|

市場調查報告書

商品編碼

1851081

氣相層析法:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Gas Chromatography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

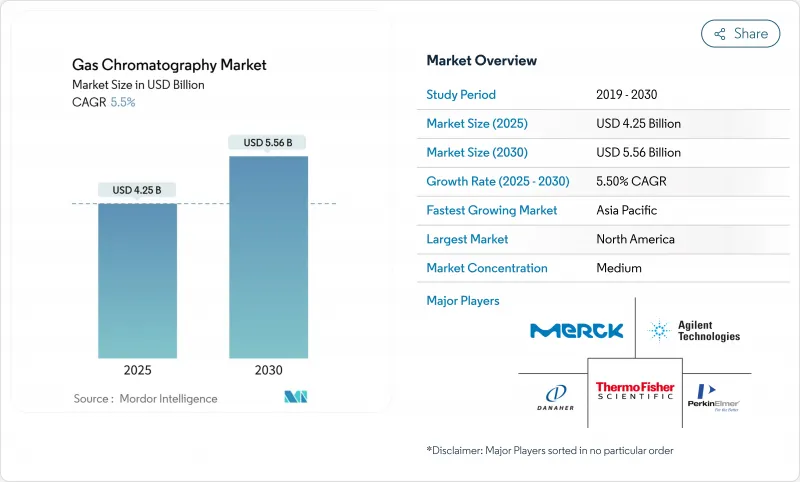

預計到 2025 年,氣相層析法市場規模將達到 42.5 億美元,到 2030 年將達到 55.6 億美元,年複合成長率為 5.50%。

環境和藥物檢測領域日益嚴格的法規、氫能系統等技術的快速升級以及載氣供應鏈的積極策略,都在推動著這一穩步發展趨勢。全球實驗室正從氦氣轉向氫氣和氮氣,在降低營運成本的同時,也減少了對稀缺惰性氣體的依賴。與質譜儀的整合如今已成為資本支出計劃的重點,它將分離和鑑定整合到一次運行中,提高了分析通量,並增強了數據完整性。可攜式和微型氣相層析儀正在重塑現場分析,而技術創新,尤其是在氣體發生器和低相容比毛細管柱等配件方面的創新,表明永續和自主運行將在2030年之前成為競爭優勢的關鍵所在。

全球氣相層析法市場趨勢與洞察

擴大 GC-MS 工作流程的應用

氣相層析法質譜聯用技術(GC-MS)現已成為受監管產業的標準做法。製藥研發管線利用GC-MS進行雜質分析,超過80%的新藥認證申請會參考整合層析法資料系統。環保機構使用GC-MS來檢測微量污染物,而大氣壓力化學電離等技術的進步進一步提高了靈敏度。這些功能的結合縮短了樣品製備步驟,節省了分析人員的時間,並滿足了監管機構對資料完整性的要求。

氣相層析在藥物核准品管中的作用日益增強

美國食品藥物管理局 (FDA) 嚴格的製程分析技術指南要求進行即時監測,這促使企業投資建設能夠在生產車間連續運作的高性能氣相層析 (GC) 設備。2D氣相層析 (2D GC) 和自動化雜質定量技術能夠應對生物製藥的特性,而機器學習演算法則能加速峰值識別,從而強化 GC 在加快核准中的作用。

對先進GC平台的高額資本投入

一套完整的2D氣相層析質譜聯用系統單價可能超過50萬美元,而安裝和服務合約可能使總成本增加30%。小型實驗室在設備升級方面一直較為滯後,但租賃項目和設備共用計畫正在蓬勃發展,逐漸降低了經濟門檻。

細分市場分析

系統仍將是主要市場參與者,預計2024年將貢獻38.50%的銷售額。受更新換代週期和整合檢測器的推動,這些桌上型氣相層析法儀的市場規模預計將持續成長。可攜式和微型氣相層析儀以9.84%的複合年成長率成長,滿足了緊急應變、採礦、燃料配送和其他行業的現場監測需求。例如,FLIR Griffin G510等儀器在堅固耐用的機殼中提供了實驗室等級的檢測能力。現場安裝可縮短樣品處理時間並支援即時決策。添加自動取樣器還可以彌補技能差距並標準化通量,而分液收集器則為製備工作流程開闢了一片天地。檢測器升級和基於MEMS的創新將分析擴展到以前無法進入的環境,從而增強了可攜式系統在氣相層析法市場中的重要性。

與此同時,高性能模組正朝著小型化方向發展。柱上加熱器、微型進樣器和快速冷卻設計在保持層析法分離度的同時,顯著縮小了體積。氫氣載氣偏好符合可攜式的功率預算和環保目標,正推動對氫燃料電池微型氣相層析儀的需求。預計未來五年,成本的持續降低將推動可攜式氣相層析法平台市場佔有率的成長。

2024年,色譜柱將佔總支出的46.26%,這反映了其作為耗材的地位,以及其可預測的更換週期。低相容比毛細管的創新提高了揮發性硫化物的惰性和峰形。然而,隨著實驗室以按需供應的氫氣、氮氣和零級空氣取代鋼瓶,氣體發生器的年複合成長率高達8.8%。 PEAK Scientific收購Noblegen擴大了該領域的產能,並使其業務遍及全球。保護柱和高純度接頭等色譜柱附件可提高維護效率。採用先進合金製成的壓力穩壓器可承受氫氣的使用,而支援RFID的閥門可自動發出更換警報。改進的管路可減少死體積、提高峰形對稱性並節省氣體。隨著永續性受到重視,能夠減少浪費並提高儀器運作運行時間的優質耗材價格更高,這將直接影響氣相層析法市場。

區域分析

2024年,北美將佔全球銷售額的36.36%,這主要得益於美國環保署(EPA)的強力監管、強勁的製藥生產以及眾多分析密集型產業。賽默飛世爾科技(Thermo Fisher)在北美地區20億美元的擴張計劃,體現了其對設備持續需求的信心。在美國,飲用水中全氟烷基和多氟烷基物質(PFAS)的檢測標準要求低於兆分之一,這項要求正在逐步實施,推動了實驗室的升級改造和新設備的安裝。加拿大和墨西哥將憑藉著不斷成長的石化產品產量和統一的環境通訊協定,為市場成長提供助力,確保在整個預測期內設備都能保持積極的更新換代。

歐洲憑藉著影響深遠的環境指令和嚴格的食品安全法規,保持其第二梯隊的領先地位。聯邦層級的農藥殘留限制和積極的微塑膠治理措施推動了對高靈敏度氣相層析儀平台的需求,而氫能轉化獎勵則與區域能源目標相契合。德國、英國和法國佔據訂單主導地位,義大利和西班牙的農產品品質檢測業務也呈現成長態勢。歐洲市場重視低功耗、氫能最佳化的儀器以及能夠簡化GDPR和GMP法規合規性的整合式資料完整性模組。

亞太地區以8.74%的複合年成長率成為成長最快的地區,這主要得益於工業化、藥品產量成長以及先進的監測方法。中國仍是最大的市場貢獻者,但受宏觀經濟逆風的影響,供應商的銷售額有所波動。日本和印度將透過清潔能源計畫和原料藥生產規模的擴大來加速需求成長。韓國正在投資需要超微量分析的高科技產業,而澳洲的採礦業正在採用可攜式氣相層析儀來簡化現場調查。技術轉移、本地化生產和政府資助計畫正在擴大潛在市場,鞏固該地區在未來氣相層析法市場成長中的地位。

隨著中東和非洲的石化企業對其品質實驗室進行現代化改造,該地區正迎來新的發展勢頭。海灣合作理事會(GCC)煉油廠升級和氫氣生產的投資帶來了穩定的設備訂單,而南非的採礦和化學工業則依賴氣相層析(GC)平台進行製程控制。經濟波動將抑制短期內的訂單量,但區域內與國際標準的接軌將推動技術的逐步普及。

南美洲呈現緩慢但穩定的成長態勢。巴西的製藥和石化產業叢集著訂單,而阿根廷的農產品則推動了農藥殘留檢測的發展。區域貿易協定促進了設備跨境流動,智利的銅礦開採業務則整合了線上氣相層析系統以符合排放標準。外匯波動和政治變革加劇了市場波動,但當地分銷商透過提供融資和維護合約來降低風險。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- GC-MS工作流程的日益普及

- 擴大GC在藥物核准品管中的作用

- 頁岩氣與石油化學分析擴展

- 世界各地都制定了嚴格的空氣和水質法規。

- 在全球氦氣短缺的情況下,轉向使用氫氣作為載氣

- PFAS/微塑膠監測要求激增

- 市場限制

- 對尖端GC平台的高額資本投入

- 訓練有素的色譜分析人員短缺

- 氦氣供應鏈波動影響運轉率

- 遵守氣相層析溶劑排放法規的成本

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依設備類型

- 系統

- 檢測器

- 自動取樣器

- 分液收集器

- 微型可攜式層析儀

- 其他設備

- 配件及耗材

- 柱子

- 立柱配件

- 壓力調節器

- 瓦斯發電機

- 管件和管材

- 其他

- 按下檢測器類型

- 火焰離子化檢測器(FID)

- 熱導檢測器(TCD)

- 電子捕獲檢測器(ECD)

- 質譜檢測器(GC-MS)

- 其他

- 最終用戶

- 製藥和生物技術公司

- 石油天然氣/石化業

- 環境和污水處理劑

- 食品飲料業

- 學術和政府研究機構

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Agilent Technologies

- Shimadzu Corporation

- Thermo Fisher Scientific

- Danaher(Cytiva & Pall)

- PerkinElmer

- Merck KGaA

- Waters Corporation

- Teledyne Technologies

- Restek Corporation

- Chromatotec

- Scion Instruments

- Sartorius

- Air Liquide(Extended Life Sciences)

- Process Sensing Tech(LDetek)

- Hobre Instruments BV

- Phenomenex

- Bruker Corporation

- LECO Corporation

- Markes International

- Falcon Analytical

第7章 市場機會與未來展望

The gas chromatography market stands at USD 4.25 billion in 2025 and is forecast to reach USD 5.56 billion by 2030, advancing at a 5.50% CAGR.

Heightened regulatory scrutiny in environmental and pharmaceutical testing, rapid technology upgrades such as hydrogen-ready systems, and proactive supply-chain strategies around carrier gases underpin this steady trajectory. Laboratories worldwide are moving from helium to hydrogen and nitrogen, trimming operating costs while reducing dependence on scarce noble gas supplies. Integrations with mass spectrometry now dominate capital-spending agendas because they condense separation and identification into a single run, accelerating throughput and improving data integrity. Portable and micro-GC units are reshaping field analytics, and accessory innovations, particularly gas generators and low-phase-ratio capillary columns, signal that sustainable, autonomous operations will define competitive advantage through 2030.

Global Gas Chromatography Market Trends and Insights

Rising Adoption of GC-MS Workflows

Linking gas chromatography with mass spectrometry is now standard practice across regulated industries. Pharmaceutical pipelines rely on GC-MS for impurity profiling, and more than 80% of new-drug dossiers reference integrated chromatography data systems. Environmental agencies use GC-MS to detect contaminants at trace levels, and developments such as atmospheric pressure chemical ionization push sensitivity even further. These combined capabilities shorten sample preparation steps, free analyst time, and meet regulators' data-integrity demands.

Growing Role of GC in Drug-Approval Quality Controls

Stringent process analytical technology guidance from the FDA mandates real-time monitoring, driving investment in rugged GC units that can run continuously on production floors. Two-dimensional GC and automated impurity quantitation address increasingly complex biologic formulations, while machine-learning algorithms accelerate peak identification, reinforcing GC's role in fast-tracking approvals.

High Capital Expenditure for Advanced GC Platforms

Comprehensive two-dimensional GC-MS systems can top USD 500,000 per unit, and installation plus service contracts can add 30% to total spend. Smaller laboratories delay upgrades, yet leasing programs and shared-instrument initiatives are gaining momentum, softening the financial barrier.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Shale-Gas & Petrochemical Analytics

- Stringent Air & Water-Quality Regulations Worldwide

- Shortage of Trained Chromatographers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Systems remained the workhorse, contributing 38.50% to 2024 revenue. The gas chromatography market size for these benchtop units will continue to rise, propelled by replacement cycles and integrated detectors. Portable and micro-GC instruments, growing at 9.84% CAGR, meet on-site monitoring needs in emergency response, mining, and fuel distribution. Devices such as the FLIR Griffin G510 deliver laboratory-grade detection in rugged housing. Field deployability saves sample-handling time and supports real-time decision making. Laboratories also add auto-samplers to close skill gaps and standardize throughput, while fraction collectors carve niches in preparative workflows. Detector upgrades and MEMS-based innovations extend analytics to previously inaccessible environments, reinforcing the relevance of portable systems within the gas chromatography market.

A parallel trend is the miniaturization of high-performance modules: on-column heaters, micro-injectors, and rapid cooling designs shrink physical footprints while maintaining chromatographic resolution. The preference for hydrogen carrier gas aligns with portable power budgets and environmental objectives, reinforcing demand for hydrogen-ready micro-GCs. Continuous cost improvements suggest portable platforms will capture a growing slice of gas chromatography market share over the next five years.

Columns captured 46.26% of the 2024 spend, reflecting their status as consumables with predictable replacement intervals. Low-phase-ratio capillary innovations improve inertness and peak shape for volatile sulfur compounds. Gas generators, however, are racing ahead at an 8.8% CAGR as labs swap cylinders for on-demand hydrogen, nitrogen, and zero air. PEAK Scientific's takeover of Noblegen extends capacity and global reach in this segment. Column accessories such as guard columns and high-purity connectors keep maintenance workflows efficient. Pressure regulators made from advanced alloys withstand hydrogen service, while RFID-enabled valves automate replacement alerts. Tubing refinements cut dead volume, sharpening peak symmetry and conserving gas. As sustainability priorities climb, premium consumables that reduce waste and extend instrument uptime earn price premiums, directly influencing the gas chromatography market.

The Gas Chromatography Market is Segmented by Instrument (Systems, Detectors, Auto-Samplers, and More), Accessories & Consumables (Columns, Column Accessories, and More), Detector Type (Flame Ionization, Thermal Conductivity, and More), End User (Pharmaceutical & Biotechnology, Oil & Gas, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributes 36.36% of global revenue in 2024, anchored by robust EPA mandates, strong pharmaceutical output, and a deep bench of analytically intensive industries. Thermo Fisher's USD 2 billion domestic expansion plan asserts confidence in sustained equipment demand. The United States enforces PFAS drinking-water limits that require sub-parts-per-trillion detection, driving laboratory upgrades and new installations. Canada and Mexico supplement growth via petrochemical outputs and harmonized environmental protocols, ensuring replacement cycles stay active throughout the forecast window.

Europe maintains second-tier leadership through far-reaching environmental directives and stringent food-safety regulations. Union-wide pesticide residue controls and vigorous microplastic initiatives elevate demand for sensitive GC platforms, and hydrogen conversion incentives align with regional energy goals. Germany, the United Kingdom, and France dominate orders, while Italy and Spain grow through agricultural quality testing. The European market rewards low-power, hydrogen-optimized instruments and integrated data integrity modules that simplify compliance with GDPR and GMP provisions.

Asia Pacific records the fastest trajectory at 8.74% CAGR, driven by industrialization, rising pharmaceutical output, and progressive monitoring laws. China remains the largest contributor, though vendor sales fluctuated amid macroeconomic headwinds. Japan and India accelerate demand through clean-energy programs and API manufacturing scale-up. South Korea invests in high-tech industries requiring ultra-trace analytics, whereas Australia's mining sector adopts portable GC units for site survey efficiency. Technology transfer, local production, and government funding schemes expand the addressable base, cementing the region's role in future gas chromatography market growth.

Middle East and Africa register emerging momentum as petrochemical complexes modernize quality labs. GCC investments in refinery upgrades and hydrogen production translate into steady instrument orders, while South Africa's mining and chemicals sectors rely on GC platforms for process control. Economic variance tempers short-term volumes, but regional alignment with international standards fosters gradual adoption.

South America presents moderate yet stable expansion. Brazil's pharmaceutical and petrochemical clusters anchor orders, and Argentine agribusiness drives pesticide residue testing. Regional trade pacts ease cross-border equipment movement, and Chilean copper operations integrate online GC systems for emission compliance. Currency swings and political shifts add volatility, but local distributors offset risk by offering financing and maintenance contracts.

- Agilent Technologies

- Shimadzu

- Thermo Fisher Scientific

- Danaher (Cytiva & Pall)

- PerkinElmer

- Merck

- Waters Corporation

- Teledyne Technologies

- Restek

- Chromatotec

- Scion Instruments

- Sartorius

- Air Liquide (Extended Life Sciences)

- Process Sensing Tech (LDetek)

- Hobre Instruments

- Phenomenex

- Bruker

- LECO

- Markes International

- Falcon Analytical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of GC-MS Workflows

- 4.2.2 Growing Role of GC In Drug-Approval Quality Controls

- 4.2.3 Expansion of Shale-Gas & Petrochemical Analytics

- 4.2.4 Stringent Air- & Water-Quality Regulations Worldwide

- 4.2.5 Shift To Hydrogen Carrier Gas Amid Global Helium Shortage

- 4.2.6 Surge In PFAS/Micro-Plastic Monitoring Requirements

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure For Advanced GC Platforms

- 4.3.2 Shortage Of Trained Chromatographers

- 4.3.3 Supply-Chain Volatility for Helium Impacting Uptime

- 4.3.4 Emission-Control Compliance Costs for GC Solvents

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Instrument Type

- 5.1.1 Systems

- 5.1.2 Detectors

- 5.1.3 Auto-samplers

- 5.1.4 Fraction Collectors

- 5.1.5 Micro & Portable GC

- 5.1.6 Other Instruments

- 5.2 By Accessories & Consumables

- 5.2.1 Columns

- 5.2.2 Column Accessories

- 5.2.3 Pressure Regulators

- 5.2.4 Gas Generators

- 5.2.5 Fittings & Tubing

- 5.2.6 Others

- 5.3 By Detector Type

- 5.3.1 Flame Ionization Detector (FID)

- 5.3.2 Thermal Conductivity Detector (TCD)

- 5.3.3 Electron Capture Detector (ECD)

- 5.3.4 Mass-Spectrometry Detector (GC-MS)

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Oil & Gas / Petrochemical Industry

- 5.4.3 Environmental & Waste-water Agencies

- 5.4.4 Food & Beverage Industry

- 5.4.5 Academic & Government Research Institutes

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies

- 6.3.2 Shimadzu Corporation

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Danaher (Cytiva & Pall)

- 6.3.5 PerkinElmer

- 6.3.6 Merck KGaA

- 6.3.7 Waters Corporation

- 6.3.8 Teledyne Technologies

- 6.3.9 Restek Corporation

- 6.3.10 Chromatotec

- 6.3.11 Scion Instruments

- 6.3.12 Sartorius

- 6.3.13 Air Liquide (Extended Life Sciences)

- 6.3.14 Process Sensing Tech (LDetek)

- 6.3.15 Hobre Instruments BV

- 6.3.16 Phenomenex

- 6.3.17 Bruker Corporation

- 6.3.18 LECO Corporation

- 6.3.19 Markes International

- 6.3.20 Falcon Analytical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

微型氣相層析法市場:按組件、技術、應用和最終用戶分類,全球預測,2026-2032年多點氣體檢測櫃市場:依產品類型、氣體類型、應用、終端用戶產業和分銷管道分類,全球預測,2026-2032年按填料類型、結構材料、排放類型、運作模式和應用產業分類的填料塔洗滌器市場,全球預測,2026-2032年

微型氣相層析法市場:按組件、技術、應用和最終用戶分類,全球預測,2026-2032年多點氣體檢測櫃市場:依產品類型、氣體類型、應用、終端用戶產業和分銷管道分類,全球預測,2026-2032年按填料類型、結構材料、排放類型、運作模式和應用產業分類的填料塔洗滌器市場,全球預測,2026-2032年 全球氣相層析法市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球氣相層析法市場規模、佔有率、趨勢和成長分析報告(2026-2034) 氣相層析法市場規模、佔有率及成長分析(按產品、最終用戶及地區分類)-2026-2033年產業預測

氣相層析法市場規模、佔有率及成長分析(按產品、最終用戶及地區分類)-2026-2033年產業預測 氣相層析的全球市場 - 使用趨勢,預測(2025年~2033年)

氣相層析的全球市場 - 使用趨勢,預測(2025年~2033年) 氣相層析市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032

氣相層析市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 亞太地區氣相層析市場預測至 2031 年 - 區域分析 - 依進樣技術、進樣類型、偵測器類型和最終用戶

亞太地區氣相層析市場預測至 2031 年 - 區域分析 - 依進樣技術、進樣類型、偵測器類型和最終用戶 北美氣相層析市場預測至 2031 年 - 區域分析 - 按樣品引入技術、進樣類型、檢測器類型和最終用戶

北美氣相層析市場預測至 2031 年 - 區域分析 - 按樣品引入技術、進樣類型、檢測器類型和最終用戶 歐洲氣相層析市場預測至 2031 年 - 區域分析 - 按樣品引入技術、進樣類型、偵測器類型和最終用戶

歐洲氣相層析市場預測至 2031 年 - 區域分析 - 按樣品引入技術、進樣類型、偵測器類型和最終用戶