|

市場調查報告書

商品編碼

1851034

OTT( Over-the-Top):市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Over The Top (OTT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

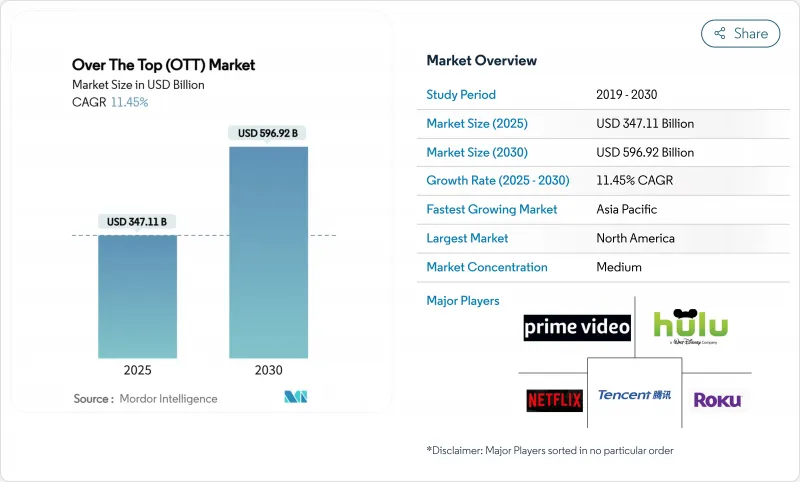

預計到 2025 年,OTT 市場規模將達到 3,471.1 億美元,到 2030 年將達到 5,969.2 億美元。

這是因為不斷增強的網路連線、裝置普及和廣告遷移持續推動線上影片成為全球娛樂的中心。

成長動能取決於寬頻升級,它將全高清和4K串流帶入主流家庭,而智慧型手機的普及則增加了人們在通勤和休息時間的觀看時長。廣告主受到精準定位和效果指標的吸引,正在重新分配傳統電視預算,並擴大跨平台收入派餅。競爭對手的崛起推動了將體育賽事直播、優質劇集和用戶原創視訊整合到單一介面的服務的發展,這既提高了用戶的期望,也實現了盈利模式的多元化。現有廣播公司正在加速推出直接面對消費者(DTC)的服務,利用其豐富的節目庫,有效地消除了傳統電視和串流媒體之間的歷史隔閡。同時,介面在地化、配音和字幕等措施正在悄悄提升用戶留存率,讓內容更具文化共鳴。

全球OTT(Over-the-Top)市場趨勢與洞察

通訊業者和OTT捆綁套餐:新興市場成長的關鍵

行動電話商與串流媒體服務供應商的合作正在透過將娛樂內容捆綁到預付數據包中來拓展OTT市場,從而降低雙方的獲客成本。印尼Telkomsel與Catchplay+的合作利用了4G網路的廣泛覆蓋,繞過了固網覆蓋範圍有限的問題,擴大了串流媒體服務的初始滲透率,同時增加了通訊業者的數據使用量。行動儲值套餐的整合定價降低了用戶流失率,並將交易數據回饋給建議,使其能夠快速適應本地用戶的偏好。通訊業者的收入增加彌補了語音傳輸利潤率下降的局面,而平台則在價格敏感型用戶群中實現了快速成長。

體育版權價格上漲:重塑高階經濟

NBA與ESPN、NBC環球和亞馬遜簽署的為期11年、價值760億美元的媒體協議,凸顯了實況活動日益成長的戰略價值。像ESPN、FOX和華納兄弟探索頻道這樣的合資企業,既能擴展業務範圍,又能分散風險。不斷攀升的估值也帶動了人們對區域性和小眾體育賽事的興趣,這些賽事即使在較低的版權溢價下也能保持觀眾群,從而在不損害利潤的情況下實現內容豐富的播出安排。分級提供的賽季通行證、按次付費和旗艦套餐,既能滿足鐵桿粉絲的需求,又能為普通觀眾提供豐富的節目選擇。

內容獲取成本:盈利的挑戰

激烈的競標戰正在擠壓淨利率,尤其是對中型遊戲開發商而言。如今,遊戲工作室在評估計劃,包括系列潛力、周邊產品潛力以及跨平台遊戲玩法,以確保首發串流媒體播放之外的持續收益。他們也會利用人工智慧驅動的需求預測,在開發初期就辨識出反響不佳的項目,進而降低沉沒成本風險。投資者越來越重視營運利潤率而非用戶數量,這促使經營團隊在資本配置方面更加謹慎。

細分市場分析

到2024年,AVOD和FAST將佔OTT市場規模的13%。預計到2030年,該細分市場將以13.4%的複合年成長率成長,顯著高於OTT市場的整體成長速度。 Netflix的廣告層級在推出的第一年就吸引了大量新訂閱用戶。改進後的指標將增強廣告主的信心,並提高廣告填充率,從而為更廣泛的原創內容提供資金,同時又不影響高階SVOD套餐的獲利。該平台受益於雙重收入來源:廣告提高了每位用戶平均收入,而訂閱則確保了基礎收入。同時,FAST頻道透過將其龐大的內容庫重新剪輯成精簡的線性節目,降低了內容攤銷成本,這種節目形式更能吸引那些已經養成固定頻道觀看習慣的用戶。

隨著新興市場用戶可支配收入有限,純訂閱模式難以普及,AVOD模式的持續成長對整個OTT產業至關重要。 AVOD模式的成熟將推動用戶群的拓展,尤其是在新興市場,其用戶群規模不斷擴大。隨著混合獲利模式的日趨成熟,分層式的入門級服務模式將會出現,包括面向普通用戶的免費廣告支援模式、預算有限用戶的折扣廣告支援精簡版模式,以及針對追求極致便利的家庭用戶的無廣告高級版模式。預計廣告支援串流媒體將以13.4%的速度成長,未來將在內容投資中佔據更大佔有率,並在競爭中扮演越來越重要的套件。

區域分析

北美地區將佔2024年總收入的37%,這主要得益於寬頻普及和用戶逐漸形成的「剪線族」習慣。如今,成長的驅動力更多來自平均每用戶收入(ARPU)的提升,而非新增用戶的成長,這促使平台推出密碼共用額外費用、價格上漲以及配套服務,以提升用戶感知價值。合資企業面臨美國反壟斷審查,這可能會延緩大型併購案的發生,但內容授權將得到戰術性加強,從而在共用生態系統中維護各個品牌的獨立性。來自NFL、NBA和MLB等體育賽事的轉播權費用確保了平台的持續穩健發展,儘管利潤率壓力不斷增加,需要拓展多元化的收入來源,例如商品行銷和電影票房。

2025年至2030年間,亞太地區將以10.3%的複合年成長率成為成長最快的地區,智慧型手機的普及和低成本資料通訊的增加將推動用戶觀看時長的成長。印度本土平台JioCinema和騰訊投資的WeTV等正在建構以本地語言和微支付選項為基礎的介面,以加深不同收入群體的用戶參與度。國際巨頭將推出針對特定地區的原創節目,通常採用短季或單元劇的形式。通訊業者、儲值卡套餐和現金券將有助於縮小信用卡普及率差距,並擴大潛在用戶群。

到2024年,拉丁美洲和中東及非洲地區的總收入將佔全球OTT市場收入的不到15%,但隨著宏觀經濟經濟狀況趨於穩定,年輕人口步入消費年齡,這些地區仍有龐大的成長空間。像Televisa和MBC這樣的區域性廣播公司將透過混合型AVOD模式對其傳統內容庫進行現代化改造,從而將廣告商的資金留在國內市場生態系統內。涵蓋行動錢包、現金充值和通訊業者計費等支付創新將進一步擴大覆蓋範圍。隨著光纖和5G部署的加速推進,這些地區預計在未來十年內顯著提升其對全球OTT市場收費的貢獻。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 通訊業者與OTT捆綁夥伴關係加速了南亞和東南亞低ARPU用戶成長

- 創紀錄的體育賽事直播版權價格上漲推高了北美和歐洲D2C OTT服務的溢價。

- 聯網電視廣告需求的轉變推動了美國和英國AVOD和FAST的收入成長

- 政府對國產產品含量設定配額(例如歐盟的30%規則)會刺激對本地原創產品的消費。

- 市場限制

- 內容獲取成本不斷上漲,削弱了成熟的SVOD市場的盈利。

- 北美訂閱疊加模式的高解約率

- 產業生態系分析

- 監理展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 影響OTT和電視產業的宏觀經濟因素

第5章 市場規模與成長預測

- 按服務類型

- SVOD

- AVOD

- TVOD

- 混合模式(訂閱+廣告)

- 按設備平台

- 智慧型手機和平板電腦

- 智慧連網電視

- 筆記型電腦和桌上型電腦

- 串流媒體播放器

- 其他

- 按內容類型

- 娛樂與電影

- 運動的

- 新聞資訊

- 教學與學習

- 其他(紀錄片、真人秀)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- Netflix Inc.

- Google LLC(YouTube)

- Amazon.com Inc.(Prime Video)

- The Walt Disney Company(Disney+& Hulu)

- Tencent Holdings Ltd(Tencent Video)

- Apple Inc.(Apple TV+)

- Warner Bros. Discovery(Max)

- Comcast Corp.(Peacock)

- Paramount Global(Paramount+)

- DAZN Group Ltd.

- Roku Inc.

- PCCW Media Group(Viu)

- Baidu Inc.(iQIYI)

- Alibaba Pictures(Youku Tudou)

- Zee Entertainment(ZEE5)

- Viacom18 Media(JioCinema)

- MBC Group(Shahid)

- Canal+Group(myCanal)

- Rakuten Group(Rakuten TV)

- NHK World-Japan

第7章 市場機會與未來展望

The OTT market size is estimated at USD 347.11 billion in 2025 and is projected to reach USD 596.92 billion by 2030, expanding at an 11.45% CAGR as richer connectivity, device proliferation, and escalating advertising migration keep propelling online video toward the core of global entertainment.

Growth momentum rests on broadband upgrades that bring full-HD and 4K streaming to mainstream households, while ubiquitous smartphones unlock incremental viewing hours during commutes and breaks. Advertisers, lured by addressable targeting and outcome-based metrics, are re-allocating linear TV budgets, widening the overall revenue pie for platforms. Heightened rivalries are pushing services to combine live sports, premium scripted franchises, and user-generated clips in a single interface, simultaneously raising customer expectations and diversifying monetization. Established broadcasters are accelerating direct-to-consumer (DTC) launches that leverage deep program libraries, effectively erasing the historical wall between linear and streaming, while localization of interfaces, dubbing, and subtitles quietly improves retention by making content culturally resonant.

Global Over The Top (OTT) Market Trends and Insights

Telco-OTT Bundling: Unlocking Growth in Emerging Markets

Partnerships between mobile operators and streaming providers are widening the OTT market by embedding entertainment in prepaid data packs, lowering acquisition costs for both parties. Telkomsel's alliance with Catchplay+ in Indonesia taps ubiquitous 4G coverage to bypass limited fixed-line reach, expanding first-time streamer penetration while boosting data usage for the carrier. Integrated pricing within mobile top-ups reduces involuntary churn and feeds transaction insights into recommendation engines that quickly adapt to local tastes. Operators benefit from incremental revenue that cushions shrinking voice margins, while platforms gain swift scale among price-sensitive users.

Sports Rights Inflation: Reshaping Premium Economics

The NBA's 11-year USD 76 billion media pact with ESPN, NBCUniversal, and Amazon signposts the growing strategic value of live events. Expensive rights forge a defensive moat that few services can finance alone, spurring joint ventures such as the ESPN-FOX-Warner Bros. Discovery consortium to spread risk yet maintain portfolio breadth. Rising valuations intensify interest in regional or niche sports whose rights carry lower premiums but still retain audiences, thereby filling content calendars without denting margins. Tiered offers-season passes, pay-per-view, and bundled flagship tiers-monetize superfans while preserving broader packages for casual viewers.

Content Acquisition Costs: The Profitability Challenge

Escalating bidding wars for marquee titles have compressed margins, especially for mid-scale players. Studios now enforce stricter green-light criteria that rate projects on franchise potential, merchandise viability, and cross-platform game adaptations, ensuring returns extend beyond first-window streaming. Shorter exclusivity periods allow second-window syndication that offsets cash burn, while AI-driven demand forecasts trim sunk-cost risk by flagging low-resonance concepts earlier in development. Investors increasingly focus on blended operating margins rather than raw subscriber adds, nudging management to favor disciplined capital allocation.

Other drivers and restraints analyzed in the detailed report include:

- AVOD and FAST Growth: Advertising's Streaming Renaissance

- Content Quotas: Regulatory Catalysts for Local Production

- Subscription Stacking: The Churn Challenge

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AVOD and FAST constituted 13% of the OTT market size in 2024. This cohort is forecast to rise at 13.4% CAGR through 2030, notably faster than the overall OTT market path, as inflation pressures heighten price sensitivity while advertisers chase addressable audiences. Netflix's ad tier captured a sizable slice of new sign-ups within its debut year . Enhanced measurement standards raise advertiser confidence, driving higher fill rates that fund broader original slates without eroding premium SVOD bundles. Platforms benefit from a dual revenue stream in which advertising uplifts average revenue per user while subscriptions secure base income. In parallel, FAST channels recycle deep libraries into lean, linear-style programming that appeals to habitual channel surfers, helping reduce content amortization costs.

Continued AVOD traction proves decisive for the broader OTT industry because it widens the accessible user base in emerging markets where disposable income constrains pure subscription adoption. As hybrid monetization matures, tiered entry points emerge: free-with-ads for casual viewers, discounted ad-lite models for budget watchers, and premium ad-free tiers for households demanding maximal convenience. Given its 13.4% forecast cadence, ad-supported streaming is positioned to shoulder a larger share of future content investments, reinforcing its importance in the competitive toolkit.

The OTT Market is Segmented by Service Type (SVOD, AVOD, TVOD, Hybrid (Subscription + Ads)), Device Platform (Smartphones and Tablets, Smart and Connected TVs, Laptops and Desktops, Streaming Media Players, and More), Content Genre (Entertainment and Movies, Sports, News and Information, Education and Learning, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 37% of 2024 revenue, benefiting from near-universal broadband and entrenched cord-cutting habits. Growth now hinges more on ARPU lifts than fresh subscriber gains, pushing platforms to introduce password-sharing surcharges, price rises, and bundled offerings that stretch perceived value. Joint ventures face U.S. antitrust scrutiny that may slow mega-mergers but tactically tighten content licensing, preserving individual brand identities even within shared ecosystems. Robust sports rights expenditures-NFL, NBA, MLB-ensure continued stickiness, though they heighten margin pressures that necessitate diversified income streams such as merchandising or theatrical windows.

Asia-Pacific posts the fastest regional CAGR at 10.3% for 2025-2030 as smartphone affordability and low-cost data unlock incremental viewing hours. Indigenous platforms like India's JioCinema and Tencent-backed WeTV craft interfaces around local languages and micro-payment options, deepening engagement across varied income brackets. International giants respond with region-specific originals-short seasons, anthology formats-that fit local budgets yet carry global export potential. Telco partnerships, bundled prepaid plans, and cash vouchers mitigate credit-card penetration gaps, broadening the bankable audience.

Latin America and the Middle East & Africa together accounted for under 15% of 2024 revenue but present meaningful headroom as macroeconomic conditions stabilize and young populations enter consumption age. Regional broadcasters such as Televisa and MBC modernize legacy libraries through hybrid AVOD models that keep advertiser funds within domestic ecosystems. Payment innovation spanning mobile wallets, cash top-ups, and telco billing further expands reach. As fiber and 5G deployments gain momentum, these regions could stretch their contribution to global OTT market revenue in the next decade.

- Netflix Inc.

- Google LLC (YouTube)

- Amazon.com Inc. (Prime Video)

- The Walt Disney Company (Disney+ & Hulu)

- Tencent Holdings Ltd (Tencent Video)

- Apple Inc. (Apple TV+)

- Warner Bros. Discovery (Max)

- Comcast Corp. (Peacock)

- Paramount Global (Paramount+)

- DAZN Group Ltd.

- Roku Inc.

- PCCW Media Group (Viu)

- Baidu Inc. (iQIYI)

- Alibaba Pictures (Youku Tudou)

- Zee Entertainment (ZEE5)

- Viacom18 Media (JioCinema)

- MBC Group (Shahid)

- Canal+ Group (myCanal)

- Rakuten Group (Rakuten TV)

- NHK World-Japan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Bundled telco-OTT partnerships accelerating low-ARPU subscriber uptake in South & Southeast Asia

- 4.2.2 Record live-sports media rights inflation driving premium pricing for D2C OTT in North America & Europe

- 4.2.3 Connected-TV advertising demand shift fueling AVOD & FAST revenue growth in US & UK

- 4.2.4 Government domestic-content quotas (EU 30% rule, etc.) stimulating local originals spend

- 4.3 Market Restraints

- 4.3.1 Escalating content-acquisition costs eroding profitability in mature SVOD markets

- 4.3.2 High churn amid subscription stacking in North America

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macro-Economic Factors on the OTT and TV Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 SVOD

- 5.1.2 AVOD

- 5.1.3 TVOD

- 5.1.4 Hybrid (Subscription + Ads)

- 5.2 By Device Platform

- 5.2.1 Smartphones and Tablets

- 5.2.2 Smart and Connected TVs

- 5.2.3 Laptops and Desktops

- 5.2.4 Streaming Media Players

- 5.2.5 Others

- 5.3 By Content Genre

- 5.3.1 Entertainment and Movies

- 5.3.2 Sports

- 5.3.3 News and Information

- 5.3.4 Education and Learning

- 5.3.5 Others (Documentary, Reality)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Netflix Inc.

- 6.3.2 Google LLC (YouTube)

- 6.3.3 Amazon.com Inc. (Prime Video)

- 6.3.4 The Walt Disney Company (Disney+ & Hulu)

- 6.3.5 Tencent Holdings Ltd (Tencent Video)

- 6.3.6 Apple Inc. (Apple TV+)

- 6.3.7 Warner Bros. Discovery (Max)

- 6.3.8 Comcast Corp. (Peacock)

- 6.3.9 Paramount Global (Paramount+)

- 6.3.10 DAZN Group Ltd.

- 6.3.11 Roku Inc.

- 6.3.12 PCCW Media Group (Viu)

- 6.3.13 Baidu Inc. (iQIYI)

- 6.3.14 Alibaba Pictures (Youku Tudou)

- 6.3.15 Zee Entertainment (ZEE5)

- 6.3.16 Viacom18 Media (JioCinema)

- 6.3.17 MBC Group (Shahid)

- 6.3.18 Canal+ Group (myCanal)

- 6.3.19 Rakuten Group (Rakuten TV)

- 6.3.20 NHK World-Japan

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

OTT設備和服務市場按設備類型、服務類型、內容類型、收益來源和最終用戶分類-2025-2032年全球預測Over-the-Top通訊市場(按內容、設備類型、服務類型、應用和產業)預測 2025-2032

OTT設備和服務市場按設備類型、服務類型、內容類型、收益來源和最終用戶分類-2025-2032年全球預測Over-the-Top通訊市場(按內容、設備類型、服務類型、應用和產業)預測 2025-2032 2025年OTT設備與服務全球市場報告2025年全球OTT串流媒體市場報告

2025年OTT設備與服務全球市場報告2025年全球OTT串流媒體市場報告 OTT媒體服務的全球市場

OTT媒體服務的全球市場 2025 年至 2033 年按組件、平台類型、部署類型、內容類型、收入模式、服務類型、垂直行業和地區分類的 Over-Top 市場報告Over-the-Top設備和服務市場規模、佔有率和趨勢分析報告:按類型、設備、服務類型、OTT經營模式、平台、地區和細分市場進行預測全球OTT內容市場2025 年至 2033 年日本 Over the Top 市場報告(按組件、平台類型、部署類型、內容類型、收入模式、垂直行業和地區分類)

2025 年至 2033 年按組件、平台類型、部署類型、內容類型、收入模式、服務類型、垂直行業和地區分類的 Over-Top 市場報告Over-the-Top設備和服務市場規模、佔有率和趨勢分析報告:按類型、設備、服務類型、OTT經營模式、平台、地區和細分市場進行預測全球OTT內容市場2025 年至 2033 年日本 Over the Top 市場報告(按組件、平台類型、部署類型、內容類型、收入模式、垂直行業和地區分類) 全球Over-the-Top(OTT)服務市場:市場規模、佔有率、趨勢分析(按平台、收益模式、服務區域、類型、串流媒體設備和地區)、展望和未來預測(2025-2032 年)

全球Over-the-Top(OTT)服務市場:市場規模、佔有率、趨勢分析(按平台、收益模式、服務區域、類型、串流媒體設備和地區)、展望和未來預測(2025-2032 年)