|

市場調查報告書

商品編碼

1851162

過氧乙酸:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)Peracetic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

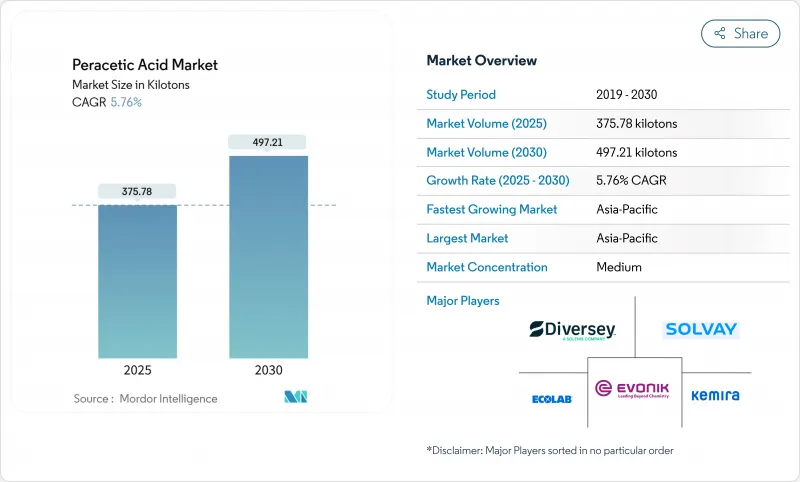

預計到 2025 年,過氧乙酸市場規模將達到 375.78 千噸,到 2030 年將達到 497.21 千噸,在預測期(2025-2030 年)內複合年成長率為 5.76%。

推動這一前景的因素包括:監管政策轉向逐步淘汰氯基除生物劑、巴氏殺菌系統的應用以及對水資源再利用基礎設施的持續投資。食品加工商對經批准的頻譜抗菌劑的需求不斷成長,這些抗菌劑用於有機物處理和無殘留消毒,進一步推動了銷售量成長。生產商也在利用製程創新來穩定水性混合物、降低運輸成本並減少工人接觸風險。在亞太和北美地區的收購凸顯了企業策略轉向區域生產基地,以便快速滿足高成長終端用戶的需求。

全球過氧乙酸市場趨勢與洞察

水處理產業的需求不斷成長

市政和工業業者正在轉向使用過氧乙酸,因為它會分解成乙酸、水和氧氣,從而避免產生受監管的消毒副產物。儘管由於2024年飲用水中全氟烷基和多氟烷基物質(PFAS)法規的實施,對殘留化學物質的審查力度加大,但初步試驗已證實,過氧乙酸在較寬的pH範圍內均能有效惰性病毒和原生動物。由於該氧化劑可透過現有的漂白劑供應管線注入,維修成本低,從而降低了資本支出。此外,也有報告指出,過氧乙酸還能減少膜上的生物膜積聚,縮短清洗週期,並延長設備使用壽命。這些性能和合規性優勢相結合,將使大型市政系統在2027年之前能夠提高平均投加量,尤其是在中國和美國排放標準日益嚴格的背景下。

促進食品和飲料衛生的食品安全法規

美國農業部有機法規允許使用過氧乙酸進行設備和表面消毒,而美國環保署500ppm的殘留豁免規定則消除了傳統氯清洗中常見的微生物滯留時間過長的問題。使用乾粉或泡沫穩定型過氧乙酸製劑的加工商正在提高肉類和農產品加工廠的生產效率,減少用水量並加快生產線切換速度。研究表明,濃度為100ppm或更低的除生物劑即可有效殺滅沙門氏菌和李斯特菌,並符合潔淨標示標準。美國職業安全與健康管理局(OSHA)2024年10月發布的肉類加工指南強調過氧乙酸是一種有效的細菌控制方案,鼓勵高風險工廠採用此方案。先前因過氧乙酸保存期限短而猶豫不決的小型加工商現在開始購買保存期限長達6個月的預稀釋袋裝系統,這在農村地區催生了新的市場需求。

職業事故及處理問題

美國職業安全與健康管理局 (OSHA) 將過氧乙酸列為高度危險化學品,當庫存超過 1000 磅時,必須遵守製程安全法規。過氧乙酸的蒸氣閾值值為 1.24 mg/m³,因此相關設施必須安裝專用通風系統和連續監測器。規模較小的加工企業有時缺乏實施這些控制規定的資金,導致其實施延遲。在預算允許的情況下,工人必須穿戴經過密合性測試的呼吸器和化學防護個人防護裝備 (PPE),這增加了訓練成本。過氧乙酸對軟金屬具有腐蝕性,因此需要使用聚合物或不銹鋼管道,這增加了改造成本。雖然自動注射系統減少了直接接觸,但保險公司仍會收取高額保費,直到證明多年的事故率處於有利水平為止。

細分市場分析

到2024年,液態過氧乙酸將佔過氧乙酸市場68.17%的佔有率,相當於超過25.5萬噸。其可靠性、供應穩定性以及配方簡單性是其領先優勢的支撐因素。隨著市政部門、酪農和飲料生產商採用成熟的飼料系統,液態過氧乙酸市場規模預計將穩定成長。然而,水性混合物的成長速度最快,複合年成長率達5.98%。供應商目前正在配製含有過氧化氫和穩定劑的緩衝過氧乙酸,以將保存期限延長至12個月並降低處置成本。混合物的運輸濃度較低,因此運輸規範要求較低,在農村地區的應用也更廣泛。設備製造商正在將這些混合物與線上稀釋模組配合使用,以減少工人接觸,從而推動其在精釀啤酒廠和分散式水資源再利用裝置中的應用。粉末和顆粒則滿足了對長期儲存和零洩漏運輸至關重要的特殊衛生需求,例如在偏遠礦區和軍用廚房。

技術進步促進了產品形式的多樣化。泡沫穩定的噴霧劑可附著於垂直表面,延長孵化場和肉類的接觸時間。乾粉混合袋可在現場溶解,形成針對性濃度,用於清潔農產品,同時減輕重量和降低運輸成本。供應商聲稱,他們可以將乾粉產品分銷的碳排放減少20%。在預測期內,不斷上漲的能源成本和淨零排放目標將促使用戶轉向濃縮乾粉泡沫,儘管需要復溶步驟。整體而言,產品形式的多樣化增強了供應商的韌性,並鼓勵客製化,但除非監管措施或保險費大幅增加,否則液體產品仍可能保持其大容量優勢。

預計到2024年,中等濃度(5-15%)的過氧乙酸將佔過氧乙酸市場(約20萬噸)的54.17%。此濃度範圍的過氧乙酸可達到6-log的微生物殺滅效果,同時低於防爆儲存所需的閾值,為使用者提供最佳的成本效益比。飲料灌裝機、起司輪和家禽加工廠的噴霧冷卻器等設備的需求是推動該市場成長的主要因素,這些設備需要在換班時進行消毒。到2030年,該市場將以6.02%的複合年成長率成長,這主要得益於東南亞新參與企業選擇中等濃度包裝以滿足進口設備的規格要求。低濃度(<5%)的過氧乙酸適用於餐飲連鎖店和醫用表面擦拭巾等小眾即用型包裝。高濃度(>15%)的過氧乙酸用於軟式內視鏡再處理和製藥無塵室的散裝消毒劑,但其高昂的處理成本限制了其廣泛應用。

混配商正在設計添加了防腐蝕添加劑的中級配方,使其能夠與鋁製輸送機和計量泵接觸。這種相容性為客戶節省了昂貴的升級不銹鋼設備的費用。同時,聯網計量器會記錄濃度數據以審核追蹤,從而減輕了美國食品藥物管理局 (FDA) 和歐盟的衛生記錄要求。這些改進措施提高了轉換成本,並導致供應商鎖定。儘管原物料價格波動可能擠壓淨利率,但生產商正透過雙重醋酸採購和期貨合約進行避險。具有競爭力的價格可見度使中級價差保持在永續的範圍內,使其在未來幾年內保持穩定。

區域分析

亞太地區,以中國、印度和泰國為首,預計2024年將佔全球銷售額的38.24%。可支配收入的成長推動了包裝食品的需求,而諸如中國GB 31604.1食品接觸材料標準等嚴格法規,正促使加工商轉向氯的替代品。日本唯一的生產商正利用非氯技術吸引高純度電子和製藥業的客戶。政府對智慧水網的投資也推動了過氧乙酸進入三級消毒階段。該地區預計6.75%的複合年成長率主要得益於印度和印尼的醫院建設。

北美市場雖然仍較成熟,但規模龐大。 2024 年 PFAS 法規和美國環保署 (EPA) 的蒸氣滅菌排放提案正促使公用事業公司和醫院考慮使用過氧乙酸以符合相關規定。肉類和家禽出口依賴美國)批准的消毒劑,大型加工商通常將化學物質與自動化噴霧櫃結合使用。美國創新叢集聚集了多家配方專家,供應乾粉級和緩衝級產品。市政再利用計劃,例如加州的聖地牙哥純淨水計劃,正在推動基準需求。由於維修活動和產品多樣化,全部區域的成長接近全球平均水平。

在永續性指令的推動下,歐洲正呈現穩定擴張的態勢。斯堪地那維亞的紙漿廠正在引入過氧乙酸漂白過程以獲得生態標籤認證,德國和比利時的啤酒廠則採用低發泡混合物進行生產線清洗。歐盟的職業安全指令限制了操作人員的曝射量,並鼓勵採用封閉式進料系統。新興的東歐國家正在凝聚基金的支持下升級市政污水處理設施,並引入過氧乙酸進行二次消毒。儘管目前處理量成長緩慢,但更嚴格的碳排放和氯排放限制使得相關技術的應用預計在2030年之前進一步推廣。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 水處理產業的需求不斷成長

- 食品安全法規旨在改善食品和飲料衛生狀況

- 醫療設備低溫滅菌技術的發展

- 從氯漂白劑轉向環保紙漿漂白劑

- 在各行業中作為消毒劑的應用日益廣泛

- 市場限制

- 職業危害及應對挑戰

- 高成本與氯基替代品

- 前驅乙酸酐的價格波動

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按產品形式

- 液體溶液

- 粉末/顆粒

- 水性混合物

- 按濃縮級

- <5% PAA(低)

- 5-15% PAA(中)

- PAA含量15%或以上(高)

- 透過使用

- 消毒劑

- 氧化劑

- 消毒器

- 其他用途(漂白、消毒等)

- 按最終用戶行業分類

- 食品和飲料加工

- 水處理

- 紙漿和造紙

- 醫療保健(包括藥品)

- 化學

- 其他終端用戶產業(農業、水產養殖等)

- 按地區(數量)

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ACURO ORGANICS LIMITED

- Aditya Birla Chemicals

- Airedale Group

- Biosan

- Brainerd Chemical

- Christeyns

- Diversey, Inc

- Ecolab

- Enviro Tech Chemical Services, Inc.

- Evonik Industries AG

- Hydrite Chemical

- Jubilant Pharmova Limited

- Kemira

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Solvay

- STOCKMEIER Group

第7章 市場機會與未來展望

The Peracetic Acid Market size is estimated at 375.78 kilotons in 2025, and is expected to reach 497.21 kilotons by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The outlook benefits from regulatory shifts that discourage chlorine-based biocides, uptake in low-temperature sterilization systems, and ongoing investment in water reuse infrastructure. Rising demand from food processors that require broad-spectrum antimicrobials approved for organic handling and residue-free sanitation further supports volume gains. Producers are also capitalizing on process innovations that stabilize aqueous blends, lower shipping costs, and cut worker exposure risks. Acquisitions in Asia-Pacific and North America underline a strategic pivot toward regional production hubs able to serve high-growth end-uses quickly.

Global Peracetic Acid Market Trends and Insights

Growing Demand From Water Treatment Industry

Municipal and industrial operators are switching to peracetic acid because it breaks down into acetic acid, water, and oxygen, thus avoiding regulated disinfection by-products. The 2024 PFAS drinking-water rule has intensified scrutiny of residual chemicals, and pilot trials confirm that peracetic acid achieves superior virus and protozoa inactivation across wide pH ranges. Retrofit costs stay low because the oxidant can be dosed through existing bleach feed lines, trimming capital outlays. Operators also report lower biofilm build-up in membranes, which reduces cleaning cycles and extends asset life. These performance and compliance benefits combine to raise average dose volumes in large municipal systems, particularly through 2027 when tighter effluent targets phase in across China and the United States.

Food-safety Regulations Boosting Food and Beverage Sanitation

USDA organic rules permit peracetic acid for equipment and surface sanitation, and a 500 ppm residue exemption by the EPA removes microbiological hold-time delays common with legacy chlorine rinses. Processors that adopt dry or foam-stabilized peracetic acid formulations are cutting water usage and achieving quicker line changeovers, which improves throughput in meat and produce facilities. Studies show the biocide is lethal to Salmonella and Listeria at sub-100 ppm doses, supporting clean-label positioning. The October 2024 OSHA guidance for meat-packing highlighted peracetic acid as a validated bacterial control option, accelerating conversions in high-risk plants. Smaller processors, once deterred by short shelf life, now purchase diluted bag-in-box systems with six-month stability, opening new rural demand pockets.

Occupational Hazards and Handling Challenges

OSHA lists peracetic acid among highly hazardous chemicals, triggering process-safety rules at inventories above 1,000 lb. Facilities must install dedicated ventilation and continuous monitors because the vapor threshold limit is 1.24 mg/m3. Small processors sometimes lack capital for these controls, slowing adoption. Even where budgets allow, staff require fit-tested respirators and chemical splash PPE, raising training costs. Corrosivity toward soft metals demands polymer or stainless piping, adding to retrofit expenses. Although automatic dosing systems reduce direct handling, insurers still impose higher premiums until multi-year incident rates prove favorable.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Low-temperature Sterilization of Medical Devices

- Shift From Chlorine to Eco-friendly Pulp-bleaching Agents

- High Cost Versus Chlorine-based Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid solutions represented 68.17% of the peracetic acid market in 2024, equivalent to more than 255 kilo tons. Reliability, supply familiarity, and low formulation complexity sustain this lead. The peracetic acid market size for liquid products is projected to climb steadily as municipalities, dairies, and beverage lines stick with established feed systems. However, aqueous blends are scaling fastest at a 5.98% CAGR. Suppliers now formulate buffered peracetic acid with hydrogen peroxide and stabilizers that extend shelf life up to 12 months, slashing disposal costs. Blends are shipped at lower concentrations, qualifying for less stringent transport codes that widen rural reach. Equipment makers are pairing these blends with inline dilution modules that trim worker exposure, stoking adoption across craft breweries and decentralized water reuse units. Powder and granule formats occupy niche hygiene needs where long storage or zero-spill transport is vital, such as remote mines and military kitchens.

Technological progress supports form diversification. Foam-stabilized sprays cling to vertical surfaces, giving longer contact time in hatcheries and slaughterhouses. Dry-blended sachets dissolve on-site and generate targeted strengths for produce washes, reducing weight and freight. Suppliers claim 20% lower carbon footprints for dry product distribution. Over the forecast window, rising energy costs and net-zero goals should push users toward concentrated dry forms despite reconstitution steps. Overall, form variety strengthens supplier resilience and encourages customization, yet liquids will likely retain bulk dominance until regulatory moves or insurance premiums decisively penalize high-strength storage.

The peracetic acid market reported 54.17% share for the medium (5-15%) range in 2024, roughly 200 kilo tons. This span delivers six-log microbial kill while staying below thresholds that demand explosion-proof storage, giving users the best cost-to-compliance ratio. Demand stems from beverage fillers, cheese wheels, and spray chillers in poultry plants where operators sanitize every shift. The medium segment is set for a 6.02% CAGR through 2030 as new entrants in Southeast Asia choose mid-strength packages that match imported equipment specs. Low ranges under 5% serve ready-to-use niche packs for restaurant chains and medical surface wipes. High ranges above 15% feed bulk sterilizers for flexible endoscope reprocessing and pharmaceutical clean rooms but face handling premiums that limit broad uptake.

Formulators are engineering medium-grade blends with anti-corrosive additives, allowing contact with aluminum conveyors and dosing pumps. This compatibility saves clients from costly stainless upgrades. In parallel, cloud-connected meters log concentration data for audit trails, easing FDA and EU hygiene record mandates. These enhancements raise switching costs and foster supplier lock-in. Although feedstock volatility can squeeze margins, producers hedge with dual acetic acid sourcing and forward contracts. Competitive price visibility keeps medium-grade spreads within sustainable bands, preserving its anchor position in coming years.

The Peracetic Acid Market Report Segments the Industry by Product Form (Liquid Solutions, Powder/Granules, and Aqueous Blends), Concentration Grade (Less Than 5 % PAA (Low), and More), Application (Disinfectant, Oxidizer, and More), End-User Industry (Food and Beverage, Water Treatment, Pulp and Paper, Chemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific generated 38.24% of global revenue in 2024, led by China, India, and Thailand. Rising disposable incomes spur packaged food demand, while stringent rules such as China's GB 31604.1 food-contact material standard are nudging processors toward chlorine alternatives. Japan's sole producer leverages chlorine-free technology that appeals to high-purity electronics and pharmaceutical clients. Government investments in smart water grids also pull peracetic acid into tertiary disinfection stages. The region's forecast 6.75% CAGR is further backed by hospital construction in India and Indonesia, where low-temperature sterilizers suit power-constrained facilities.

North America remains a mature but sizable market. The 2024 PFAS rule and the EPA's steam sterilization emission proposals are pushing utilities and hospitals to consider peracetic acid for compliance. Meat and poultry exports rely on USDA-approved sanitizers, and large processors often pair the chemistry with automated spray cabinets. Innovation clusters in the United States Midwest house multiple formulation specialists that supply dry or buffered grades. Adoption in municipal reuse schemes like California's Pure Water San Diego project boosts baseline demand. Overall regional growth runs near the global average thanks to retrofit activity and product diversification.

Europe demonstrates stable expansion anchored by sustainability mandates. Scandinavian pulp mills deploy peracetic acid bleaching to secure eco-label status, and breweries in Germany and Belgium integrate low foaming blends for line cleaning. The EU Employment Safety Directive caps operator exposure, encouraging closed-feed systems. Emerging Eastern European members are upgrading municipal treatment works with support from cohesion funds, inserting peracetic acid into secondary disinfection. Although volume gains are moderate at present, tight carbon and chlorine discharge limits provide a long runway for additional uptake through 2030.

- ACURO ORGANICS LIMITED

- Aditya Birla Chemicals

- Airedale Group

- Biosan

- Brainerd Chemical

- Christeyns

- Diversey, Inc

- Ecolab

- Enviro Tech Chemical Services, Inc.

- Evonik Industries AG

- Hydrite Chemical

- Jubilant Pharmova Limited

- Kemira

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Solvay

- STOCKMEIER Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand From Water Treatment Industry

- 4.2.2 Food-safety regulations boosting Food and Beverage sanitation

- 4.2.3 Growth in low-temperature sterilization of medical devices

- 4.2.4 Shift from chlorine to eco-friendly pulp-bleaching agents

- 4.2.5 Increasing Usage as A Disinfectant Across Various Industries

- 4.3 Market Restraints

- 4.3.1 Occupational hazards and handling challenges

- 4.3.2 High cost versus chlorine-based substitutes

- 4.3.3 Precursor acetic-anhydride price volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Form

- 5.1.1 Liquid Solutions

- 5.1.2 Powder/Granules

- 5.1.3 Aqueous Blends

- 5.2 By Concentration Grade

- 5.2.1 Less than 5 % PAA (Low)

- 5.2.2 5-15 % PAA (Medium)

- 5.2.3 More than 15 % PAA (High)

- 5.3 By Application

- 5.3.1 Disinfectant

- 5.3.2 Oxidizer

- 5.3.3 Sterilant

- 5.3.4 Other Apllications (Bleaching Agent, Sanitizer, etc.)

- 5.4 By End-user Industry

- 5.4.1 Food and Beverage Processing

- 5.4.2 Water Treatment

- 5.4.3 Pulp and Paper

- 5.4.4 Healthcare (inc. Pharmaceutical)

- 5.4.5 Chemical

- 5.4.6 Other End-user Industries (Agriculture and Aquaculture, etc.)

- 5.5 By Geography (Volume)

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACURO ORGANICS LIMITED

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Airedale Group

- 6.4.4 Biosan

- 6.4.5 Brainerd Chemical

- 6.4.6 Christeyns

- 6.4.7 Diversey, Inc

- 6.4.8 Ecolab

- 6.4.9 Enviro Tech Chemical Services, Inc.

- 6.4.10 Evonik Industries AG

- 6.4.11 Hydrite Chemical

- 6.4.12 Jubilant Pharmova Limited

- 6.4.13 Kemira

- 6.4.14 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.15 Solvay

- 6.4.16 STOCKMEIER Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Usage In Aseptic Packaging Applications

過氧乙酸市場:全球市場按等級、形態、濃度、包裝、應用和分銷管道分類的預測-2026-2032年

過氧乙酸市場:全球市場按等級、形態、濃度、包裝、應用和分銷管道分類的預測-2026-2032年 過氧乙酸市場分析及預測(至2035年):類型、產品、應用、終端用戶、形態、技術、製程、材料類型、功能、設備

過氧乙酸市場分析及預測(至2035年):類型、產品、應用、終端用戶、形態、技術、製程、材料類型、功能、設備 過氧乙酸市場報告:依等級、應用、終端用戶產業及地區分類(2026-2034年)

過氧乙酸市場報告:依等級、應用、終端用戶產業及地區分類(2026-2034年) 2026年過氧乙酸全球市場報告

2026年過氧乙酸全球市場報告 過氧乙酸市場 - 全球產業規模、佔有率、趨勢、機會及預測(按等級、應用、最終用途產業、地區和競爭格局分類,2021-2031年)

過氧乙酸市場 - 全球產業規模、佔有率、趨勢、機會及預測(按等級、應用、最終用途產業、地區和競爭格局分類,2021-2031年) 過氧乙酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測日本過氧乙酸市場報告:依等級、應用、終端用戶產業及地區分類(2026-2034年)

過氧乙酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測日本過氧乙酸市場報告:依等級、應用、終端用戶產業及地區分類(2026-2034年) 過氧乙酸市場規模、佔有率及成長分析(按等級、應用、最終用途及地區分類)-2026-2033年產業預測

過氧乙酸市場規模、佔有率及成長分析(按等級、應用、最終用途及地區分類)-2026-2033年產業預測 全球過氧乙酸市場(按等級、應用、最終用途產業、形式和地區分類)- 預測至 2030 年

全球過氧乙酸市場(按等級、應用、最終用途產業、形式和地區分類)- 預測至 2030 年 過氧乙酸市場,規模,佔有率,趨勢,產業分析報告:各等級,各用途,各最終用途,各地區,2025年~2034年的市場預測

過氧乙酸市場,規模,佔有率,趨勢,產業分析報告:各等級,各用途,各最終用途,各地區,2025年~2034年的市場預測