|

市場調查報告書

商品編碼

1851272

能源領域統一通訊即服務 (UCaaS) - 市場佔有率分析、產業趨勢、統計數據和成長預測 (2025-2030)UCaaS In Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

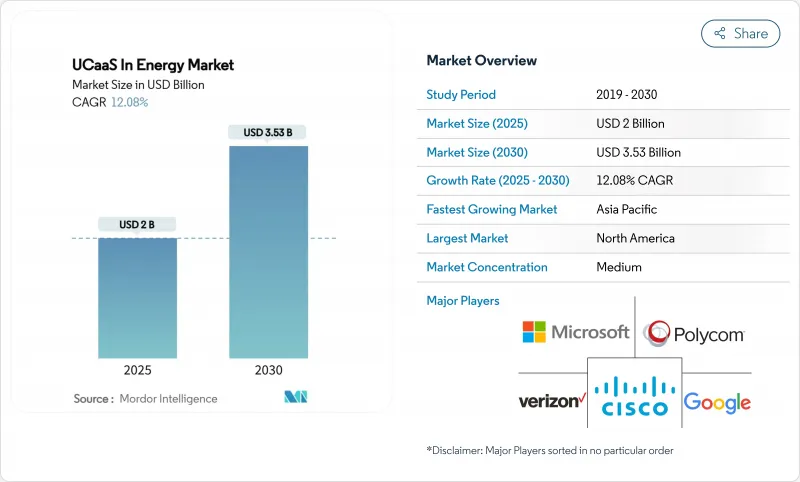

預計到 2025 年,能源 UCaaS 市場規模將達到 20 億美元,到 2030 年將達到 35.3 億美元,2025 年至 2030 年的複合年成長率為 12.08%。

快速的數位化、日益成長的現場人員協作需求以及操作技術和資訊技術的融合正在加速統一通訊技術的應用。公共產業正在對其電網進行現代化改造,油氣營運商正在對油井進行數位化改造,可再生能源資產所有者正在採用雲端原生工具——所有這些都需要能夠在嚴苛的分散式環境中可靠運作的統一通訊。邊緣架構、專用5G連接和基於消費的定價模式正在降低整體擁有成本,而網路安全彈性要求則促使企業採用安全、整合的語音和影像平台。市場競爭較為溫和,主要通訊集團、雲端供應商和專注於能源領域的專家都在尋求透過混合部署和特定領域的功能來獲取市場佔有率。儘管整合複雜性和資料主權規則正在減緩一些計劃的進度,但監管機構對現代化、人工智慧賦能通訊的支援仍在不斷為各個領域和地區帶來新的機會。

全球能源統一通訊即服務 (UCaaS) 市場趨勢與洞察

雲端原生能源IT生態系統的普及

像沙烏地阿美這樣的領先營運商正在部署工業分散式雲,將運算和儲存資源更靠近資產,從而實現需要同樣敏捷通訊的即時分析。透過開放API整合的雲端原生UCaaS平台簡化了資源配置,使能源公司能夠在邊緣工作負載的同時推出新的語音、視訊和通訊服務。從本地PBX遷移到可擴展的雲端中心系統,有助於滿足監管補丁管理要求,同時降低生命週期成本。隨著越來越多的營運應用程式採用容器化技術,基於微服務建構的整合通訊能夠實現控制室和現場團隊之間的無縫資料流,從而顯著提高生產力和安全性。

基於邊緣運算的遠端資產協作

雪佛龍和殼牌部署了邊緣閘道器來監控井口感應器,並在出現異常情況時立即觸發語音或視訊通話,從而減少停機時間和差旅成本。擴增實境頭戴裝置使技術人員能夠在接收專家指導的同時,將示意圖疊加到裝置上,並透過統一通訊即服務 (UCaaS) 視訊串流進行指導。邊緣端的低延遲處理確保關鍵警報通過冗餘通道路由,即使在海上和沙漠地區也能保證安全合規性。因此,支援邊緣運算的工作流程提高了協作質量,而不會使回程傳輸鏈路過載,從而增強了在現場部署整合通訊的商業價值。

傳統資產OT-IT整合的複雜性

煉油廠依賴使用了數十年的SCADA和DCS平台,這些平台運行專有通訊協定,並且出於安全考慮與企業網路隔離。採用雲端基礎的UCaaS需要安全閘道、通訊協定轉換器和嚴格的變更控制,所有這些都會延長部署週期。工廠工程師優先考慮運作而非新功能,這種抵觸情緒也迫使採用分階段部署的方式,將本地語音功能與最新的雲端功能結合。高昂的諮詢和網路安全成本阻礙了近期採用,尤其是對於中型資產所有者而言。

細分市場分析

2024年,語音通訊仍將佔據能源統一通訊即服務(UCaaS)市場37.5%的最大佔有率,這主要得益於電廠和管線以語音為中心的安全通訊協定。然而,隨著公用事業公司採用人工智慧聊天機器人和全通路介面來處理停電報告和帳單查詢,客服中心即服務(CCaaS)預計到2030年將以17.86%的複合年成長率成長。這種轉變將提高客戶滿意度,同時降低呼叫處理成本。

除了前台辦公優勢外,CCaaS 還與停電管理系統和智慧電錶資料整合,使代理商能夠在電網事件發生時主動提醒客戶。同時,協作套件、統一通訊和會議工具透過整合桌面、行動裝置和現場設備,增強了內部團隊的協作能力。受 API 整合等「其他服務」的推動,能源 UCaaS 市場規模預計將隨著營運商將通訊融入物聯網和維護工作流程而穩定成長。

至2024年,公共雲端實例將佔能源統一通訊即服務(UCaaS)市場規模的60.4%。然而,企業對本地資料儲存的需求,例如SCADA對話和事件日誌,將推動混合模式模式達到21.2%的複合年成長率。混合模式將低風險流量路由到超大規模區域,同時將敏感資料流錨定到本地或邊緣節點。

這種架構兼具敏捷性和合規性,因此在遵守嚴格資料隱私法律的歐洲公用事業公司中廣受歡迎。雖然在核能發電廠和海上鑽機等必須完全隔離的場所,私有部署仍然至關重要,但不斷上漲的維護成本促使非關鍵工作負載逐步遷移到雲端,凸顯了混合架構的長期吸引力。

能源產業整合通訊(即服務)市場報告按組件(語音通訊、協作工具、統一通訊、會議等)、部署模式(私人、公共、混合)、公司規模(大型企業、中小企業)、能源子行業(石油和天然氣、發電等)和地區對產業進行細分。

區域分析

北美地區2024年44.3%的收入佔有率反映了其龐大的數位化油田、智慧電網試點計畫和成熟的雲端基礎設施的裝置量。聯邦政府對電網修復的獎勵策略以及頁岩盆地的私有5G試點計畫將支撐持續的需求。僅由公共產業推動的能源統一通訊即服務(UCaaS)市場規模就將成長,因為投資者擁有的公司正在升級客服中心以處理電氣化諮詢。

到2030年,亞太地區將以19.8%的複合年成長率成長,這主要得益於中國加速推進基於人工智慧的電力產業改革,以及印度開闢可再生能源走廊,而這些走廊需要雲端整合通訊。區域各國政府傾向在國內進行資料託管,從而推動了混合模式和本地邊緣節點的發展。日本天然氣發行和澳洲液化天然氣出口商也積極整合統一通訊即服務(UCaaS),以監控遠端資產並滿足員工安全要求。

在「Fit for 55」法規的推動下,歐洲保持著穩步發展勢頭。該法規要求電網具備網路安全性和互通性。跨境能源交易和離岸風力發電叢集需要輸電系統營運商(TSO)和服務船之間進行即時協調。東歐電網正在投資雲端原生調度工具,以減少對俄羅斯天然氣的依賴。同時,中東和非洲正在為大型企劃部署專用LTE和5G網路,但農村生產基地的網路連接不足阻礙了這些技術的全面應用。監管政策的清晰度和可靠的寬頻仍然是決定各地區普及速度的關鍵因素。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 雲端原生能源IT生態系統的普及

- 基於邊緣運算的遠端資產協作

- 油田和工廠的5G專用網路

- 供應商轉向以消費量定價

- 將 UCaaS 和 O-RAN 整合到現場通訊中

- 監管機構強制要求建立網路安全語音/視訊系統

- 市場限制

- 傳統資產的OT-IT整合複雜性

- 持續存在的數據主權障礙

- 能源價格波動會延緩IT資本投資。

- 偏遠地區最後一公里連結的局限性

- 關鍵法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 按組件

- 語音通訊

- 協作工具

- 統一通訊

- 會議

- 客服中心即服務

- 其他服務

- 按部署模式

- 公共

- 私人的

- 混合

- 按公司規模

- 主要企業

- 小型企業

- 按能源子部門

- 石油和天然氣

- 發電

- 公共產業(輸配電)

- 可再生能源資產

- 採礦和開採

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Verizon Communications Inc.

- Microsoft Corporation

- Cisco Systems, Inc.

- RingCentral, Inc.

- Google LLC

- 8x8, Inc.

- Zoom Video Communications, Inc.

- Avaya LLC

- BT Group plc

- Vodafone Group Plc

- AT&T Inc.

- Vonage Holdings Corp.

- Genesys Telecommunications Laboratories, Inc.

- Twilio Inc.

- Mitel Networks Corporation

- NEC Corporation

- ALE International SAS

- West Technology Group, LLC

- Plantronics, Inc.

- Fuze, Inc.

- Tata Communications Limited

- Orange SA

- GoTo Group, Inc.

第7章 市場機會與未來展望

The UCaaS in energy market size stood at USD 2 billion in 2025 and is forecast to reach USD 3.53 billion by 2030, translating into a 12.08% CAGR over 2025-2030.

Rapid digitalization, rising field-worker collaboration needs and the fusion of operational technology with information technology are accelerating adoption. Utilities are modernizing grids, oil and gas operators are digitizing wells, and renewable asset owners are deploying cloud-native tools, all of which demand unified communications that operate reliably across harsh, distributed environments. Edge architectures, private-5G connectivity and consumption-based pricing lower total cost of ownership, while cyber-resilience mandates push firms to standardize on secure, unified voice and video platforms. Competitive intensity is moderate; large telecom groups, cloud vendors and energy-focused specialists seek share through hybrid deployments and domain-specific features. Although integration complexity and data-sovereignty rules slow some projects, regulatory support for modern, AI-enabled communications continues to unlock opportunities across segments and regions.

Global UCaaS In Energy Market Trends and Insights

Proliferation of Cloud-Native Energy IT Ecosystems

Major operators such as Aramco are rolling out industrial distributed clouds that bring compute and storage closer to assets, enabling real-time analytics that demand equally agile communications . Cloud-native UCaaS platforms integrate via open APIs, streamline provisioning and allow energy firms to spin up new voice, video and messaging services alongside edge workloads. Shifting from on-premises PBXs to scalable, cloud-centric systems also helps reduce lifecycle costs while satisfying regulatory patch-management requirements. As more operational applications become container-based, unified communications embedded within those micro-services enable seamless data flow between control rooms and field teams, driving a tangible uplift in productivity and safety.

Edge-Enabled Remote Asset Collaboration

Chevron and Shell deploy edge gateways that monitor wellhead sensors and instantly trigger voice or video calls when anomalies surface, lowering downtime and travel costs. Augmented-reality headsets let technicians overlay schematics while receiving expert guidance through UCaaS video streams that stay local when connectivity falters. Low-latency processing at the edge ensures critical alerts route through redundant channels, preserving safety compliance even in offshore or desert sites. Edge-enabled workflows therefore upgrade collaboration quality without overloading backhaul links, strengthening the business case for unified communications embedded at site level.

OT-IT Integration Complexity in Legacy Assets

Refineries still depend on decades-old SCADA and DCS platforms that run proprietary protocols and isolate themselves from corporate networks for safety reasons. Introducing cloud-based UCaaS requires secure gateways, protocol converters and rigorous change-management, all of which extend roll-out timelines. Resistance also stems from plant engineers who prioritize uptime over new features, forcing phased deployments that blend on-premises voice with modern cloud functions. High consulting and cybersecurity costs therefore curb short-term uptake, particularly among mid-sized asset owners.

Other drivers and restraints analyzed in the detailed report include:

- 5G Private Networks in Oilfields and Plants

- Vendor Shift to Consumption-Based Pricing

- Persistent Data-Sovereignty Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephony retained the biggest slice of the UCaaS in energy market share at 37.5% in 2024, supported by voice-centric safety protocols across plants and pipelines . Yet Contact-Center-as-a-Service (CCaaS) is projected to post a 17.86% CAGR through 2030 as utilities deploy AI chatbots and omnichannel interfaces to handle outage reports and billing queries. This pivot improves satisfaction scores while trimming call-handling costs.

Beyond front-office gains, CCaaS also integrates with outage-management systems and smart-meter data, letting agents proactively alert customers during grid events. Collaboration suites, unified messaging and conferencing tools meanwhile serve internal teams by unifying desktop, mobile and field devices. Across the forecast, the UCaaS in energy market size attributable to "other services" such as API integrations will expand steadily as operators embed communications within IoT and maintenance workflows.

Public cloud instances commanded 60.4% of the UCaaS in energy market size in 2024 due to rapid spin-up times and minimal hardware needs. However enterprises seeking local data residency for SCADA conversations or incident recordings are driving hybrid models toward a 21.2% CAGR. Hybrid designs route low-risk traffic via hyperscale regions while anchoring sensitive streams in on-premises or edge nodes.

This architecture balances agility with compliance and has become popular among European utilities navigating strict privacy statutes. Private deployments remain vital for nuclear plants and offshore rigs where full isolation is mandatory, yet rising maintenance costs encourage gradual migration of non-critical workloads to cloud touchpoints, underscoring hybrid's long-term appeal.

The Unified Communication As-A-Service in Energy Market Report Segments the Industry Into by Component (Telephony, Collaboration Tools, Unified Messaging, Conferencing, and More), Deployment Model (Private, Public, and Hybrid), Enterprise Size (Large Enterprise, and Small and Medium Enterprise), Energy Subsector (Oil and Gas, Power Generation, and More), and Geography.

Geography Analysis

North America's 44.3% 2024 revenue share reflects a large installed base of digital oilfields, smart-grid pilots and mature cloud infrastructure. Federal stimulus for grid resilience coupled with private-5G pilots in shale basins underpin continued demand. The UCaaS in energy market size attributable to utilities alone is set to climb as investor-owned firms upgrade contact centers to manage electrification queries.

Asia-Pacific will expand at a 19.8% CAGR through 2030 as China accelerates AI-based power-sector reforms and India opens renewable corridors that require cloud-integrated communications . Regional governments endorse domestic data hosting, spurring hybrid models and local edge nodes. Japanese gas distributors and Australian LNG exporters likewise integrate UCaaS to oversee remote assets and meet workforce-safety mandates.

Europe maintains steady momentum driven by Fit-for-55 regulations demanding cyber-secure, interoperable grids. Cross-border energy exchanges and offshore wind clusters necessitate real-time coordination among TSOs and service vessels. Eastern European grids, seeking to reduce Russian gas dependency, invest in cloud-native dispatch tools. Meanwhile, Middle East and Africa embrace private-LTE and 5G for mega-projects, yet connectivity gaps in rural production sites restrain full-scale adoption. Across all regions, regulatory clarity and reliable broadband remain key determinants of rollout pace.

- Verizon Communications Inc.

- Microsoft Corporation

- Cisco Systems, Inc.

- RingCentral, Inc.

- Google LLC

- 8x8, Inc.

- Zoom Video Communications, Inc.

- Avaya LLC

- BT Group plc

- Vodafone Group Plc

- AT&T Inc.

- Vonage Holdings Corp.

- Genesys Telecommunications Laboratories, Inc.

- Twilio Inc.

- Mitel Networks Corporation

- NEC Corporation

- ALE International SAS

- West Technology Group, LLC

- Plantronics, Inc.

- Fuze, Inc.

- Tata Communications Limited

- Orange SA

- GoTo Group, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of cloud-native energy IT ecosystems

- 4.2.2 Edge-enabled remote asset collaboration

- 4.2.3 5G private networks in oilfields and plants

- 4.2.4 Vendor shift to consumption-based pricing

- 4.2.5 O-RAN integration with UCaaS for field comms

- 4.2.6 Cyber-resilient voice/video mandates by regulators

- 4.3 Market Restraints

- 4.3.1 OT-IT integration complexity in legacy assets

- 4.3.2 Persistent data-sovereignty hurdles

- 4.3.3 Volatile energy prices delaying IT cap-ex

- 4.3.4 Limited last-mile connectivity in remote sites

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Telephony

- 5.1.2 Collaboration Tools

- 5.1.3 Unified Messaging

- 5.1.4 Conferencing

- 5.1.5 Contact-Center-as-a-Service

- 5.1.6 Other Services

- 5.2 By Deployment Model

- 5.2.1 Public

- 5.2.2 Private

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Energy Sub-Sector

- 5.4.1 Oil and Gas

- 5.4.2 Power Generation

- 5.4.3 Utilities (TandD)

- 5.4.4 Renewable Energy Assets

- 5.4.5 Mining and Extraction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Verizon Communications Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 RingCentral, Inc.

- 6.4.5 Google LLC

- 6.4.6 8x8, Inc.

- 6.4.7 Zoom Video Communications, Inc.

- 6.4.8 Avaya LLC

- 6.4.9 BT Group plc

- 6.4.10 Vodafone Group Plc

- 6.4.11 AT&T Inc.

- 6.4.12 Vonage Holdings Corp.

- 6.4.13 Genesys Telecommunications Laboratories, Inc.

- 6.4.14 Twilio Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 NEC Corporation

- 6.4.17 ALE International SAS

- 6.4.18 West Technology Group, LLC

- 6.4.19 Plantronics, Inc.

- 6.4.20 Fuze, Inc.

- 6.4.21 Tata Communications Limited

- 6.4.22 Orange SA

- 6.4.23 GoTo Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

整合通訊即服務 (UCaaS) 市場規模、佔有率和趨勢分析報告:按部署類型、產業、地區和細分市場預測 (2026–2033)

整合通訊即服務 (UCaaS) 市場規模、佔有率和趨勢分析報告:按部署類型、產業、地區和細分市場預測 (2026–2033) 整合通訊即服務 (UCaaS) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

整合通訊即服務 (UCaaS) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 2026年全球整合通訊即服務(UCaaS)市場報告整合通訊即服務 (UCaaS) 市場:策略洞察與預測 (2026–2031)

2026年全球整合通訊即服務(UCaaS)市場報告整合通訊即服務 (UCaaS) 市場:策略洞察與預測 (2026–2031) 整合通訊即服務 (UCaaS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球綜合通訊即服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)

整合通訊即服務 (UCaaS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球綜合通訊即服務市場規模、佔有率、趨勢和成長分析報告(2026-2034) 統一通訊即服務 (UCaaS) 市場 - 全球產業規模、佔有率、趨勢、機會及預測(按服務、部署、部署模式、交付模式、最終用戶、地區和競爭格局分類),2021-2031 年全球統一通訊即服務 (UCaaS) 市場:成長機會(2024-2031 年)

統一通訊即服務 (UCaaS) 市場 - 全球產業規模、佔有率、趨勢、機會及預測(按服務、部署、部署模式、交付模式、最終用戶、地區和競爭格局分類),2021-2031 年全球統一通訊即服務 (UCaaS) 市場:成長機會(2024-2031 年) 2025-2029 年整合通訊即服務 (UCAAS) 市場2026 年至 2032 年統一通訊即服務 (UCaaS) 市場(按部署類型、組織規模、最終用戶產業和地區分類)

2025-2029 年整合通訊即服務 (UCAAS) 市場2026 年至 2032 年統一通訊即服務 (UCaaS) 市場(按部署類型、組織規模、最終用戶產業和地區分類)