|

市場調查報告書

商品編碼

1851358

智慧眼鏡:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Smart Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

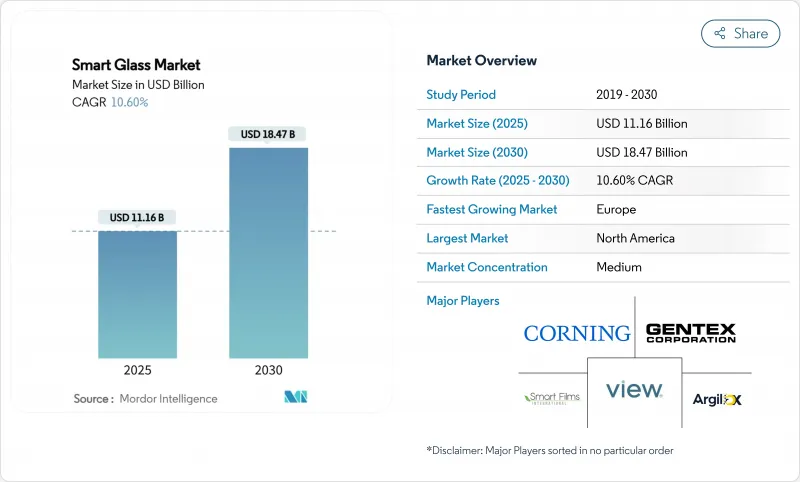

預計到 2025 年,智慧眼鏡市場規模將達到 111.6 億美元,到 2030 年將達到 184.7 億美元,年複合成長率為 10.60%。

這一發展趨勢的驅動力來自強制性能源性能法規、電致變色效率的提升以及汽車優質化,這些因素縮短了該技術的投資回收期。商業地產業主優先考慮控制暖通空調成本,汽車製造商將動態天窗捆綁到高利潤配置車型中,材料科學家則專注於研發可降低製造成本的無電極裝置。同時,政府對先進製造和5G賦能建築幕牆的獎勵也為智慧玻璃市場拓展了機會。

全球智慧眼鏡市場趨勢與洞察

嚴格的綠建築標準與維修強制令

強制性外牆性能基準值,例如加州2025年建築能源效率標準,正催生對電致變色建築幕牆的迫切需求。電致變色幕牆在U值和太陽能熱增益係數方面均優於傳統嵌裝玻璃。 2024年修訂的《國際節能規範》消除了權衡取捨的漏洞,提高了玻璃性能基準,與上一周期相比,節能幅度達9.8%。歐洲的類似措施,包括荷蘭的混合爐舉措,正在強化以合規為導向的採購週期,從而刺激維修活動。隨著業主看到尖峰時段冷卻負荷降低、獲得綠色金融合格以及資產價值提升,智慧玻璃市場可望持續受益於監管方面的利多因素。

在高階汽車嵌裝玻璃和天窗領域迅速普及

汽車製造商正引入動態光控車頂,以區分不同的車廂並降低空調負荷。雷諾的Solarbay PDLC天窗在實現同級領先的透光率的同時,也使用了近50%的回收材料。 AGC基於SPD技術的Wonder Light Roof天窗應用於梅賽德斯-奔馳S-Class小轎車,可降低空調需求和廢氣二氧化碳排放。現代的奈米冷卻膜在測試車輛中將車內溫度降低了12.33°C,標誌著其正走向主流應用。由於汽車設計週期為3-5年,成本節約也將波及建築領域,進而擴大智慧玻璃市場的潛在用戶群。

與傳統嵌裝玻璃相比,初始成本較高

電致變色窗的成本在每平方公尺180至250美元之間,而標準窗的成本僅為每平方公尺20至30美元。分析師認為,215平方公尺(20平方英尺)是實現大規模替代的臨界點,這引發了一場創新競賽。無電極電致變色原型透過剝離氧化銦錫層,已將成本降低至每平方公尺80美元。等離子體增強化學沉澱技術可望在年產量達到140萬平方公尺的情況下,將成本降至每平方公尺5.26美元左右。雖然隨著安裝人員技術的日益熟練,安裝的複雜性正在降低,但價格阻力仍然是成本敏感型智慧玻璃市場最大的限制因素。

細分市場分析

到2024年,電致變色解決方案將佔據智慧玻璃市場43.00%的佔有率。其低功耗運作、漸層著色和5萬次循環壽命等優勢,使其成為大型建築幕牆和企業園區的首選。預計電致變色智慧玻璃市場將從2025年的48億美元成長到2030年的77億美元,複合年成長率(CAGR)為9.8%。從線上濺鍍到全固體化學製程的成本降低藍圖,確保了資本支出預算的可預測性。同時,混合光伏玻璃正以18.50%的複合年成長率快速成長,其採用透明有機太陽能電池,在丹麥的CitySolar計劃中,該電池的效率已達到12.3%。 Next Energy Technologies公司估計,這些面板可以在保持建築透明度的同時,滿足典型辦公大樓25%的用電需求,使混合玻璃成為現有電致變色技術的顛覆者。

懸浮粒子裝置產品在駕駛座、火車車廂和豪華轎車等對亞秒切換要求極高的場所中佔有一席之地。聚合物分散液晶窗作為低壓隱私隔間,正逐漸被醫療病房和會議室所採用。感溫變色和光致變色技術主要應用於被動式氣候環境,而無線安裝則較符合改裝預算的要求。因此,此技術體系呈現出兩極化的特點:電致變色技術用於滿足能源需求,混合光伏技術用於打造淨零能耗建築幕牆,而懸浮粒子裝置(SPD)和聚合物分散液晶(PDLC)技術則適用於速度和隱私保護等應用情境。

到2024年,商業房地產應用將佔總收入的38.20%,這主要得益於智慧玻璃在辦公大樓和零售商店的廣泛應用。在該領域,節能、最佳化採光以及ESG認證等優勢使其溢價物有所值。預計商業房地產智慧玻璃市場規模將以9.6%的複合年成長率成長,從2025年的42.7億美元成長到2030年的67.5億美元。然而,醫療保健領域預計將以17.50%的複合年成長率快速成長,因為感染控制通訊協定優先考慮非接觸式隱私保護。加護治療病房正在採用即時不透明的PDLC面板以減少窗簾清洗次數,而精神科病房則正在採用防碎動態玻璃,以兼顧病患監護和尊嚴。

汽車嵌裝玻璃仍然是第三大收入來源,動態天窗可以有效補充耗電量高的空調系統,尤其是在豪華車和電動車領域。住宅領域的應用進展緩慢,但稅收優惠和模組價格的下降正在改變高性能住宅的投資回報率。航太、鐵路和船舶領域正在穩步推進,消費性電子產業也正在嘗試使用微型電致變色螢幕和擴增實境(AR)頭戴裝置。

智慧玻璃市場報告按技術類型(電致變色、感溫變色、光致變色、其他)、最終用戶(汽車、航空電子、船舶、零售、其他)、控制模式(有線開關/牆板、遙控/射頻控制器、調光面板/滑塊、其他)、應用(建築幕牆/幕牆、室內隔間/隱私面板、其他)和地區進行細分。

區域分析

2024年,北美地區佔全球銷售額的34.70%,這主要得益於加州建築規範提高了嵌裝玻璃基準值,以及聯邦《CHIPS法案》為高純度玻璃工廠提供的獎勵。康寧在紐約投資3.15億美元擴建熔融石英生產線,體現了該地區供應鏈的日益成熟,縮短了前置作業時間,並提供五年服務保固。此外,原始設備製造商(OEM)對全景天窗的需求以及聯邦政府設施的公私合作維修專案也支撐了該地區的智慧玻璃市場。

到2030年,亞太地區將以14.60%的複合年成長率實現最快增速,主要得益於中國京東方投資88億美元的OLED產業園、日本的5G建築幕牆試點計畫以及韓國的電動車玻璃升級。福耀等中國製造商正在新增58億元的車規級產能,擴大規模經濟效益,降低售價。儘管氧化鎢前驅體的相關法規構成供應風險,但地方政府正在加速本地開採和回收利用,以增強策略自主性。

在更嚴格的能源性能證書(EPC)評級和維修補貼的支持下,歐洲正穩步發展。聖戈班的低碳ORAE玻璃和AGC Interpane的多站點部署,都反映了該地區對再生材料和淨零排放製造的重視。然而,不斷上漲的電費和重疊的授權框架正在降低大眾住宅的盈利,從而推動了對商業大廈和高階維修的需求。這些動態共同維持了地域多元化的市場動態。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 嚴格的綠建築法規與維修強制令

- 在高階汽車嵌裝玻璃和天窗領域迅速普及

- 降低商業不動產業者的能源成本

- 面向智慧建築的物聯網玻璃感測器平台

- 相容於 5G/毫米波的低損耗建築幕牆解決方案

- 新冠疫情後對抗菌、非接觸式表面的需求

- 市場限制

- 與傳統嵌裝玻璃相比,初始成本較高

- 極端氣候下的可靠性問題

- 大型EC建築幕牆的EMI輻射合規限值

- 特種EC前驅供應瓶頸

- 價值鏈分析

- 監管環境

- 技術展望

- 技術概覽

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 依技術類型

- 電致變色

- 懸浮顆粒裝置(SPD)

- 聚合物分散液晶(PDLC)

- 感溫變色

- 光致變色

- 混合動力和太陽能

- 最終用戶

- 車

- 建築設計 - 住宅

- 建築 - 商業

- 航空電子設備

- 海洋

- 鐵路

- 消費性電子產品和穿戴式裝置

- 醫療機構

- 其他最終用戶

- 透過控制模式

- 有線開關/牆板

- 遠端/射頻控制器

- 調光面板/滑桿

- 智慧型手機/語音助手

- 基於感測器的自動控制

- 透過使用

- 建築幕牆和幕牆

- 室內隔間和隱私面板

- 天窗、採光窗、屋頂嵌裝玻璃

- 鏡子和展示

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AGC Inc.

- Compagnie de Saint-Gobain SA(SageGlass)

- Guardian Glass LLC

- View Inc.

- Halio International SA

- Gentex Corporation

- Corning Incorporated

- Nippon Sheet Glass Co. Ltd.(NSG)

- Polytronix Inc.

- Research Frontiers Inc.

- Pleotint LLC

- EControl-Glas GmbH

- BOE Technology Group Co.

- Hitachi Chemical Co.

- Merck KGaA(liquid-crystal materials)

- Smart Films International

- uniteGlass(CNBM)

- Pro Display/Intelligent Glass

- Magic Film Factory

- Argil Inc.

第7章 市場機會與未來展望

The smart glass market stands at USD 11.16 billion in 2025 and is forecast to post USD 18.47 billion by 2030, expanding at a 10.60% CAGR.

This trajectory is propelled by mandatory energy-performance codes, electrochromic efficiency gains, and premium automotive adoption that shortens technology payback cycles. Commercial landlords are prioritizing HVAC cost control, automotive OEMs are bundling dynamic sunroofs into high-margin trims, and materials scientists are converging on electrode-free devices that lower production costs. Simultaneously, government incentives for advanced manufacturing and 5G-ready facades are enlarging the smart glass market opportunity set.

Global Smart Glass Market Trends and Insights

Stringent Green-Building Codes and Retrofit Mandates

Mandatory envelope performance thresholds such as California's 2025 Building Energy Efficiency Standards are creating non-discretionary demand for electrochromic facades that outperform conventional glazing on U-factor and Solar Heat Gain Coefficient criteria. The 2024 International Energy Conservation Code revision delivers 9.8% incremental savings versus the prior cycle, eliminating trade-off loopholes and elevating glass performance baselines. Similar measures in Europe, including the Netherlands' hybrid-furnace initiative, reinforce a compliance-driven procurement cycle that lifts retrofit activity. As owners witness lower peak cooling loads, green-finance eligibility, and enhanced asset values, the smart glass market gains a durable regulatory tailwind.

Rapid Adoption in Premium Automotive Glazing and Sunroofs

Automakers are deploying dynamic light-control roofs to differentiate cabins and trim HVAC loads. Renault's Solarbay PDLC sunroof supplies segmental opacification while using nearly 50% recycled content. AGC's SPD-based Wonderlite roof on the Mercedes S-Class Coupe cuts air-conditioning demand and lowers tailpipe CO2. Hyundai's Nano Cooling Film shows mainstream migration by shaving interior temperatures by 12.33 °C in pilot fleets. Automotive design cycles of 3-5 years accelerate cost degression that cascades into the building sector, expanding the smart glass market addressable base.

High Upfront Cost vs. Conventional Glazing

Electrochromic windows still price at USD 180-250 m2 against USD 20-30 m2 for standard units. Analysts peg USD 215 m2 (USD 20 ft2) as the crossover point for mass substitution, prompting an innovation race. Electrode-free electrochromic prototypes have sliced costs toward USD 80 m2 by stripping indium-tin-oxide layers. Plasma-enhanced chemical vapor deposition promises costs near USD 5.26 m2 at 1.4 million m2 annual scale. Installation complexity is receding as contractor familiarity grows, but price resistance remains the foremost limiting factor in cost-sensitive slices of the smart glass market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Cost Savings for Commercial Real-Estate Operators

- IoT-Ready Glass-as-a-Sensor Platforms for Smart Buildings

- Reliability Issues in Extreme Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrochromic solutions dominated 2024 with 43.00% smart glass market share. Their low-power operation, gradual tinting, and proven 50,000 cycle life make them the default choice for large facades and corporate campuses. The smart glass market size for electrochromic products is projected to expand from USD 4.80 billion in 2025 to USD 7.70 billion by 2030 at a 9.8% CAGR. Cost-out roadmaps ranging from in-line sputtering to all-solid-state chemistries keep capex budgets predictable. Meanwhile, hybrid photovoltaic glass is scaling at an 18.50% CAGR, leveraging transparent organic photovoltaics that already hit 12.3% cell efficiency in Denmark's CitySolar project. NEXT Energy Technologies estimates these panels could offset 25% of typical office demand while retaining architectural clarity, positioning hybrids as the disruptor that challenges electrochromic incumbency.

Suspended Particle Device products maintain a niche where sub-second switching is critical-cockpits, rail cabins, and luxury sedans. Polymer-Dispersed Liquid Crystal windows are penetrating healthcare suites and conference rooms as low-voltage privacy partitions. Thermochromic and photochromic variants stay limited to passive climates, yet their wiring-free installation appeals to retrofit budgets. The technology stack is therefore bifurcating: electrochromic for energy mandates and hybrid PV for net-zero facades, with SPD and PDLC covering speed and privacy use cases.

Commercial real-estate applications captured 38.20% of 2024 revenue through broad office and retail uptake. The segment relied on energy savings, daylight optimization, and ESG credentialing to justify premium costs. Smart glass market size for commercial real estate is forecast to grow at 9.6% CAGR, moving from USD 4.27 billion in 2025 to USD 6.75 billion in 2030. Healthcare, however, secures the steepest 17.50% CAGR as infection-control protocols privilege touch-free privacy. Intensive-care wards deploy instant-opaque PDLC panels to reduce curtain laundering, while psychiatric units harness break-resistant dynamic glass to balance patient oversight with dignity.

Automotive glazing remains the third revenue pillar, particularly within luxury and electric vehicles, where dynamic skylights offset battery-draining HVAC. Residential uptake is slower, but tax incentives and lower module prices are shifting the ROI narrative for high-performance homes. Aerospace, rail, and marine progress steadily, albeit off smaller bases, and consumer electronics experiment with miniaturized electrochromic screens and AR headsets.

Smart Glass Market Report is Segmented by Technology Type (Electrochromic, Thermochromic, Photochromic, and More), End User (Automotive, Avionics, Marine, Retail, and More), Control Mode (Wired Switch / Wall Panel, Remote / RF Controller, Dimming Panel / Slider, and More), Application (Facades and Curtain Walls, Interior Partitions and Privacy Panels, and More), and Geography.

Geography Analysis

North America anchored 34.70% of 2024 revenue as California's building code raised glazing baselines and the federal CHIPS Act funnelled incentives to high-purity glass fabs. Corning's USD 315 million fused-silica expansion in New York exemplifies local supply-chain maturation that lowers lead times and underwrites five-year service warranties. The regional smart glass market is also buoyed by OEM demand for panoramic roofs and public-private retrofit programmes targeting federal properties.

Asia Pacific charts the fastest 14.60% CAGR through 2030, propelled by China's BOE USD 8.8 billion OLED campus, Japan's 5G facade pilots, and South Korea's EV-glass upgrades. Chinese producers such as Fuyao are adding CNY 5.8 billion of auto-grade capacity, amplifying economies of scale that compress selling prices. While tungsten-oxide precursor restrictions pose supply risk, regional governments are accelerating localised mining and recycling to fortify strategic autonomy.

Europe advances at a stable pace underpinned by stricter EPC ratings and renovation-wave subsidies. Saint-Gobain's low-carbon ORAE glass and AGC Interpane's multi-site expansion validate a regional focus on recycled content and net-zero manufacturing. However, elevated electricity prices and overlapping permitting frameworks dampen return profiles in mass-market housing, steering demand toward commercial towers and premium retrofits. Together, these dynamics sustain a geographically diversified smart glass market footprint.

- AGC Inc.

- Compagnie de Saint-Gobain S.A. (SageGlass)

- Guardian Glass LLC

- View Inc.

- Halio International SA

- Gentex Corporation

- Corning Incorporated

- Nippon Sheet Glass Co. Ltd. (NSG)

- Polytronix Inc.

- Research Frontiers Inc.

- Pleotint LLC

- EControl-Glas GmbH

- BOE Technology Group Co.

- Hitachi Chemical Co.

- Merck KGaA (liquid-crystal materials)

- Smart Films International

- uniteGlass (CNBM)

- Pro Display / Intelligent Glass

- Magic Film Factory

- Argil Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent green-building codes and retrofit mandates

- 4.2.2 Rapid adoption in premium automotive glazing and sunroofs

- 4.2.3 Energy-cost savings for commercial real-estate operators

- 4.2.4 IoT-ready glass-as-a-sensor platforms for smart-buildings

- 4.2.5 5G/mm-wave friendly, low-loss facade solutions

- 4.2.6 Post-COVID demand for antimicrobial, touch-free surfaces

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. conventional glazing

- 4.3.2 Reliability issues in extreme climates

- 4.3.3 EMI-emission compliance limits for large EC facades

- 4.3.4 Supply bottlenecks for specialty EC precursors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Technology Snapshot

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology Type

- 5.1.1 Electrochromic

- 5.1.2 Suspended Particle Device (SPD)

- 5.1.3 Polymer-Dispersed Liquid Crystal (PDLC)

- 5.1.4 Thermochromic

- 5.1.5 Photochromic

- 5.1.6 Hybrid and Photovoltaic

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Architectural - Residential

- 5.2.3 Architectural - Commercial

- 5.2.4 Avionics

- 5.2.5 Marine

- 5.2.6 Rail

- 5.2.7 Consumer Electronics and Wearables

- 5.2.8 Healthcare Facilities

- 5.2.9 Other End Users

- 5.3 By Control Mode

- 5.3.1 Wired Switch / Wall Panel

- 5.3.2 Remote / RF Controller

- 5.3.3 Dimming Panel / Slider

- 5.3.4 Smartphone / Voice Assistant

- 5.3.5 Sensor-Based Automatic Control

- 5.4 By Application

- 5.4.1 Facades and Curtain Walls

- 5.4.2 Interior Partitions and Privacy Panels

- 5.4.3 Sunroofs, Skylights and Roof Glazing

- 5.4.4 Mirrors and Displays

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Turkey

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Qatar

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Compagnie de Saint-Gobain S.A. (SageGlass)

- 6.4.3 Guardian Glass LLC

- 6.4.4 View Inc.

- 6.4.5 Halio International SA

- 6.4.6 Gentex Corporation

- 6.4.7 Corning Incorporated

- 6.4.8 Nippon Sheet Glass Co. Ltd. (NSG)

- 6.4.9 Polytronix Inc.

- 6.4.10 Research Frontiers Inc.

- 6.4.11 Pleotint LLC

- 6.4.12 EControl-Glas GmbH

- 6.4.13 BOE Technology Group Co.

- 6.4.14 Hitachi Chemical Co.

- 6.4.15 Merck KGaA (liquid-crystal materials)

- 6.4.16 Smart Films International

- 6.4.17 uniteGlass (CNBM)

- 6.4.18 Pro Display / Intelligent Glass

- 6.4.19 Magic Film Factory

- 6.4.20 Argil Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

智慧玻璃市場:2026-2032年全球市場預測(按玻璃類型、功能、控制方式、安裝方式、形狀、應用和分銷管道分類)

智慧玻璃市場:2026-2032年全球市場預測(按玻璃類型、功能、控制方式、安裝方式、形狀、應用和分銷管道分類) 2026-2030年全球智慧眼鏡市場

2026-2030年全球智慧眼鏡市場 智慧眼鏡市場規模、佔有率和趨勢分析報告:按類型、作業系統、鏡片著色技術、應用、連接方式、地區和細分市場預測(2026-2033 年)

智慧眼鏡市場規模、佔有率和趨勢分析報告:按類型、作業系統、鏡片著色技術、應用、連接方式、地區和細分市場預測(2026-2033 年) 智慧眼鏡市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、鏡框形狀、分銷管道、地區和競爭格局分類,2021-2031年

智慧眼鏡市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、鏡框形狀、分銷管道、地區和競爭格局分類,2021-2031年 智慧玻璃和自適應窗戶系統市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析智慧玻璃市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年智慧玻璃和智慧窗戶市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析

智慧玻璃和自適應窗戶系統市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析智慧玻璃市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年智慧玻璃和智慧窗戶市場預測至2034年—按技術、應用、最終用戶和地區分類的全球分析 智慧玻璃市場報告:按技術、控制方法、應用和地區分類(2026-2034 年)

智慧玻璃市場報告:按技術、控制方法、應用和地區分類(2026-2034 年) 2026年全球智慧玻璃市場報告2026年全球電致變色智慧玻璃與窗戶市場報告

2026年全球智慧玻璃市場報告2026年全球電致變色智慧玻璃與窗戶市場報告