|

市場調查報告書

商品編碼

1939050

智慧標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smart Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

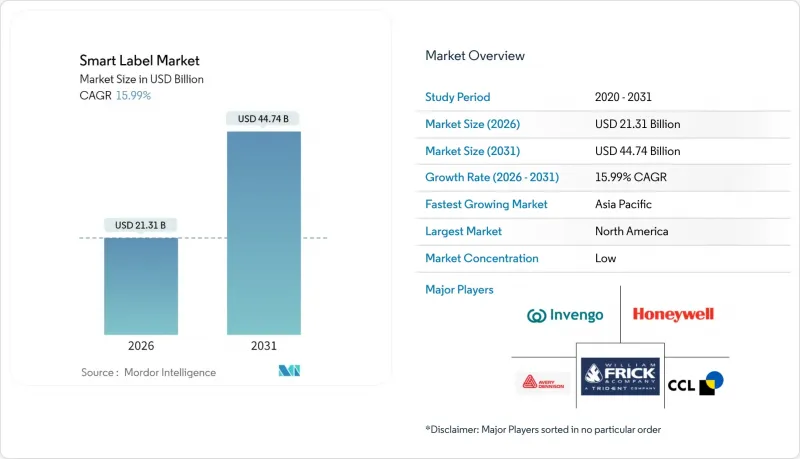

預計到 2026 年,智慧標籤市場規模將達到 213.1 億美元,高於 2025 年的 183.8 億美元。

預計到 2031 年將達到 447.4 億美元,2026 年至 2031 年的複合年成長率為 15.99%。

這一成長是由監管要求、無線射頻識別 (RFID) 和近距離場通訊 (NFC) 技術的進步以及對端到端供應鏈透明度日益成長的需求共同推動的。美國食品藥物管理局 (FDA) 的《藥品供應鏈安全法案》下的藥品序列化、歐盟的《包裝和包裝廢棄物法規》(PPWR)(其中包含數位產品護照的概念)以及沃爾瑪等零售商主導的RFID 項目,共同促成了強制性合規標準的建立。為了因應這些標準,各公司正在整合雲端分析、區塊鏈認證和環境物聯網感測器,將被動標籤轉化為數據豐富的資產,從而實現跨行業的即時庫存可見度、動態定價和狀態監測。

全球智慧標籤市場趨勢與洞察

擴大RFID在庫存可見性方面的應用

沃爾瑪強制要求數千個庫存單位(SKU)配備超高頻(UHF)RFID標籤,這迫使供應商改造生產線,推動了整個產業對RAIN RFID編碼解決方案的投資。供應商將獲得持續的庫存可視性,並可直接連接到製造執行系統(MES),透過數位雙胞胎減少物料短缺並提高排產效率。高通計畫將RAIN RFID嵌入智慧型手機,這意味著不久之後,每台消費性電子設備都將具備讀取功能,從而無需固定的掃描器基礎設施,並加速小規模零售商的採用。同時,更小的天線將實現3米的讀取範圍,從而打造無縫結帳區域,提升客戶體驗。

藥品供應鏈中對防偽措施的需求日益成長

當《藥品供應鏈安全法案》(DSCSA)於2024年11月全面生效時,貿易夥伴將被要求在產品交付前檢驗序列化識別碼。這推動了標籤升級,整合了近場通訊(NFC)晶片、區塊鏈加密和電子紙顯示器,以實現防篡改和劑量資訊顯示。例如,Ynvisible公司的ConnectedLabel每年可對超過一百萬個藥品包裝進行近乎即時的溫度追蹤。在美國以外,印度正在強制要求在暢銷藥品上使用QR碼,這表明序列化正從一項合規措施轉變為一項保障患者安全的差異化因素。

小規模零售商的初始硬體和整合成本較高

電子貨架標籤(ESL)價格昂貴,每個標籤售價11-12美元,如果要在成千上萬個SKU上部署,則需要大量的資金投入。小規模零售商還需要預算銷售點(POS)系統升級和員工培訓費用,儘管電子貨架標籤具有潛在的勞動力成本節省優勢,但這些因素仍然會減緩其普及速度。訂閱模式正在興起,但仍處於起步階段。

細分市場分析

到2025年,RFID將佔據智慧標籤市場37.86%的佔有率,這得益於其在零售和物流領域成熟的擴充性。目前規模較小的NFC預計將以19.52%的複合年成長率成長,這主要得益於智慧型手機全球普及帶來的「檢驗」體驗。因此,NFC相關的智慧標籤市場規模(以絕對值以金額為準)將實現最快成長,尤其是在奢侈品認證領域,區塊鏈整合賦予了其防篡改功能。電子商品防盜系統(EAS)將保持穩定,而感測標籤在低溫運輸和環境監管應用領域正蓬勃發展。總體而言,技術轉型正從被動識別轉向多功能感測器和互動工具。

意法半導體 (STMicroelectronics) 的 ST25Connect 專案正在進一步拓展消費者互動體驗。將 NFC 標籤嵌入醫療設備、葡萄酒和化妝品中,不僅可以提供個人化內容,還能收集使用者互動分析數據。將低成本感測器整合到嵌體中,進一步模糊了追蹤、狀態監控和客戶溝通之間的界限,從而進一步鞏固了 RFID 和 NFC 融合創新的發展路徑。

預計到2025年,零售業將維持30.48%的收入佔有率,這反映了門市RFID計畫的早期應用以及電子貨架標籤(ESL)的日益普及。然而,與醫療保健和製藥行業相關的智慧標籤市場規模預計將以19.08%的複合年成長率(CAGR)在所有行業中成長最快。受序列化有效期和溫控物流需求的驅動,醫院、藥房和契約製造製造商正在採用智慧標籤來實現端到端的可追溯性。物流業者和第三方物流(3PL)公司也正在採用混合蜂窩-BLE標籤,以實現交接文件的即時自動化。

費森尤斯卡比的Data Matrix + RFID解決方案展示了藥物核查如何在重症監護醫院環境中減少人為錯誤。臨床試驗的數位化標籤無需人工重新貼標以應對語言差異,從而提高了患者依從性並簡化了監管審核。隨著食品飲料產業為因應FDA的FSMA 204可追溯性要求做好準備,類似的趨勢也正在食品飲料產業中湧現。

智慧標籤市場報告按技術(RFID、EAS、NFC、感測標籤、ESL 等)、最終用戶(零售、醫療保健、物流、製造等)、組件(整合電路、電池、天線等)、應用(追蹤、安全、低溫運輸、價格顯示等)、外形尺寸(貼紙、吊牌等)和地區(北美、歐洲、亞太地區、北美、歐洲、亞太地區)進行細分。市場預測以美元以金額為準。

區域分析

到2025年,北美將佔全球收入的37.12%,這主要得益於美國零售業早期對RFID技術的應用以及具有法律約束力的DSCSA序列化藍圖。聯邦政府持續投資,力求2030年將國內半導體產量提高兩倍,預計將緩解近期導致晶片短缺、延緩產品普及進程的局面。隨著近岸外包的推進,加拿大和墨西哥正受益於跨境貿易的整合,而艾利丹尼森在克雷塔羅投資1億美元的工廠將滿足該地區日益成長的智慧標籤需求。

在以永續性為導向的法規的支持下,歐洲正在形成第二個區域集團。即將訂定的《塑膠包裝法規》(PPWR)將強制要求使用數位識別碼進行可回收性評估,而德國針對電動車的電池護照試點計畫將進一步推動RFID技術在汽車價值鏈中的應用。Konica Minolta預測,到2027年,歐洲RFID標籤市場規模將達到25億歐元(28億美元),反映出RFID技術在消費品、醫療保健和工業領域的廣泛應用。

亞太地區將成為成長最快的地區,到2031年複合年成長率將達到18.21%。中國向7000家食品生產商推廣2D條碼、印度的塑膠廢棄物QR碼追蹤系統以及日本的工業5.0計劃,共同推動了該地區的顯著成長。不斷擴展的5G網路和規劃中的6G網路將為環境物聯網奠定基礎,並支援大規模部署無電池感測器。台灣和韓國半導體製造業的集中優勢帶來了供應優勢,但地緣政治風險仍然是一個不確定因素。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大RFID在庫存可見性方面的應用

- 藥品供應鏈中對防偽措施的需求日益成長

- 全通路零售的興起意味著對即時定價的需求。

- 物聯網賦能物流的滲透率不斷提高

- 推出印刷式、無電池感應器標籤,以確保低溫運輸完整性

- 歐盟ESG包裝法規(PPWR 2026)加速智慧標籤整合

- 市場限制

- 小規模零售商的初始硬體和整合成本較高

- 缺乏通用的互通性標準

- 由於半導體供應受限,超高頻射頻識別積體電路的供應出現延遲。

- 資料隱私法規限制了NFC消費者互動分析

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方和消費者的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 透過技術

- RFID

- 電子商品防盜系統(EAS)

- 近距離場通訊(NFC)

- 感測標籤(溫度、氣體等)

- 電子貨架標籤(ESL)

- 其他新興市場(2D碼、藍牙低功耗)

- 按最終用戶行業分類

- 零售

- 醫療和藥品

- 物流/運輸

- 製造業和工業

- 食品/飲料

- 其他終端用戶產業

- 按組件

- 微控制器/積體電路

- 電池和電源單元

- 天線和收發器

- 感應器

- 軟體和中介軟體

- 基材和保護材料

- 透過使用

- 資產和庫存管理

- 防盜和安全

- 低溫運輸監測

- 動態定價和促銷

- 品牌認證與消費者互動

- 在製品管理

- 按標籤形狀

- 濕式嵌體/貼紙標籤

- 吊牌

- 套模標籤

- 紡織品和服裝標籤

- 可列印軟性感測器標籤

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- CCL Industries Inc.

- Zebra Technologies Corp.

- Honeywell International Inc.

- SATO Holdings Corp.

- William Frick & Company

- Invengo Information Technology Co. Ltd.

- Scanbuy Inc.

- Alien Technology LLC

- Roambee Corporation

- Smartrac(NXP)

- SES-imagotag SA

- Pricer AB

- Thinfilm Electronics ASA

- Digimarc Corporation

- Tapwow LLC

- Stora Enso Oyj

- Identiv Inc.

- Impinj Inc.

- Checkpoint Systems Inc.

- Confidex Ltd.

- NXP Semiconductors NV

第7章 市場機會與未來展望

Smart label market size in 2026 is estimated at USD 21.31 billion, growing from 2025 value of USD 18.38 billion with 2031 projections showing USD 44.74 billion, growing at 15.99% CAGR over 2026-2031.

This growth reflects the intersection of regulatory mandates, advances in radio-frequency identification (RFID) and near-field communication (NFC) technologies, and rising demand for end-to-end supply-chain transparency. Pharmaceutical serialization under the FDA's Drug Supply Chain Security Act, the European Union's Packaging and Packaging Waste Regulation (PPWR) that embeds digital-product-passport concepts, and retailer-driven RFID programs such as Walmart's have together created a non-negotiable compliance baseline. Companies are responding by integrating cloud analytics, blockchain authentication, and ambient IoT sensors that convert passive labels into data-rich assets, enabling real-time inventory visibility, dynamic pricing, and condition monitoring across industries.

Global Smart Label Market Trends and Insights

Growing RFID Adoption for Inventory Visibility

Walmart's mandate for ultra-high-frequency (UHF) RFID tags on thousands of stock-keeping units has pushed suppliers to retrofit production lines, catalyzing sector-wide investment in RAIN RFID encoding solutions. Suppliers gain perpetual stock visibility that feeds directly into manufacturing execution systems, reducing material shortages and unlocking digital-twin scheduling efficiencies. Qualcomm's plan to embed RAIN RFID in smartphones will soon turn every consumer device into a reader, eliminating the need for fixed scanner infrastructure and accelerating small-retailer adoption. Meanwhile, antenna miniaturization now supports 10-foot read ranges, enabling frictionless checkout zones that elevate customer experience.

Rising Demand for Anti-Counterfeiting in Pharma Supply Chains

Full enforcement of the DSCSA in November 2024 requires trading partners to verify serialized identifiers before product hand-off, prompting label upgrades that combine NFC chips, blockchain encryption, and e-paper displays for tamper evidence and dosage information. Ynvisible's ConnectedLabel, for instance, supports near real-time temperature tracking on over 1 million pharma packs annually. Outside the United States, India has ordered QR codes on the top-selling medicines, illustrating how serialization is moving from compliance exercise to patient-safety differentiator.

High Initial Hardware and Integration Costs for Small Retailers

ESLs cost USD 11-12 per tag, creating steep capital requirements when rolled out across thousands of SKUs. Smaller retailers must also budget for point-of-sale upgrades and staff training, delaying adoption despite labor-saving potential. Subscription models are emerging but remain nascent.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Omnichannel Retail Requiring Real-Time Pricing

- Increasing Penetration of IoT-Enabled Logistics

- Semiconductor Supply Constraints Delaying UHF RFID IC Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

RFID accounted for 37.86% of the smart label market share in 2025, underpinned by proven scalability in retail and logistics. NFC, though smaller today, is projected for 19.52% CAGR because it exploits the global ubiquity of smartphones for tap-to-verify experiences. The smart label market size tied to NFC therefore shows the steepest absolute dollar expansion, especially in luxury authentication where blockchain integration delivers tamper-evident provenance. Electronic article surveillance remains steady, whereas sensing labels gain momentum through cold-chain and environmental compliance use cases. Overall, technology migration is moving from passive identification toward multifunction sensors and engagement tools.

Greater consumer interactivity is being unlocked by STMicroelectronics' ST25Connect program, enabling NFC tags in medical devices, wine, and cosmetics to deliver personalized content while capturing engagement analytics. Integrating low-cost sensors within inlays further blurs lines between tracking, condition monitoring, and customer communication, placing RFID and NFC on convergent innovation paths.

Retail retained 30.48% revenue share in 2025, reflecting early adoption of store-wide RFID programs and growing ESL footprints. However, the smart label market size linked to healthcare and pharmaceuticals is set to grow at 19.08% CAGR, the fastest across industries. Serialization deadlines and the need for temperature-controlled logistics drive hospitals, pharmacies, and contract manufacturers to embed smart labels for end-to-end traceability. Logistics providers and 3PLs also deploy hybrid cellular-BLE labels to automate hand-off documentation in real time.

Fresenius Kabi's Data Matrix plus RFID initiative illustrates how medication verification cuts human error in high-acuity hospital environments. Digital display labels for clinical trials eliminate manual relabeling across language variants, improving patient compliance and simplifying regulatory audits. Similar dynamics extend to food and beverage players gearing up for the FDA's FSMA 204 traceability mandates.

The Smart Label Market Report is Segmented by Technology (RFID, EAS, NFC, Sensing Labels, ESL, and More), End-User (Retail, Healthcare, Logistics, Manufacturing, and More), Component (ICs, Batteries, Antennas, and More), Application (Tracking, Security, Cold-Chain, Pricing, and More), Form Factor (Stickers, Tags, and More), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts in Value (USD).

Geography Analysis

North America held 37.12% of global revenue in 2025, anchored by the United States' early adoption of RFID in retail and the legally binding DSCSA serialization roadmap. Continued federal investment aimed at tripling domestic semiconductor output by 2030 will reduce chip shortages that have recently slowed deployment schedules. Canada and Mexico benefit from integrated cross-border commerce as near-shoring picks up, while Avery Dennison's USD 100 million Queretaro facility is set to meet rising regional demand for smart labels.

Europe represents the second-largest regional block, buoyed by sustainability-centric regulation. The forthcoming PPWR mandates digital identifiers for recyclability scoring, and Germany's battery-passport pilot for electric vehicles solidifies RFID within automotive value chains. Konica Minolta forecasts the European RFID label market to reach EUR 2.5 billion (USD 2.8 billion) by 2027, reflecting widespread adoption in consumer goods, healthcare, and industrial sectors.

Asia-Pacific is the fastest-growing geography with an 18.21% CAGR through 2031. China's 2D-barcode rollout across 7,000 food producers, India's QR-code traceability for plastic waste, and Japan's industry-5.0 incentives together generate outsized momentum. Growing 5G and planned 6G coverage provides the network backbone for ambient IoT, supporting large-volume adoption of battery-free sensors. Chip manufacturing concentration in Taiwan and South Korea offers supply advantages, although geopolitical risk remains a variable.

- Avery Dennison Corporation

- CCL Industries Inc.

- Zebra Technologies Corp.

- Honeywell International Inc.

- SATO Holdings Corp.

- William Frick & Company

- Invengo Information Technology Co. Ltd.

- Scanbuy Inc.

- Alien Technology LLC

- Roambee Corporation

- Smartrac (NXP)

- SES-imagotag SA

- Pricer AB

- Thinfilm Electronics ASA

- Digimarc Corporation

- Tapwow LLC

- Stora Enso Oyj

- Identiv Inc.

- Impinj Inc.

- Checkpoint Systems Inc.

- Confidex Ltd.

- NXP Semiconductors N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing RFID adoption for inventory visibility

- 4.2.2 Rising demand for anti-counterfeiting in pharma supply chains

- 4.2.3 Expansion of omnichannel retail requiring real-time pricing

- 4.2.4 Increasing penetration of IoT-enabled logistics

- 4.2.5 Emergence of printed battery-free sensor labels for cold-chain integrity

- 4.2.6 EU ESG packaging mandates (PPWR 2026) accelerating smart-label integration

- 4.3 Market Restraints

- 4.3.1 High initial hardware and integration costs for small retailers

- 4.3.2 Lack of universal interoperability standards

- 4.3.3 Semiconductor supply constraints delaying UHF RFID IC availability

- 4.3.4 Data-privacy regulations limiting NFC consumer-engagement analytics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 RFID

- 5.1.2 Electronic Article Surveillance (EAS)

- 5.1.3 Near Field Communication (NFC)

- 5.1.4 Sensing Labels (Temp, Gas, etc.)

- 5.1.5 Electronic Shelf Label (ESL)

- 5.1.6 Other Emerging (QR, BLE)

- 5.2 By End-user Industry

- 5.2.1 Retail

- 5.2.2 Healthcare and Pharmaceuticals

- 5.2.3 Logistics and Transportation

- 5.2.4 Manufacturing and Industrial

- 5.2.5 Food and Beverage

- 5.2.6 Other End-user Industry

- 5.3 By Component

- 5.3.1 Micro-controllers / ICs

- 5.3.2 Batteries and Power Units

- 5.3.3 Antennas and Transceivers

- 5.3.4 Sensors

- 5.3.5 Software and Middleware

- 5.3.6 Substrate and Protective Materials

- 5.4 By Application

- 5.4.1 Asset and Inventory Tracking

- 5.4.2 Anti-theft and Security

- 5.4.3 Cold-chain Monitoring

- 5.4.4 Dynamic Pricing and Promotion

- 5.4.5 Brand Authentication and Consumer Engagement

- 5.4.6 Work-in-Process Management

- 5.5 By Label Form Factor

- 5.5.1 Wet-inlay / Sticker Labels

- 5.5.2 Hang Tags

- 5.5.3 In-mold Labels

- 5.5.4 Textile and Apparel Labels

- 5.5.5 Printable Flexible Sensor Labels

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc.

- 6.4.3 Zebra Technologies Corp.

- 6.4.4 Honeywell International Inc.

- 6.4.5 SATO Holdings Corp.

- 6.4.6 William Frick & Company

- 6.4.7 Invengo Information Technology Co. Ltd.

- 6.4.8 Scanbuy Inc.

- 6.4.9 Alien Technology LLC

- 6.4.10 Roambee Corporation

- 6.4.11 Smartrac (NXP)

- 6.4.12 SES-imagotag SA

- 6.4.13 Pricer AB

- 6.4.14 Thinfilm Electronics ASA

- 6.4.15 Digimarc Corporation

- 6.4.16 Tapwow LLC

- 6.4.17 Stora Enso Oyj

- 6.4.18 Identiv Inc.

- 6.4.19 Impinj Inc.

- 6.4.20 Checkpoint Systems Inc.

- 6.4.21 Confidex Ltd.

- 6.4.22 NXP Semiconductors N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

物流智慧標籤—第二版

物流智慧標籤—第二版 智慧標籤市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材質、功能、安裝類型及解決方案分類

智慧標籤市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材質、功能、安裝類型及解決方案分類 全球智慧標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球智慧標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本智慧標籤市場規模、佔有率、趨勢和預測:按技術、組件、最終用戶和地區分類,2026-2034年

日本智慧標籤市場規模、佔有率、趨勢和預測:按技術、組件、最終用戶和地區分類,2026-2034年 NFC標籤市場:按標籤類型、晶片類型、材料類型、應用和最終用戶分類,全球預測,2026-2032年智慧標籤市場規模、佔有率、成長及全球產業分析:按技術、終端用戶和地區劃分的洞察與預測(2026-2034)

NFC標籤市場:按標籤類型、晶片類型、材料類型、應用和最終用戶分類,全球預測,2026-2032年智慧標籤市場規模、佔有率、成長及全球產業分析:按技術、終端用戶和地區劃分的洞察與預測(2026-2034) 智慧標籤市場規模、佔有率及成長分析(按技術、組件、應用、最終用戶和地區分類)-2026-2033年產業預測

智慧標籤市場規模、佔有率及成長分析(按技術、組件、應用、最終用戶和地區分類)-2026-2033年產業預測 智慧標籤市場:產業趨勢及全球預測(至 2035 年)-依技術類型、包裝類型、初級包裝類型、次要包裝類型和地區劃分

智慧標籤市場:產業趨勢及全球預測(至 2035 年)-依技術類型、包裝類型、初級包裝類型、次要包裝類型和地區劃分 RFID·智慧標記的全球市場(2025年)

RFID·智慧標記的全球市場(2025年) 智慧標籤-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

智慧標籤-全球市場佔有率和排名、總收入和需求預測(2025-2031年)