|

市場調查報告書

商品編碼

1851335

胺類:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Amines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

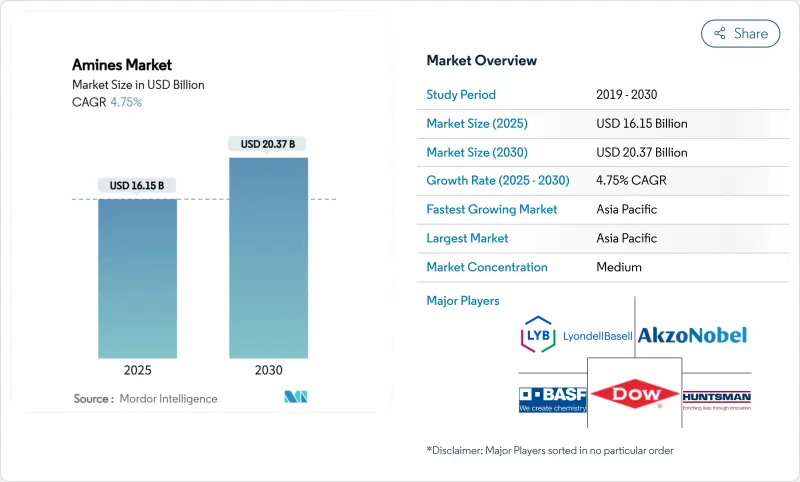

預計到 2025 年,胺類物質市場規模將達到 161.5 億美元,到 2030 年將達到 203.7 億美元,預測期(2025-2030 年)複合年成長率為 4.75%。

強勁的工業需求、有利於清潔化學品的日益嚴格的環境法規以及不斷成長的高價值應用(例如碳捕獲溶劑)項目,共同支撐了胺類市場的持續擴張。半導體製造領域的投資增加、大規模農業的現代化以及生物基個人護理界面活性劑的廣泛應用,都為胺類市場帶來了更大的規模和價值成長機會。生產商正透過提高能源效率和整合可再生原料來應對氨和乙烯價格的波動,同時遵守主要經濟體新興的揮發性有機化合物法規。領先的供應商也在加大對超高純度電子級胺產能的投入,以滿足下一代晶片對金屬的嚴格要求,這凸顯了胺類生產正從大宗商品生產向利潤空間更大的特種解決方案的顯著轉變。

全球胺類市場趨勢與洞察

亞洲個人護理產品配方師的需求激增

自2010年以來,胺基酸界面活性劑的市佔率已超越傳統硫酸鹽界面活性劑,年均成長率高達18%。亞洲配方師憑藉麩胺酸和丙氨酸界面活性劑的溫和性和生物分解性佔據主導地位,這促使胺類界面活性劑生產商通過國際永續性和碳認證(ISCC-PLUS)拓展其生物基產品線。諾力昂(Nouryon)獲得認證的綠色環氧乙烷和乙醇胺生產線,展現了工廠營運商如何調整產品組合,轉向潔淨標示配方。同時,多功能胺氧化物在洗髮精、沐浴露和家居用品領域也日益普及,因為生產商追求的是高發泡且溫和的特性。隨著中產階級消費者越來越傾向於選擇天然成分含量接近100%的產品,胺類界面活性劑市場有望進一步鞏固其作為亞洲蓬勃發展的清潔美容生態系統關鍵推動者的地位。

新興農業中心快速採用殺蟲劑

亞太和南美洲的現代農業實踐需要精準的化學投入,從而推動了對胺類農業化學鹽和乳化劑的需求。採用可再生電力動力來源的新型分散式氨廠正在降低物流成本,並提高區域供應安全,尤其是在巴西和印度。 CF Industries 和 POET 的低碳氨肥初步試驗展示了整合綠色氫能途徑所帶來的農藝和永續性優勢。這些進展有助於提高用於除草劑、殺蟲劑和種子處理劑的乙醇胺、烷基胺和脂族胺的長期市場需求。

轉向非木質紙張和數位文件的轉變

已開發國家辦公用紙消費量的下降正在削弱對胺基紙漿漂白劑和紙張被覆劑的需求。為了緩解這種長期拖累,各公司正將銷售量轉移到成長更快的個人護理和建築領域。BASF決定將其傳統的胺類資產重新定位到特種化學品領域,凸顯了該行業積極應對這一結構性變化的舉措。

細分市場分析

由於乙醇胺在氣體脫硫劑、個人護理界面活性劑和腐蝕抑制劑等領域發揮至關重要的作用,預計到2024年,乙醇胺將佔胺類市場總量的42.55%。天然氣加工和三乙醇胺基水泥添加劑的穩定需求支撐著該市場強勁的基準,即便在碳捕獲溶劑等領域出現了新的應用。此細分市場規模龐大,使得主要供應商能夠充分利用成本優勢和業務協同效應,涵蓋從乙氧基化物到嗎福林的整個衍生性商品鏈。相較之下,受電子、製藥和先進複合材料等細分應用領域的推動,特種胺預計將在2030年之前以5.01%的複合年成長率實現最快成長。

生產商正在安裝多功能反應器,以便在高純度嗎福林、二胺和手性胺中間體之間快速切換。贏創在南京的擴建計畫正是這種向高附加價值分子轉型的一個例證。同時,諸如釕/三磷酸催化劑等學術突破可望擴大特種胺的永續原料來源,該催化劑利用可再生原料即可實現90%的產率。乙醇胺規模化生產與特種胺市場成長之間的相互作用,為胺類市場長期的平衡發展軌跡提供了支撐。

區域分析

亞太地區繼續保持其雙重領先地位,2024年佔全球銷售額的38.91%,並預計到2030年將以5.88%的複合年成長率持續成長。中國4552萬噸的氨產能鞏固了該地區的原料優勢。印度的特種化學品領軍企業,包括Alkyl Amines和Balaji Amines,擁有20多家工廠,產品出口到100多個國家,充分發揮了其成本優勢。台灣、韓國和中國當地半導體產業的擴張推動了對電子級胺的需求,而東南亞國協在醫藥、農業化學品和日用產品領域也實現了進一步成長。BASF計劃投資100億美元建設湛江一體化計劃,該項目將完全使用可再生能源電力,這表明跨國公司正積極尋求把握該地區持續的成長潛力。

北美是一個成熟且具有重要戰略意義的叢集,對整合碳捕獲系統的藍氨設施的投資不斷增加。預計到2030年,美國的氨產能將成長四倍。這項擴張將保障國內化肥供應,並為乙醇胺和尿素衍生物提供本地原料。同時,加拿大豐富的水力資源使其成為低碳胺生產領域的有力競爭者,其產品面向國內和出口市場。

歐洲持續推動循環經濟目標,推動生物基中間體和節能反應器的創新。諾力昂綠色環氧乙烷獲得ISCC-PLUS認證,滿足了歐洲對生態標籤界面活性劑的區域需求。歐盟委員會日益嚴格的VOC排放目標促使配方師以符合性能標準的高閃點衍生物取代傳統的揮發性胺。中東和非洲受益於天然氣原料的供應,尤其是在沙烏地阿拉伯和阿曼,這使得氨及其下游胺類產品的價格更具競爭力。在南美洲,大豆和玉米種植蓬勃發展,確保了巴西和阿根廷對除草劑胺鹽的穩定需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲對個人護理配方師的需求激增

- 新興農業中心農藥的快速擴散

- 基礎建設熱潮刺激建築化學品需求

- 用於尖端半導體工廠的電子級胺

- 現場綠色氫衍生先導計畫

- 市場限制

- 轉向非木質紙張和數位文件的轉變

- 揮發性氨和乙烯原料定價

- 更嚴格的胺類揮發性有機化合物/氣味法規

- 價值鏈分析

- 監管環境

- 技術展望

- 目前技術

- 沸石催化甲胺工藝

- 異丁烯的直接胺化

- 催化蒸餾

- EDC氨解

- 未來科技

- 目前技術

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 定價分析

- 生產分析

第5章 市場規模與成長預測

- 按類型

- 乙胺

- 烷基胺

- 脂肪胺

- 特種胺

- 乙醇胺

- 按最終用途行業分類

- 橡皮

- 個人保健產品

- 清潔產品

- 黏合劑、油漆、樹脂

- 農業化學品

- 石油/石化

- 其他最終用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Air Products and Chemicals, Inc.

- Akzo Nobel NV

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings BV

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

第7章 市場機會與未來展望

The Amines Market size is estimated at USD 16.15 billion in 2025, and is expected to reach USD 20.37 billion by 2030, at a CAGR of 4.75% during the forecast period (2025-2030).

This sustained expansion is supported by resilient industrial demand, stricter environmental regulations that favor cleaner chemistries and a growing pipeline of high-value applications such as carbon-capture solvents. Rising investments in semiconductor fabrication, large-scale agricultural modernization and widespread adoption of bio-based personal-care surfactants are expanding both volume and value opportunities in the amines market. Producers are improving energy efficiency and integrating renewable feedstocks to manage volatile ammonia and ethylene prices while complying with emerging volatile organic compound limits across major economies. Leading suppliers are also channeling capital toward ultra-pure electronics-grade capacities to meet the stringent metal specifications required by next-generation chips, highlighting a visible shift from commodity production toward specialized solutions that offer superior margin potential.

Global Amines Market Trends and Insights

Surging Demand from Asian Personal-Care Formulators

Amino acid-based surfactants have outpaced traditional sulfate systems, recording 18% average annual growth since 2010. Asian formulators are mainstreaming glutamate and alaninate derivatives that offer low irritation and high biodegradability, forcing amine suppliers to expand bio-based lines with International Sustainability and Carbon Certification (ISCC-PLUS) credentials. Nouryon's certified production of green ethylene oxide and ethanolamines illustrates how plant operators are realigning portfolios toward clean-label formulations. In tandem, multifunctional amine oxides are gaining ground in shampoo, body-wash and household categories as manufacturers pursue high-foaming yet mild profiles. With middle-class consumers gravitating toward products boasting a natural-origin index approaching 100%, the amines market is set to deepen its role as a pivotal enabler of Asia's fast-growing clean-beauty ecosystem.

Rapid Pesticide Adoption in Emerging Agriculture Hubs

Modern farming practices in Asia Pacific and South America require precision chemical inputs, lifting demand for amine-based pesticide salts and emulsifiers. Novel decentralized ammonia plants powered by renewable electricity are lowering logistics costs and improving regional supply security, notably in Brazil and India. CF Industries and POET's pilot of low-carbon ammonia fertilizer demonstrates the agronomic and sustainability pay-off of integrating green hydrogen pathways. Such developments bolster long-term offtake for ethanolamines, alkylamines and fatty amines used in herbicides, insecticides and seed-treatment agents.

Shift to Wood-Free Paper & Digital Documentation

Declining office-paper consumption in developed economies is dampening demand for amine-based pulp bleaching agents and paper coatings. Companies are reallocating volumes toward faster-growing personal-care and construction segments to cushion the long-term drag. BASF's decision to reconfigure legacy amine assets toward specialty chemicals highlights the industry's proactive adjustment to this structural shift.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Boom Spurring Construction Chemicals

- Electronics-Grade Amines for Advanced Semiconductor Fabs

- Volatile Ammonia & Ethylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethanolamines captured 42.55% of the overall amines market in 2024, owing to their indispensable role in gas sweetening, personal-care surfactants and corrosion inhibitors. Steady demand from natural-gas treatment and triethanolamine-based cement additives underpins a robust baseline, even as newer uses in carbon-capture solvents emerge. The segment's scale gives leading suppliers cost leverage and operational synergies across derivative chains ranging from ethoxylates to morpholine. In contrast, specialty amines are projected to post the fastest 5.01% CAGR through 2030, propelled by niche applications in electronics, pharmaceuticals and advanced composites.

Producers are installing multipurpose reactors capable of quick changeovers between high-purity morpholines, diamines and chiral amine intermediates. Evonik's expansion in Nanjing exemplifies this pivot toward higher value-added molecules. Concurrently, academic breakthroughs such as ruthenium/triphos catalysts achieving 90% yields on renewable feedstocks promise to widen the sustainable feedstock pool for specialty grades. The interplay of scale in ethanolamines and growth in specialty amines underpins the balanced long-term trajectory of the amines market.

The Amines Market Report is Segmented by Type (Ethyleneamines, Alkylamines, Fatty Amines, Specialty Amines, Ethanolamines), End-Use Industry (Rubber, Personal Care Products, Cleaning Products, Adhesives/Paints/Resins, Agro-Chemicals, Oil/Petrochemicals, Other End-Uses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained its dual leadership position, generating 38.91% of global revenue in 2024 and expanding at a 5.88% CAGR through 2030. China's 45.52 million t ammonia capacity anchors the region's raw-material advantage. India's specialty chemicals champions, including Alkyl Amines and Balaji Amines, operate more than 20 plants and export to over 100 countries, leveraging cost-competitive manufacturing. Semiconductor expansions across Taiwan, South Korea and mainland China are pushing demand for electronics-grade amines, while ASEAN nations add incremental growth through pharmaceuticals, agro chemicals and household products. BASF's planned USD 10 billion Zhanjiang Verbund project, powered entirely by renewable electricity, illustrates how multinationals intend to capture enduring regional upside.

North America represents a mature yet strategically vital cluster, with rising investments in blue ammonia facilities integrated with carbon-capture systems. The United States is expected to quadruple ammonia capacity by 2030. This expansion safeguards domestic fertilizer supply and provides a local feedstock base for ethanolamine and urea derivatives. Meanwhile, Canada's abundant hydropower positions it as a contender for low-carbon amine production targeting both domestic and export markets.

Europe continues to pursue circular-economy objectives, driving innovations in bio-based intermediates and energy-efficient reactors. Nouryon's ISCC-PLUS certification for green ethylene oxide supports regional demand for eco-labeled surfactants. The European Commission's stricter VOC targets are encouraging formulators to substitute conventional volatile amines with higher-flashpoint derivatives that meet performance criteria. The Middle East and Africa benefit from natural-gas feedstock availability, enabling competitively priced ammonia and downstream amine chains, especially in Saudi Arabia and Oman. South America's focus on soybean and corn cultivation assures steady consumption of herbicidal amine salts, with Brazil and Argentina leading uptake.

- Air Products and Chemicals, Inc.

- Akzo Nobel N.V.

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings B.V.

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from Asian personal-care formulators

- 4.2.2 Rapid pesticide adoption in emerging agriculture hubs

- 4.2.3 Infrastructure boom spurring construction chemicals

- 4.2.4 Electronics-grade amines for advanced semiconductor fabs

- 4.2.5 On-site green-hydrogen-derived amines pilots

- 4.3 Market Restraints

- 4.3.1 Shift to wood-free paper and digital documentation

- 4.3.2 Volatile ammonia and ethylene feedstock pricing

- 4.3.3 Stricter amine VOC/odor regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Current Technologies

- 4.6.1.1 Zeolite-catalyzed methylamine processes

- 4.6.1.2 Direct amination of isobutylene

- 4.6.1.3 Catalytic distillation

- 4.6.1.4 Ammonolysis of EDC

- 4.6.2 Upcoming Technologies

- 4.6.1 Current Technologies

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Price Analysis

- 4.9 Production Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Ethyleneamines

- 5.1.2 Alkylamines

- 5.1.3 Fatty Amines

- 5.1.4 Specialty Amines

- 5.1.5 Ethanolamines

- 5.2 By End-use Industry

- 5.2.1 Rubber

- 5.2.2 Personal Care Products

- 5.2.3 Cleaning Products

- 5.2.4 Adhesives, Paints and Resins

- 5.2.5 Agro-Chemicals

- 5.2.6 Oil and Petrochemicals

- 5.2.7 Other End-uses

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Air Products and Chemicals, Inc.

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Alkyl Amines Chemicals Limited

- 6.4.4 Arkema

- 6.4.5 BASF SE

- 6.4.6 Celanese Corporation

- 6.4.7 Clariant

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 Eastman Chemical Company

- 6.4.11 Huntsman International LLC

- 6.4.12 INEOS

- 6.4.13 Invista

- 6.4.14 Kemipex

- 6.4.15 LyondellBasell Industries Holdings B.V.

- 6.4.16 MITSUBISHI GAS CHEMICAL COMPANY, INC

- 6.4.17 NIPPON SHOKUBAI CO., LTD.

- 6.4.18 SABIC

- 6.4.19 Solvay

- 6.4.20 Tosoh Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

二異丙基乙胺市場:依形態、等級、應用及通路-2026-2032年全球預測

二異丙基乙胺市場:依形態、等級、應用及通路-2026-2032年全球預測 烷基胺市場規模、佔有率和成長分析:按形態、烷基胺類型、最終用途、通路、地區和產業預測,2026-2033年

烷基胺市場規模、佔有率和成長分析:按形態、烷基胺類型、最終用途、通路、地區和產業預測,2026-2033年 2026年全球兒茶酚胺市場報告

2026年全球兒茶酚胺市場報告 對苯二異氰酸酯市場分析及預測(至2035年):按類型、產品、應用、技術、組件、最終用戶、製程、材料類型、安裝類型和解決方案分類

對苯二異氰酸酯市場分析及預測(至2035年):按類型、產品、應用、技術、組件、最終用戶、製程、材料類型、安裝類型和解決方案分類 全球胺類市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球胺類市場規模、佔有率、趨勢及成長分析報告(2026-2034年) Piperazine市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、應用、區域和競爭對手分類,2021-2031年胺類市場 - 全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、地區及競爭格局分類,2021-2031年)

Piperazine市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、應用、區域和競爭對手分類,2021-2031年胺類市場 - 全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、地區及競爭格局分類,2021-2031年) 2026-2030年全球異丙胺市場水溶性咪唑啉市場按類型、劑型、應用和最終用戶分類,全球預測(2026-2032)

2026-2030年全球異丙胺市場水溶性咪唑啉市場按類型、劑型、應用和最終用戶分類,全球預測(2026-2032) 對苯二胺市場規模、佔有率和成長分析(按應用、純度等級、最終用途產業、銷售管道和地區分類)-2026-2033年產業預測

對苯二胺市場規模、佔有率和成長分析(按應用、純度等級、最終用途產業、銷售管道和地區分類)-2026-2033年產業預測