|

市場調查報告書

商品編碼

1851328

安全開關:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Safety Switches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

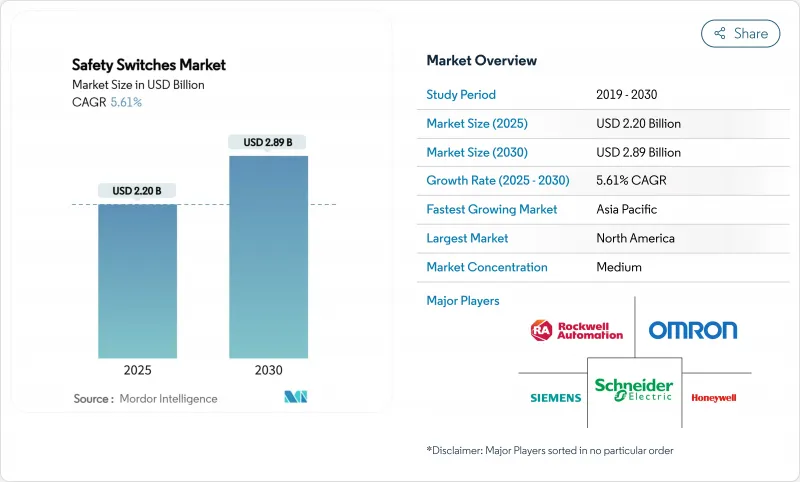

全球安全開關市場預計到 2025 年將達到 22 億美元,到 2030 年將達到 28.9 億美元,複合年成長率為 5.61%。

成長的驅動力來自工廠自動化領域的積極投資、日益嚴格的機器安全法規以及向協作機器人工作空間的快速轉型。終端用戶現在需要具備防篡改、自我診斷和現場匯流排連接功能的設備,而供應商則正在整合RFID編碼、物聯網感測器和預測性維護分析技術。亞太地區佔據最大市場佔有率,受惠於大規模智慧工廠專案;而中東地區則有望憑藉油氣產業的現代化和防爆要求實現最快成長。競爭焦點正轉向以解決方案為導向的產品組合,這些組合整合了硬體、軟體和服務,以實現快速合規並降低整體擁有成本。能夠彌合功能安全和即時資料可見性之間差距的設備製造商有望在下一波安全開關市場浪潮中佔據主導地位。

全球安全開關市場趨勢與洞察

亞洲日益成長的自動化主導安全需求

隨著自動化普及速度加快,亞洲製造業的安全概念正在發生根本性轉變,對先進安全開關的需求也隨之顯著成長。中國、日本和韓國等國家正在實施更嚴格的職場安全法規,強制要求在自動化生產線上使用經認證的安全裝置。這些法規的演變與該地區轉型為智慧製造的步伐不謀而合,使得安全開關成為確保人機共存的關鍵組件。在人事費用不斷上漲和熟練工人持續短缺的背景下,將安全開關整合到工廠自動化系統中已成為製造商尋求平衡生產效率和工人安全的重要戰略考量。根據IDEC預測,從2024年起,亞洲對安全開關的需求預計將成長超過30%,其中非接觸式開關在電子製造業的普及率最高。

協作機器人的興起對整合安全解決方案提出了更高的要求。

協作機器人(cobot)在製造環境中的廣泛應用,從根本上改變了安全系統的要求,並為先進的安全開關技術提供了巨大的發展機會。與在封閉迴路境中運作的傳統工業機器人不同,協作機器人與人類協同工作,因此需要複雜的安全機制,能夠根據接近程度和運作模式動態調整保護參數。 2024 年修訂的 ISO 10218 工業機器人安全標準明確了協作機器人的功能安全要求,從而推動了對能夠與機器人控制系統對接的安全開關的需求。儘管協作機器人本身俱有一定的安全特性,但仍需要補充防護解決方案來應對諸如夾點和程式錯誤等殘餘風險。據 PowerSafe Automation 稱,正確整合安全開關可以將協作機器人相關事故減少高達 85%,同時保持運作效率,使其成為實現工業 4.0 的關鍵組件。

面向注重成本的中小型企業的非接觸式開關,平均售價較高。

RFID感測器的成本是電子機械感測器的兩到三倍,這使得預算和技術能力有限的小型維修車間難以快速更換。因此,先進設備在中小型機械製造商的普及率仍低於25%,限制了安全開關市場整體的短期應用。

細分市場分析

安全開關市場仍以電子機械開關為主導,這類開關已在多塵、振動的環境中證明了其耐用性。然而,非接觸式RFID感測器發展勢頭最為強勁,年複合成長率高達7.8%。 2024年,電子機械設備將佔46%的收入佔有率,而隨著監管機構加強防篡改措施,RFID在製藥生產線上的應用也大幅成長。預計到2030年,非接觸式設備的市場規模將達到10.4億美元,反映出它們在機器人組裝單元中的應用日益廣泛。

RFID感測器還支援預測性維護分析。內建記憶體記錄循環次數,從而實現故障前預警。防爆外殼和不銹鋼結構拓展了其在腐蝕性和危險環境中的應用,擴大了供應商的潛在收入來源。持續的微型化技術使得在緊湊型協作機器人夾爪中整合多感測器陣列成為可能,從而增強了安全開關市場的未來需求。

由於機械結構簡單、單價低廉,鑰匙式連鎖裝置應用廣泛。然而,RFID編碼和磁性致動器正逐漸興起,尤其是在4類PLe應用中,它們能有效防止防護裝置被竄改。這些設計可透過單一電纜連鎖多達32個節點,從而縮短安裝時間。製藥無塵室和食品加工生產線更傾向於使用非接觸式聯鎖裝置,以消除污染物可能滯留的縫隙,這推動了安全開關市場的新成長。

基於乙太網路的功能安全技術也正在興起。供應商將致動器和安全繼電器的功能整合在同一機殼內,並將診斷資料傳輸到製造執行系統 (MES) 控制面板。這實現了傳統硬佈線鏈路的虛擬化,並支援靈活的單元重配置,這是工業 4.0 的核心要求。因此,致動器創新對於在安全開關市場中獲取價值仍然至關重要。

工業安全開關市場按類型(電磁式、非接觸式)、致動器類型(鑰匙操作聯鎖、其他)、安裝類型(面板安裝、DIN導軌安裝)、最終用戶(工業、商業、醫療保健、石油天然氣)和地區(北美、歐洲、亞太)進行細分。市場規模和預測以百萬美元為單位。

區域分析

亞太地區,尤其是在中國和韓國電子產業叢集的帶動下,預計到2024年將佔全球銷售額的38.2%。各國「智慧製造」計畫下的工廠升級,特別是採用RFID連鎖和IO-Link診斷技術,正推高平均售價。印度和越南政府對自動化生產線的補貼,預計將有助於它們保持其在安全開關市場的區域領先地位。

預計到2030年,中東地區的複合年成長率將達到9.1%。阿拉伯聯合大公國和沙烏地阿拉伯的國家石油公司目前要求天然氣壓縮、煉油和液化天然氣出口裝置使用ATEX或IECEx認證的開關設備。能夠提供溫度等級為+度C至+55 度C且採用不銹鋼外殼的供應商已獲得多年期框架契約,從而推動了市場的快速擴張。

歐洲和北美市場雖然仍處於發展階段,但蘊藏著巨大的機會。歐盟機械指令的修訂迫使化學和食品加工企業在兩年內對老舊的攪拌機和輸送機進行改造。在美國,隨著電子商務履約系統(WMS)的網路化交換機,安全開關市場持續穩定成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲日益成長的自動化主導安全需求

- 協作機器人的興起以及整合安全解決方案的需求

- 歐洲流程工業中老舊機械的強制性改裝

- 中東石油和天然氣產業對防爆設備的需求激增

- 在具有高潛力的製藥設施中採用RFID編碼連鎖裝置(美國/歐盟)

- 電子商務倉儲熱潮推動輸送機安全開關的使用(北美)

- 市場限制

- 面向注重成本的中小型企業的非接觸式開關,平均售價較高。

- 跨多個區域的複雜身分驗證流程

- 與特定產業安全現場匯流排的兼容性差距

- 假低價進口商品阻礙品牌滲透(亞太地區)

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 電子機械安全開關

- 非接觸式(RFID/磁性)安全開關

- 防爆/重型安全開關

- 其他類型

- 按下致動器類型

- 鑰匙操作聯鎖裝置

- 鉸鏈互鎖

- RFID編碼互鎖

- 磁性致動器

- 按安裝類型

- 面板安裝

- DIN導軌安裝

- 最終用戶

- 工業生產

- 車

- 飲食

- 化學品和製藥

- 航太/國防

- 金屬和採礦

- 能源與電力

- 石油和天然氣

- 發電業務

- 商業和機構

- 建築自動化

- 物流/倉儲

- 衛生保健

- 其他

- 工業生產

- 按銷售管道

- 直接 OEM

- 分銷商/系統整合商

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他拉丁美洲地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 中東和非洲

- 土耳其

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric

- Rockwell Automation

- Banner Engineering

- Eaton Corporation

- Euchner GmbH

- SICK AG

- Pilz GmbH and Co. KG

- Siemens AG

- Omron Corporation

- Honeywell International

- Phoenix Contact

- ABB Ltd.

- IDEC Corporation

- BERNSTEIN AG

- Pepperl+Fuchs

- Keyence Corporation

- Leuze electronic

- Schmersal Group

- TURCK

- Crouzet

第7章 市場機會與未來展望

The global Safety switches market size stands at USD 2.2 billion in 2025 and is forecast to reach USD 2.89 billion by 2030, registering a 5.61% CAGR.

Growth is underpinned by aggressive factory-automation investments, stricter machine-safety laws and a rapid shift toward collaborative robot workspaces. End users now demand devices that combine tamper resistance, self-diagnostics and fieldbus connectivity, pushing suppliers to embed RFID coding, IoT sensors and predictive-maintenance analytics. Asia-Pacific holds the largest regional position, benefitting from large-scale smart-factory programs, while the Middle East is set for the quickest rise on the back of oil-and-gas modernization and explosion-proof mandates. Competitive focus has moved toward solution-oriented portfolios that integrate hardware, software and services, enabling quicker compliance and reduced total cost of ownership. Device makers able to bridge functional safety and real-time data visibility are expected to capture the next wave of opportunities in the Safety switches market.

Global Safety Switches Market Trends and Insights

Expanding automation-driven safety requirements in Asia

Asia's manufacturing sector is experiencing a fundamental shift in safety paradigms as automation adoption accelerates, creating substantial demand for sophisticated safety switches. Countries like China, Japan, and South Korea are implementing stricter workplace safety regulations that mandate the use of certified safety devices in automated production lines. This regulatory evolution coincides with the region's push toward smart manufacturing, where safety switches serve as critical components in ensuring human-machine coexistence. The integration of safety switches with factory automation systems has become a strategic priority for manufacturers seeking to balance productivity with worker protection, particularly as labor costs rise and skilled worker shortages persist. According to IDEC, demand for safety switches in Asia has grown by over 30% since 2024, with non-contact varieties seeing the highest adoption rates in electronics manufacturing

Rise in collaborative robots necessitating integrated safety solutions

The proliferation of collaborative robots (cobots) across manufacturing environments is fundamentally transforming safety system requirements, creating significant opportunities for advanced safety switch technologies. Unlike traditional industrial robots that operate in caged environments, cobots work alongside humans, necessitating sophisticated safety mechanisms that can dynamically adjust protection parameters based on proximity and operation mode. The revision of ISO 10218 standard for industrial robot safety in 2024 has established clearer functional safety requirements for collaborative applications, driving demand for safety switches that can interface with robot control systems. Despite their inherent safety features, cobots still require complementary guarding solutions to address residual risks such as pinch points and programming errors. PowerSafe Automation reports that properly integrated safety switches can reduce cobot-related incidents by up to 85% while maintaining operational efficiency, making them essential components in Industry 4.0 implementations

Higher ASPs of Non-Contact Switches in Cost-Sensitive SMEs

RFID sensors cost two to three times more than electromechanical models, discouraging rapid swap-outs in small workshops where budget and technical skills are limited. Consequently, penetration of advanced units among SME machine builders remains below 25%, tempering near-term uptake across the Safety switches market .

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Retrofit of Legacy Machinery in Europe's Process Industries

- Demand Surge for Explosion-Proof Devices in Middle-East Oil & Gas

- Complex Certification Cycles Across Multi-Jurisdictional Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electromechanical models still lead the Safety switches market thanks to proven durability in dusty, high-vibration sites. Yet non-contact RFID sensors show the swiftest momentum, expanding at 7.8% CAGR as OEMs look to curb bypassing and gain live diagnostic data. In 2024, electromechanicals held a 46% revenue share, while RFID uptake in pharma lines rose sharply after regulators tightened tampering rules. The Safety switches market size for non-contact devices is projected to reach USD 1.04 billion by 2030, mirroring wider adoption in robotic assembly cells.

RFID sensors also unlock predictive-maintenance analytics; embedded memory logs cycle counts, enabling service alerts before failure. Explosion-proof housings and stainless-steel variants are broadening use in corrosive and hazardous settings, expanding supplier addressable revenue pools. Continuous miniaturization further allows multi-sensor arrays inside compact cobot grippers, reinforcing future demand within the Safety switches market.

Key-operated interlocks retain widespread use due to mechanical simplicity and low unit cost. Still, RFID-coded and magnetic actuators now set the pace, especially in Category 4, PLe applications that prohibit guard cheating. These designs cascade up to 32 nodes over a single cable, shrinking installation time. Pharmaceutical cleanrooms and food-processing lines favor non-contact formats to eliminate crevices where contaminants might lodge, spurring fresh volume in the Safety switches market.

Functional safety over Ethernet is also emerging. Vendors bundle actuator and safety-relay functions in the same housing, streaming diagnostics to MES dashboards. This virtualizes traditional hard-wired chains and supports flexible cell reconfiguration, a core Industry 4.0 requirement. Consequently, actuator innovation will remain pivotal to value capture within the Safety switches market.

Industrial Safety Switch Market is Segmented Type (Electromagnetic, Non-Contact), Actuator Type ( Key-Operated Interlock and More). Installation Configuration( Panel-Mounted, DIN-Rail Mounted ), End-User (Industrial, Commercial, Healthcare, Oil & Gas), and Geography (North America, Europe, and Asia-Pacific). The Market Sizes and Forecasts are Provided in Terms of Value (USD Million)

Geography Analysis

Asia-Pacific generated 38.2% of 2024 revenue, led by Chinese and South Korean electronics clusters. Factory upgrades under national "smart manufacturing" plans specify RFID interlocks and IO-Link diagnostics, lifting average selling prices. Government subsidies for automated lines in India and Vietnam will sustain regional leadership of the Safety switches market.

The Middle East is forecast to grow at 9.1% CAGR through 2030. National oil companies in UAE and Saudi Arabia now demand ATEX or IECEx-certified switchgear for gas compression, refining and LNG export trains. Suppliers offering -55 °C to +55 °C temperature ratings and stainless-steel enclosures have secured multiyear framework deals, catalyzing swift market expansion.

Europe and North America remain mature but opportunity rich. EU Machinery Directive revisions compel chemical and food processors to retrofit older mixers and conveyors within two years; this short-cycle demand inflates replacement volumes. In the US, e-commerce fulfillment centers adopt network-ready switches that feed safety data to cloud WMS platforms, preserving steady unit growth in the Safety switches market.

- Schneider Electric

- Rockwell Automation

- Banner Engineering

- Eaton Corporation

- Euchner GmbH

- SICK AG

- Pilz GmbH and Co. KG

- Siemens AG

- Omron Corporation

- Honeywell International

- Phoenix Contact

- ABB Ltd.

- IDEC Corporation

- BERNSTEIN AG

- Pepperl+Fuchs

- Keyence Corporation

- Leuze electronic

- Schmersal Group

- TURCK

- Crouzet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Automation-Driven Safety Requirements in Asia

- 4.2.2 Rise in Collaborative Robots Necessitating Integrated Safety Solutions

- 4.2.3 Mandatory Retrofit of Legacy Machinery in Europe's Process Industries

- 4.2.4 Demand Surge for Explosion-Proof Devices in Middle-East Oil and Gas

- 4.2.5 Adoption of RFID-Coded Interlocks in High-Potency Pharma Facilities (US/EU)

- 4.2.6 E-Commerce Warehousing Boom Boosting Conveyor Safety Switch Usage (NA)

- 4.3 Market Restraints

- 4.3.1 Higher ASPs of Non-Contact Switches in Cost-Sensitive SMEs

- 4.3.2 Complex Certification Cycles Across Multi-Jurisdictional Plants

- 4.3.3 Compatibility Gaps with Industry-Specific Safety Fieldbuses

- 4.3.4 Counterfeit Low-Cost Imports Undermining Brand Adoption (APAC)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Electromechanical Safety Switches

- 5.1.2 Non-Contact (RFID / Magnetic) Safety Switches

- 5.1.3 Explosion-Proof / Heavy-Duty Safety Switches

- 5.1.4 Other Types

- 5.2 By Actuator Type

- 5.2.1 Key-Operated Interlock

- 5.2.2 Hinge-Operated Interlock

- 5.2.3 RFID-Coded Interlock

- 5.2.4 Magnetic Actuator

- 5.3 By Installation Configuration

- 5.3.1 Panel-Mounted

- 5.3.2 DIN-Rail Mounted

- 5.4 By End-User

- 5.4.1 Industrial Manufacturing

- 5.4.1.1 Automotive

- 5.4.1.2 Food and Beverage

- 5.4.1.3 Chemicals and Pharmaceuticals

- 5.4.1.4 Aerospace and Defense

- 5.4.1.5 Metals and Mining

- 5.4.2 Energy and Power

- 5.4.2.1 Oil and Gas

- 5.4.2.2 Power Generation

- 5.4.3 Commercial and Institutional

- 5.4.3.1 Building Automation

- 5.4.3.2 Logistics and Warehousing

- 5.4.4 Healthcare

- 5.4.5 Others

- 5.4.1 Industrial Manufacturing

- 5.5 By Sales Channel

- 5.5.1 Direct OEM

- 5.5.2 Distributor / System Integrator

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of Latin America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Middle East and Africa

- 5.6.4.1 Turkey

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Saudi Arabia

- 5.6.4.4 South Africa

- 5.6.4.5 Rest of Middle East and Africa

- 5.6.5 Asia-Pacific

- 5.6.5.1 China

- 5.6.5.2 Japan

- 5.6.5.3 South Korea

- 5.6.5.4 India

- 5.6.5.5 Australia

- 5.6.5.6 Rest of Asia Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric

- 6.4.2 Rockwell Automation

- 6.4.3 Banner Engineering

- 6.4.4 Eaton Corporation

- 6.4.5 Euchner GmbH

- 6.4.6 SICK AG

- 6.4.7 Pilz GmbH and Co. KG

- 6.4.8 Siemens AG

- 6.4.9 Omron Corporation

- 6.4.10 Honeywell International

- 6.4.11 Phoenix Contact

- 6.4.12 ABB Ltd.

- 6.4.13 IDEC Corporation

- 6.4.14 BERNSTEIN AG

- 6.4.15 Pepperl+Fuchs

- 6.4.16 Keyence Corporation

- 6.4.17 Leuze electronic

- 6.4.18 Schmersal Group

- 6.4.19 TURCK

- 6.4.20 Crouzet

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

安全開關市場規模、佔有率、成長分析(按產品類型、按電壓範圍、按安全系統、按開關類型、按最終用戶、按地區)- 2025 年至 2032 年行業預測

安全開關市場規模、佔有率、成長分析(按產品類型、按電壓範圍、按安全系統、按開關類型、按最終用戶、按地區)- 2025 年至 2032 年行業預測 全球緊急停止開關市場

全球緊急停止開關市場 全球緊急停止開關市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年)

全球緊急停止開關市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年) 安全開關市場規模、佔有率、趨勢及預測(按產品類型、安全系統、開關類型、最終用戶和地區分類),2025 年至 2033 年

安全開關市場規模、佔有率、趨勢及預測(按產品類型、安全系統、開關類型、最終用戶和地區分類),2025 年至 2033 年 亞太地區安全開關:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲安全開關:市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區安全開關:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲安全開關:市場佔有率分析、產業趨勢、成長預測(2025-2030) 安全開關市場:按類型、安全系統、應用、最終用戶分類 - 全球預測 2025-2030

安全開關市場:按類型、安全系統、應用、最終用戶分類 - 全球預測 2025-2030 鎖定安全開關市場報告:2030 年趨勢、預測與競爭分析全球安全開關市場規模:依產品類型、安全系統、產業、地區、範圍及預測安全限位開關市場,按類型、按驅動類型、按垂直行業(製造、石油和天然氣、化學和製藥、採礦、能源和公用事業、食品和飲料)、按應用和預測,2024 - 2032 年

鎖定安全開關市場報告:2030 年趨勢、預測與競爭分析全球安全開關市場規模:依產品類型、安全系統、產業、地區、範圍及預測安全限位開關市場,按類型、按驅動類型、按垂直行業(製造、石油和天然氣、化學和製藥、採礦、能源和公用事業、食品和飲料)、按應用和預測,2024 - 2032 年