|

市場調查報告書

商品編碼

1851047

室內無線網路:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)In Building Wireless - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

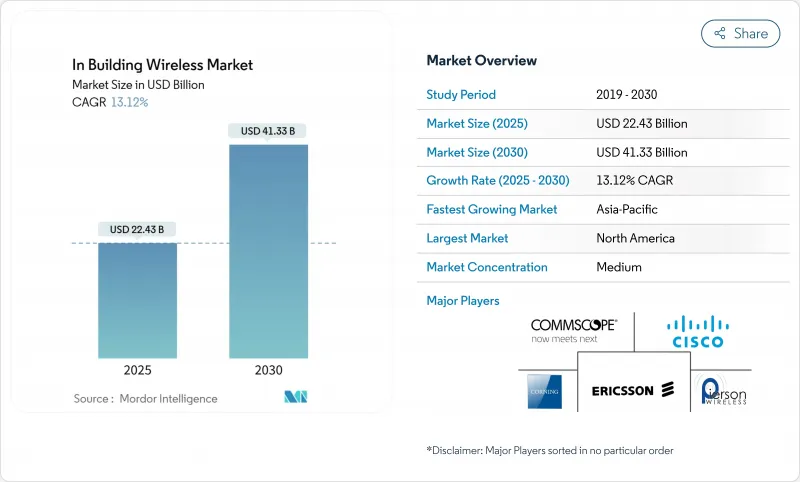

預計到 2025 年,室內無線市場規模將達到 224.3 億美元,到 2030 年將達到 413.3 億美元,預測期(2025-2030 年)的複合年成長率為 13.12%。

對始終線上室內連接的持續需求、向5G建築的轉型以及日益成長的智慧設施要求,正在推動這一趨勢。企業目前正投資於以蜂窩網路為先導的架構,將室內覆蓋視為核心基礎設施,並將專用5G與下一代Wi-Fi相結合,以確保應用程式的執行時間。供應鏈成本上漲推高了部署成本,但中立的主機設計和基於人工智慧的最佳化降低了生命週期成本,部分抵消了成本壓力。隨著設備製造商尋求涵蓋無線電、傳輸和雲端管理層的端到端解決方案組合,供應商整合正在重塑室內無線市場格局。

全球室內無線市場趨勢與洞察

室內行動數據消耗增加

目前,約 80% 的行動流量發生在建築物內,隨著視訊、AR 培訓和高密度物聯網工作負載的激增,傳統 Wi-Fi 不堪負荷。像 Tractor Supply 這樣的零售連鎖店在 2000 多家門市部署了 5G 網路,因為 Wi-Fi 無法支援即時庫存和客戶管理應用。在醫療保健領域,一家兒童醫院安裝了 900 個三頻接入點 (AP),以確保遠端醫療和診斷影像流量的安全,同時不影響患者。視訊協作和邊緣分析工作負載的成長正在推動室內無線市場的需求成長,並增強其收入前景。

5G頻譜分配用於室內

監管機構正在預留專用室內頻譜,從一開始就將企業網路設計從室外到室內的疊加網路轉向專用蜂巢網路。在美國,CBRS競標為3.5GHz頻段的企業和場館部署分配了46億美元的許可證,其中僅一家一級營運商就花費了18.9億美元。歐洲在6GHz頻段發放了480-500MHz的許可證,為體育場館、機場、大學等場所提供了關鍵的320MHz寬頻道。中國移動累計4.16億美元用於在300個城市部署5G-Advanced,以加速大規模工廠自動化。這些頻譜分配確保了頻譜的長期穩定性,提振了室內無線市場的信心和資本投資意願。

資料隱私和網路安全問題

企業仍然謹慎地將業務流量暴露給更廣泛的蜂窩網路生態系統。 GDPR合規性提高了歐洲對位置追蹤功能的審查力度,並延長了智慧辦公室計劃的採購週期。由於患者資料透過同一無線介面傳輸,醫療保健機構在批准新無線電設備之前,要求其具備受保護的管理框架和高級加密功能。在美國,針對不安全設備的「拆除並更換」規則雖然增加了意外的更換成本,但最終加強了核准無線市場的安全態勢。

細分市場分析

分散式天線系統(DAS)預計在2024年將佔總收入的38%,透過深度滲透到體育場館、機場和A級辦公大樓等場所,為室內無線市場提供支援。同時,私有5G小型基地台正以13.89%的複合年成長率成長,這標誌著企業正朝著可自主擁有和控制的敏捷蜂巢式網路轉型。光纖和同軸電纜價格的上漲促使整合商更傾向於採用主動DAS和小型基地台架構,以最大限度地減少佈線並方便遠端軟體升級。

天線創新目前優先發展多頻段、多營運商設計,將Wi-Fi和蜂窩網路覆蓋整合於單一外形規格中,從而減少屋頂空間佔用。隨著小型基地台叢集提供不受射頻噪聲影響的強大上行鏈路,中繼器的使用正在減少。供應商整合,例如安費諾以21億美元收購康普的行動業務資產,透過捆綁電纜、連接器和無線電組件簡化了採購流程。隨著對中立主機需求的成長,能夠同時承載公共和私有網路切片的單一骨幹網路基礎設施可能會重塑室內無線市場的資本配置模式。

到2024年,4G/LTE將維持65%的市場佔有率,這得益於其成熟的設備生態系統以及在語音和數據方面久經考驗的可靠性。然而,5G NR將以14.67%的複合年成長率快速成長,這主要得益於工業自動化計劃對10毫秒或更低確定性延遲的需求。 Wi-Fi 6E也在不斷發展,而Wi-Fi 7引入了320 MHz頻道、多鏈路操作和4K-QAM調製,為企業提供了一條無需蜂窩網路即可實現超高吞吐量的路徑。

融合5G和Wi-Fi 7的混合部署正成為醫院、智慧工廠和高等院校的參考架構。製造廠利用5G技術驅動行動機器人和安全關鍵型遙測,而Wi-Fi則負責平板電腦和筆記型電腦的大量資料傳輸。中國的5G-Advanced部署證明了該技術適用於室內寬頻,從而推動了有源DAS和小型基地台供應商對組件的需求。隨著每張新的私人執照的發放,室內無線市場正不斷深化從營運商主導向企業主導的網路轉型。

室內無線市場報告按組件類型(天線、分散式天線系統、電纜、中繼器、小型基地台)、技術(4G/LTE、5G NR、Wi-Fi 6/6E、Wi-Fi 7)、頻段(1 GHz 以下、1-6 GHz、6 GHz 以上)、最終用戶產業(商業、住宅、工業、公共/政府)和地區進行細分。

區域分析

北美在2024年引領室內無線市場,佔據34%的收入佔有率,這主要得益於CBRS頻譜自由化和FirstNet對公共的80億美元投資,該投資將用於建設1000個新的行動通訊基地台。美國企業採用中立主機架構來鞏固與通訊業者的關係,並實現未來建立專用網路的目標。多家廠商推出Wi-Fi 7,加快了產品更新換代速度,而加拿大和墨西哥則利用其汽車和航太叢集的優勢,為在工廠部署專用蜂巢式網路提供了合理的依據。

到2030年,亞太地區的複合年成長率將達到14.60%。中國目前已擁有440萬個5G基地台,隨著製造業和物流的數位化,預計在預測期內將超過450萬個。日本的許可製度支持智慧工廠中6G以下頻段和毫米波混合網路,韓國則為半導體工廠的園區網路提供國家獎勵。印度的電子製造業受益於天線在地化合作項目,這些項目降低了進口成本並縮短了部署前置作業時間。

歐洲正穩步推進5G技術的應用,這主要得益於資料隱私和建築排放法規的日益嚴格。 6GHz頻譜的分配正在擴大高密度場所的Wi-Fi容量,法國城市也正在展示專用5G網路在市政攝影機回程傳輸鏈路的成本優勢。德國、英國和法國的企業引領5G技術的普及,而中東的製造商則在試行專用5G網路以支援工業4.0的發展。嚴格的GDPR合規要求正促使買家轉向本地核心網路和安全設備ID框架,從而在室內無線市場形成以安全為先的策略。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 室內行動數據消費量增加

- 室內5G頻率分配

- 對不間斷業務連結的需求日益成長

- 智慧建築中Gigabit級Wi-Fi將成為標配

- 低功耗、中立託管的分散式天線系統 (DAS) 助力企業實現淨零排放目標

- 一個利用店內客流量分析數據來實現獲利的零售媒體網路

- 市場限制

- 資料隱私和網路安全問題

- 多營運商分散式天線系統安裝需要高額資本投入

- CBRS/私有5G整合所需熟練勞工短缺

- 遺產建築的無線電波穿透規則

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 依組件類型

- 天線

- 分散式天線系統(有源DAS、無源DAS)

- 電纜(同軸電纜、光纖)

- 中繼器

- 小型基地台(毫微微基地台、微微型基地台、微細胞)

- 透過技術

- 4G/LTE

- 5G NR

- Wi-Fi 6/6E

- Wi-Fi 7

- 按頻寬

- 低於 1GHz(低頻段)

- 1-6 GHz(中頻段,含 CBRS)

- 6GHz以上(毫米波)

- 按最終用戶行業分類

- 商業的

- 辦公室

- 零售

- 衛生保健

- 飯店業

- 住宅

- MDU

- 獨立式住宅

- 工業的

- 製造業

- 倉儲業

- 石油和天然氣

- 公共與政府

- 商業的

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CommScope Holding Co.

- Cisco Systems Inc.

- Corning Inc.

- Ericsson AB

- Nokia Corp.

- ATandT Inc.

- Verizon Communications Inc.

- Pierson Wireless Corp.

- Cobham PLC

- Cambium Networks

- TE Connectivity Ltd.

- Dali Wireless Inc.

- Airspan Networks

- American Tower Corp.

- Boingo Wireless Inc.

- Extreme Networks Inc.

- Juniper Networks Inc.

- HPE(Aruba Networks)

- Samsung Electronics(Co. Networks)

- Huawei Technologies Co. Ltd.

第7章 市場機會與未來展望

The In Building Wireless Market size is estimated at USD 22.43 billion in 2025, and is expected to reach USD 41.33 billion by 2030, at a CAGR of 13.12% during the forecast period (2025-2030).

Sustained demand for always-available indoor connectivity, the transition to 5G-ready buildings, and rising smart-facility mandates are driving this momentum. Enterprises now treat indoor coverage as core infrastructure, investing in cellular-first architectures that pair private 5G with next-generation Wi-Fi to guarantee application uptime. Supply-chain inflation has nudged deployment costs higher, yet cost pressures are partially offset by neutral-host designs and AI-based optimisation that lower life-cycle expenses. Vendor consolidation is reshaping the In-Building Wireless market as equipment makers pursue end-to-end solution portfolios capable of spanning radio, transport, and cloud management layers.

Global In Building Wireless Market Trends and Insights

Rising mobile-data consumption indoors

Roughly 80% of all mobile traffic now originates inside buildings, overwhelming legacy Wi-Fi whenever video, AR training, or high-density IoT workloads spike. Retail chains such as Tractor Supply adopted 5G across more than 2,000 outlets after Wi-Fi could not support real-time inventory and customer-engagement applications. In healthcare, a single children's hospital installed 900 tri-radio APs to safeguard tele-medicine and imaging traffic without patient disruption, underscoring the capacity gap that indoor 5G plus Wi-Fi 6E is filling. Growing video collaboration and edge analytics workloads will intensify the demand curve, reinforcing the revenue outlook for the In-Building Wireless market.

5G spectrum allocations for indoor use

Regulators are carving out dedicated indoor spectrum, shifting enterprise design from outdoor-to-indoor overlay to private cellular from day one. In the United States, the CBRS auction channelled USD 4.6 billion into 3.5 GHz licences aimed at enterprise and venue deployments, with one Tier-1 carrier alone spending USD 1.89 billion. Europe authorised 480-500 MHz in the 6 GHz band, enabling 320 MHz-wide channels critical for stadiums, airports, and universities. China Mobile earmarked USD 416 million for 5G-Advanced rollouts across 300 cities to accelerate factory automation at scale. Such allocations ensure long-term spectrum certainty, lifting confidence and capex commitment across the In-Building Wireless market.

Data-privacy and cybersecurity concerns

Enterprises remain cautious about exposing operational traffic to broader cellular ecosystems. GDPR compliance elevates scrutiny of location-tracking functions in Europe, prolonging procurement cycles for smart-office projects. Healthcare providers mandate Protected Management Frames and advanced encryption before approving new radios because patient data moves over the same air interface. The US "rip-and-replace" rules for insecure equipment add unexpected swap-out costs but ultimately harden the security posture of the In-Building Wireless market.

Other drivers and restraints analyzed in the detailed report include:

- Demand for uninterrupted enterprise connectivity

- Smart-building mandates for gigabit Wi-Fi

- High capex of multi-operator DAS deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Distributed Antenna Systems held 38% of 2024 revenue, anchoring the In-Building Wireless market through deep penetration in stadiums, airports, and Class-A offices. Private-5G small cells, however, are advancing at a 13.89% CAGR, signaling a pivot toward agile cellular networks that enterprises can own and manage. Rising fibre and coax prices push integrators to favour active DAS or small-cell architectures that minimise cabling runs and facilitate remote software upgrades.

Antenna innovation now prioritises multi-band, multi-operator designs that collapse Wi-Fi and cellular coverage into one form factor, trimming roof-space requirements. Repeater use is declining as small-cell clusters deliver stronger uplinks without RF noise penalties. Vendor consolidation, illustrated by Amphenol's USD 2.1 billion acquisition of CommScope's mobility assets, bundles cabling, connectors, and radio components to streamline procurement. As neutral-host demand grows, single backbone infrastructures capable of carrying public and private slices simultaneously will reshape capital-allocation patterns across the In-Building Wireless market.

4G/LTE retained 65% share in 2024, underpinned by a mature device ecosystem and proven stability for voice and data. Yet 5G NR is expanding at a 14.67% CAGR, driven by industrial automation projects that need deterministic latency below 10 ms. Wi-Fi 6E is also scaling, but Wi-Fi 7 introduces 320 MHz channels, multi-link operation, and 4K-QAM, giving enterprises a non-cellular path to ultra-high throughput.

Hybrid deployments blending 5G and Wi-Fi 7 are emerging as the reference architecture in hospitals, smart factories, and higher-education campuses. Manufacturing plants use 5G for mobile robotics and safety-critical telemetry, while Wi-Fi handles bulk data offload for tablets and laptops. China's 5G-Advanced roll-out validates the technology's readiness for indoor broadband, fuelling component demand from active DAS and small-cell vendors. With each additional private licence granted, the In-Building Wireless market deepens its shift from operator-led to enterprise-controlled networks.

The in Building Wireless Market Report is Segmented by Component Type (Antenna, Distributed Antenna Systems, Cables, Repeaters, and Small Cells), Technology (4G/LTE, 5G NR, Wi-Fi 6/6E, and Wi-Fi 7), Frequency Band (Less Than 1 GHz, 1 - 6 GHz, and More Than 6 GHz), End-User Industry (Commercial, Residential, Industrial, and Public-Safety and Government), and Geography.

Geography Analysis

North America led the In-Building Wireless market with 34% revenue share in 2024, aided by CBRS spectrum liberalisation and FirstNet's USD 8 billion public-safety investment that funded 1,000 new cell sites. Enterprises in the United States adopt neutral-host architectures to consolidate carrier relationships and future-proof private-network ambitions. Wi-Fi 7 launches from multiple vendors accelerate refresh cycles, while Canada and Mexico leverage their automotive and aerospace clusters to justify private cellular rollouts inside plants.

Asia-Pacific is expanding at a 14.60% CAGR to 2030. China already hosts 4.4 million 5G base stations and plans to exceed 4.5 million within the forecast horizon as it digitalises manufacturing and logistics. Japan's licence regime supports sub-6 and mmWave hybrids in smart factories, and South Korea channels state incentives into campus networks at semiconductor fabs. India's electronic-manufacturing drive is supported by antenna localisation partnerships that trim import costs and shorten deployment lead times.

Europe shows steady uptake influenced by regulatory stringency around data privacy and building emissions. The 6 GHz allocation enlarges Wi-Fi capacity for dense venues, and French cities demonstrate the cost advantage of private 5G for municipal camera backhaul. German, British, and French enterprises lead adoption, while Central-Eastern manufacturers pilot private 5G to support Industry 4.0. Strict GDPR compliance requirements nudge buyers toward on-premises core networks and secure device-identity frameworks, shaping a security-first approach within the In-Building Wireless market.

- CommScope Holding Co.

- Cisco Systems Inc.

- Corning Inc.

- Ericsson AB

- Nokia Corp.

- ATandT Inc.

- Verizon Communications Inc.

- Pierson Wireless Corp.

- Cobham PLC

- Cambium Networks

- TE Connectivity Ltd.

- Dali Wireless Inc.

- Airspan Networks

- American Tower Corp.

- Boingo Wireless Inc.

- Extreme Networks Inc.

- Juniper Networks Inc.

- HPE (Aruba Networks)

- Samsung Electronics (Co. Networks)

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising mobile data consumption indoors

- 4.2.2 5G spectrum allocations for indoor use

- 4.2.3 Growing demand for uninterrupted enterprise connectivity

- 4.2.4 Smart-building mandates for gigabit-grade Wi-Fi

- 4.2.5 Corporate net-zero targets driving low-power neutral-host DAS

- 4.2.6 Retail media networks monetising in-store footfall analytics

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 High capex of multi-operator DAS deployments

- 4.3.3 Skilled-labour shortage for CBRS/Private-5G integration

- 4.3.4 Radio-frequency transparency rules in heritage buildings

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component Type

- 5.1.1 Antenna

- 5.1.2 Distributed Antenna Systems (Active DAS, Passive DAS)

- 5.1.3 Cables (Coax, Fiber)

- 5.1.4 Repeaters

- 5.1.5 Small Cells (Femtocell, Picocell, Microcell)

- 5.2 By Technology

- 5.2.1 4G/LTE

- 5.2.2 5G NR

- 5.2.3 Wi-Fi 6/6E

- 5.2.4 Wi-Fi 7

- 5.3 By Frequency Band

- 5.3.1 Less than 1 GHz (Low-band)

- 5.3.2 1 - 6 GHz (Mid-band incl. CBRS)

- 5.3.3 More than 6 GHz (mmWave)

- 5.4 By End-user Industry

- 5.4.1 Commercial

- 5.4.1.1 Offices

- 5.4.1.2 Retail

- 5.4.1.3 Healthcare

- 5.4.1.4 Hospitality

- 5.4.2 Residential

- 5.4.2.1 MDU

- 5.4.2.2 Single-family

- 5.4.3 Industrial

- 5.4.3.1 Manufacturing

- 5.4.3.2 Warehousing

- 5.4.3.3 Oil and Gas

- 5.4.4 Public-Safety and Government

- 5.4.1 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CommScope Holding Co.

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Corning Inc.

- 6.4.4 Ericsson AB

- 6.4.5 Nokia Corp.

- 6.4.6 ATandT Inc.

- 6.4.7 Verizon Communications Inc.

- 6.4.8 Pierson Wireless Corp.

- 6.4.9 Cobham PLC

- 6.4.10 Cambium Networks

- 6.4.11 TE Connectivity Ltd.

- 6.4.12 Dali Wireless Inc.

- 6.4.13 Airspan Networks

- 6.4.14 American Tower Corp.

- 6.4.15 Boingo Wireless Inc.

- 6.4.16 Extreme Networks Inc.

- 6.4.17 Juniper Networks Inc.

- 6.4.18 HPE (Aruba Networks)

- 6.4.19 Samsung Electronics (Co. Networks)

- 6.4.20 Huawei Technologies Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

室內無線市場:按組件、系統類型、技術和應用分類-2026年至2032年全球市場預測

室內無線市場:按組件、系統類型、技術和應用分類-2026年至2032年全球市場預測 2026年全球室內無線市場報告

2026年全球室內無線市場報告 室內無線市場:依組件、應用、部署模式、技術、最終用戶、國家及地區分類-全球市場分析、市場規模、市場佔有率及2026年至2033年預測

室內無線市場:依組件、應用、部署模式、技術、最終用戶、國家及地區分類-全球市場分析、市場規模、市場佔有率及2026年至2033年預測 室內無線市場規模、佔有率和成長分析(按組件、系統類型、技術、部署類型、最終用戶產業和地區分類)-2026-2033年產業預測無線演示與協作系統市場:按組件類型、部署類型、連接技術、組織規模和最終用戶行業分類 - 全球預測(2026-2032 年)室內蜂窩系統無線 BMS 解決方案市場(按組件、拓撲、電池類型、連接性和應用)- 2025-2030 年全球預測

室內無線市場規模、佔有率和成長分析(按組件、系統類型、技術、部署類型、最終用戶產業和地區分類)-2026-2033年產業預測無線演示與協作系統市場:按組件類型、部署類型、連接技術、組織規模和最終用戶行業分類 - 全球預測(2026-2032 年)室內蜂窩系統無線 BMS 解決方案市場(按組件、拓撲、電池類型、連接性和應用)- 2025-2030 年全球預測 室內無線市場:全球按產品、技術、經營模式、建築規模、網路類型、最終用戶和地區分類 - 預測至 2030 年

室內無線市場:全球按產品、技術、經營模式、建築規模、網路類型、最終用戶和地區分類 - 預測至 2030 年 無線簡報解決方案市場按技術、經營模式、安裝類型和最終用戶行業分類的室內覆蓋市場 - 2025 年至 2030 年全球預測

無線簡報解決方案市場按技術、經營模式、安裝類型和最終用戶行業分類的室內覆蓋市場 - 2025 年至 2030 年全球預測