|

市場調查報告書

商品編碼

1851390

環保水泥:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Green Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

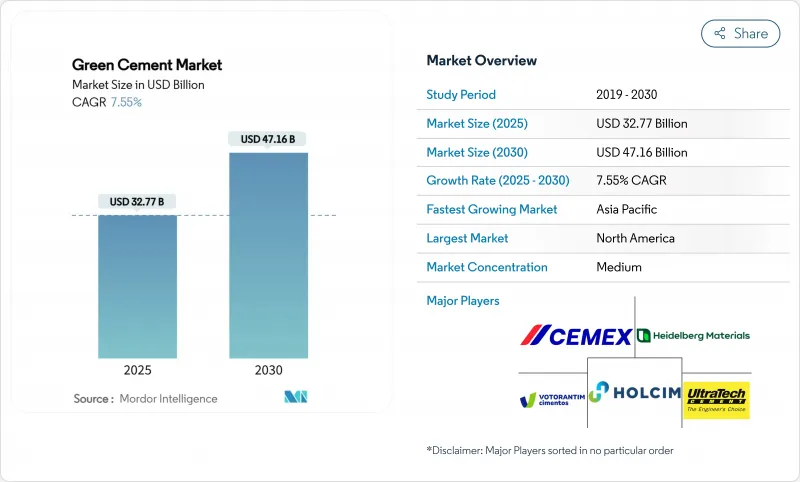

預計到 2025 年,環保水泥市場規模將達到 327.7 億美元,到 2030 年將達到 471.6 億美元,預測期(2025-2030 年)複合年成長率為 7.55%。

監管要求、不斷上漲的碳價以及有利於低碳材料的採購規則,正推動環保水泥市場從利基市場走向公共和私人計劃的主流選擇。飛灰基配方佔據最大的銷售佔有率,而計劃建設支出和與環境、社會及社會責任(ESG)相關的融資正在加速非住宅建築領域對綠色水泥的採用。亞太地區將迎來最快的成長,而北美地區由於政策實施較早和供應鏈成熟,將繼續保持其銷售量主導。隨著老牌水泥企業擴大其綠色水泥產品組合,以及專業生產商利用已簽訂的原料契約,市場競爭將保持溫和態勢。

全球環保水泥市場趨勢與洞察

全球脫碳指令及注重環境、社會及公司治理(ESG)的建築規範

強制性低碳採購政策正迅速推動市場需求從普通波特蘭水泥轉向檢驗的綠色水泥。加州的目標是到2035年將水泥產業的排放減少40%,並在2045年實現淨零排放,美國其他州也在做出類似的努力。歐盟修訂後的建築產品法規將從2024年起要求混凝土產品使用數位護照並揭露二氧化碳排放量,這將使擁有現有生命週期文件的生產商在競標中佔據優先地位。法國、丹麥、愛爾蘭和紐約州都已推出漸進式排放上限或清潔採購規則,使合規材料成為預設選項,而非更昂貴的選擇。隨著各州效仿這些開創性法規,環保水泥市場正獲得政策主導的成長底線,而傳統生產商只能透過維修窯爐或與專業供應商合作來應對這些成長。

碳價格上漲與排放交易機制

碳成本的增加改變了水泥熟料的經濟效益,將二氧化碳排放轉化為直接成本。歐盟排放權交易體係正在逐步取消免費的排放配額,促使水泥生產商加快開發低碳替代方案,否則將面臨利潤空間壓縮的風險。中國的國家碳交易平台現已涵蓋水泥,加劇了全球最大水泥生產國的成本壓力。隨著更多地區對碳排放定價,配套的膠凝材料將獲得相對競爭力,環保水泥市場相對於傳統產品將享有結構性的成本優勢。

建築商和承包商對施工品質的懷疑

由於養護時間延長、寒冷氣候下硬化速度減慢以及輔助材料在不同地區供應不穩定,一些建築商抵制規範變更。標準組織正努力以基於性能的指南取代強制性的混合料配比限制,但知識缺口仍然存在,尤其是在中小企業中。示範計劃和有針對性的培訓對於規範的廣泛應用仍然至關重要。

細分市場分析

預計到2024年,飛灰基配方將佔環保水泥市場佔有率的44.22%,這表明在燃煤殘渣豐富的地區,粉煤灰基配方是低碳替代方案。生產商利用其成熟的物流和良好的業績記錄來履行大型基礎設施合約和政府競標。然而,燃煤發電量的下降正在縮小未來的原料供應,迫使企業開採遺留的灰渣池或轉向使用石灰石和煅燒粘土混合物。 LC3技術能夠減少高達40%的排放,隨著實驗室測試檢驗其機械性能與普通矽酸鹽水泥相當,該技術正日益受到認可。矽粉基混凝土在高規格應用領域佔有一席之地,可提供適用於海洋和化學品密封結構的防滲混凝土。礦渣基替代品正面臨即將到來的供應變化,但在綜合鋼鐵廠附近仍具有應用價值。包括無機聚合物混凝土在內的新型接合材料化學技術正在透過先導計畫來推進,如果規模經濟效益得到改善,則可能使環保水泥市場多樣化。

多角化經營可以減少對單一輔助業務的過度依賴,並使生產商免受原料衝擊的影響。伐木灰占美國飛灰回收的10%,提高了供應安全性,但也增加了加工成本。因此,水泥生產商與煤灰回收營業單位之間的戰略協議在近期的交易中佔據了重要地位。隨著企業在技術可行性、排放目標和原料經濟性之間尋求平衡,礦渣研磨夥伴關係和黏土燒製合資企業也變得同樣重要。

區域分析

2024年,北美將佔全球銷售額的37.88%,這得益於聯邦和州政府的清潔採購法規、早期碳捕獲測試以及熟悉混合水泥的承包商。海德堡材料公司的米切爾碳捕獲與封存(CCS)計劃在30年內地質儲存超過5,000萬噸二氧化碳,顯示其基礎設施足以支持長期的產量承諾。供應情況因地區而異:中西部各州可利用其靠近煤灰盆地的優勢,而沿海各州則需要進口爐渣和煅燒粘土以滿足規格要求。

亞太地區到2030年將以8.22%的複合年成長率成為全球成長最快的地區,這主要得益於印度多年基礎建設規劃以及東南亞地區逐步收緊的監管政策。中國的整合舉措將促使各大集團升級其工廠,採用低碳軌道以應對房地產行業的逆風,從而維持營運許可。全球三分之二的高鐵網路位於該地區,因此需要符合更嚴格排放標準的混凝土,這將有利於環保水泥市場的發展,因為計劃需要補充軌道和車站的混凝土庫存。

歐洲兼具強而有力的氣候變遷政策和成熟的工業能力。愛爾蘭2024年強制所有國家級計劃使用低碳水泥,丹麥2025年設定的排放為7.1公斤二氧化碳當量/平方公尺/年,這些都樹立了具有影響力的標竿。儘管建築量有所波動,但碳定價無疑將擴大環保水泥水泥的市場規模,因為二氧化碳成本將促使競標評估傾向於低熟料混合料。中東和非洲地區也出現了新的需求,特別是海灣國家正在規劃建造氫能中心和大型公共。然而,在統一的指導方針訂定之前,標準的分散和現場經驗的匱乏將阻礙綠色水泥的推廣應用。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球脫碳指令與以ESG為中心的建築規範

- 碳價格上漲與排放交易機制

- 亞太地區的都市化浪潮對低碳材料的需求日益成長。

- 降低儲量豐富的輔助膠凝材料原料(飛灰、礦渣)的成本

- 氫燃料窯的商業化

- 市場限制

- 建築商和承包商對施工品質的懷疑

- 新興市場標準的片段化

- 由於煉鋼工藝轉向電弧爐/直接還原鐵工藝,爐渣供應量減少。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 粉煤灰基

- 礦渣基

- 石灰石基底

- 矽灰基

- 其他產品類型

- 按建築業

- 住宅

- 除了住房之外

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Adani Group

- Buzzi SpA

- CarbonCure Technologies Inc.

- Cemex SAB DE CV

- Cenin

- China National Building Material Group Corporation

- Ecocem

- Heidelberg Materials

- Hoffmann Green Cement Technologies

- Holcim

- JSW Cement

- Kiran Global Chem Limited.

- TAIHEIYO CEMENT CORPORATION

- UltraTech Cement Ltd.

- Votorantim Cimentos

第7章 市場機會與未來展望

The Green Cement Market size is estimated at USD 32.77 billion in 2025, and is expected to reach USD 47.16 billion by 2030, at a CAGR of 7.55% during the forecast period (2025-2030).

Regulatory mandates, rising carbon prices, and procurement rules that favor low-carbon materials move the green cement market from niche status to mainstream selection in public and private projects. Fly-ash-based formulations command the largest revenue share, while infrastructure spending and ESG-linked financing accelerate uptake across non-residential works. Asia-Pacific provides the fastest growth, whereas North America retains volume leadership because of early policy adoption and mature supply chains. Competitive intensity stays moderate as incumbent cement majors scale green portfolios and specialized producers leverage secured feedstock contracts.

Global Green Cement Market Trends and Insights

Global Decarbonization Mandates & ESG-Centric Building Codes

Mandatory low-carbon procurement policies drive immediate demand shifts from ordinary Portland cement to verified green formulations. California targets a 40% emissions cut for its cement sector by 2035 and net-zero by 2045, anchoring similar actions in other U.S. states. The EU's revised Construction Products Regulation obliges digital passports and CO2 disclosure for concrete from 2024, pushing producers already equipped with life-cycle documentation to the front of tender lists. France, Denmark, Ireland, and New York State have each introduced progressive emissions ceilings or Buy Clean rules that make compliant materials the default choice rather than a premium option. As jurisdictions replicate pioneering statutes, the green cement market gains a policy-driven growth floor that traditional producers can meet only by retrofitting kilns or partnering with specialized suppliers.

Rising Carbon Pricing & Emissions-Trading Schemes

Carbon costs alter clinker economics by turning CO2 into a direct expense. The EU Emission Trading System gradually withholds free allowances, prompting cement manufacturers to accelerate low-carbon substitutions or risk margin compression. China's national trading platform now covers cement, expanding cost pressure to the world's largest producer. As more regions price carbon, supplementary cementitious materials gain relative competitiveness, and the green cement market benefits from a structural cost advantage over legacy products.

Performance Scepticism Among Builders & Contractors

Some contractors resist specification changes, citing extended curing, cold-weather set delays, and inconsistent regional availability of supplementary materials. Standards bodies work to replace prescriptive mix limits with performance-based guidelines, yet knowledge gaps persist, especially in small and mid-size firms. Demonstration projects and targeted training remain essential for mainstream adoption.

Other drivers and restraints analyzed in the detailed report include:

- APAC Urbanization Surge Requiring Low-Carbon Materials

- Abundant SCM Feedstocks Lowering Costs

- Fragmented Standards in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fly-ash-based formulations kept a 44.22% green cement market share in 2024, underscoring their status as the default low-carbon substitute where coal-combustion residues remain abundant. Producers leverage mature logistics and well-documented performance to serve large infrastructure contracts and government tenders. However, declining coal generation narrows future feedstock pools, prompting companies to harvest legacy ash ponds or shift toward limestone-calcined clay blends. LC3 technology, able to trim emissions by up to 40%, gains visibility as laboratories validate mechanical parity with ordinary Portland cement. Silica-fume-based variants occupy high-specification niches, delivering impermeable concrete suited to marine and chemical containment structures. Slag-based alternatives struggle with impending supply shifts but retain relevance near integrated steelworks. Novel binder chemistries, including geopolymer concretes, progress through pilot projects that could diversify the green cement market if scale economics improve.

Growing diversification reduces over-reliance on any single supplementary stream and insulates producers from raw-material shocks. With harvested ash constituting 10% of recycled U.S. fly ash, supply security improves, yet processing costs rise. Strategic agreements between cement makers and utility coal-ash reclamation entities therefore feature prominently in recent deal flow. Slag-grinding partnerships and clay-calcination joint ventures become equally critical as companies balance technical feasibility, emissions objectives, and raw-material economics.

The Green Cement Market Report is Segmented by Product Type (Fly-Ash-Based, Slag-Based, Limestone-Based, Silica-Fume-Based, Other Product Types), Construction Sector (Residential, Non-Residential), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.88% of 2024 revenues, anchored by federal and state Buy Clean rules, early carbon-capture pilots, and high contractor familiarity with blended cements. Heidelberg Materials' Mitchell CCS project alone targets geological storage for more than 50 million t of CO2 over 30 years, signaling infrastructure that can underpin long-run volume commitments. Supply availability differs by region: Midwest states leverage proximity to coal-ash basins, while coastal areas import slag or calcined clay to meet specifications.

Asia-Pacific registers the fastest 8.22% CAGR to 2030, fueled by India's multi-year infrastructure pipeline and progressively stricter codes across Southeast Asia. China's consolidation efforts prompt large groups to upgrade plants with low-carbon lines to retain permits amid property-sector headwinds. Two-thirds of global high-speed rail networks reside in the region, requiring concrete that satisfies tightening emissions caps and boon the green cement market as projects replenish track and station stock.

Europe blends robust climate policy with mature industrial capabilities. Ireland's 2024 mandate for low-carbon cement in all state projects and Denmark's 2025 emissions ceiling of 7.1 kg CO2e/m2/year set influential benchmarks. Carbon pricing ensures that the green cement market size expands despite construction-volume volatility, as CO2 costs tilt bid evaluations toward low-clinker mixes. The Middle East and Africa witness emerging demand, especially in Gulf economies planning hydrogen hubs and large-scale public works, yet fragmented standards and limited on-site expertise slow penetration until harmonized guidelines mature.

- Adani Group

- Buzzi S.p.A.

- CarbonCure Technologies Inc.

- Cemex S.A.B DE C.V.

- Cenin

- China National Building Material Group Corporation

- Ecocem

- Heidelberg Materials

- Hoffmann Green Cement Technologies

- Holcim

- JSW Cement

- Kiran Global Chem Limited.

- TAIHEIYO CEMENT CORPORATION

- UltraTech Cement Ltd.

- Votorantim Cimentos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global decarbonisation mandates and ESG-centric building codes

- 4.2.2 Rising carbon pricing and emissions-trading schemes

- 4.2.3 APAC urbanisation surge requiring low-carbon materials

- 4.2.4 Abundant SCM feedstocks (fly-ash, slag) lowering costs

- 4.2.5 Commercialisation of hydrogen-fuelled kilns

- 4.3 Market Restraints

- 4.3.1 Performance scepticism among builders and contractors

- 4.3.2 Fragmented standards in emerging markets

- 4.3.3 Shrinking slag supply as steel shifts to EAF/DRI

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Fly-Ash-Based

- 5.1.2 Slag-Based

- 5.1.3 Limestone-Based

- 5.1.4 Silica-Fume-Based

- 5.1.5 Other Product Types

- 5.2 By Construction Sector

- 5.2.1 Residential

- 5.2.2 Non-Residential

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adani Group

- 6.4.2 Buzzi S.p.A.

- 6.4.3 CarbonCure Technologies Inc.

- 6.4.4 Cemex S.A.B DE C.V.

- 6.4.5 Cenin

- 6.4.6 China National Building Material Group Corporation

- 6.4.7 Ecocem

- 6.4.8 Heidelberg Materials

- 6.4.9 Hoffmann Green Cement Technologies

- 6.4.10 Holcim

- 6.4.11 JSW Cement

- 6.4.12 Kiran Global Chem Limited.

- 6.4.13 TAIHEIYO CEMENT CORPORATION

- 6.4.14 UltraTech Cement Ltd.

- 6.4.15 Votorantim Cimentos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球石灰石基環保水泥市場報告2026年全球礦渣基環保水泥市場報告

2026年全球石灰石基環保水泥市場報告2026年全球礦渣基環保水泥市場報告 環保水泥市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

環保水泥市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 環保水泥市場:按原料、製造流程、通路、應用和最終用戶分類-2026年至2032年全球預測

環保水泥市場:按原料、製造流程、通路、應用和最終用戶分類-2026年至2032年全球預測 環保水泥市場分析及預測(至2035年):依類型、產品、技術、應用、材料類型、製程、最終用戶、安裝類型、設備分類

環保水泥市場分析及預測(至2035年):依類型、產品、技術、應用、材料類型、製程、最終用戶、安裝類型、設備分類 環保水泥市場規模、佔有率、趨勢和預測:按產品類型、最終用途行業和地區分類,2026-2034年2026年全球環保水泥市場報告

環保水泥市場規模、佔有率、趨勢和預測:按產品類型、最終用途行業和地區分類,2026-2034年2026年全球環保水泥市場報告 綠色水泥市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、包裝規格、最終用戶、地區分類),競爭格局預測及機會(2020-2030年預測)

綠色水泥市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、包裝規格、最終用戶、地區分類),競爭格局預測及機會(2020-2030年預測) 全球環保水泥市場預測分析(2018-2034)日本綠色水泥市場報告(按產品類型(粉煤灰基、礦渣基、石灰石基、矽灰基等)、最終用途行業(住宅、非住宅、基礎設施)和地區分類,2025-2033 年

全球環保水泥市場預測分析(2018-2034)日本綠色水泥市場報告(按產品類型(粉煤灰基、礦渣基、石灰石基、矽灰基等)、最終用途行業(住宅、非住宅、基礎設施)和地區分類,2025-2033 年