|

市場調查報告書

商品編碼

1851035

自助式商業智慧:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Self-service BI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

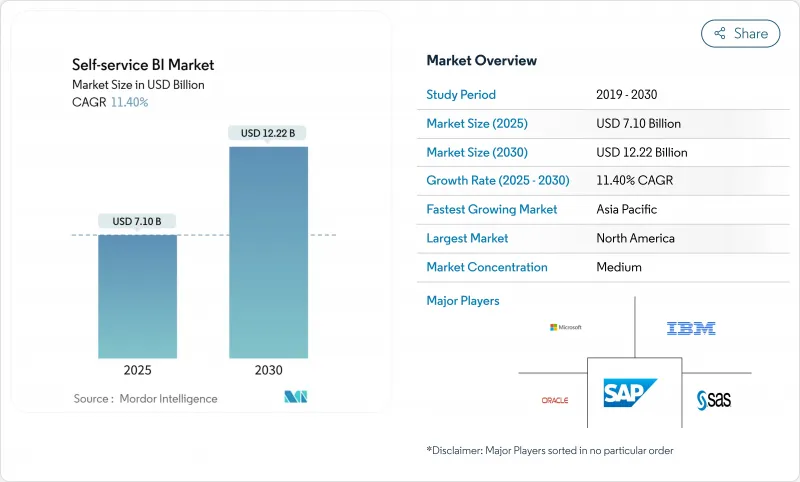

預計到 2025 年,自助式 BI 市場價值將達到 71 億美元,到 2030 年將達到 122.2 億美元,複合年成長率為 11.47%。

企業正在擴展低程式碼分析,整合生成式人工智慧,並將工作負載遷移到雲端資料倉儲,以縮短洞察週期,並讓IT人員騰出時間從事策略性工作。北美公司在採用這些技術方面處於領先地位,因為它們已經證明,直覺的工具可以將彙報積壓減少約三分之一。但隨著亞太地區雲端基礎設施的成熟,亞太地區的公司正迅速迎頭趕上。供應商正競相整合自然語言查詢以支援多語言環境,這項功能已經引起了歐洲用戶的興趣。同時,監管壓力和影子IT事件促使人們更加關注管治,從而推動了買家對兼具開放架構和自動化控制的平台的需求。

全球自助式商業智慧市場趨勢與洞察

利用低程式碼/無程式碼工具實現分析民主化

低程式碼介面使業務人員無需依賴開發人員即可建立儀表板,這種轉變在北美最為顯著。隨著非專業資料科學家將他們的領域知識與簡化的工具結合,挖掘出傳統 BI 團隊經常忽略的模式,分析任務的效率提高了 74%。將民主化與強大的語義層結合的公司正在減少積壓工作的交接,並在工作時間內交付洞察,這仍然是一項至關重要的舉措。這種文化轉變正在擴展平台評估標準,從功能豐富性轉向非技術人員的易用性,推動平台圍繞直覺的拖放式創作和應用內指導進行整合。

雲端基礎的資料倉儲日益普及,加速了自助式服務的採用。

亞太地區的企業正透過消除限制 BI 並發性的瓶頸並將資料遷移到雲端,實現跨越式發展。雲端資料倉儲細分市場的複合年成長率高達 27.64%,使分析團隊能夠查詢新資料而無需排隊等待作業,並將報告時間縮短多達 40%。將自助式部署與資料倉儲現代化結合的企業,其洞察速度可比孤立的部署方式快三倍。這些資料倉儲內建的集中式管治也提高了資料質量,並確保了跨部門指標的一致性。

未受管理的可見性工具所帶來的影子 IT 風險

使用核准的工具會導致關鍵績效指標 (KPI) 不一致,並洩露敏感資料集,不合規的公司平均每次事件損失 103 萬美元。行銷和財務部門經常違規,因為他們會透過快速迭代繞過 IT 部門。同類最佳公司實施目錄主導的管治、自動化資料沿襲和基於角色的存取控制,以在保持敏捷性的同時降低風險,其採用率比全面封鎖方法高出 45%。

細分市場分析

軟體仍是主要的收入促進因素,但服務收入正以15.2%的複合年成長率加速成長。將平台購買與培訓計畫結合的組織,其採用率比僅購買工具的組織高出45%。市場需求正轉向持續的賦能訂閱服務,涵蓋資料素養提升和管治審核。因此,實施專家正在打包行業特定的操作手冊,並將儀表板與行業關鍵績效指標 (KPI) 相匹配,以加快價值實現速度。預計到2030年,自助式商業智慧 (BI) 即服務市場規模將達到32億美元,反映出市場對人工專業知識和自動化技術的持續需求。

同時,軟體供應商優先考慮人工智慧功能的對等性,透過增加自然語言查詢(NLQ)、自動化洞察和嵌入式模式來保持競爭力。持續的更新促使企業傾向於模組化架構,這種架構允許他們在不破壞語義層的情況下更換分析引擎。這種方法可以緩解對供應商鎖定的擔憂,並支援隨著人工智慧能力的成熟而不斷發展的混合工具環境。

雲端採用在用戶數量和發展勢頭方面均佔據主導地位,目前佔收入的 73%,用戶數量正以 13.5% 的複合年成長率成長。規模經濟使中型企業無需資本支出即可部署企業級分析,從而與大型企業站在了同一起跑線上。此外,分散式團隊現在能夠在共用工作空間中即時協作,並加快回饋循環。安全態勢也不斷提升,靜態資料加密、私人連結和區域資料中心現在已通過大多數監管機構的審核,從而緩解了先前對公有雲的擔憂。

在資料駐留要求嚴格的監管產業中,本地部署解決方案依然佔據主導地位。然而,即便在這些產業,混合架構也十分常見,敏感資料表保留在本地,而聚合模型則同步到雲端以供更廣泛使用。預計在預測期內,隨著超大規模資料中心將商業智慧 (BI) 與儲存和人工智慧 (AI) 服務緊密整合,它們將佔據超過 80% 的雲端自助式 BI 市場佔有率。

自助式商業智慧市場按組件(軟體和服務)、部署模式(雲端/按需和本地部署)、應用(銷售和行銷管理、客戶參與和分析、詐欺和安全管理等)、最終用戶行業(銀行、金融服務和保險、醫療保健、製造業等)、組織規模(大型企業和中小企業)以及地區進行細分。市場預測以美元計價。

區域分析

北美地區佔據自助式商業智慧市場42%的佔有率,這主要得益於低程式碼平台的早期應用以及主要供應商的存在。金融服務和醫療保健機構正在將自然語言查詢融入日常工作流程,並擁有成熟的管治方案,以增強用戶參與度並遏制影子IT事件。研發投資的重點在於提升人工智慧的可解釋性,使系統能夠在法規環境下為推薦結果提供合理的依據。儘管跨境數據共用規則仍然是觀點,但該地區先進的雲端基礎設施持續吸引許多創新分析新興企業,這些公司正在不斷擴展其平台生態系統。

亞太地區是成長最快的區域,複合年成長率達13.77%。中國、印度、日本和澳洲的需求強勁,國內雲端巨頭和超大規模資料中心業者大規模企業紛紛投資資料中心。該地區的中小型企業正利用行動優先分析來應對桌面電腦短缺的問題,智慧型手機儀錶板已成為許多第一線員工的主要互動介面。資料管治人才短缺問題依然存在,促使各國政府和學術機構推出認證項目,以期從2027年起緩解這一難題。日本和韓國的製造業正在加速採用預測性維護技術,這與工業4.0藍圖相符。同時,新加坡等金融中心正優先發展客戶分析,以提升其在亞太地區的銀行服務競爭力。

在歐洲,嚴格的資料隱私法正在推動雲端技術的穩定普及。企業透過選擇支援精細化授權管理和本地資料處理的平台,在實現民主化的同時兼顧GDPR合規性。多語言自然語言介面尤其受到重視,先導計畫顯示,非技術人員的參與度提高了50%。隨著監管機構明確加密和本地容錯移轉符合主權要求,西歐的雲端遷移正在加速。東歐正迅速追趕,數位轉型資金正湧入波蘭、羅馬尼亞和捷克共和國。零售業和離散製造業佔據了大部分需求,但開放原始碼替代方案正受到那些擔心被專有軟體鎖定的機構的青睞。

南美洲和中東/非洲地區仍處於起步階段,但展現出巨大潛力。巴西和墨西哥在拉丁美洲引領商業智慧(BI)的普及,主要得益於通訊業者和銀行尋求即時客戶視圖的需求。在中東,波灣合作理事會成員國政府走在投資前沿,利用商業智慧來支持其多元化發展策略和智慧城市舉措。非洲的普及程度較為分散,南非在企業應用方面處於領先地位,而奈及利亞和肯亞則憑藉其金融科技生態系統正在迅速發展。在桌上型電腦普及率較低的地區,行動儀錶板正在彌補基礎設施的不足。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在北美利用低程式碼/無程式碼工具實現分析民主化

- 亞太地區雲端基礎資料倉儲的激增將推動自助服務模式的普及。

- 在歐洲整合生成式人工智慧以進行自然語言查詢

- 銀行、金融服務和零售業對SaaS供應商提供的嵌入式分析的需求

- 中型企業的數據素養培訓計畫正在興起。

- 日益嚴格的資料駐留合規法規推動在地化商業智慧平台(中東和非洲)的發展

- 市場限制

- 不受控制的資料視覺化工具造成的影子IT風險

- 新興國家資料管治人才短缺

- 從傳統 BI 系統遷移到自助服務堆疊的成本很高。

- 由於專有語義層而導致的供應商鎖定問題令人擔憂

- 價值/供應鏈分析

- 技術展望

- 監理展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按部署模式

- 雲端/按需

- 本地部署

- 透過使用

- 銷售和行銷管理

- 客戶參與與分析

- 詐欺和安全控制

- 預測性資產保全

- 風險與合規管理

- 供應鏈與採購

- 營運管理

- 按最終用戶行業分類

- BFSI

- 零售與電子商務

- 衛生保健

- 製造業

- 通訊

- 媒體與娛樂

- 運輸與物流

- 能源與公共產業

- 政府和國防部

- 按組織規模

- 主要企業

- 中小企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- SAP SE

- Salesforce(Tableau)

- Qlik Tech Intl.

- IBM Corporation

- Oracle Corporation

- SAS Institute

- MicroStrategy Inc.

- TIBCO Software

- Zoho Corporation(Analytics)

- Amazon Web Services(QuickSight)

- Google LLC(Looker)

- Domo Inc.

- Sisense Inc.

- ThoughtSpot Inc.

- Pyramid Analytics

- Yellowfin BI

- GoodData Corp.

- Board International

- Infor(Birst)

- Alibaba Cloud(Quick BI)

- Dundas Data Visualization

- SentryOne(BI Sentry)

- Phocas Software

第7章 市場機會與未來展望

The self-service BI market size is estimated at USD 7.10 billion in 2025 and is forecast to reach USD 12.22 billion by 2030, reflecting an 11.47% CAGR.

Firms are scaling low-code analytics, embedding generative AI, and shifting workloads to cloud data warehouses, which shortens insight cycles and frees IT staff for strategic work. North American organizations lead adoption after proving that intuitive tools can cut reporting backlogs by roughly one-third, while Asia-Pacific businesses are catching up fast as cloud infrastructure matures. Vendors are racing to integrate natural-language querying that supports multilingual environments, a capability already boosting engagement among European users. Meanwhile, heightened attention to governance, driven by regulatory pressure and shadow-IT incidents, is steering purchasing toward platforms that pair open architectures with automated control features.

Global Self-service BI Market Trends and Insights

Democratization of analytics via low-code/no-code tools

Low-code interfaces let business professionals create dashboards without relying on developers, a shift most visible in North America where 80% of executives credit wider data access for faster decisions. Productivity for analytical tasks has risen 74% as citizen data scientists pair domain knowledge with simplified tooling, unearthing patterns traditional BI teams often overlook. Companies that married democratization with robust semantic layers cut backlog hand-offs and delivered insight within the operational window where actions still matter. This cultural change is expanding platform evaluation criteria from feature depth to the ease of onboarding non-technical staff, driving platform consolidation around intuitive drag-and-drop authoring and in-app guidance.

Surge in cloud-based data warehouses accelerating self-service adoption

Asia-Pacific organizations are leapfrogging legacy stacks by landing data in the cloud, eliminating bottlenecks that once restricted BI concurrency. With the cloud warehouse segment itself climbing at 27.64% CAGR, analytics teams now query fresh data without queuing jobs, shrinking report time by as much as 40%. Firms that align self-service rollouts with warehouse modernization gain triple-speed time-to-insight compared with siloed deployments. Centralized governance baked into these warehouses also raises data quality, enabling consistent metrics across departments.

Shadow-IT risks from uncontrolled visualization tools

Unvetted tool adoption has generated conflicting KPIs and exposed sensitive datasets, costing non-compliant firms USD 1.03 million on average per incident. Marketing and finance units are frequent offenders because rapid iterations tempt them to sidestep IT. Best-in-class enterprises deploy catalog-driven governance, automated lineage, and role-based access that preserve agility yet curb risk, yielding 45% higher adoption than blanket lockdown approaches.

Other drivers and restraints analyzed in the detailed report include:

- Integration of generative AI for natural-language querying

- Embedded analytics demand from SaaS vendors

- Shortage of data-governance talent in emerging economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment continues to anchor revenue, yet services revenue is compounding faster at 15.2% CAGR. Organizations that pair platform purchases with training programs report adoption rates 45% higher than tool-only buyers. Demand is shifting toward continuous enablement subscriptions that cover data-literacy upskilling and governance audits. As a result, implementation specialists are packaging industry-specific playbooks, aligning dashboards with vertical KPIs, and expediting time-to-value. The self-service BI market size for services is projected to reach USD 3.2 billion by 2030, reflecting sustained appetite for human expertise alongside automation.

Software vendors, meanwhile, prioritize AI feature parity, adding NLQ, automated insights, and embedded modes to remain competitive. The relentless update cadence pushes enterprises to favor modular architectures that let them swap analytic engines without ripping out semantic layers. This posture mitigates vendor lock-in concerns and supports mixed-tool environments that evolve as AI capabilities mature.

Cloud deployments own both usage and momentum, commanding 73% of current revenue and adding users at a 13.5% CAGR. Economies of scale let mid-market firms implement enterprise-grade analytics without capital outlay, leveling the playing field with larger peers. Moreover, distributed teams can collaborate on shared workspaces in real time, accelerating feedback loops. Security postures have evolved; encryption-at-rest, private links, and regional data centers now satisfy most regulatory audits, tempering earlier reservations about public cloud.

On-premises solutions persist in heavily regulated verticals where data residency is mandatory. Yet even there, hybrid designs are common: sensitive tables stay onsite while aggregated models sync to the cloud for broad exploration. Over the forecast period, the self-service BI market share for cloud is expected to edge past 80% as hyperscalers integrate BI tightly with their storage and AI services.

Self Service BI Market is Segmented by Component (Software and Services), Deployment Model (Cloud / On-Demand and On-Premises), Application (Sales and Marketing Management, Customer Engagement and Analysis, Fraud and Security Management and More), End-User Industry (BFSI, Healthcare, Manufacturing and More), Organization Size ( Large Enterprises and SMEs), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 42% of self-service BI market revenue, buoyed by early adoption of low-code platforms and the presence of leading vendors. Financial services and healthcare providers there embed natural-language querying in day-to-day workflows, keeping user sentiment high and shadow-IT incidents under control through mature governance programs. R&D investments focus on advanced AI explainability, preparing systems to justify recommendations in regulated settings. Cross-border data-sharing rules remain a watchpoint, yet the region's sophisticated cloud infrastructure continues to attract innovative analytics startups that expand platform ecosystems.

Asia-Pacific is the fastest growing territory, advancing at a 13.77% CAGR. China, India, Japan, and Australia demonstrate vigorous demand as domestic cloud giants and hyperscalers alike pour capital into data centers. SMEs in the region use mobile-first analytics to overcome desktop scarcity, with smartphone dashboards becoming the primary interface for many field employees. Talent shortages in data governance persist, prompting governments and academia to launch certification programs that should ease constraints after 2027. Manufacturing adoption is strong in Japan and South Korea, where predictive maintenance aligns with Industry 4.0 roadmaps, while financial hubs like Singapore emphasize customer analytics to differentiate regional banking services.

Europe shows steady uptake shaped by strict privacy statutes. Organizations balance democratization with GDPR compliance by opting for platforms that support fine-grained consent management and local data processing. Multilingual natural-language interfaces are especially valued, lifting engagement among non-technical staff by 50% in pilot projects. Western European cloud migration is accelerating after regulators clarified that encryption and local failover meet sovereignty requirements. Eastern Europe is catching up quickly as digital transformation funding flows into Poland, Romania, and the Czech Republic. Retail and discrete manufacturing dominate demand, though open-source alternatives gain traction in institutions wary of proprietary lock-in.

South America, the Middle East, and Africa remain early-stage yet promising. Brazil and Mexico head Latin American adoption, with telecom operators and banks seeking real-time customer views. Gulf Cooperation Council governments anchor investment in the Middle East, leveraging BI to support diversification agendas and smart-city initiatives. African uptake is fragmented; South Africa leads enterprise deployments, while Nigeria and Kenya show momentum through fintech ecosystems. Across these regions, cloud solutions enjoy preference owing to limited legacy estates, and mobile dashboards bridge infrastructure gaps in areas where desktop penetration is low.

- Microsoft Corporation

- SAP SE

- Salesforce (Tableau)

- Qlik Tech Intl.

- IBM Corporation

- Oracle Corporation

- SAS Institute

- MicroStrategy Inc.

- TIBCO Software

- Zoho Corporation (Analytics)

- Amazon Web Services (QuickSight)

- Google LLC (Looker)

- Domo Inc.

- Sisense Inc.

- ThoughtSpot Inc.

- Pyramid Analytics

- Yellowfin BI

- GoodData Corp.

- Board International

- Infor (Birst)

- Alibaba Cloud (Quick BI)

- Dundas Data Visualization

- SentryOne (BI Sentry)

- Phocas Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Democratization of Analytics via Low-code/No-code Tools in North America

- 4.2.2 Surge in Cloud-based Data Warehouses Accelerating Self-service Adoption in APAC

- 4.2.3 Integration of Generative AI for Natural-Language Querying in Europe

- 4.2.4 Embedded Analytics Demand from SaaS Vendors in BFSI & Retail

- 4.2.5 Rising Data-Literacy Programs Among Mid-Sized Enterprises

- 4.2.6 Regulatory Push for Data-Residency Compliance Driving Localized BI Platforms (MEA)

- 4.3 Market Restraints

- 4.3.1 Shadow-IT Risks from Uncontrolled Data Visualization Tools

- 4.3.2 Shortage of Data Governance Talent in Emerging Economies

- 4.3.3 High Migration Cost from Legacy BI to Self-service Stacks

- 4.3.4 Vendor Lock-in Concerns with Proprietary Semantic Layers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud / On-Demand

- 5.2.2 On-Premises

- 5.3 By Application

- 5.3.1 Sales and Marketing Management

- 5.3.2 Customer Engagement and Analysis

- 5.3.3 Fraud and Security Management

- 5.3.4 Predictive Asset Maintenance

- 5.3.5 Risk and Compliance Management

- 5.3.6 Supply Chain and Procurement

- 5.3.7 Operations Management

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Retail and E-commerce

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Telecommunications

- 5.4.6 Media and Entertainment

- 5.4.7 Transportation and Logistics

- 5.4.8 Energy and Utilities

- 5.4.9 Government and Defense

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium-sized Enterprises (SMEs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 SAP SE

- 6.4.3 Salesforce (Tableau)

- 6.4.4 Qlik Tech Intl.

- 6.4.5 IBM Corporation

- 6.4.6 Oracle Corporation

- 6.4.7 SAS Institute

- 6.4.8 MicroStrategy Inc.

- 6.4.9 TIBCO Software

- 6.4.10 Zoho Corporation (Analytics)

- 6.4.11 Amazon Web Services (QuickSight)

- 6.4.12 Google LLC (Looker)

- 6.4.13 Domo Inc.

- 6.4.14 Sisense Inc.

- 6.4.15 ThoughtSpot Inc.

- 6.4.16 Pyramid Analytics

- 6.4.17 Yellowfin BI

- 6.4.18 GoodData Corp.

- 6.4.19 Board International

- 6.4.20 Infor (Birst)

- 6.4.21 Alibaba Cloud (Quick BI)

- 6.4.22 Dundas Data Visualization

- 6.4.23 SentryOne (BI Sentry)

- 6.4.24 Phocas Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

自助式 BI 市場報告:按組件、部署模式、應用、產業和地區分類(2026-2034 年)

自助式 BI 市場報告:按組件、部署模式、應用、產業和地區分類(2026-2034 年) 自助式 BI 市場規模、佔有率和成長分析:按組件、部署類型、企業規模、應用、最終用戶行業、用戶類型和地區分類——2026-2033 年行業預測

自助式 BI 市場規模、佔有率和成長分析:按組件、部署類型、企業規模、應用、最終用戶行業、用戶類型和地區分類——2026-2033 年行業預測 2026年全球自助式商業智慧市場報告

2026年全球自助式商業智慧市場報告 全球自助式商業智慧 (BI) 市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測 (2026-2034)

全球自助式商業智慧 (BI) 市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測 (2026-2034) 全球自助服務 BI 市場規模研究與預測(依部署、企業類型、產業和區域分類)2025 年至 2035 年預測2024 年至 2031 年自助式 BI 市場(按地區)

全球自助服務 BI 市場規模研究與預測(依部署、企業類型、產業和區域分類)2025 年至 2035 年預測2024 年至 2031 年自助式 BI 市場(按地區)