的設備;韓國的顯示器巨頭正在將OLED產能與MicroLED試點生產線相結合;台灣地區則在不斷提高後端封裝的產量比率。

北美正充分利用國防預算和大學研發資源。虛擬視網膜顯示市場將受益於美國的大量微型LED合約以及《晶片法案》(CHIPS Act)支持的矽光電工廠,這些工廠將實現關鍵光學元件的本地化生產。加拿大簡化的醫療設備核准流程使其成為治療藥物首發上市的理想地區,而墨西哥的加工出口走廊則為北美地區的出口提供了免稅的最終組裝。

歐洲依然是監管領域的領頭羊。 1類雷射法規,加上Valeda光生物調節技術的先例,為全球製造商提供了一個可預測的框架。德國和瑞士正將精密光學加工和醫療技術投資相結合,以培育一個專為高價值醫療顯示器量身定做的生態系統。北歐的早期採用者正在測試面向生活方式的擴增實境(AR)眼鏡產品,從而獲得關於電池續航時間和人體工學的回饋。歐盟能源指令進一步推動供應商轉向低功耗設計,使歐洲企業在以永續性為導向的市場中擁有優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 軍用智慧頭盔對超緊湊型近眼顯示器的需求激增

- 在日本和德國,視網膜投影輔助設備正迅速受到低視力患者的歡迎。

- 美國矽光電成本下降推動AR穿戴裝置從基於螢幕轉向無螢幕轉變

- 歐盟一級雷射防護法規推動消費者接受該法規

- AI眼動追蹤模組的整合提升了北美身臨其境型訓練模擬器的效能

- 市場限制

- 高成本雷射掃描儀的ASP(平均售價)對400美元以下價格分佈的AR玻璃的BOM(物料清單)造成了壓力。

- 植入式/治療性VRD的複雜FDA與MDR核准路徑

- RGB雷射引擎延遲和散斑偽影會限制您的遊戲體驗。

- 用於抬頭顯示器的車用級MEMS後視鏡(AEC-Q100)供不應求

- 生態系分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 顯示光源(RGB雷射、微型LED、OLED)

- MEMS掃描單元

- 驅動和控制電子設備

- 眼動追蹤與校準模組

- 整合器和波導

- 其他

- 依產品類型

- 獨立式視網膜投影頭戴裝置

- 擴增實境智慧眼鏡

- 汽車抬頭顯示器

- 植入式/低視力輔助器具

- 其他

- 透過使用

- 醫學與生命科學

- 航太/國防

- 家用電器和遊戲

- 汽車與運輸

- 產業、教育和培訓

- 通過決議

- 高清(最高 720p)

- 全高清 (1080p)

- 2K-4K

- 4K以上解析度

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 其他南美洲

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avegant Corporation

- QD Laser, Inc.

- Magic Leap, Inc.

- Texas Instruments Incorporated

- Himax Technologies, Inc.

- eMagin Corporation

- Vuzix Corporation

- OmniVision Technologies, Inc.

- Sony Group Corporation

- Kopin Corporation

- STMicroelectronics NV

- MicroVision, Inc.

- SeeYa Technology Co., Ltd.

- Syndiant, Inc.

- DigiLens Inc.

- Lumus Ltd.

- Mojo Vision Inc.

- Analogix Semiconductor, Inc.

- Jenoptik AG

- Corning Incorporated

- Optivent

- Human Interface Technology Laboratory

第7章 市場機會與未來展望

The virtual retinal display market size is is estimated reached USD 1.28 billion in 2025 and is expected to attain USD 3.83 billion by 2030, registering a 24.51% CAGR.

Light-weight retinal projection is moving from experimental labs to mainstream production because silicon-photonics costs are declining, military orders are accelerating, and healthcare providers in developed economies are digitizing vision-care workflows. Transitioning from screen-based to screen-less augmented-reality architecture removes viewing-angle and ambient-light limits while enabling glasses-grade form factors. Procurement programs such as the U.S. Army's soldier color MicroLED initiative and Japan's aged-care vision rehabilitation funding are pulling demand forward. Meanwhile, component makers are shrinking controllers, lasers, and waveguides, which lowers power budgets and opens consumer electronics channels.

Global Virtual Retinal Display Market Trends and Insights

Surging Demand for Ultra-Compact Near-Eye Displays in Military Smart Helmets

Defense programs prioritize displays invisible to night-vision detectors yet bright in daylight. The U.S. Army's Light Secure Special Warfare Display project funds prototypes that illuminate the retina directly, eliminating outward light leakage. Kopin's soldier color MicroLED contracts worth more than USD 7.5 million underscore how ruggedized retinal projection meets size, weight, and power targets for field use.

Rapid Adoption of Retinal Projection Aids for Low-Vision Patients across Japan and DACH

Randomized trials show retinal laser eyewear improves acuity where lenses fail, prompting Japan's insurers and German clinics to reimburse high-end systems. Streamlined EU-MDR approvals and generous coverage in Switzerland support premium therapeutic devices, encouraging manufacturers to prioritize health-care-focused designs.

High Per-Unit Laser Scanner ASPs Causing BOM Pressures below USD 400 AR Glass Price-Point

RGB laser engines still consume up to 40% of total device cost because compound-semiconductor wafers and precision MEMS scanners lack mass-volume scale. Automotive experience shows similar price rigidity for AEC-Q100 mirrors, meaning consumer brands must subsidize optics or forego sub-USD 400 price targets.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Screen-Based to Screen-Less AR Wearables Driven by Silicon-Photonics Cost Drops in U.S.

- Vision-Safe Class-1 Laser Regulations Enabling Wider Consumer Adoption in EU

- Complex FDA and MDR Pathways for Implantable/Therapeutic VRDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Display Light Source elements, chiefly RGB laser and MicroLED engines, accounted for 34.5% of virtual retinal display market share in 2024. Their dominance stems from the direct link between optical efficiency and battery life. Eye-Tracking & Calibration Modules are expanding fastest at 26.7% CAGR, fueled by AI-enabled gaze analytics. The virtual retinal display market size for Eye-Tracking is expected to widen as MEMS mirrors remain supply-constrained, nudging integrators toward software-centric precision monitoring. Texas Instruments' DLPC8445 controller shrinks by 90% while driving 4K UHD, proving backend silicon keeps pace with front-end lasers.

Optical Combiners and Waveguides are advancing through collaborations such as DigiLens and Avegant, which merge transparent waveguides with retinal projectors. Meanwhile, Q-Pixel's 10,000 PPI tunable polychromatic LEDs hint at single-pixel architectures that could lower alignment tolerances and yield gains. As vertical integration deepens, component vendors that control both emitters and control electronics command sustainable margins.

AR Smart Glasses delivered 41% of virtual retinal display market revenue in 2024, cementing their role as the anchor hardware category. Implantable/Low-Vision Aids, though smaller today, will post a 27.2% CAGR to 2030 as aging populations and insurer reimbursement accelerate uptake. The virtual retinal display market size for therapeutic aids is poised to climb because clinical evidence keeps expanding. Investments such as Quanta Computer's additional USD 5 million in Vuzix improve waveguide throughput, signaling contract manufacturing's growing influence.

Standalone Retinal Projection Headsets persist in defense and industrial simulation niches where long-mission runtimes justify dedicated power packs. Automotive HUDs await qualified MEMS mirrors, which restrains volume scaling despite Texas Instruments' new DLP4620S-Q1 automotive micromirror introduction through Mouser in March 2025. Market skews show consumer convenience versus professional specialization, and suppliers must balance the two roadmaps.

The Virtual Retinal Display Market Report is Segmented by Component (Display Light Source, MEMS Scanning Unit, and More), Product Type (Standalone Retinal Projection Headsets, Augmented-Reality Smart Glasses, and More), Application (Medical and Life Sciences, Aerospace and Defense, and More), Resolution (HD (Upto 720p), Full HD (1080p), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 27.8% revenue share in 2024 and is forecast to compound 27.6% annually through 2030, reflecting unmatched semiconductor fabs, optics polishing supply chains, and domestic consumer appetites. China's foundry incentives push down laser-die pricing, and Japan's healthcare system actively deploys therapeutic devices for age-related degeneration. South Korea's display giants couple OLED competencies with MicroLED pilot lines, while Taiwan tightens backend packaging yields.

North America leverages defense budgets and university R&D. The virtual retinal display market benefits from the U.S. Army's successive microLED contracts and CHIPS-Act-backed silicon-photonics fabs that localize critical optics. Canada offers streamlined medical-device reviews, making it an attractive first-in-region for therapeutic launches, and Mexico's maquiladora corridors provide tariff-free final assembly for export within North America.

Europe remains regulatory pacesetter. Class-1 laser regulations, coupled with the Valeda photobiomodulation precedent, furnish predictable frameworks that manufacturers can replicate globally. Germany and Switzerland merge precision optics machining with med-tech funding, fostering an ecosystem tailored to high-value medical displays. Nordic early-adopters test lifestyle-oriented AR eyewear, providing feedback loops for battery life and ergonomics. EU energy directives additionally steer suppliers toward low-power designs, giving European players leverage in sustainability-minded markets.

- Avegant Corporation

- QD Laser, Inc.

- Magic Leap, Inc.

- Texas Instruments Incorporated

- Himax Technologies, Inc.

- eMagin Corporation

- Vuzix Corporation

- OmniVision Technologies, Inc.

- Sony Group Corporation

- Kopin Corporation

- STMicroelectronics N.V.

- MicroVision, Inc.

- SeeYa Technology Co., Ltd.

- Syndiant, Inc.

- DigiLens Inc.

- Lumus Ltd.

- Mojo Vision Inc.

- Analogix Semiconductor, Inc.

- Jenoptik AG

- Corning Incorporated

- Optivent

- Human Interface Technology Laboratory

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Ultra-Compact Near-Eye Displays in Military Smart Helmets

- 4.2.2 Rapid Adoption of Retinal Projection Aids for Low-Vision Patients across Japan and DACH

- 4.2.3 Shift from Screen-Based to Screen-Less AR Wearables Driven by Silicon-Photonics Cost Drops in U.S.

- 4.2.4 Vision-Safe Class-1 Laser Regulations Enabling Wider Consumer Adoption in EU

- 4.2.5 Integration of AI Eye-Tracking Modules Boosting Immersive Training Simulators in North America

- 4.3 Market Restraints

- 4.3.1 High Per-Unit Laser Scanner ASPs Causing BOM Pressures below USD 400 AR Glass Price-Point

- 4.3.2 Complex FDA and MDR Pathways for Implantable/Therapeutic VRDs

- 4.3.3 Latency and Speckle Artifacts in RGB-Laser Engines Limiting Gaming Experience

- 4.3.4 Shortage of Automotive-Grade MEMS Mirrors (AEC-Q100) for Head-Up Displays

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Display Light Source (RGB Laser, Micro-LED, OLED)

- 5.1.2 MEMS Scanning Unit

- 5.1.3 Driver and Control Electronics

- 5.1.4 Eye-Tracking and Calibration Module

- 5.1.5 Optical Combiner and Waveguide

- 5.1.6 Others

- 5.2 By Product Type

- 5.2.1 Standalone Retinal Projection Headsets

- 5.2.2 Augmented-Reality Smart Glasses

- 5.2.3 Automotive Head-Up Displays

- 5.2.4 Implantable/Low-Vision Aids

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Medical and Life Sciences

- 5.3.2 Aerospace and Defense

- 5.3.3 Consumer Electronics and Gaming

- 5.3.4 Automotive and Transportation

- 5.3.5 Industrial, Education and Training

- 5.4 By Resolution

- 5.4.1 HD (Upto 720p)

- 5.4.2 Full HD (1080p)

- 5.4.3 2K-4K

- 5.4.4 Above 4K

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avegant Corporation

- 6.4.2 QD Laser, Inc.

- 6.4.3 Magic Leap, Inc.

- 6.4.4 Texas Instruments Incorporated

- 6.4.5 Himax Technologies, Inc.

- 6.4.6 eMagin Corporation

- 6.4.7 Vuzix Corporation

- 6.4.8 OmniVision Technologies, Inc.

- 6.4.9 Sony Group Corporation

- 6.4.10 Kopin Corporation

- 6.4.11 STMicroelectronics N.V.

- 6.4.12 MicroVision, Inc.

- 6.4.13 SeeYa Technology Co., Ltd.

- 6.4.14 Syndiant, Inc.

- 6.4.15 DigiLens Inc.

- 6.4.16 Lumus Ltd.

- 6.4.17 Mojo Vision Inc.

- 6.4.18 Analogix Semiconductor, Inc.

- 6.4.19 Jenoptik AG

- 6.4.20 Corning Incorporated

- 6.4.21 Optivent

- 6.4.22 Human Interface Technology Laboratory

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment