|

市場調查報告書

商品編碼

1851076

雲端無線接取網路:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Cloud Radio Access Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

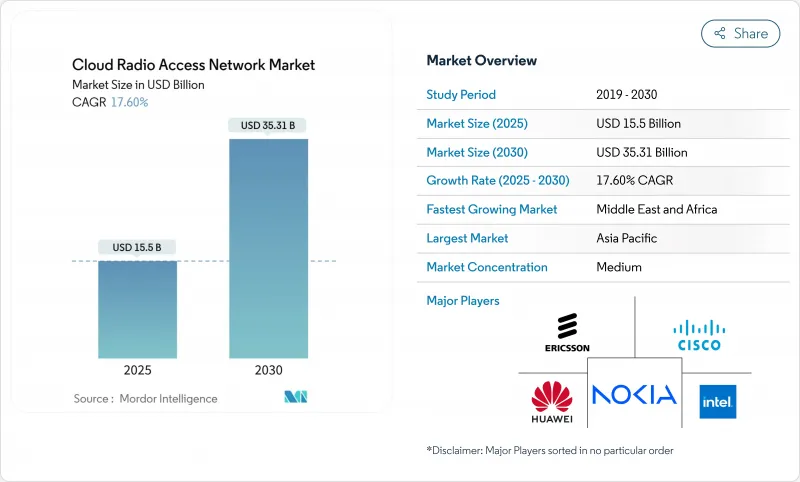

雲端無線接取網路市場規模預計到 2025 年將達到 155 億美元,到 2030 年將達到 353.1 億美元,在預測期(2025-2030 年)內複合年成長率為 17.60%。

5G的快速部署、基頻的日益集中化以及降低網路營運成本的壓力不斷增加,正在推動市場對雲端無線存取網路的持續需求。通訊業者人口密集的城市叢集中開發多層覆蓋策略,透過雲端資源池化來提高行動通訊基地台吞吐量和頻譜利用率。在美國、日本和歐洲主要城市的商業展示表明,人工智慧輔助調度可以降低活躍無線電的功耗,在實現網路現代化的同時,也支持永續性目標。隨著現有供應商競相抵禦以軟體為中心的參與企業,大量聯盟應運而生,這些聯盟融合了無線電、運算和晶片方面的專業知識,以加速產品藍圖的推進。儘管雲端無線接取網路市場受益於政策支持,但它也面臨來自各國頻寬釋放計畫差異巨大以及去程傳輸瓶頸等不利因素。

全球雲端無線接取網路市場趨勢與洞察

5G的快速普及和密集化將推動架構變革

全球通訊業者加速部署中頻段5G網路,並增設小型基地台以填補覆蓋盲點。在此背景下,雲端無線接取網路市場提供了集中式運算資源池,用於管理數千個無線電模組,而無需重複配置硬體。在東京、首爾和紐約進行的現場試驗表明,透過動態調整基頻工作負載,網路利用率提高了30%,尖峰小區吞吐量提高了25%。商用5G獨立網路核心網路現在可以協調虛擬基頻功能和時間敏感型調度,這清楚地展示了雲端原生原則如何縮短功能發布週期。在中國和美國的大規模部署已經證明,在同一雲端站點上託管多代無線電模組的能力,簡化了頻譜重新採購決策,並支援漸進式遷移。這些優勢刺激了持續的投資,尤其是在室內覆蓋要求需要高密度無線網路的情況下。

資本支出和營運支出的節省為該商業案例提供了支持。

虛擬化基頻池的經濟優勢立竿見影。池化減少了硬體重複,降低了房地產成本,並簡化了升級流程。北美一家供應商的案例研究發現,一家業者將三個傳統基頻整合到一個雲端集群中,在一年的部署期間內,資本支出減少了近三分之一。隨著自動化工具能夠更大規模地進行預防性保養和遠端軟體更新,營運支出也隨之降低。人工智慧調度器可在非尖峰時段將負載較低的無線電模組置於深度睡眠模式,從而提高網路能源效率並降低能源成本。這些節省的成本支持了積極的 5G 擴展計劃,對於需要在分紅承諾和提升服務品質之間取得平衡的通訊業者而言尤其重要。隨著公有雲基於消費的定價模式日益普及,通訊業者可以更靈活地根據流量高峰調整支出,這使得雲端架構更具吸引力。

頻譜稀缺和監管限制減緩了發展勢頭。

及時清理和競標中頻段頻譜仍是限制全國5G網路建設的一大因素。美國聯邦通訊委員會(FCC)的競標授權將於2024年到期,這為未來的頻譜釋放帶來了不確定性,並延緩了部分通訊業者的投資週期。許多新興市場也面臨著不透明或受政治因素主導的頻譜分配流程,這導致雲端無線存取網路(Cloud RAN)最佳化的5G網路層的承包部署延遲。即使許可證已經發放,保護頻段條件和功率上限也會限制網路佈局,迫使營運商依賴分散的頻譜資源,從而增加無線規劃的複雜性。這些現實情況可能會減緩部署速度,並推遲頻譜共享經濟效益顯現的時機。

細分市場分析

解決方案市場區隔:到2024年,市場規模將達到113億美元,佔該細分市場收入的73%。然而,隨著多廠商環境逐漸成為主流,服務市場正以18.4%的複合年成長率快速擴張。早期的待開發區部署主要需要硬體和虛擬化基頻許可證,而現今棕地的升級則需要整合、網路最佳化和生命週期支援。歐洲通訊業者正在簽署多年期託管服務協議,將人工智慧主導的效能分析和DevOps賦能相結合,使內部團隊能夠優先考慮新的服務設計。諮詢團隊目前正在指導現有業者進行頻譜重耕、功能分類選擇和遷移順序安排——這些對於平衡傳統4G流量和新興5G私有應用場景的現有業者至關重要。硬體供應商正在透過整合開放介面和參考自動化工作流程來應對這項挑戰,模糊了產品和專業服務之間的界線。隨著2030年的臨近,這種組合將推動雲端無線接取網路市場收入池中服務佔有率的成長。

源源不絕的技術創新使解決方案業務保持活力。晶片巨頭們正在推出用於波束成形和前向糾錯的整合加速技術,與 2023 年的刀片式晶片相比,每個框架單位的基頻容量加倍以上。無線供應商則透過專為屋頂和室內應用量身定做的輕量級大規模 MIMO 陣列來補充這些優勢。這些進步降低了整體擁有成本,同時擴大了潛在客戶群,從而支撐了解決方案業務穩健但持續的收入成長。最終呈現出一幅平衡的編配:軟體、晶片和服務都在共同推動向集中式無線電層的過渡,並擴大現有市場和企業市場領域的應用。

2024年,隨著通訊業者充分利用中頻段頻譜,5G層將佔雲端無線接取網路總收入的61%。通訊業者已迅速轉向獨立組網架構,從而實現切片和超低延遲流水線,這對於工業4.0工作負載至關重要。虛擬化基頻池允許非獨立組網的5G、LTE和NR在通用伺服器上運行,使營運商能夠逐步淘汰3G,轉而進行容量升級。雖然4G LTE仍能帶來可觀的收益,但隨著數據密集型消費者轉向包含補貼設備的5G套餐,其市佔率正逐年下降。

開放式無線接取網路(Open RAN)發展勢頭迅猛,預計到2030年將以27%的複合年成長率成長,這主要得益於北美和亞洲的Tieron等知名企業為實現供應鏈多元化而做出的重大承諾。此模式的開放介面便於實現最佳組合,但整合成本仍然較高。儘管如此,達拉斯和首爾的運作網路試驗表明,透過統一雲端平台編配的多廠商大規模MIMO(大規模MIMO)協議堆疊可以達到與單體系統相媲美的頻譜效率。監管支持,包括美國政府的津貼計劃,也進一步推動了其發展。綜上所述,這些因素共同作用,使開放式無線接取網成為顛覆性創新,在增加供應商多樣性的同時,也加劇了整個市場的競爭動態。

區域分析

亞太地區將在2024年佔據雲端無線接取網路市場的主導地位,營收佔有率將達到39%,並以23.1%的複合年成長率引領成長。中國、日本和韓國積極推進5G部署,依賴與大型區域資料中心相連的高密度小型小型基地台。深圳和首爾的通訊業者已在核心商業區營運商用開放介面叢集,並在尖峰時段展示了用於視訊串流的即時頻譜池化。各國政府正在提供支持性政策框架,包括虛擬化投資的頻譜費用回饋。圍繞著開放測試平台,供應商生態系統正在發展,像OREX這樣的舉措企業正著眼於出口機會,鞏固了該地區的領先地位。

北美地區在收入方面排名第二。美國通訊業者已投入數十億美元,累計在2026年前用開放式無線電技術取代傳統硬體。根據CHIPS計畫和《科學法案》,聯邦政府將共同資助矽晶片研究,以支援基於人工智慧的調度引擎,從而增強美國供應鏈的韌性。拉斯維加斯和西雅圖的初步部署將證明,GPU加速的雲端節點能夠滿足XR遊戲和工業自動化領域嚴格的毫秒延遲目標。加拿大營運商與芬蘭和韓國供應商的合作拓展了該地區的創新空間,並凸顯了支援更廣泛的雲端無線接取網路市場的跨境技術交流。

在歐洲,由於監管趨嚴和競爭的需要,5G部署正在加速。英國、德國和西班牙的通訊業者已部署了首批商用5G開放式無線接取網路(Open RAN)宏基站,並由公共測試實驗室進行認證,確保無線電、基頻和管理系統之間的互通性。歐盟正在資助5G和6G網路的研發,加強無線接取網軟體人才的產學合作。儘管獨立組網(SA)5G覆蓋率仍落後,但現有營運商正在加快無線層雲化的計劃,其主要動機是降低整體擁有成本和加快服務創新。正在進行的基礎設施項目正在透過區域走廊升級光纖骨幹網,消除歷史遺留的瓶頸,並進一步擴大雲端無線接取網路在全部區域的市場部署。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速部署和密集化 5G

- 採用集中式基頻節省資本支出和營運支出

- 行動數據呈指數級成長

- 網路虛擬化和軟體定義網路(SDN)的需求

- 採用人工智慧驅動的無線接取網最佳化技術

- 能源效率法規推動雲端無線存取網發展

- 市場限制

- 頻譜稀缺和監管限制

- 去程傳輸光纖有限和延遲挑戰

- 集中式架構中的安全與隱私風險

- 新興市場投資報酬率不確定

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 專業的

- 管理

- 依網路類型

- 5G

- 4G

- LTE

- 3G(EDGE)

- 按部署模式

- 集中式無線存取網(C-RAN)

- 虛擬化無線存取網(vRAN)

- 開放式無線接取網路(O-RAN)

- 混合雲端無線存取網

- 最終用戶

- 行動網路營運商

- 公司

- 政府/公共

- 中立主機/塔樓服裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 南美洲

- 巴西

- 其他南美洲

- 中東和非洲

- GCC

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Rakuten Symphony

- Altiostar(Rakuten)

- CommScope Holding Co. Inc.

- Casa Systems Inc.

- Airspan Networks Inc.

- Hewlett Packard Enterprise(HPE)

第7章 市場機會與未來展望

The Cloud Radio Access Network Market size is estimated at USD 15.5 billion in 2025, and is expected to reach USD 35.31 billion by 2030, at a CAGR of 17.60% during the forecast period (2025-2030).

Rapid 5G rollouts, the push for centralized baseband processing, and mounting pressure to trim network operating costs keep demand high. Operators are mapping out multi-layer coverage strategies in dense urban clusters, where pooling resources in the cloud has begun lifting cell-site throughput and spectrum utilization. Commercial proofs in the United States, Japan, and leading European capitals also indicate that AI-assisted scheduling can cut power draw across active radios, supporting sustainability targets alongside network modernization. Competition is intensifying as incumbent vendors defend their share against software-centric entrants, prompting a wave of partnerships that combine radio, compute, and silicon expertise to accelerate product road maps. While the cloud radio access network market benefits from supportive policy incentives, it still faces headwinds linked to spectrum release timetables and fronthaul bottlenecks that vary sharply by country.

Global Cloud Radio Access Network Market Trends and Insights

Rapid 5G Rollouts and Densification Drive Architectural Change

Global operators are lighting up mid-band 5G layers and adding small cells to fill coverage gaps. In this environment, the cloud radio access network market delivers the centralized compute pools needed to manage thousands of radios without duplicating hardware. Field trials in Tokyo, Seoul, and New York show that dynamically shifting baseband workloads can raise utilisation by 30% and boost peak cell throughput by 25%. Commercial 5G standalone cores are now coordinating time-sensitive scheduling with virtual baseband functions, underscoring how cloud-native principles shorten feature release cycles. Large-scale deployments in China and the United States reveal that the same cloud site can host multiple radio generations, easing spectrum-refarming decisions and supporting progressive migration paths. These advantages spur continued investment, particularly where indoor coverage obligations require dense radio grids.

CAPEX and OPEX Savings Sustain the Business Case

The economic attraction of virtualized baseband pools is immediate: pooling reduces hardware duplication, trims real-estate expense, and simplifies upgrades. Vendor case studies from North America indicate that operators consolidating three legacy baseband types into a single cloud cluster recorded CAPEX cuts nearing one-third during year-one rollouts. OPEX declines follow as automation tools scale preventive maintenance and remote software updates. Energy bills fall when AI schedulers place lightly loaded radios in deep-sleep modes during off-peak periods, improving the network's power-efficiency profile. These savings underpin aggressive 5G expansion plans, especially for carriers balancing dividend commitments with the need to enhance the quality of service. As consumption-based pricing models for public cloud gain traction, operators gain added flexibility to align spending with traffic peaks, reinforcing the appeal of cloud architecture.

Spectrum Scarcity and Regulatory Limits Dent Momentum

Timely clearance and auction of mid-band spectrum remains a gating factor for nationwide 5G builds. The expiry of auction authority at the United States Federal Communications Commission in 2024 introduced uncertainty around future releases, slowing some carrier investment cycles. Many emerging markets also grapple with opaque or politically driven allocation processes that delay turnkey deployment of 5G layers optimized for cloud RAN. Even where licenses are in place, guard-band conditions and power-level caps can restrict network layouts, forcing operators to rely on fragmented holdings that complicate radio planning. These realities moderate roll-out velocity and can postpone the point when pooling economics become compelling.

Other drivers and restraints analyzed in the detailed report include:

- Exponential Mobile-Data Growth Necessitates Architectural Innovation

- Network Virtualization and SDN Adoption Reshape Strategies

- Limited Fronthaul Fibre and Latency Challenges Constrain Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud radio access network market size derived from Solutions hit USD 11.3 billion in 2024, equal to 73% of segment revenue. Yet the Services market is expanding faster at an 18.4% CAGR as multi-vendor environments become the norm. Early greenfield installations chiefly required hardware and virtualized baseband licenses, but current brownfield upgrades demand integration, network optimization, and lifecycle support. Operators in Europe are signing multi-year managed-service contracts that bundle AI-driven performance analytics with DevOps enablement, letting internal teams prioritise new-service design. Consulting teams now guide spectrum-refarming, functional-split selection, and migration sequencing, roles critical for incumbent carriers balancing legacy 4G traffic and emerging private 5G use cases. Hardware providers respond by embedding open interfaces and reference automation workflows, blurring the line between product and professional service. In turn, this mix pushes the Services slice to account for a deeper share of the cloud radio access network market revenue pool as 2030 approaches.

A steady flow of innovation keeps the Solutions business vibrant. Silicon majors introduced integrated acceleration for beamforming and forward-error correction, lifting baseband capacity per rack unit by over 2X compared with 2023 blades. Radio suppliers complement these gains with lightweight Massive MIMO arrays tailored for rooftop and indoor settings. Such advancements compress the total cost of ownership while widening the addressable customer base, supporting consistent though moderate revenue growth on the Solutions side. The net result is a balanced landscape where software, silicon, and services each reinforce the transition to centrally orchestrated radio layers, widening adoption across incumbent and enterprise segments of the cloud radio access network market.

In 2024, the 5G tier commanded 61% of the overall cloud radio access network market revenue as carriers devoted capital to harness mid-band spectrum. Operators pivoted quickly to standalone architectures, which permit slicing and ultra-low-latency pipelines critical for Industry 4.0 workloads. Virtualized baseband pools make it feasible to run non-standalone 5G, LTE, and NR on common servers, letting carriers phase out 3G in favor of capacity upgrades. While 4G LTE still generates meaningful returns, its share declines each year as data-heavy consumer usage gravitates toward 5G bundles with subsidized devices.

Open RAN exhibits the fastest trajectory at a 27% CAGR through 2030, buoyed by high-profile commitments from North American and Asian tier-ones keen to diversify supply chains. The model's open interfaces encourage best-of-breed combinations, but integration overhead remains considerable. Nevertheless, pilot results from live networks in Dallas and Seoul show that multi-vendor Massive MIMO stacks can reach spectral-efficiency parity with monolithic systems when orchestrated from a unified cloud platform. Regulatory support, such as grant programs from the United States government, offers added momentum. Collectively, these forces position Open RAN as a key disruptor, widening supplier diversity while intensifying competitive dynamics across the cloud radio access network market.

The Cloud Radio Access Network (C-RAN) Market Report is Segmented by Component (Solution and Services), Network Type (5G, 4G, LTE, 3G ), Deployment Model (Centralised RAN [C-RAN], Virtualised RAN [vRAN], Open RAN [O-RAN], and Hybrid Cloud RAN), End User (Mobile Network Operators, Enterprises, Government and Public-Safety, and Neutral Host/TowerCos) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominates the cloud radio access network market with 39% revenue share in 2024 and leads in growth with a 23.1% CAGR. Aggressive 5G rollouts in China, Japan, and South Korea rely on high-density small-cell grids linked to large regional data centres. Operators in Shenzhen and Seoul already operate commercial open-interface clusters in core business districts, showcasing real-time spectrum pooling for video streaming during peak festivals. Governments provide supportive policy frameworks, such as spectrum fee rebates for virtualisation investments. Vendor ecosystems flourish around open testbeds, and joint ventures like the OREX initiative target export opportunities, cementing the region's leadership.

North America ranks second in terms of revenue. United States carriers earmarked multibillion-dollar budgets to swap legacy hardware for open-capable radios by 2026. Federal grants under the CHIPS and Science Act co-fund silicon research that empowers AI-based scheduling engines, giving domestic supply chains greater resilience. Early deployments in Las Vegas and Seattle prove that GPU-accelerated cloud nodes can meet stringent millisecond-level latency targets for XR gaming and industrial automation. Canadian operator collaborations with Finnish and Korean vendors extend the regional innovation sphere, highlighting cross-border technology exchange that supports the wider cloud radio access network market.

Europe accelerates adoption through a blend of regulatory mandates and competitive necessity. Operators in the United Kingdom, Germany, and Spain rolled out the first commercial 5G Open RAN macro sites, supported by public test labs that certify interoperability among radios, basebands, and management systems. The European Union dedicates funding tranches to 5G and 6G network R&D, which bolsters an academic-industry pipeline for RAN software talent. Despite lagging standalone 5G coverage, incumbents pursue fast-track plans to cloudify their radio layers, citing lower total cost of ownership and faster service innovation as key motivators. Ongoing infrastructure programs upgrade fibre backbones through rural corridors, which will remove a historic bottleneck and further expand the cloud radio access network market footprint across the region.

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Rakuten Symphony

- Altiostar (Rakuten)

- CommScope Holding Co. Inc.

- Casa Systems Inc.

- Airspan Networks Inc.

- Hewlett Packard Enterprise (HPE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G rollout and densification

- 4.2.2 CAPEX-OPEX savings via centralized baseband

- 4.2.3 Exponential mobile-data growth

- 4.2.4 Network virtualization and SDN demand

- 4.2.5 AI-driven RAN optimisation adoption

- 4.2.6 Energy-efficiency regulations push cloud RAN

- 4.3 Market Restraints

- 4.3.1 Spectrum scarcity and regulatory limits

- 4.3.2 Limited fronthaul fibre and latency challenges

- 4.3.3 Security and privacy risks in centralised architecture

- 4.3.4 Uncertain ROI in emerging markets

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Professional

- 5.1.2.2 Managed

- 5.2 By Network Type

- 5.2.1 5G

- 5.2.2 4G

- 5.2.3 LTE

- 5.2.4 3G (EDGE)

- 5.3 By Deployment Model

- 5.3.1 Centralised RAN (C-RAN)

- 5.3.2 Virtualised RAN (vRAN)

- 5.3.3 Open RAN (O-RAN)

- 5.3.4 Hybrid Cloud RAN

- 5.4 By End User

- 5.4.1 Mobile Network Operators

- 5.4.2 Enterprises

- 5.4.3 Government and Public-Safety

- 5.4.4 Neutral Host/TowerCos

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co. Ltd.

- 6.4.2 Nokia Corporation

- 6.4.3 Telefonaktiebolaget LM Ericsson

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 ZTE Corporation

- 6.4.7 Intel Corporation

- 6.4.8 Fujitsu Limited

- 6.4.9 NEC Corporation

- 6.4.10 Mavenir Systems Inc.

- 6.4.11 Parallel Wireless Inc.

- 6.4.12 Rakuten Symphony

- 6.4.13 Altiostar (Rakuten)

- 6.4.14 CommScope Holding Co. Inc.

- 6.4.15 Casa Systems Inc.

- 6.4.16 Airspan Networks Inc.

- 6.4.17 Hewlett Packard Enterprise (HPE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

雲端無線存取網市場:按組件、部署類型和最終用戶分類-2026-2032年全球市場預測

雲端無線存取網市場:按組件、部署類型和最終用戶分類-2026-2032年全球市場預測 雲端無線接取網路(C-RAN) 市場分析及至 2035 年預測:類型、產品、服務、技術、元件、應用、部署、最終用戶、功能

雲端無線接取網路(C-RAN) 市場分析及至 2035 年預測:類型、產品、服務、技術、元件、應用、部署、最終用戶、功能 2026年全球雲端無線接取網路市場報告

2026年全球雲端無線接取網路市場報告 全球雲端無線接取網路(C-RAN)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球雲端無線接取網路(C-RAN)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球宏蜂窩無線電單元/主動天線單元 (RU/AAU) 市場分析與預測 (2024-2029) (第七版)全球雲端無線存取網 (C-RAN) 市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測 (2026-2034)

全球宏蜂窩無線電單元/主動天線單元 (RU/AAU) 市場分析與預測 (2024-2029) (第七版)全球雲端無線存取網 (C-RAN) 市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測 (2026-2034) 全球雲端無線接取網路市場,2026-2030年

全球雲端無線接取網路市場,2026-2030年 雲端無線接取網路(C-RAN) 市場規模、佔有率和成長分析(按元件、網路類型、架構類型、最終用戶和地區分類)-2026-2033 年產業預測全球雲端無線接取網路市場規模(按技術、網路類型、部署區域、區域範圍和預測)

雲端無線接取網路(C-RAN) 市場規模、佔有率和成長分析(按元件、網路類型、架構類型、最終用戶和地區分類)-2026-2033 年產業預測全球雲端無線接取網路市場規模(按技術、網路類型、部署區域、區域範圍和預測) C-RAN 市場規模、佔有率、趨勢分析報告:按元件、按網路類型、按架構類型、按部署模型、按地區、按細分市場、預測,2025-2030 年

C-RAN 市場規模、佔有率、趨勢分析報告:按元件、按網路類型、按架構類型、按部署模型、按地區、按細分市場、預測,2025-2030 年