|

市場調查報告書

商品編碼

1851361

歐洲自動導引運輸車(AGV):市場佔有率分析、產業趨勢、統計和成長預測(2025-2030 年)Europe Automated Guided Vehicle (AGV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

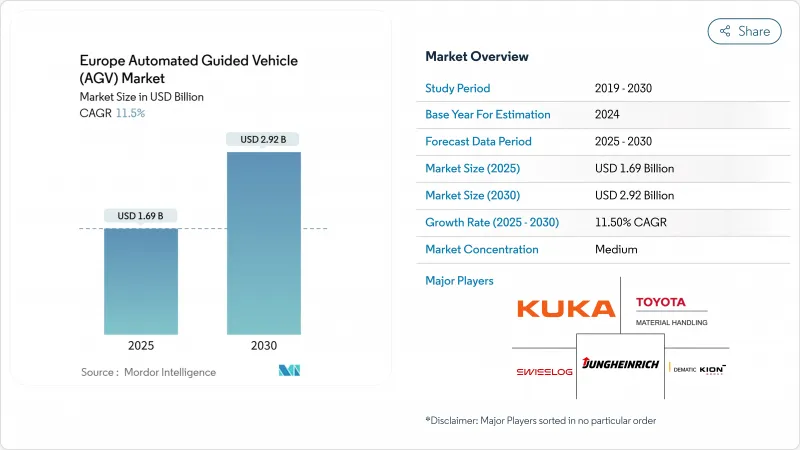

預計到 2025 年,歐洲 AGV 市場規模將達到 16.9 億美元,到 2030 年將達到 29.2 億美元,複合年成長率為 11.5%。

汽車產業的彈性製造措施、大規模港口自動化專案以及電子商務的持續擴張(需要高吞吐量的物流)是推動成長的主要動力。鋰離子動力傳動系統、5G賦能的車隊編配以及基於人工智慧的交通管理平台正在融合,以提高各設施的生產效率,同時滿足歐盟的脫碳目標。儘管德國在自動化領域的領先地位、荷蘭的港口計劃以及英國應對嚴重勞動力短缺的舉措都極大地促進了技術的普及,但射頻頻譜的分散和高昂的整合成本仍然阻礙著技術的普及速度。

歐洲自動導引運輸車(AGV)市場趨勢與洞察

歐洲都市區電子商務履約中心激增

都市區履約中心的快速成長正促使AGV(自動導引車)的設計重點轉向緊湊型佈局和全天候運作。 REWE集團位於馬德堡、耗資2.5億歐元的物流中心實現了50%的物流自動化,日處理包裹量達28.6萬件,充分展現了以AGV為中心的佈局所帶來的規模經濟效益。專業零售商也跟進:Dr. Max在義大利新建的倉庫利用行動機器人來支援線上銷售額55%的成長。隨著物流地產供應趨於穩定,零售商們正積極洽談能夠支援AGV快速充電基礎設施的自動化空間。

德國汽車工廠中面向工業4.0的彈性生產線

德國汽車製造商正在摒棄傳統的輸送機模式,轉而採用由AGV車隊協同運作的矩陣式生產方式。在賓士的白車身製造車間,約100輛庫卡AGV能夠即時自主地同步零件的流轉。 BMW工廠則利用人工智慧車隊控制軟體,根據車型組合的變化靈活調整運輸路線,從而避免停機。像杜爾的EcoProFleet這樣的專用AGV系統,將這一理念延伸至噴漆車間,使多種車型能夠共用資源運作。

中小企業系統整合和客製化的前期成本較高

許多中小企業安裝兩台自動導引車 (AGV) 的綜合報價超過 49,000 歐元,這阻礙了其更廣泛的市場滲透。雖然最佳化佈局可以將投資回收期縮短至不到八個月,但由於企業內部專業知識有限以及對補貼計劃了解不足,AGV 的普及程度並不均衡。經合組織的一項調查顯示,72% 的歐洲中小企業了解數位化帶來的好處,但由於缺乏技能和資金,只有 18% 的企業積極採用先進的自動化技術。

細分市場分析

自動化堆高機憑藉著與現有托盤工作流程的無縫相容性以及成熟的安全認證,預計到2024年將佔據歐洲AGV市場38%的佔有率。牽引車和牽引車仍然是大型製造工廠的標配,而組裝平台則支援汽車的準時制生產。受電子商務需求的推動,單元貨載具預計將以13.2%的複合年成長率成長,並在2030年前為歐洲AGV市場規模做出更大貢獻。

技術演進模糊了傳統界線。凱傲(KION)的KAnIS計劃展示了一款5G聯網的室外堆高機與室內車隊協同工作,將自動化覆蓋範圍擴展到了堆場區域。豐田與吉迪恩(Gideon)的合作則將堆高機傳統技術與人工智慧驅動的自主移動機器人(AMR)結合,揭示了供應商如何重新定位自身,轉向適應性強、用途廣泛的平台。

由於雷射導引在結構化路徑中展現出卓越的精度,預計到2024年,其市場佔有率將達到42%。視覺引導車輛正以14.6%的複合年成長率成長,它們利用SLAM和感測器融合技術,能夠自主繪製複雜環境地圖,並減少基礎設施維修。磁力路徑和雷射引導路徑仍然是低溫運輸隧道等關鍵路徑追蹤應用場景中不可或缺的組成部分。弗勞恩霍夫IPA研究所的自由導航研究表明,混合視覺-雷射系統能夠在保持毫米級精度的同時,無需固定反射器。 Innok Robotics公司將此模型擴展到戶外,透過融合LiDAR和運動追蹤器來應對崎嶇地形。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐洲都市區中履約中心如雨後春筍般出現

- 工業4.0使德國汽車工廠的彈性生產線成為可能。

- 人事費用上漲和西歐物流勞動力隊伍中的比例偏低

- 歐盟綠色交易為低排放物流設備提供獎勵措施

- 鹿特丹和安特衛普的港口自動化計劃促進了船舶自動導引車(AGV)的普及應用。

- 歐洲地平線計畫資助下一代群體導航演算法

- 市場限制

- 對於中小企業而言,系統整合和客製化的初始成本很高。

- 歐洲射頻頻譜碎片化導致高密度倉庫網路延遲。

- CE標誌和ISO 3691-4安全認證的前置作業時間較長

- 熟練的AGV系統整合商數量有限

- 價值/供應鏈分析

- 監理與技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

第5章 市場規模與成長預測

- 按車輛類型

- 自動堆高機

- 拖車/牽引車/拖輪

- 單元載體

- 組裝車輛

- 特殊用途/客製化

- 透過導航技術

- 雷射導

- 磁性/感應式

- 視覺指南

- 自然特徵/SLAM

- 依電池類型

- 鉛酸電池

- 鋰離子

- 鎳氫化物

- 超級電容/快速充電器

- 按操作模式

- 手動控制

- 混合/雙模式

- 完全自主

- 透過使用

- 運輸和配送

- 儲存和搜尋

- 組裝和套件

- 包裝和托盤堆垛

- 按最終用戶行業分類

- 車

- 飲食

- 零售與電子商務

- 電學

- 一般製造業

- 製藥

- 航太/國防

- 按國家/地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Swisslog Holding AG

- KUKA AG

- Jungheinrich AG

- Toyota Material Handling Europe AB

- Dematic(KION Group)

- SSI Schaefer AG

- Murata Machinery Ltd

- ABB Ltd

- Seegrid Corporation

- AGILOX Services GmbH

- Balyo SA

- Elettric 80 SpA

- Linde Material Handling GmbH

- STILL GmbH

- Mobile Industrial Robots(MiR)

- Fives Intralogistics SAS

- Euroimpianti SpA

- Oceaneering International(AGV Systems)

- Transbotics Corporation

- Amerden Inc.

第7章 市場機會與未來展望

The European AGV market size is valued at USD 1.69 billion in 2025 and is projected to reach USD 2.92 billion by 2030, reflecting an 11.5% CAGR.

Growth is driven by flexible manufacturing initiatives in the automotive sector, large-scale port automation programs, and sustained e-commerce expansion that demands high-throughput intralogistics. Lithium-ion powertrains, 5G-enabled fleet orchestration, and AI-based traffic management platforms are converging to raise overall equipment productivity while meeting EU decarbonization targets. Germany's automation leadership, the Netherlands' port projects, and the United Kingdom's response to acute labor shortages serve as powerful adoption catalysts, whereas fragmented RF spectrum and high integration costs still moderate deployment velocity.

Europe Automated Guided Vehicle (AGV) Market Trends and Insights

E-commerce fulfilment centres' surge across urban Europe

Rapid growth in urban fulfilment hubs is resetting AGV design priorities toward compact footprints and 24/7 availability. REWE Group's EUR 250 million logistics hub in Magdeburg automates 50% of intralogistics and handles 286,000 packages per day, proving the scale advantages of AGV-centric layouts. Specialty retailers follow suit; Dr. Max's new Italian warehouse uses mobile robots to sustain 55% online-sales growth. Combined with stabilizing logistics-real-estate vacancies, retailers now negotiate for automation-ready space that supports rapid AGV charging infrastructure.

Industry 4.0-enabled flexible manufacturing lines in German automotive plants

German automakers are dismantling rigid conveyor lines in favor of matrix production orchestrated by AGV fleets. Mercedes-Benz's body-in-white operations run nearly 100 KUKA vehicles that autonomously synchronize component flows in real time. BMW's factory implementations rely on AI fleet control software to adapt transport routes to model-mix changes without downtime. Purpose-built paint-shop AGVs such as Durr's EcoProFleet expand the concept to finishing lines, allowing multiple vehicle types to run on shared resources.

High up-front system integration & customisation costs for SMEs

Many SMEs confront integration quotations exceeding EUR 49,000 for a modest two-AGV installation, stalling broader market penetration. Although payback can arrive within eight months in optimized layouts, limited in-house expertise and low awareness of subsidy programs leave uptake uneven. OECD surveys show 72% of European SMEs understand digital benefits, yet only 18% actively deploy advanced automation due to skills and funding gaps.

Other drivers and restraints analyzed in the detailed report include:

- Labour-cost inflation & demographic shortages in Western Europe's logistics workforce

- EU Green Deal incentives for low-emission intralogistics equipment

- Fragmented European RF spectrum causing network latency in dense warehouses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated forklifts captured 38% of the European AGV market share in 2024, underpinned by drop-in compatibility with existing pallet workflows and mature safety certifications. Tow tractors and tug vehicles remain staples in large manufacturing campuses, whereas assembly line platforms support just-in-time automotive sequencing. Unit-load carriers, propelled by e-commerce fulfilment needs, are forecast to grow at a 13.2% CAGR, increasing their contribution to the European AGV market size through 2030.

Technical evolution blurs legacy categories: KION's KAnIS project demonstrates 5G-linked outdoor forklifts that coordinate with indoor fleets, extending automated coverage to yard areas. Toyota's alliance with Gideon blends forklift heritage with AI-driven AMRs, revealing how suppliers reposition toward adaptable multi-purpose platforms.

Laser guidance commanded 42% share in 2024 thanks to proven precision in structured aisles. Vision-guided vehicles, growing at 14.6% CAGR, leverage SLAM and sensor fusion to self-map unpredictable environments, reducing infrastructure retrofits. Magnetic and inductive paths persist in critical path-following use cases such as cold-chain tunnels. Free-navigation research at Fraunhofer IPA shows how hybrid vision-laser stacks eliminate fixed reflectors while preserving millimetric accuracy. Innok Robotics extends this model outdoors with LiDAR plus motion-tracker fusion for rough terrain.

The European AGV Market Report is Segmented by Vehicle Type (Automated Forklift, Unit-Load Carrier, and More), Navigation Technology (Laser Guided, Magnetic/Inductive Guided, and More), Battery Type (Lead-Acid, Lithium-Ion, Nickel-Metal Hydride, and More), Mode of Operation (Manual Override, Hybrid/Dual-Mode, and More), Application, End-User Industry, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Swisslog Holding AG

- KUKA AG

- Jungheinrich AG

- Toyota Material Handling Europe AB

- Dematic (KION Group)

- SSI Schaefer AG

- Murata Machinery Ltd

- ABB Ltd

- Seegrid Corporation

- AGILOX Services GmbH

- Balyo SA

- Elettric 80 SpA

- Linde Material Handling GmbH

- STILL GmbH

- Mobile Industrial Robots (MiR)

- Fives Intralogistics SAS

- Euroimpianti SpA

- Oceaneering International (AGV Systems)

- Transbotics Corporation

- Amerden Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfilment Centres Surge Across Urban Europe

- 4.2.2 Industry 4.0 Enabled Flexible Manufacturing Lines in German Automotive Plants

- 4.2.3 Labour-Cost Inflation and Demographic Shortages in Western Europes Logistics Workforce

- 4.2.4 EU Green Deal Incentives for Low-Emission Intralogistics Equipment

- 4.2.5 Port Automation Projects in Rotterdam and Antwerp Boosting Maritime AGV Adoption

- 4.2.6 Horizon Europe Funding for Next-Gen Swarm Navigation Algorithms

- 4.3 Market Restraints

- 4.3.1 High Up-front System Integration and Customisation Costs for SMEs

- 4.3.2 Fragmented European RF Spectrum Causing Network Latency in Dense Warehouses

- 4.3.3 Lengthy CE-Mark and ISO 3691-4 Safety Certification Lead-Times

- 4.3.4 Limited Availability of Skilled AGV Systems Integrators

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vehicle Type

- 5.1.1 Automated Forklift

- 5.1.2 Tow / Tractor / Tug

- 5.1.3 Unit-Load Carrier

- 5.1.4 Assembly Line Vehicle

- 5.1.5 Special-Purpose / Custom

- 5.2 By Navigation Technology

- 5.2.1 Laser Guided

- 5.2.2 Magnetic / Inductive Guided

- 5.2.3 Vision Guided

- 5.2.4 Natural Feature / SLAM

- 5.3 By Battery Type

- 5.3.1 Lead-acid

- 5.3.2 Lithium-ion

- 5.3.3 Nickel-Metal Hydride

- 5.3.4 Super-capacitor / Fast-Charge

- 5.4 By Mode of Operation

- 5.4.1 Manual Override

- 5.4.2 Hybrid / Dual-Mode

- 5.4.3 Fully Autonomous

- 5.5 By Application

- 5.5.1 Transportation and Distribution

- 5.5.2 Storage and Retrieval

- 5.5.3 Assembly and Kitting

- 5.5.4 Packaging and Palletising

- 5.6 By End-User Industry

- 5.6.1 Automotive

- 5.6.2 Food and Beverage

- 5.6.3 Retail and E-commerce

- 5.6.4 Electronics and Electrical

- 5.6.5 General Manufacturing

- 5.6.6 Pharmaceuticals

- 5.6.7 Aerospace and Defence

- 5.7 By Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 France

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Netherlands

- 5.7.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Swisslog Holding AG

- 6.4.2 KUKA AG

- 6.4.3 Jungheinrich AG

- 6.4.4 Toyota Material Handling Europe AB

- 6.4.5 Dematic (KION Group)

- 6.4.6 SSI Schaefer AG

- 6.4.7 Murata Machinery Ltd

- 6.4.8 ABB Ltd

- 6.4.9 Seegrid Corporation

- 6.4.10 AGILOX Services GmbH

- 6.4.11 Balyo SA

- 6.4.12 Elettric 80 SpA

- 6.4.13 Linde Material Handling GmbH

- 6.4.14 STILL GmbH

- 6.4.15 Mobile Industrial Robots (MiR)

- 6.4.16 Fives Intralogistics SAS

- 6.4.17 Euroimpianti SpA

- 6.4.18 Oceaneering International (AGV Systems)

- 6.4.19 Transbotics Corporation

- 6.4.20 Amerden Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

自動導引車市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、導航技術、應用、組件、電池類型、地區和競爭格局分類,2020-2030年預測

自動導引車市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、導航技術、應用、組件、電池類型、地區和競爭格局分類,2020-2030年預測 小型AGV市場按類型、導航技術、有效載荷能力、應用和最終用戶分類-2025年至2032年全球預測自動導引車軟體市場:2025-2032年全球預測(依應用產業、軟體類型、部署類型和公司規模分類)自動導引運輸車市場(按組件、車輛類型、導航技術、負載容量、最終用戶和分銷管道)—2025-2032 年全球預測

小型AGV市場按類型、導航技術、有效載荷能力、應用和最終用戶分類-2025年至2032年全球預測自動導引車軟體市場:2025-2032年全球預測(依應用產業、軟體類型、部署類型和公司規模分類)自動導引運輸車市場(按組件、車輛類型、導航技術、負載容量、最終用戶和分銷管道)—2025-2032 年全球預測 自動導引車的全球市場

自動導引車的全球市場 全球自動導引運輸車市場預測(2025-2030)

全球自動導引運輸車市場預測(2025-2030) 物流中的 AGV 和 AMR - 全球市場佔有率和排名、2025-2031 年總體銷售和需求預測

物流中的 AGV 和 AMR - 全球市場佔有率和排名、2025-2031 年總體銷售和需求預測 自動導引運輸車的全球市場:各產品類型,各電池類型,各導航技術,各用途,終端各用戶業界,各地區 - 市場規模,產業動態,機會分析與預測(2025年~2033年)

自動導引運輸車的全球市場:各產品類型,各電池類型,各導航技術,各用途,終端各用戶業界,各地區 - 市場規模,產業動態,機會分析與預測(2025年~2033年) 日本自動導引車市場報告(按類型、營運模式、導航技術、應用、產業和地區)2025-2033自動導引車市場規模、佔有率、趨勢及預測(按類型、營運模式、導航技術、應用、產業和地區),2025 年至 2033 年

日本自動導引車市場報告(按類型、營運模式、導航技術、應用、產業和地區)2025-2033自動導引車市場規模、佔有率、趨勢及預測(按類型、營運模式、導航技術、應用、產業和地區),2025 年至 2033 年