|

市場調查報告書

商品編碼

1851194

空中下載 (OTA) 測試:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Over-The-Air (OTA) Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

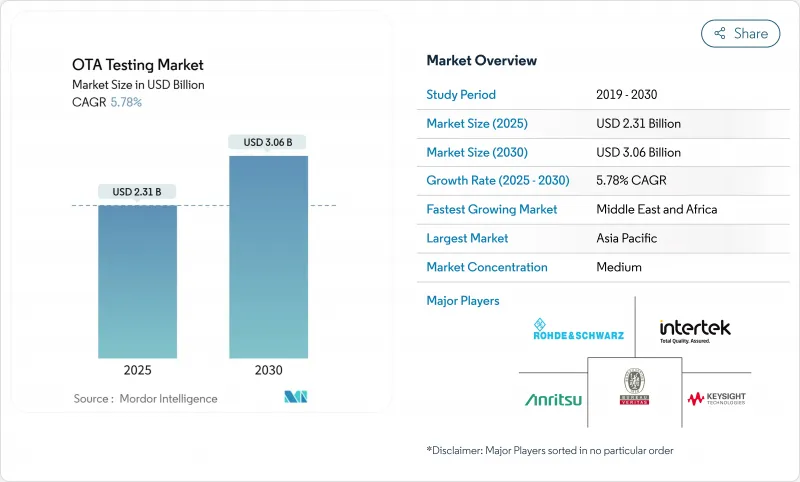

預計到 2025 年,OTA 測試市場規模將達到 23.1 億美元,到 2030 年將達到 30.6 億美元,在此期間的複合年成長率為 5.78%。

這一成長反映了5G獨立組網的日益普及、汽車中蜂窩V2X整合度的不斷提高,以及對成本敏感型物聯網模組認證需求的不斷成長。家用電子電器對毫米波合規性的需求不斷成長、工廠中私有5G部署的增加,以及CTIA和全球認證論壇等機構日益嚴格的全球認證體系,也推動了這一成長。儘管硬體仍然是資本支出的主要重點,但隨著企業尋求減少在消音室方面的前期投資,服務外包正在加速發展。從區域來看,亞太地區受益於全球最密集的5G部署,而中東和非洲則憑藉其積極的數位經濟發展策略,實現了最快的成長速度。

全球空中(OTA)檢測市場趨勢與洞察

5G非獨立組網和獨立組網部署的激增需要新的適配通訊協定

將覆蓋範圍從 24 GHz 擴展到 29 GHz,要求行動電話和平板電腦製造商確保複雜天線陣列的總輻射功率和各向同性靈敏度。和碩為 Wi-Fi 6E 和 5G檢驗投入的 1.64 億美元凸顯了設備供應鏈的資本支出壓力。毫米波波長顯著縮短了遠距離測試距離,使得近場測量至關重要。像安立 MA8172A 這樣的緊湊型天線測試場 (CATR) 平台可以在不到五天的時間內重新部署,從而減少生產停機時間。因此,提供基於可攜式CATR 的審核服務供應商的預約量激增。

北美汽車OEM廠商轉向軟體定義與V2X連接平台

由全球認證論壇 (GCF) 與 5G 汽車協會 (5G Automotive Association) 合作開發的 C-V2X 認證,正式確立了一種結合 5.9 GHz 側鏈路和網路上行鏈路的雙通訊模式。是德科技 (Keysight) 和羅德與施瓦茨 (Rohde & Schwarz) 正與一級供應商合作,模擬動態交通場景,以同時檢驗緊急煞車燈警告和空中軟體更新 (OTA)。從硬體鎖定的 ECU 到雲端升級平台的轉變,擴展了測試範圍,涵蓋了網路安全和功能安全方面。隨著這些車輛進入量產階段,OTA 測試市場將因工廠測試和道路測試而實現業務收益成長。

耗資巨大的消音室和混響室阻礙了二級實驗室的採用。

消音室需要阻燃金字塔形吸波材料、精密起重機和多軸定位器,在添加任何其他設備之前,其建造成本可能高達數百萬美元。對於拉丁美洲和東南亞的小型實驗室而言,這樣的預算尤其具有挑戰性。即使資金到位,鐵氧體瓦片和碳填充泡棉的供應瓶頸也意味著前置作業時間超過20週。因此,這些地區的公司只能將工作外包給數量有限的全球性設施,從而延長了計劃週期,並限制了其在OTA測試市場的滲透率。供應商正在推出模組化、可租賃的消音室來應對這一需求,但相對於推出資金而言,價格分佈仍然很高。

細分市場分析

2024年,硬體收入佔總收入的60.9%,這主要得益於實驗室對遠場暗室、CATR反射器以及5G和Wi-Fi 7所需寬頻訊號產生器的投資。許多實驗室擴大了測試能力,以適應更大尺寸的測試設備,例如汽車保險桿和智慧工廠機器人。然而,服務業務的成長最為迅猛,年複合成長率高達8.3%,因為企業更傾向於與認證服務商簽訂契約,而不是自行建設整個基礎設施。這些管理合約通常包含校準、標準諮詢和報告等服務,並以多年期框架進行包裝。雖然軟體和分析技術仍處於起步階段,但人工智慧驅動的自動化可以將測試週期縮短多達40%,進一步提高生產效率。

到2024年,LTE/LTE-A仍將佔總支出的38.5%,通訊業者將繼續驗證現有設備;而5G NR 9.1%的複合年成長率則凸顯了產業的轉型。毫米波認證要求進行動態波束控制檢驗,推動了偵測陣列和通道模擬器的升級。同時,Wi-Fi 6E和Wi-Fi 7引入了三頻段吞吐量閾值,促使對蜂窩網路和WLAN共存進行聯合測試。諸如NB-IoT之類的低功耗廣域網(LPWAN)格式擴大整合非地面電波網路,迫使設備製造商在合規性測試期間進行衛星延遲模擬。

區域分析

亞太地區在2024年仍佔全球5G收入的34.6%,這主要得益於中國80%的5G SA網路覆蓋率、日本的衛星物聯網試點計畫以及印度旨在到2040年實現5G經濟效益達5000億美元的製造業獎勵。該地區的OTA測試市場受益於委託製造和國內測試實驗室之間的垂直整合,從而縮短了智慧型手機和穿戴式裝置的供應鏈。印度和印尼政府支持的頻譜競標進一步擴大了認證設備的覆蓋範圍。

儘管只有2%的行動通訊基地台以獨立組網模式運行,歐洲在工業專用5G領域仍佔據領先地位。德國、英國和西班牙的監管機構正在為26GHz工業網路提供簡化的臨時授權流程,鼓勵機械設備製造商在本地實驗室進行原型開發。 6G測量的合作研究計畫正在完善文件標準,並促使測試機構升級其不確定性預算和可追溯性鏈。因此,OTA測試市場對諮詢顧問的需求強勁,硬體銷售也同樣強勁。

中東和非洲地區成長最快,複合年成長率達6.8%。中東通訊業者正加速推動5G建設,並為2030年前的6G奠定基礎。群眾外包性能工具正在指南頻譜政策,推動需要實驗室驗證的透明基準測試。南非和奈及利亞正在擴大與區域認證標誌掛鉤的設備補貼,並提升區域認證中心的容量。北美正在利用聯邦資金建造開放式無線接入網(RAN)和車聯網(V2X)走廊,而南美則在穩步推進從4G到5G的升級,尤其是在巴西的農業地區。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G非獨立組網和獨立組網部署的激增需要新的一致性通訊協定

- 消費性設備對毫米波和大規模MIMO天線OTA合規性的需求激增

- 北美汽車OEM廠商轉向軟體定義與V2X連接平台

- 歐洲智慧工廠的工業專用5G部署需要強大的射頻驗證

- CTIA 和 GCF 要求對物料清單價格低於 10 美元的物聯網模組實施快速認證流程。

- 市場限制

- 資本密集的消音室和混響室阻礙了二級實驗室的採用。

- 缺乏毫米波近場到遠場轉換演算法的技術技能

- 缺乏全球統一的低功耗廣域網路OTA標準將延緩市場融合。

- 射頻吸收體供應鏈的波動會推高測試基礎設施成本。

- 生態系分析

- 監理與技術展望

- 標準化藍圖(3GPP Rel-17/18,CTIA OTA 5.x)

- 新的調查方法(用於可重構智慧表面的OTA、6G太赫茲)

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 報價

- 硬體

- 房間(消音室、殘響室、緊湊型測距室)

- 測量設備(訊號產生器、頻譜分析儀、控制器)

- 軟體與分析

- 服務

- 測試和認證服務

- 諮詢與整合

- 硬體

- 透過技術

- 5G NR(6GHz 以下和毫米波)

- LTE/LTE-A/LTE-M

- UMTS/WCDMA

- GSM/CDMA

- Wi-Fi 6/7 和 Wi-Fi HaLow

- 藍牙和超寬頻

- LPWAN(NB-IoT、LoRaWAN、Sigfox)

- 按測試類型

- 天線效能(TRP、TIS、EIRP、EIS)

- 符合性與認證

- 相容性/互通性

- 生產/生產線末端

- 透過使用

- 電信、消費性電子

- 汽車和運輸設備

- 工業和製造業物聯網

- 航太/國防

- 醫療設備和穿戴式設備

- 智慧家庭/建築自動化

- 透過測試環境

- 遠距離消音室

- 緊湊型天線測試範圍

- 近場系統

- 殘響室

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 其他南美洲

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Keysight Technologies Inc.

- Rohde and Schwarz GmbH and Co. KG

- Anritsu Corporation

- SGS SA

- Intertek Group plc

- Bureau Veritas SA

- UL Solutions Inc.

- Eurofins Scientific SE

- Microwave Vision Group(MVG)

- CETECOM GmbH

- BluFlux LLC

- Element Materials Technology

- National Technical Systems Inc.(NTS)

- TUV Rheinland AG

- TUV SUD AG

- Spirent Communications plc

- VIAVI Solutions Inc.

- ETS-Lindgren Inc.

- Chotest Technology Inc.

- Shenzhen Sunwave Communications Co., Ltd.

第7章 市場機會與未來展望

The OTA testing market stood at USD 2.31 billion in 2025 and is forecast to reach USD 3.06 billion by 2030, translating into a 5.78% CAGR over the period.

This expansion reflects wider adoption of 5G standalone networks, increasing integration of cellular V2X in vehicles, and escalating certification needs for cost-sensitive IoT modules. Heightened demand for mmWave compliance in consumer electronics, rising private-5G deployments inside factories, and stricter global conformance schemes from bodies such as CTIA and the Global Certification Forum also underpin growth. Hardware continues to anchor capital spending, but service outsourcing is accelerating as enterprises look to curb up-front investments in anechoic chambers. Regionally, Asia Pacific benefits from the world's densest 5G roll-outs, while the Middle East and Africa register the fastest trajectory thanks to aggressive digital-economy agendas.

Global Over-The-Air (OTA) Testing Market Trends and Insights

Proliferation of 5G Non-Standalone and Stand-Alone Deployments Requiring New Conformance Protocols

Expansion of 24-29 GHz coverage obliges phone and tablet makers to assure total radiated power and isotropic sensitivity across intricate antenna arrays. Pegatron invested USD 164 million in new lines for Wi-Fi 6E and 5G validation, underlining cap-ex pressures in device supply chains. Near-field measurement has become essential, because mmWave wavelengths shorten far-field test distances dramatically. Compact Antenna Test Range (CATR) platforms such as Anritsu MA8172A can be redeployed in under five days, reducing production downtime. Consequently, service providers offering portable CATR-based audits are experiencing higher booking rates.

Automotive OEM Shift to Software-Defined and V2X Connectivity Platforms in North America

C-V2X certification, developed by the Global Certification Forum with the 5G Automotive Association, formalizes dual communication modes that combine 5.9 GHz sidelink and network uplinks. Keysight and Rohde & Schwarz have partnered with tier-one suppliers to emulate dynamic traffic scenarios, validating emergency brake-light alerts and over-the-air software updates concurrently. The change from hardware-locked ECUs to cloud-upgradable platforms widens test matrices to include cybersecurity and functional-safety vectors. As these vehicles move toward production, the OTA testing market records deeper service revenues from in-plant and roadside evaluations.

Capital-Intensive Anechoic and Reverberation Chambers Discouraging Adoption by Tier-2 Labs

Anechoic facilities require fire-retardant pyramidal absorbers, precision cranes and multi-axis positioners that can cost several million dollars before instrumentation is added. Such budgets deter smaller labs, particularly in Latin America and Southeast Asia. Even when financing is secured, supply bottlenecks for ferrite tiles and carbon-loaded foam extend lead times beyond 20 weeks. Consequently, enterprises in those regions outsource to a limited pool of global facilities, lengthening project cycles and curbing the OTA testing market's service penetration. Vendors are responding with modular, lease-ready chambers, yet price points remain high relative to start-up cash flows.

Other drivers and restraints analyzed in the detailed report include:

- Surging OTA Compliance Demand for mmWave and Massive-MIMO Antennas in Consumer Devices

- Industrial Private-5G Roll-outs in Europe for Smart Factories Requiring Robust RF Validation

- Technical Skill Scarcity for mmWave Near-Field-to-Far-Field Transform Algorithms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 60.9 % of revenue in 2024 as laboratories invested in far-field chambers, CATR reflectors and wide-bandwidth signal generators required for 5G and Wi-Fi 7. Many facilities expanded capacity to accommodate larger device-under-test form factors such as automotive bumpers and smart-factory robots. Services nonetheless record the steepest curve at an 8.3 % CAGR, because enterprises prefer contracting accredited providers rather than owning full infrastructures. Those managed contracts frequently include calibration, standards consulting and report generation packaged under multi-year frameworks. Software and analytics, still nascent, benefit from AI-driven automation that cuts test cycles by as much as 40 %, unlocking further productivity.

LTE/LTE-A maintained 38.5 % of 2024 spending as operators kept validating legacy devices; however, 5G NR's 9.1 % CAGR underscores an industry pivot. mmWave certification demands dynamic beam-steering checks, driving upgrades in probe arrays and channel emulators. Meanwhile, Wi-Fi 6E and Wi-Fi 7 introduce tri-band throughput thresholds, prompting joint testing of cellular and WLAN coexistence. LPWAN formats such as NB-IoT increasingly incorporate non-terrestrial networks, compelling device makers to run satellite delay emulation during compliance sessions.

The Over-The-Air (OTA) Testing Market Report is Segmented by Offering (Hardware, Software and Analytics, and Services), Technology (Bluetooth and UWB, and More), Test Type (Antenna Performance (TRP, TIS, EIRP, EIS), and More), Application (Telecom and Consumer Electronics, Aerospace and Defense, and More), Test Environment (Far-Field Anechoic Chambers, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained 34.6 % of global revenue in 2024 on the back of China's 80 % 5G SA coverage, Japan's satellite-IoT pilots and India's manufacturing incentives targeting USD 500 billion in economic impact from 5G by 2040. The OTA testing market in the region benefits from vertical integration between contract manufacturers and domestic test labs, shortening supply chains for smartphones and wearables. Government-backed spectrum auctions in India and Indonesia have further enlarged addressable volumes for certified devices.

Europe remains a powerhouse for industrial private-5G, even though only 2 % of cell sites operate in standalone mode. German, UK and Spanish regulators offer streamlined temporary licenses for 26 GHz industrial grids, encouraging machinery OEMs to prototype inside local labs. Joint research programs on 6G metrology sharpen documentation standards, forcing test houses to upgrade uncertainty budgets and traceability chains. Consequently, the OTA testing market records robust consultancy demand alongside hardware sales.

The Middle East and Africa is the quickest climber at a 6.8 % CAGR as operators in the Gulf expedite 5G and lay foundations for 6G before 2030. Crowdsourced performance tools increasingly guide spectrum policy, driving transparent benchmarks that require laboratory correlation. South Africa and Nigeria expand device subsidies tied to local conformance marks, enlarging throughput for regional certification centers. North America leverages federal funds for open-RAN and V2X corridors, whereas South America continues steady upgrades from 4G to 5G, particularly in Brazil's agritech zones.

- Keysight Technologies Inc.

- Rohde and Schwarz GmbH and Co. KG

- Anritsu Corporation

- SGS SA

- Intertek Group plc

- Bureau Veritas SA

- UL Solutions Inc.

- Eurofins Scientific SE

- Microwave Vision Group (MVG)

- CETECOM GmbH

- BluFlux LLC

- Element Materials Technology

- National Technical Systems Inc. (NTS)

- TUV Rheinland AG

- TUV SUD AG

- Spirent Communications plc

- VIAVI Solutions Inc.

- ETS-Lindgren Inc.

- Chotest Technology Inc.

- Shenzhen Sunwave Communications Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Non-Standalone and Stand-Alone Deployments Requiring New Conformance Protocols

- 4.2.2 Surging OTA Compliance Demand for mmWave and Massive-MIMO Antennas in Consumer Devices

- 4.2.3 Automotive OEM Shift to Software-Defined and V2X Connectivity Platforms in North America

- 4.2.4 Industrial Private-5G Roll-outs in Europe for Smart Factories Requiring Robust RF Validation

- 4.2.5 Rapid Certification Cycles Mandated by CTIA and GCF for IoT Modules Below USD-10 BOM

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Anechoic and Reverberation Chambers Discouraging Adoption by Tier-2 Labs

- 4.3.2 Technical Skill Scarcity for mmWave Near-Field-to-Far-Field Transform Algorithms

- 4.3.3 Lack of Harmonised Global Standards for LPWAN OTAs Delaying Market Convergence

- 4.3.4 Supply-Chain Volatility of RF Absorber Materials Inflating Test Infrastructure Costs

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.5.1 Standardisation Roadmap (3GPP Rel-17/18, CTIA OTA 5.x)

- 4.5.2 Emerging Test Methodologies (OTA for Reconfigurable Intelligent Surfaces, 6G Terahertz)

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 Chambers (Anechoic, Reverberation, Compact Range)

- 5.1.1.2 Instrumentation (Signal Generators, Spectrum Analysers, Controllers)

- 5.1.2 Software and Analytics

- 5.1.3 Services

- 5.1.3.1 Testing and Certification Services

- 5.1.3.2 Consulting and Integration

- 5.1.1 Hardware

- 5.2 By Technology

- 5.2.1 5G NR (Sub-6 GHz and mmWave)

- 5.2.2 LTE/LTE-A/LTE-M

- 5.2.3 UMTS/WCDMA

- 5.2.4 GSM/CDMA

- 5.2.5 Wi-Fi 6/7 and Wi-Fi HaLow

- 5.2.6 Bluetooth and UWB

- 5.2.7 LPWAN (NB-IoT, LoRaWAN, Sigfox)

- 5.3 By Test Type

- 5.3.1 Antenna Performance (TRP, TIS, EIRP, EIS)

- 5.3.2 Conformance and Certification

- 5.3.3 Compatibility/Inter-operability

- 5.3.4 Production/End-of-Line

- 5.4 By Application

- 5.4.1 Telecom and Consumer Electronics

- 5.4.2 Automotive and Transportation

- 5.4.3 Industrial and Manufacturing IoT

- 5.4.4 Aerospace and Defense

- 5.4.5 Healthcare Devices and Wearables

- 5.4.6 Smart Home and Building Automation

- 5.5 By Test Environment

- 5.5.1 Far-Field Anechoic Chambers

- 5.5.2 Compact Antenna Test Range

- 5.5.3 Near-Field Systems

- 5.5.4 Reverberation Chambers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Nordics

- 5.6.2.5 Rest of Europe

- 5.6.3 South America

- 5.6.3.1 Brazil

- 5.6.3.2 Rest of South America

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South-East Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Gulf Cooperation Council Countries

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Keysight Technologies Inc.

- 6.4.2 Rohde and Schwarz GmbH and Co. KG

- 6.4.3 Anritsu Corporation

- 6.4.4 SGS SA

- 6.4.5 Intertek Group plc

- 6.4.6 Bureau Veritas SA

- 6.4.7 UL Solutions Inc.

- 6.4.8 Eurofins Scientific SE

- 6.4.9 Microwave Vision Group (MVG)

- 6.4.10 CETECOM GmbH

- 6.4.11 BluFlux LLC

- 6.4.12 Element Materials Technology

- 6.4.13 National Technical Systems Inc. (NTS)

- 6.4.14 TUV Rheinland AG

- 6.4.15 TUV SUD AG

- 6.4.16 Spirent Communications plc

- 6.4.17 VIAVI Solutions Inc.

- 6.4.18 ETS-Lindgren Inc.

- 6.4.19 Chotest Technology Inc.

- 6.4.20 Shenzhen Sunwave Communications Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

- 7.2 Emerging 6G Terahertz OTA Opportunities

- 7.3 Sustainability-Driven Low-Power OTA Protocols

OTA 傳輸平台市場報告(按組件(硬體、服務)、平台類型(電視、廣播、行動、串流媒體設備等)、最終用戶(個人、商業)和地區分類,2025 年至 2033 年2025 年至 2033 年無線測試市場(按技術、應用、產業垂直領域和地區)報告

OTA 傳輸平台市場報告(按組件(硬體、服務)、平台類型(電視、廣播、行動、串流媒體設備等)、最終用戶(個人、商業)和地區分類,2025 年至 2033 年2025 年至 2033 年無線測試市場(按技術、應用、產業垂直領域和地區)報告 無線 (OTA) 測試市場(按服務提供、技術、應用和行業垂直分類)—2025-2030 年全球預測

無線 (OTA) 測試市場(按服務提供、技術、應用和行業垂直分類)—2025-2030 年全球預測 無線測試市場機會、成長促進因素、產業趨勢分析與 2024 - 2032 年預測

無線測試市場機會、成長促進因素、產業趨勢分析與 2024 - 2032 年預測 到 2030 年 OTA(無線)測試市場預測:按組件、技術、最終用戶和地區分類的全球分析

到 2030 年 OTA(無線)測試市場預測:按組件、技術、最終用戶和地區分類的全球分析 OTA(無線)市場:產品(解決方案(FOTA、SOTA)、服務)、應用程式(OTA 測試、無線通訊、軟體/韌體更新、監管合規性)、產業(汽車、BFSI、零售)、按地區- 2031 年全球預測OTA 市場規模、佔有率、趨勢分析報告:按組件、按技術、按最終用途、按地區、細分市場預測,2024-2030 年

OTA(無線)市場:產品(解決方案(FOTA、SOTA)、服務)、應用程式(OTA 測試、無線通訊、軟體/韌體更新、監管合規性)、產業(汽車、BFSI、零售)、按地區- 2031 年全球預測OTA 市場規模、佔有率、趨勢分析報告:按組件、按技術、按最終用途、按地區、細分市場預測,2024-2030 年