|

市場調查報告書

商品編碼

1851133

數位印刷:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Digital Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

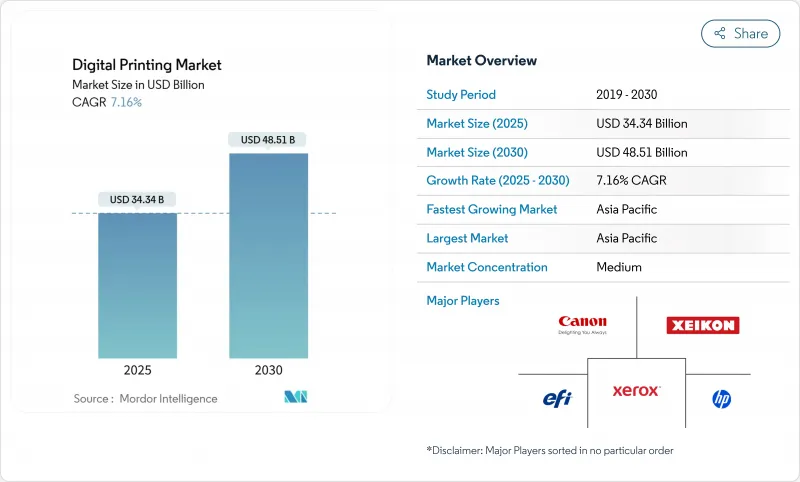

預計到 2025 年,數位印刷市場規模將達到 343.4 億美元,到 2030 年將達到 485.1 億美元,2025 年至 2030 年的複合年成長率為 7.16%。

即使供應鏈依然不穩定,對按需生產、人工智慧主導的工作流程編配以及從類比製造向數位製造轉型的強勁需求仍將支撐市場成長。市場吸引力在於能夠獲利地執行小批量生產、消除製版延遲並加快交付速度,這正吸引著尋求大規模客製化的加工商和品牌所有者。對揮發性有機化合物和全氟烷基化合物(PFAS)的監管審查正在加速向水性顏料和紫外光固化化學品的過渡,而按需噴墨列印頭的進步則不斷突破解析度、速度和基材通用性的極限。競爭策略日益圍繞著抗量子安全模組、自主維護演算法以及匯集研發資源以分攤資本成本的夥伴關係。這些因素正在匯聚,從而擴大包裝、紡織品、工業、商業和裝飾應用等市場區隔。

全球數位印刷市場趨勢與洞察

對小批量客製化包裝的需求日益成長

食品、飲料和個人護理行業的品牌所有者擴大要求批量為 10,000 件或更少,以滿足限量版產品發布和特定地區標籤的要求。採用 HP Indigo 200K 印刷機的加工商實現了無版換版,從而縮短了前置作業時間並降低了庫存風險,這使得數位印刷市場成為建立敏捷供應鏈的關鍵。電子商務的成長增加了 SKU 的複雜性,促使印刷商採用無需停機即可切換承印物和包裝盒規格的工作流程配置。零售商也越來越重視用於追蹤和防偽編碼的可變數據,這些功能無需額外工具即可在線上實現。隨著季節性和促銷週期的加劇,這些優勢進一步強化了人們對數位工作流程的偏好。

適用於小批量訂單的快速、人工智慧賦能的工作流程自動化

惠普的Nio AI智慧代理可即時最佳化油墨鋪展、噴嘴狀態和承印物推進,從而實現無人值守操作,並確保跨班次色彩的可預測性。一家日本工廠實施了AI主導的作業分組,設定表數量減少了30%,正常運作也實現了兩位數的提升。預測性維護模型可提前數週預測噴頭更換時間,從而避免計劃外停機,並為要求嚴苛的包裝客戶提供穩定的品質保障。機器學習還能最佳化每種承印物的ICC配置文件,減少高檔箔材和合成樹脂的浪費。透過減少人工投入和材料浪費,AI即使在微量印刷層也能擴大利潤空間,從而拓展了中小型加工商可進入的數位印刷市場。

高階印刷機需要高額的資本投入和研發成本

採用多層光油和白色墨水的工業噴墨生產線,單價通常超過100萬美元。空調機房、線上偵測攝影機和RIP伺服器進一步推高了初始成本,使中小型加工商無法達到最高的產能水準。快速的過時也增加了風險。噴頭每五年就需要更新換代,迫使企業持續投入資本支出,否則利潤率將面臨縮水的淨利率。大型企業集團透過企業聯合組織貸款和共享服務中心為升級提供資金,從而擴大了技術差距。這加速了產業整合,削弱了供應商規模,並將市場佔有率集中在資金最雄厚的企業手中。

細分市場分析

到2024年,噴墨技術將佔據數位印刷市場68.12%的佔有率,預計到2030年將以11.7%的複合年成長率成長。該領域的領先地位歸功於不斷縮小的墨滴體積、原生1200 dpi的列印頭以及閉合迴路液面控制技術,這些技術能夠減少在多孔和非多孔介質上出現的條紋。靜電照相技術在辦公室文件和相簿領域仍然具有應用價值,因為碳粉列印的光澤效果頗具吸引力,但由於碳粉熔合技術限制了承印物的多樣性和能源效率,其應用已趨於平穩。

Epson的直噴成型系統將六軸機器人與PrecisionCore列印頭結合,可在曲面塑膠和玻璃上實現35微米以內的套準精度。這項技術拓展至3D物件列印領域,拓寬了可應用範圍,從汽車旋鈕到飲料杯,進一步提升了該領域對整體數位印刷市場成長的貢獻。此外,噴墨列印技術還可輕鬆與水性顏料組配合使用,以應對即將到來的溶劑禁令,確保加工商的資本投資面向未來。其波形能夠動態適應黏度波動,從而提高運作並延長列印頭壽命。

溶劑型油墨預計在2024年將佔銷售額的49.43%,主要得益於其對乙烯基橫幅和車身貼膜的強附著力。然而,水性顏料系統預計將以9.34%的複合年成長率成長,這主要得益於其在室內圖形和食品包裝領域低VOC(揮發性有機化合物)的應用。 UV固化油墨將在折疊式紙盒和直接印刷應用中佔據更大的市場佔有率,因為其即時固化特性可以減少等待時間和人工成本;而乳膠混合油墨則兼顧了環保特性和戶外耐久性。

油墨製造商正在加快研發步伐,力求消除 PFAS 和芳香烴,而 Mimaki 的 2025 年 UV 油墨系列則指明了邁向無 CMR 化學品的道路。隨著認證機構設定更嚴格的過渡閾值,溶劑型油墨平台需要重新認證,這限制了其銷售成長,儘管它們歷來佔據主導地位。相反,水性顏料受益於線上乾燥器和先進底塗技術,從而能夠應用於以往難以企及的塑膠和金屬化薄膜。在預測期內,水性油墨的數位印刷市場規模預計將縮小與傳統溶劑型油墨的差距,從而重塑供應商格局和籌資策略。

數位印刷市場報告按印刷過程(靜電照相、噴墨)、油墨類型(水性顏料、溶劑型、UV固化型、其他)、基材(紙/紙板、塑膠/薄膜、紡織品/織物、其他)、應用(書籍/出版、商業印刷、包裝、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。

區域分析

亞太地區將在2024年佔全球收入的38.56%,並在2030年之前保持10.88%的最高複合年成長率,這主要得益於政府對工業4.0和積層製造生態系統的支持獎勵。中國作為高價值出口的驅動力,正在投資標籤和紙盒生產線,為高階消費品提供可變數據和彩色裝飾。日本正在推動人工智慧嵌入式工作流程,將印刷機與製造執行系統(MES)和企業資源計畫(ERP)系統同步,並最佳化工廠叢集的作業定序。印度蓬勃發展的中產階級正在推動軟質包裝的需求,吸引全球原始設備製造商(OEM)與當地整合商合作,打造承包數位化中心。

北美是一個成熟但利潤豐厚的行業,加工商正從傳統的長版柔印轉向靈活的數位印刷生產線,以滿足會員店和電商包裝中日益成長的SKU需求。美國在採用量子安全印刷技術保護品牌資產和消費者資料方面處於領先地位。加拿大注重碳透明度,推動了水性油墨和閉合迴路色彩校準技術的普及,而墨西哥則受益於近岸外包,將原本運往亞洲的組件轉運至滿足本地印刷需求的區域履約中心。

在歐洲,永續性和循環經濟的概念在歐盟綠色交易的推動下日益受到重視。紡織品和包裝的數位化產品護照需要物品等級編碼,而高解析度噴墨生產線恰好具備此特性。德國的機械工程基礎設施將印刷模組整合到機器人化的後加工單元中,而法國的奢侈品行業則對精準的專色還原和觸感光油效果有著極高的要求。英國正在挖掘創新產業對客製化限量版印刷的需求,鼓勵中小企業購買緊湊型B2幅面噴墨印表機。總而言之,這些區域性的動態正在鞏固數位印刷市場在全球下一代製造業的關鍵地位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對小批量客製化包裝的需求激增

- 適用於小批量訂單的快速、人工智慧賦能的工作流程自動化

- 歐盟和美國數位紡織微型工廠的擴張

- 更低的印刷成本和更短的交貨時間

- 市場限制

- 高階印刷機需要高額的資本投入和研發支出。

- 更嚴格的 PFAS/溶劑油墨法規導致重新認證延誤

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過印刷過程

- 電泳(墨粉)

- 噴墨

- 按墨水類型

- 水性顏料

- 溶劑

- 紫外線固化型

- 乳膠

- 熱昇華

- 按基礎材料

- 紙和紙板

- 塑膠薄膜

- 紡織品/布料

- 玻璃和陶瓷

- 金屬

- 透過使用

- 書籍/出版

- 商業印刷

- 包裹

- 標籤

- 紙板包裝

- 紙盒

- 軟包裝

- 硬質塑膠包裝

- 金屬包裝

- 紡織印花

- 照片和產品

- 標誌和大型圖形

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 波蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 奈及利亞

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HP Inc.

- Canon Inc.

- Xerox Holdings

- Ricoh Company

- Electronics For Imaging(EFI)

- Konica Minolta

- Xeikon NV

- Smurfit WestRock

- Mondi PLC

- DS Smith PLC(International Paper)

- Amcor PLC

- Multi-Color Corporation

- Avery Dennison Corporation

- Quad/Graphics Inc.

- Durst Phototechnik

- Landa Digital Printing

- Domino Printing Sciences

- Screen Holdings Co.

- Fujifilm Holdings

第7章 市場機會與未來展望

The digital printing market size is valued at USD 34.34 billion in 2025 and is forecast to reach USD 48.51 billion by 2030, advancing at a 7.16% CAGR over 2025-2030.

Robust demand for on-demand production, AI-driven workflow orchestration, and the pivot from analog to digital manufacturing keep growth resilient even as supply chains remain volatile. The market's capability to profitably execute micro-batch runs, eliminate plate-making delays, and shorten turnaround times attracts converters and brand owners seeking mass customization at scale. Regulatory scrutiny of volatile organic compounds and PFAS accelerates migration toward water-based pigment and UV-curable chemistries, while advances in drop-on-demand printheads push resolution, speed, and substrate versatility frontiers. Competitive strategies increasingly revolve around quantum-resistant security modules, autonomous maintenance algorithms, and partnerships that pool R&D assets to spread capital costs. These factors collectively widen the addressable base for the digital printing market across packaging, textile, industrial, commercial, and decor segments.

Global Digital Printing Market Trends and Insights

Booming Short-Run Customized Packaging Demand

Brand owners in food, beverage, and personal care increasingly request lot sizes below 10,000 units to support limited-edition releases and region-specific labeling requirements. Converters leveraging HP Indigo 200K presses achieve plate-free changeovers that slash lead times and inventory risk, transforming the digital printing market into a vital enabler of agile supply chains. E-commerce's growth multiplies SKU complexity, pushing printers toward workflow configurations that switch substrates and box formats without downtime. Retailers also value variable data for track-and-trace and anti-counterfeit coding, functions executed inline with no added tooling. These advantages reinforce the preference for digital workflows whenever seasonal or promotional cycles intensify.

Rapid AI-Enabled Workflow Automation for Micro-Batch Orders

HP's Nio AI agent optimizes ink laydown, nozzle health, and substrate advance in real time, enabling unattended operation and predictable color across shifts. Japanese facilities implementing AI-driven job ganging now see 30% fewer setup sheets and double-digit uptime gains. Predictive maintenance models forecast head replacements weeks in advance, preventing unplanned stops and stabilizing quality for demanding packaging accounts. Machine learning also refines ICC profiles per substrate, reducing waste on premium foils and synthetics. By collapsing labor inputs and materials overruns, AI broadens profit pools even at micro-volume tiers, enlarging the accessible digital printing market for SME converters.

High Capex and R&D Outlays for High-End Presses

Industrial inkjet lines capable of multi-layer varnish and white ink routinely exceed USD 1 million per unit. Initial spend escalates when climate-controlled rooms, inline inspection cameras, and RIP servers are included, locking smaller converters out of top-tier throughput. Rapid obsolescence compounds risk; head generations refresh within five-year windows, forcing continuous capex or risk margin erosion. Larger groups finance upgrades via syndicated loans and shared service centers, widening the technology gap. Consolidation thus accelerates, trimming the tail of the provider curve and concentrating volume among well-funded players.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Digital Textile Micro-Factories in EU and US

- Declining Per-Unit Print Cost and Faster Turnaround

- Stricter PFAS/Solvent-Ink Regulations Causing Re-Qualification Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inkjet technology commanded 68.12% of the digital printing market share in 2024 and is projected to grow at 11.7% CAGR through 2030. The segment's leadership stems from ever-smaller drop volumes, native 1,200 dpi heads, and closed-loop meniscus control that reduce banding on porous and non-porous media alike. Electrophotography maintains relevance for office documents and photo books where toner's gloss finish appeals, yet its adoption plateaus because toner fusing limits substrate diversity and energy efficiency.

Epson's Direct-to-Shape system mates six-axis robotics with PrecisionCore heads, enabling registration accuracy within 35 µm on curved plastics and glass. This expansion into 3-D objects broadens addressable applications from automotive knobs to beverage tumblers, reinforcing the segment's contribution to overall digital printing market growth. Inkjet also pairs readily with water-based pigment sets that comply with looming solvent bans, future-proofing capex for converters. As waveforms adapt dynamically to viscosity fluctuations, uptime rises and printhead life extends, counteracting historical consumables cost concerns and deepening inkjet's entrenchment.

Solvent formulations delivered 49.43% revenue in 2024 thanks to robust adhesion on vinyl banners and fleet wraps. Yet water-based pigment systems are climbing at a 9.34% CAGR as buyers favor low-VOC credentials for indoor graphics and food packaging. UV-curable inks carve share in folding carton and direct-to-object arenas where instant curing curtails wait times and labor, while latex blends balance green profile with outdoor durability.

Ink makers accelerate R&D cycles to purge PFAS and aromatic hydrocarbons; Mimaki's 2025 UV sets show the path toward CMR-free chemistry. As certification bodies impose stricter migration thresholds, solvent platforms must re-qualify, dampening volume expansion despite historical dominance. Conversely, aqueous pigments gain from inline dryers and advanced primers that open plastics and metalized films once considered out-of-reach. Over the forecast period, the digital printing market size for water-based inks is expected to close the gap with legacy solvent lines, reshaping supplier power dynamics and procurement strategies.

The Digital Printing Market Report is Segmented by Printing Process (Electrophotography, and Inkjet), Ink Type (Water-Based Pigment, Solvent, UV-Curable and More), Substrate (Paper and Paperboard, Plastics and Films, Textiles/Fabrics and More), Application (Books and Publishing, Commercial Printing, Packaging and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific retained 38.56% share of global revenue in 2024 and is set to post the highest 10.88% CAGR through 2030 thanks to state incentives supporting Industry 4.0 and additive manufacturing ecosystems. China's push toward high-value exports channels capital into label and carton lines that deliver variable data and colorful embellishments for premium consumer goods. Japan nurtures AI-infused workflows that synchronize presses with MES and ERP stacks, optimizing job sequencing across factory clusters. India's fast-growing middle class drives flexible packaging demand, attracting global OEMs to partner with local integrators on turnkey digital hubs.

North America represents a mature but lucrative arena where converters pivot from long-run flexo to agile digital lines to satisfy SKU proliferation in club stores and e-commerce packaging. The United States spearheads adoption of quantum-resistant printer security that shields brand assets and consumer data. Canada's regulatory focus on carbon transparency propels migration toward water-based inks and closed-loop color calibration, while Mexico benefits from near-shoring that routes previously Asia-bound assemblies through regional fulfillment centers requiring localized print.

Europe emphasizes sustainability and circular-economy compliance under the EU Green Deal. The Digital Product Passport for textiles and packaging necessitates item-level encoding, a function naturally embedded within high-resolution inkjet lines. Germany's mechanical engineering base integrates print modules into robotized finishing cells, while France's luxury sector insists on exacting spot-color reproduction and tactile varnish effects. The United Kingdom exploits creative industries' demand for bespoke limited-run prints, encouraging SMEs to buy compact B2 inkjet units. Collectively, these regional dynamics reinforce the digital printing market as a cornerstone of next-generation manufacturing worldwide.

- HP Inc.

- Canon Inc.

- Xerox Holdings

- Ricoh Company

- Electronics For Imaging (EFI)

- Konica Minolta

- Xeikon NV

- Smurfit WestRock

- Mondi PLC

- DS Smith PLC (International Paper)

- Amcor PLC

- Multi-Color Corporation

- Avery Dennison Corporation

- Quad/Graphics Inc.

- Durst Phototechnik

- Landa Digital Printing

- Domino Printing Sciences

- Screen Holdings Co.

- Fujifilm Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming short-run customised packaging demand

- 4.2.2 Rapid AI-enabled workflow automation for micro-batch orders (under-the-radar)

- 4.2.3 Expansion of digital textile micro-factories in EU and US (under-the-radar)

- 4.2.4 Declining per-unit print cost and faster turnaround

- 4.3 Market Restraints

- 4.3.1 High capex and RandD outlays for high-end presses

- 4.3.2 Stricter PFAS/solvent-ink regulations causing re-qualification delays (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Process

- 5.1.1 Electrophotography (Toner)

- 5.1.2 Inkjet

- 5.2 By Ink Type

- 5.2.1 Water-based pigment

- 5.2.2 Solvent

- 5.2.3 UV-curable

- 5.2.4 Latex

- 5.2.5 Dye-Sublimation

- 5.3 By Substrate

- 5.3.1 Paper and Paperboard

- 5.3.2 Plastics and Films

- 5.3.3 Textiles/Fabrics

- 5.3.4 Glass and Ceramics

- 5.3.5 Metals

- 5.4 By Application

- 5.4.1 Books and Publishing

- 5.4.2 Commercial Printing

- 5.4.3 Packaging

- 5.4.3.1 Labels

- 5.4.3.2 Corrugated Packaging

- 5.4.3.3 Cartons

- 5.4.3.4 Flexible Packaging

- 5.4.3.5 Rigid Plastic Packaging

- 5.4.3.6 Metal Packaging

- 5.4.4 Textile Printing

- 5.4.5 Photographic and Merchandise

- 5.4.6 Signage and Large-Format Graphics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Russia

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Kenya

- 5.5.4.2.3 Nigeria

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Xerox Holdings

- 6.4.4 Ricoh Company

- 6.4.5 Electronics For Imaging (EFI)

- 6.4.6 Konica Minolta

- 6.4.7 Xeikon NV

- 6.4.8 Smurfit WestRock

- 6.4.9 Mondi PLC

- 6.4.10 DS Smith PLC (International Paper)

- 6.4.11 Amcor PLC

- 6.4.12 Multi-Color Corporation

- 6.4.13 Avery Dennison Corporation

- 6.4.14 Quad/Graphics Inc.

- 6.4.15 Durst Phototechnik

- 6.4.16 Landa Digital Printing

- 6.4.17 Domino Printing Sciences

- 6.4.18 Screen Holdings Co.

- 6.4.19 Fujifilm Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

數位印刷市場報告:按類型、油墨類型、應用和地區分類(2026-2034年)

數位印刷市場報告:按類型、油墨類型、應用和地區分類(2026-2034年) 陶瓷餐具數位印刷市場報告:趨勢、預測及競爭分析(至2035年)

陶瓷餐具數位印刷市場報告:趨勢、預測及競爭分析(至2035年) 數位印刷市場:按交付方式、應用程式、銷售管道和最終用戶分類的全球市場預測 – 2026-2032 年數位包裝和標籤市場:2026-2032年全球市場預測(按包裝類型、印刷技術、油墨類型、最終用途行業和應用分類)餐具數位印刷市場:依產品類型、材料類型、印刷技術、印表機類型、最終用戶和通路分類-2026-2032年全球市場預測數位電子看板印表機市場:依列印技術、產品類型、安裝方式、連接方式、列印寬度和應用領域分類-全球預測,2026-2032年

數位印刷市場:按交付方式、應用程式、銷售管道和最終用戶分類的全球市場預測 – 2026-2032 年數位包裝和標籤市場:2026-2032年全球市場預測(按包裝類型、印刷技術、油墨類型、最終用途行業和應用分類)餐具數位印刷市場:依產品類型、材料類型、印刷技術、印表機類型、最終用戶和通路分類-2026-2032年全球市場預測數位電子看板印表機市場:依列印技術、產品類型、安裝方式、連接方式、列印寬度和應用領域分類-全球預測,2026-2032年 數位印刷市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、設備及最終用戶分類

數位印刷市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、設備及最終用戶分類 2026-2030年全球影印機市場指示牌印表機市場:依墨水技術、印表機類型、印表機技術、應用程式、銷售管道和最終用戶分類,全球預測,2026-2032年

2026-2030年全球影印機市場指示牌印表機市場:依墨水技術、印表機類型、印表機技術、應用程式、銷售管道和最終用戶分類,全球預測,2026-2032年 影印機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(單色影印機、彩色影印機、其他)、按應用(學校、政府、辦公室、零售店、其他)、按地區和競爭情況細分,2020-2030 年預測

影印機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(單色影印機、彩色影印機、其他)、按應用(學校、政府、辦公室、零售店、其他)、按地區和競爭情況細分,2020-2030 年預測